East Asia Today

In today's daily: China monetary developments, Japan CPI, Korea PPI, highlights of the BOJ meeting, and a link to my latest podcast. From today, I am taking a couple of weeks off. Thanks for your interest this year, I hope you've found the content useful. Happy Christmas, and best wishes for 2026.

If you aren't yet a subscriber, please consider becoming one! This daily product is designed for individuals, but we also have data services and a much more comprehensive offering for financial institutions.

If you have any questions, or feedback on what would be useful to you, please get in touch with me directly.

Thematic – what investors need to know about East Asia. I was very happy to do this podcast with friends at Alpine Macro, where we touched on China property, Japans's fiscal policy and the JPY, the chip super-cycle in Korea and Taiwan, and demographics. It was a fun conversation.

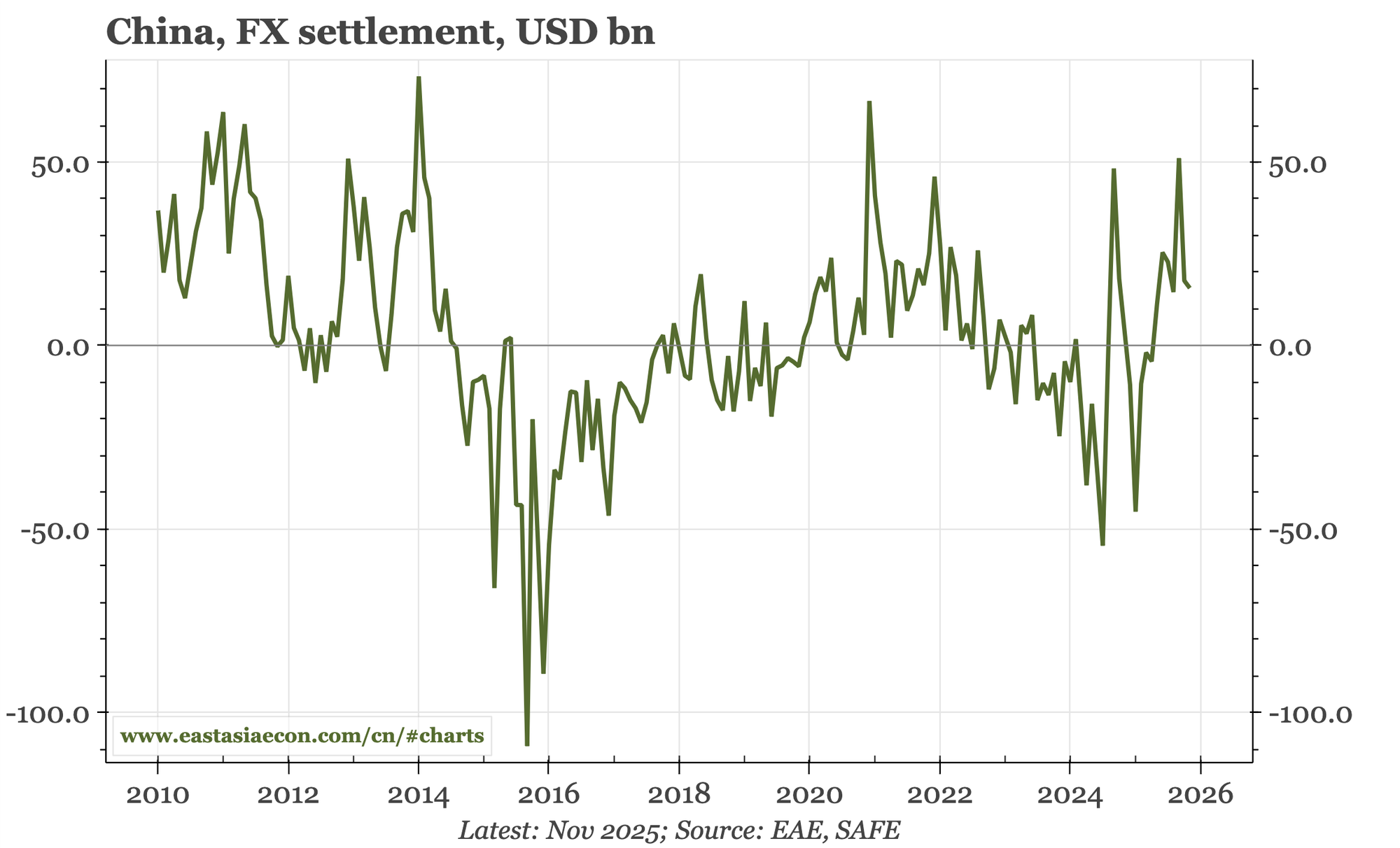

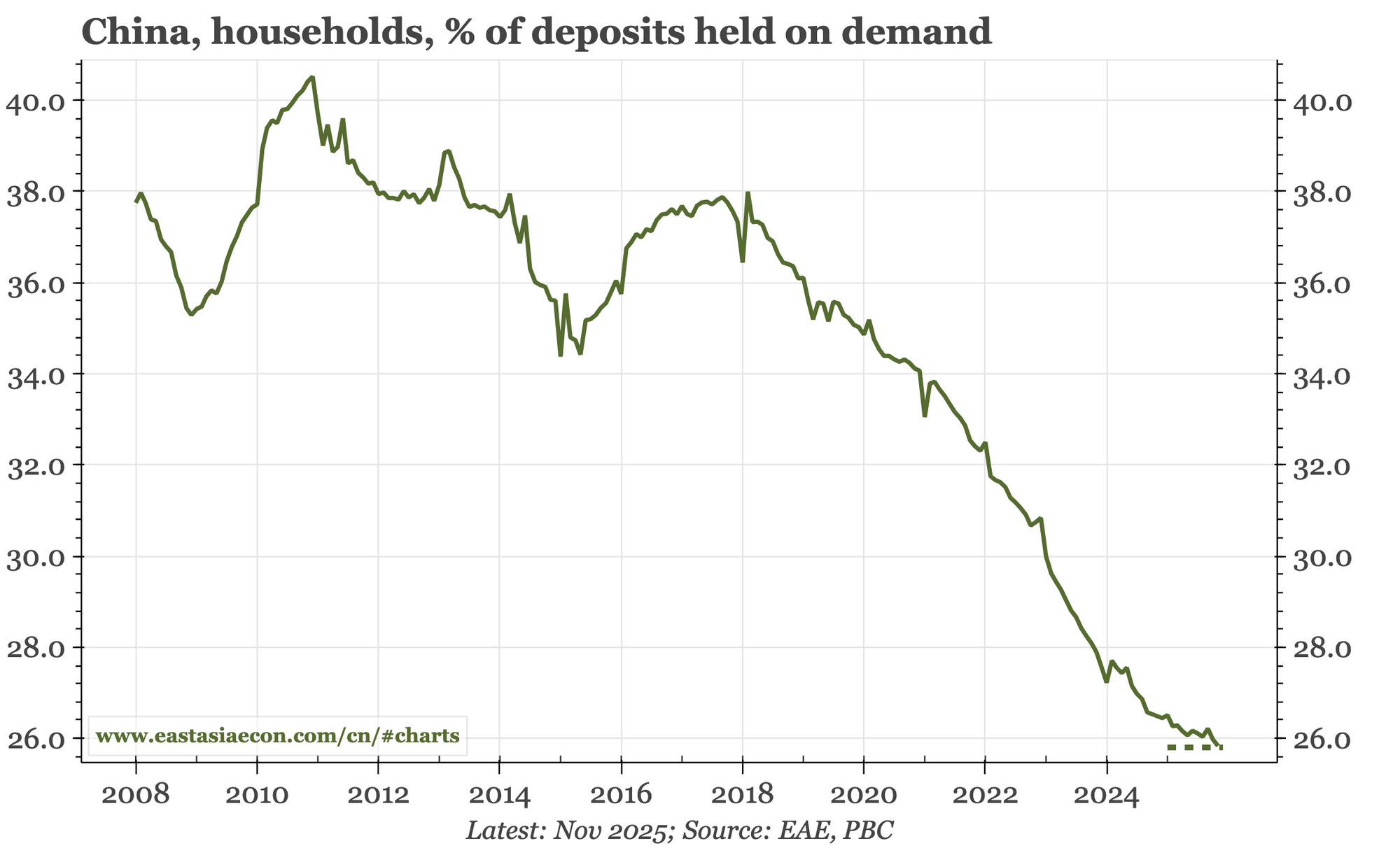

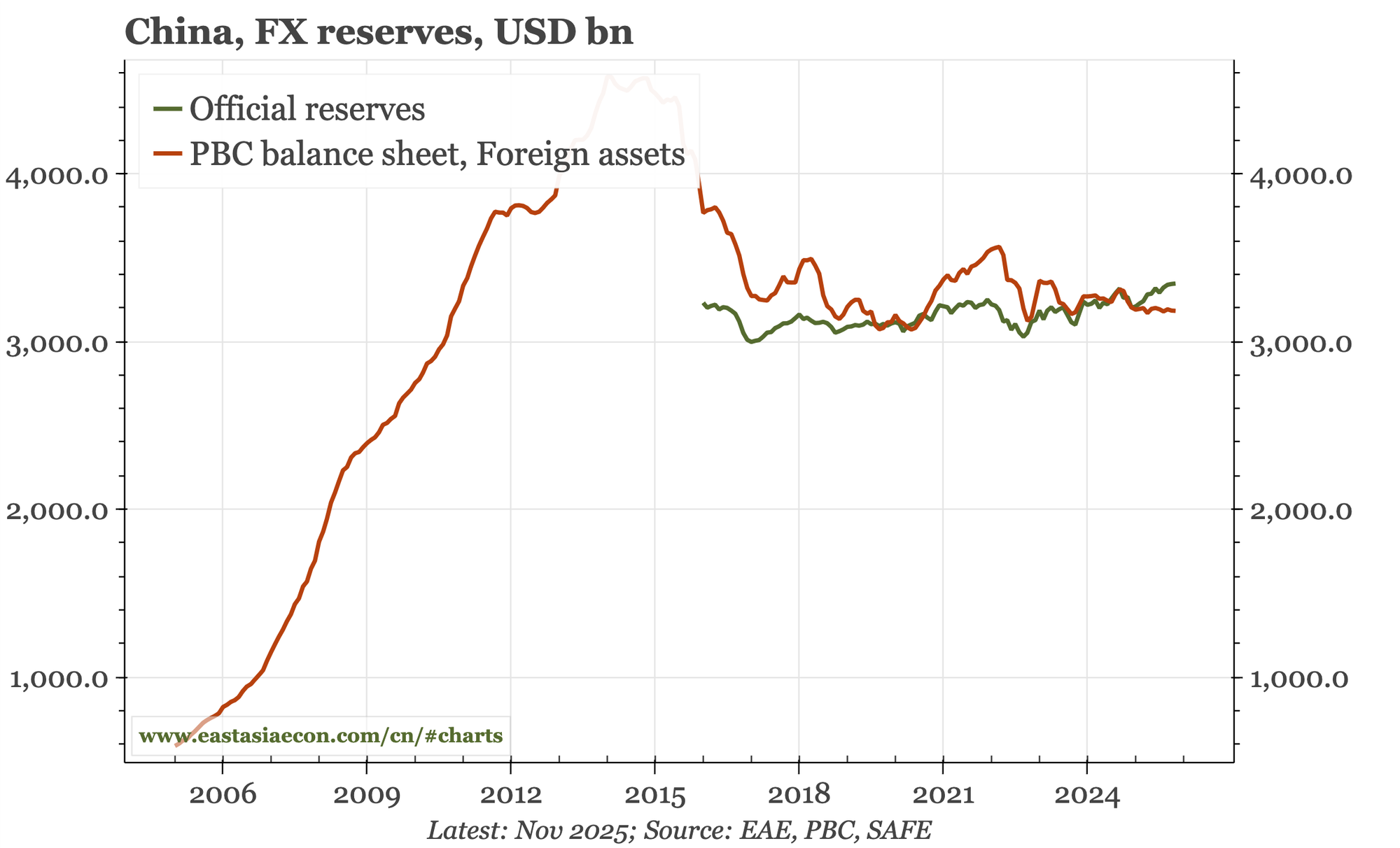

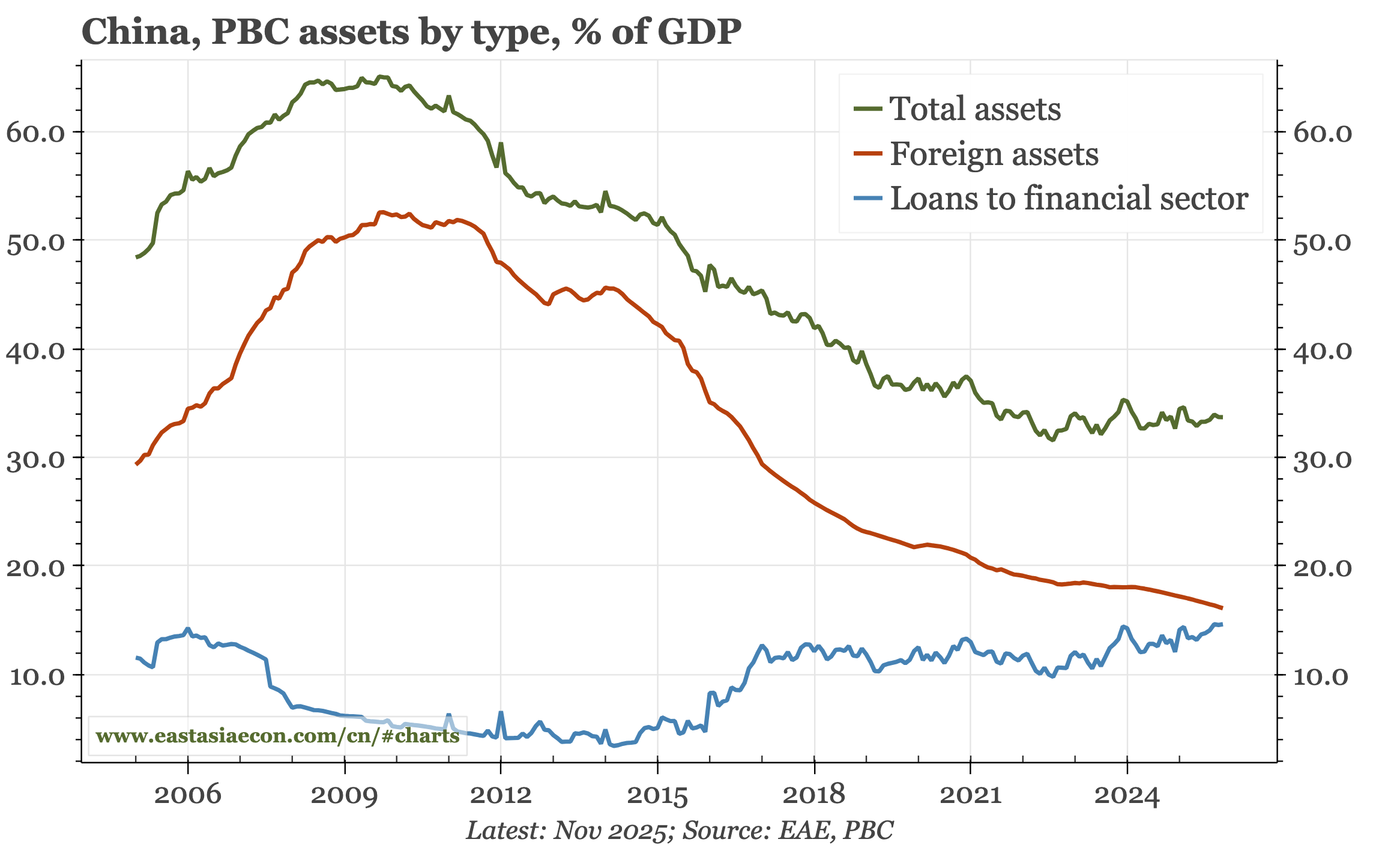

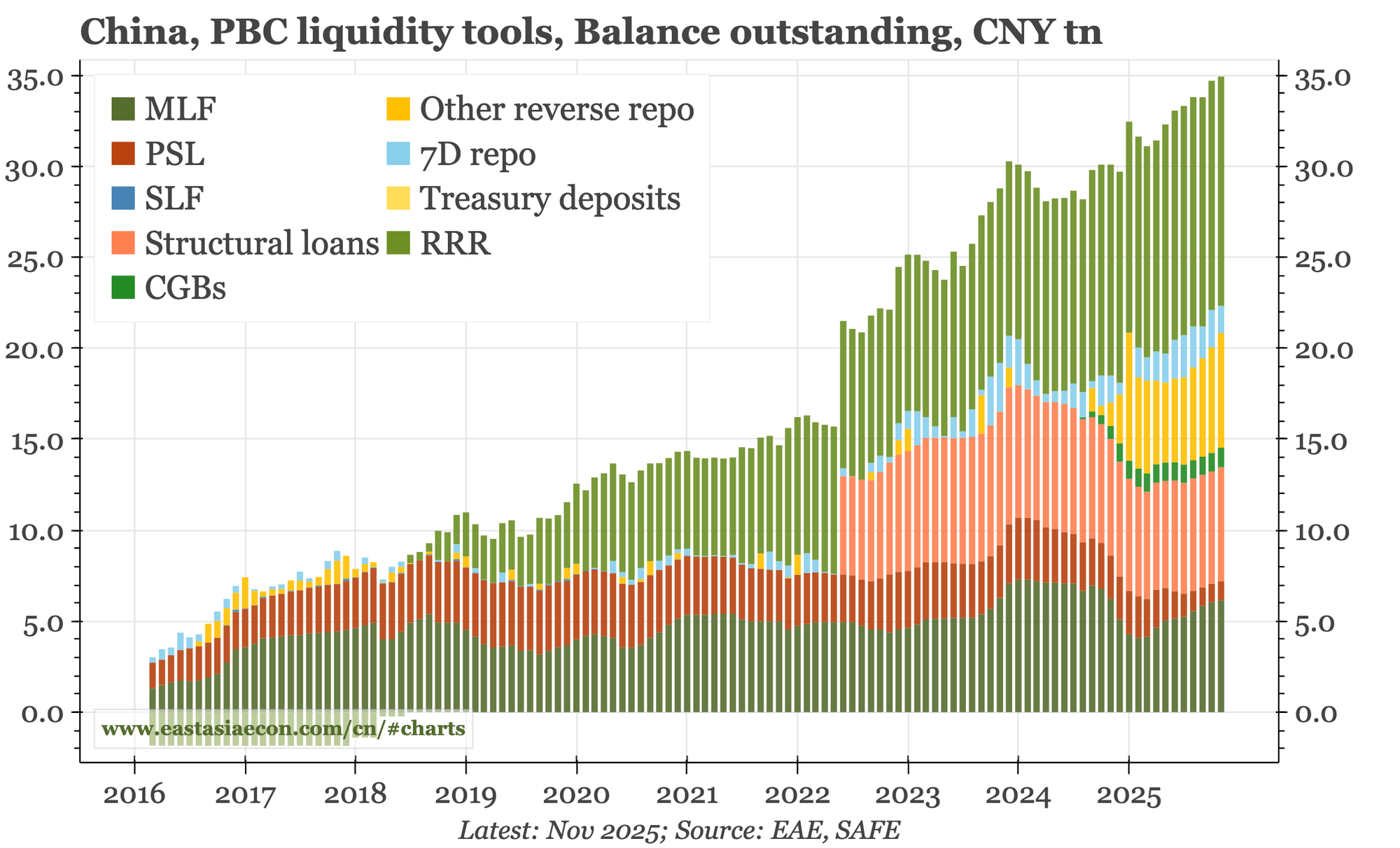

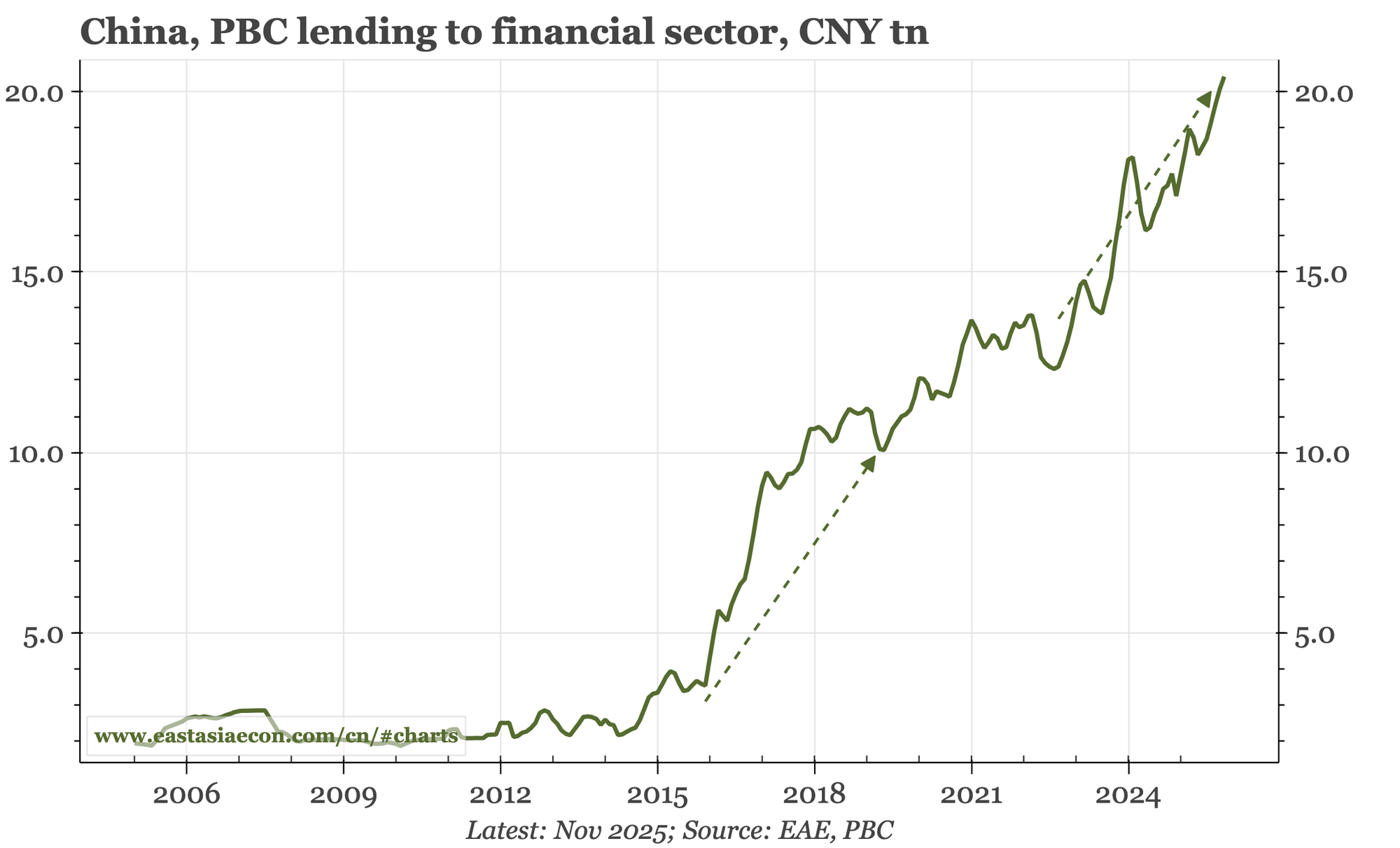

Some of the positive monetary developments of recent months cooled in November. Today's fx settlement data point to a slowing of capital inflows, and the demand:time deposit ratio in the household sector dipped down. PBC policy remains supportive, with no let-up in the pace of its lending to the financial sector. But into the end of 2025 and the macro picture remains soggy.

The tone of the slide released after today's monetary policy meeting was constructive:

uncertainties...have declined

the likelihood of realizing the baseline scenario...has been rising

And some of Ueda's comments at the press conference were encouraging:

Even after raising rates to 0.75%, there's some distance to the bottom of our estimated range of neutral

When looking at the impact of our past rate hikes, I don't think there's evidence that they have diminished the degree of monetary support enormously

But he also said

All I can say is that our future policy decision depends on the information that will become available at the time

smaller firms' profits are overall firm. The problem is that there is divergence, particularly among the smallest firms. We want to look developments carefully

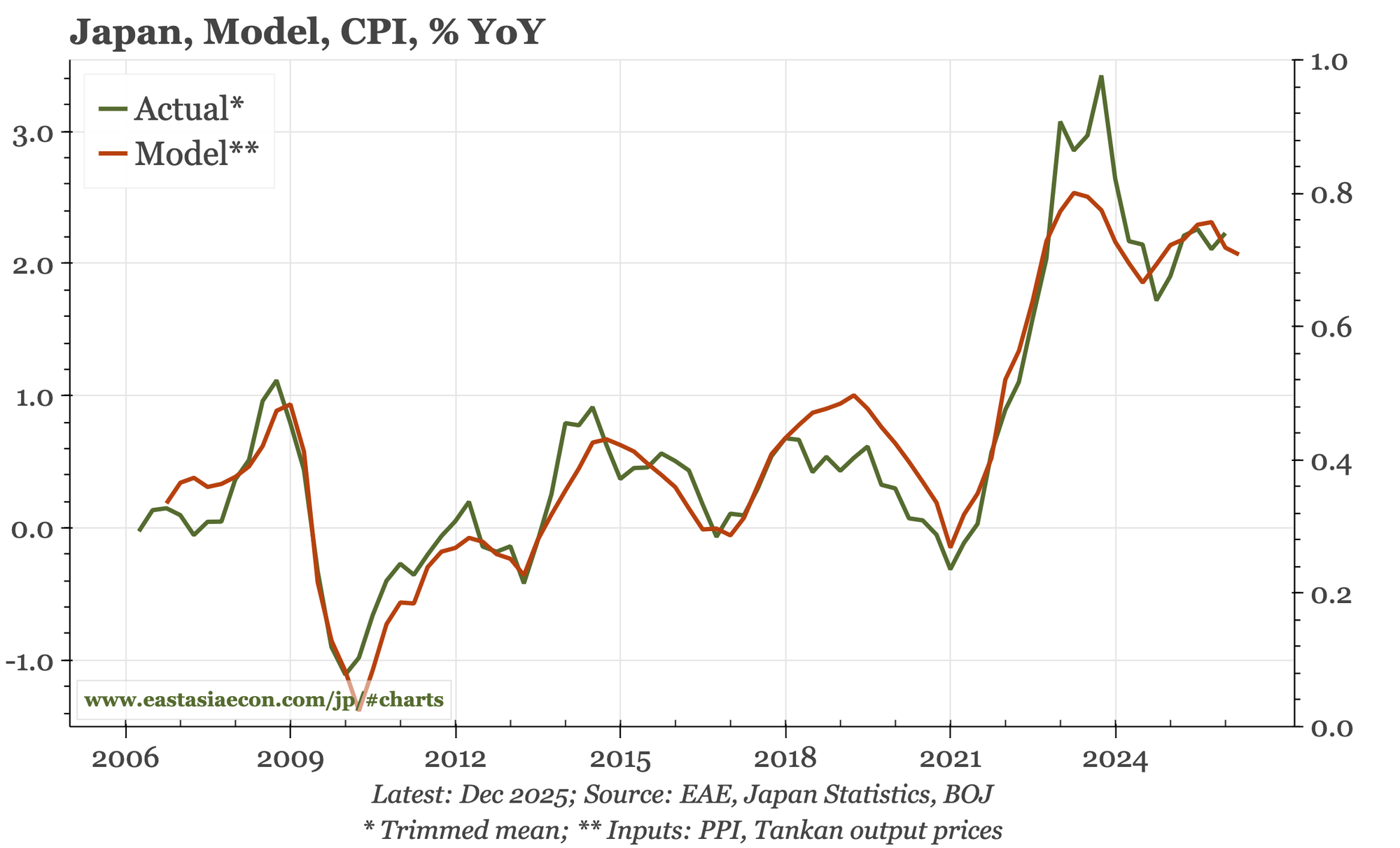

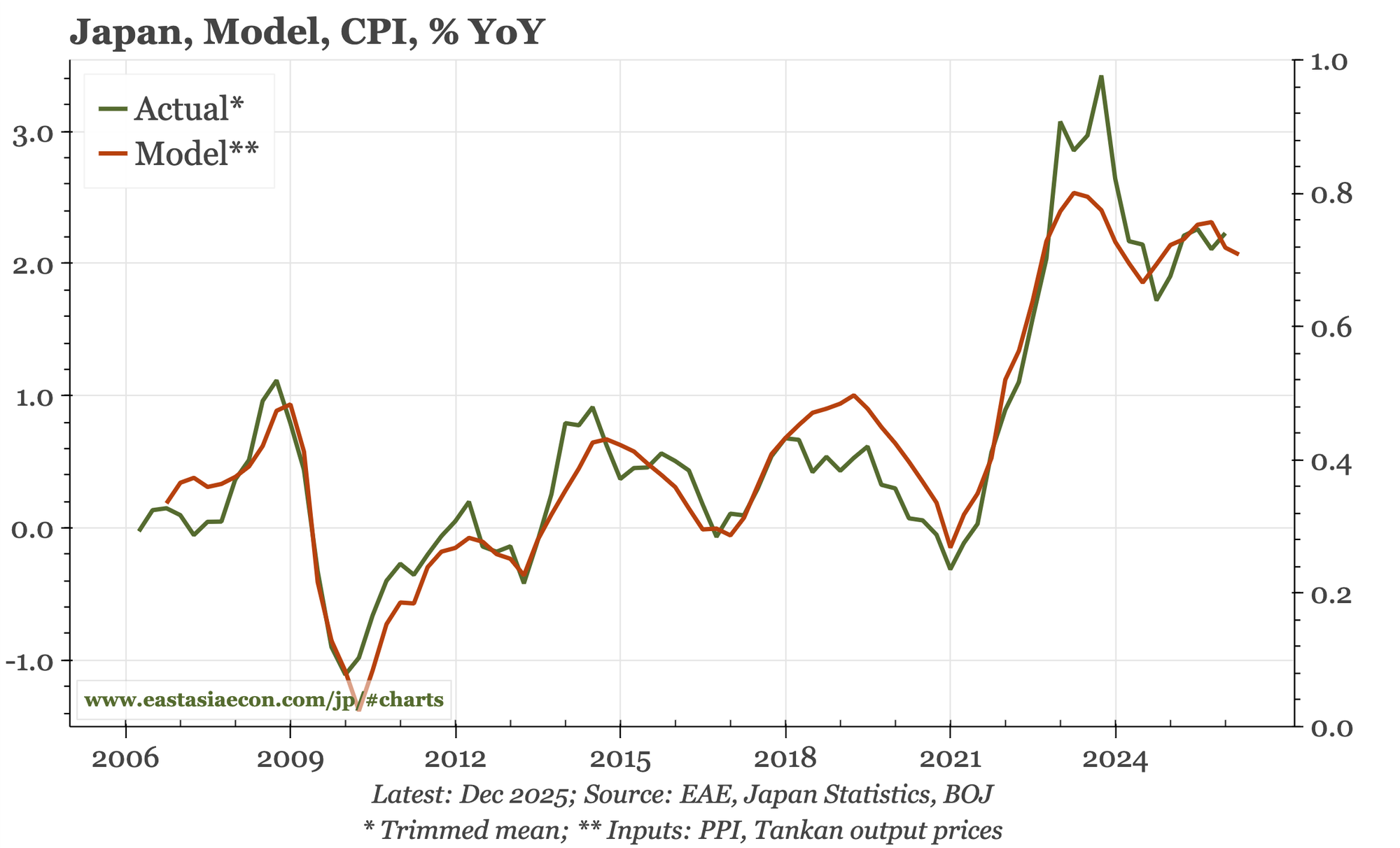

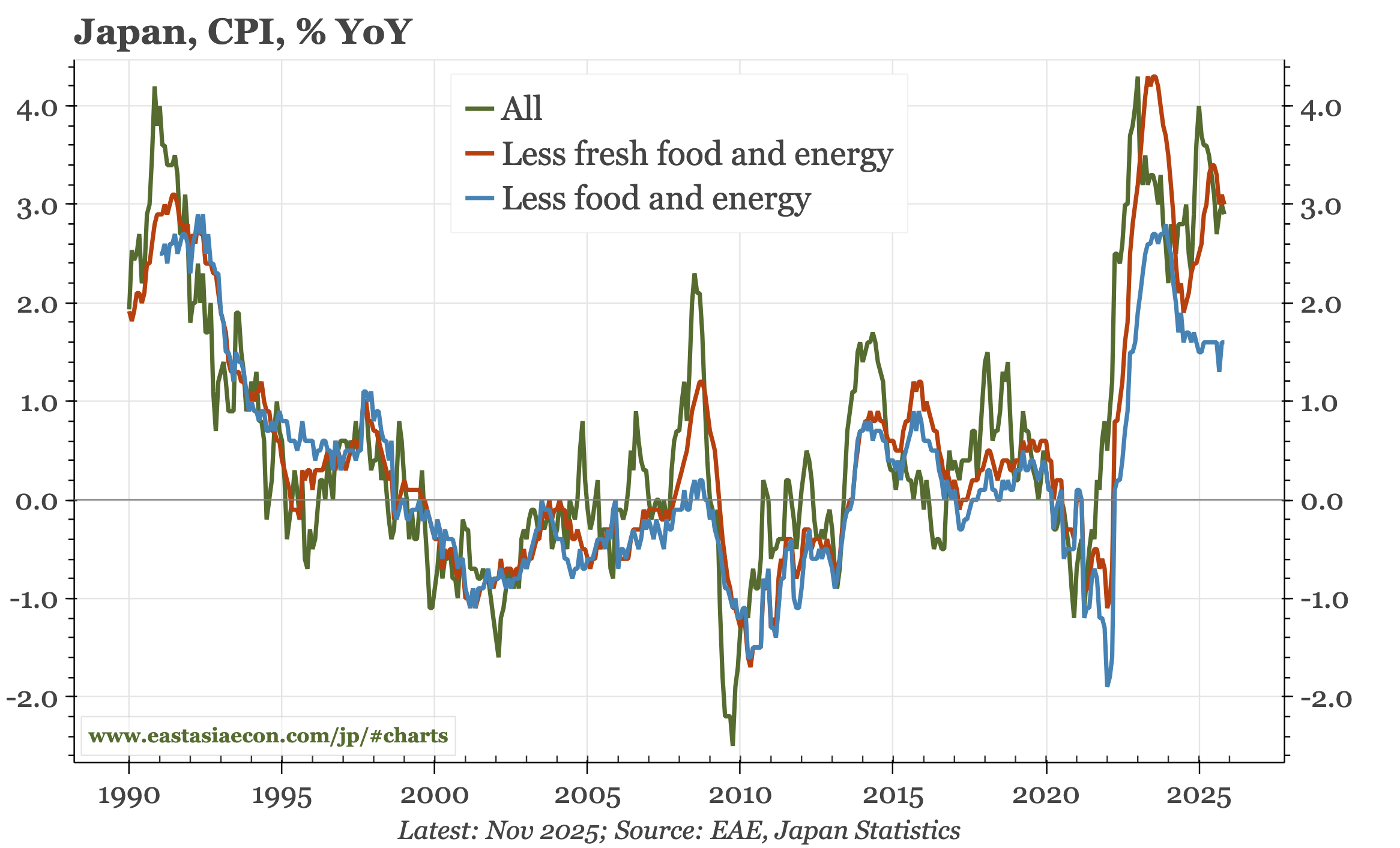

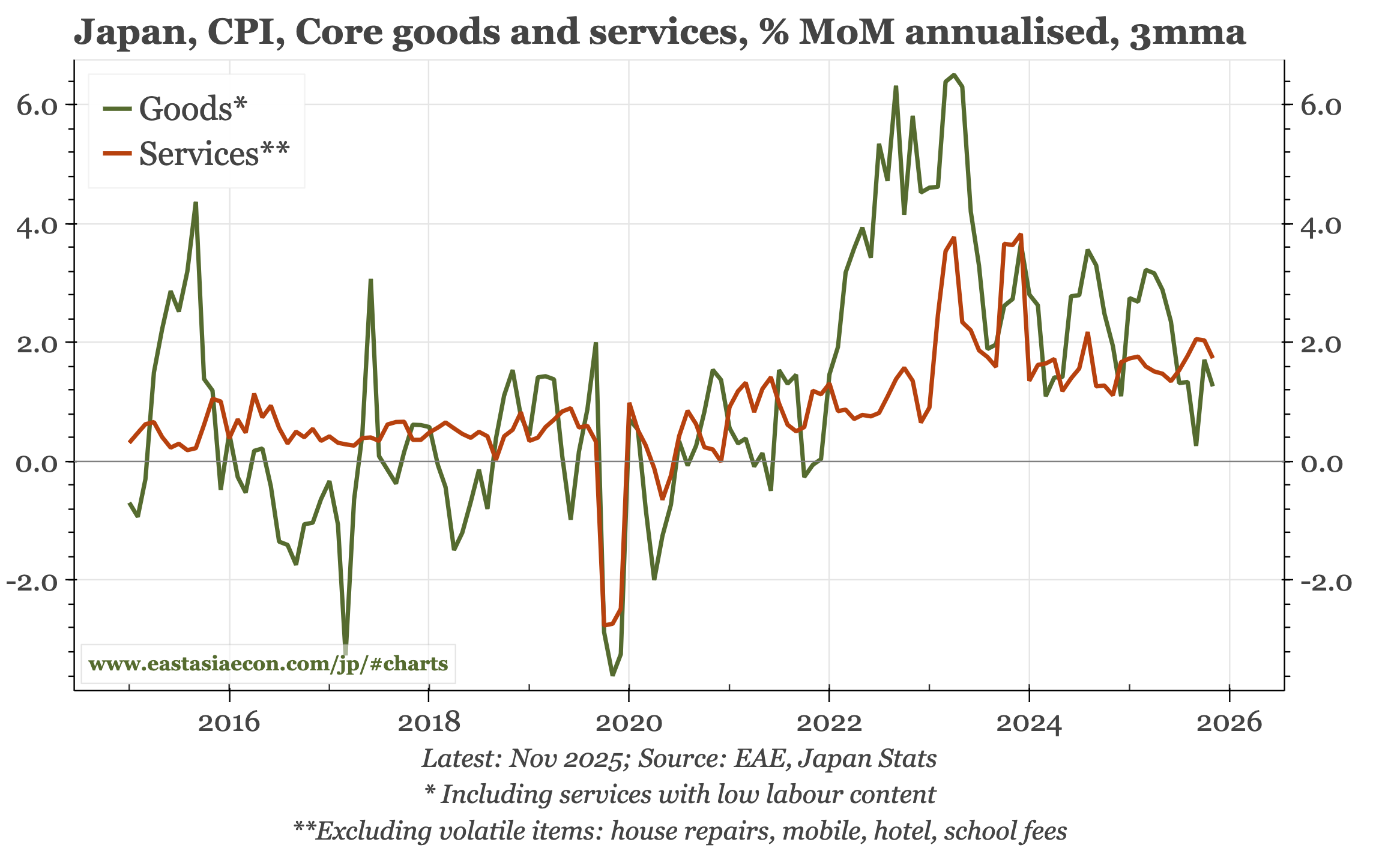

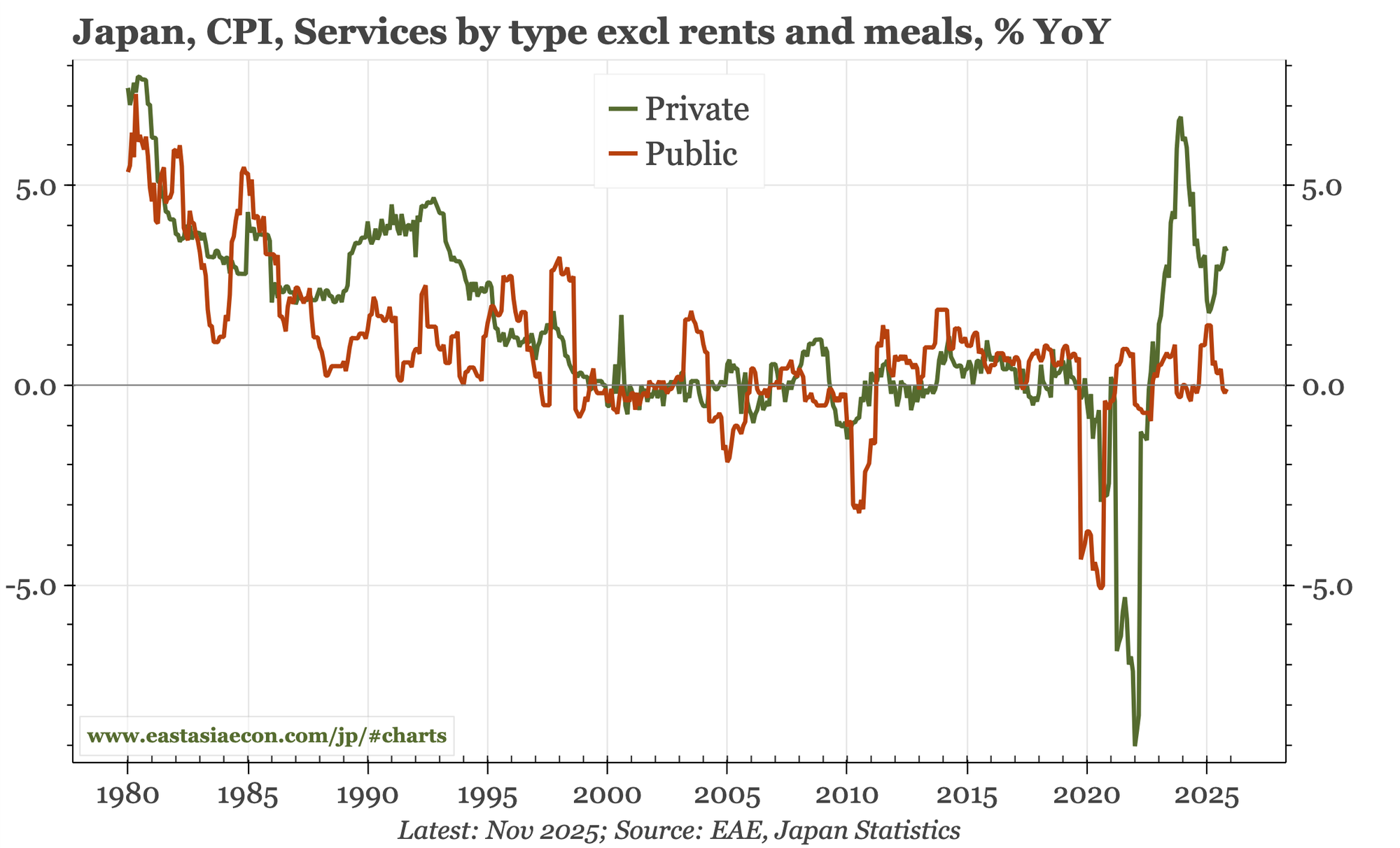

None of that is unreasonable, but the overall tone is rather neutral, whereas the JPY needed a more hawkish message. As long as the currency remains so weak, it will continue to support inflation. That said, updating my model after today's CPI data, and I don't see signs that inflation is about to accelerate up again.

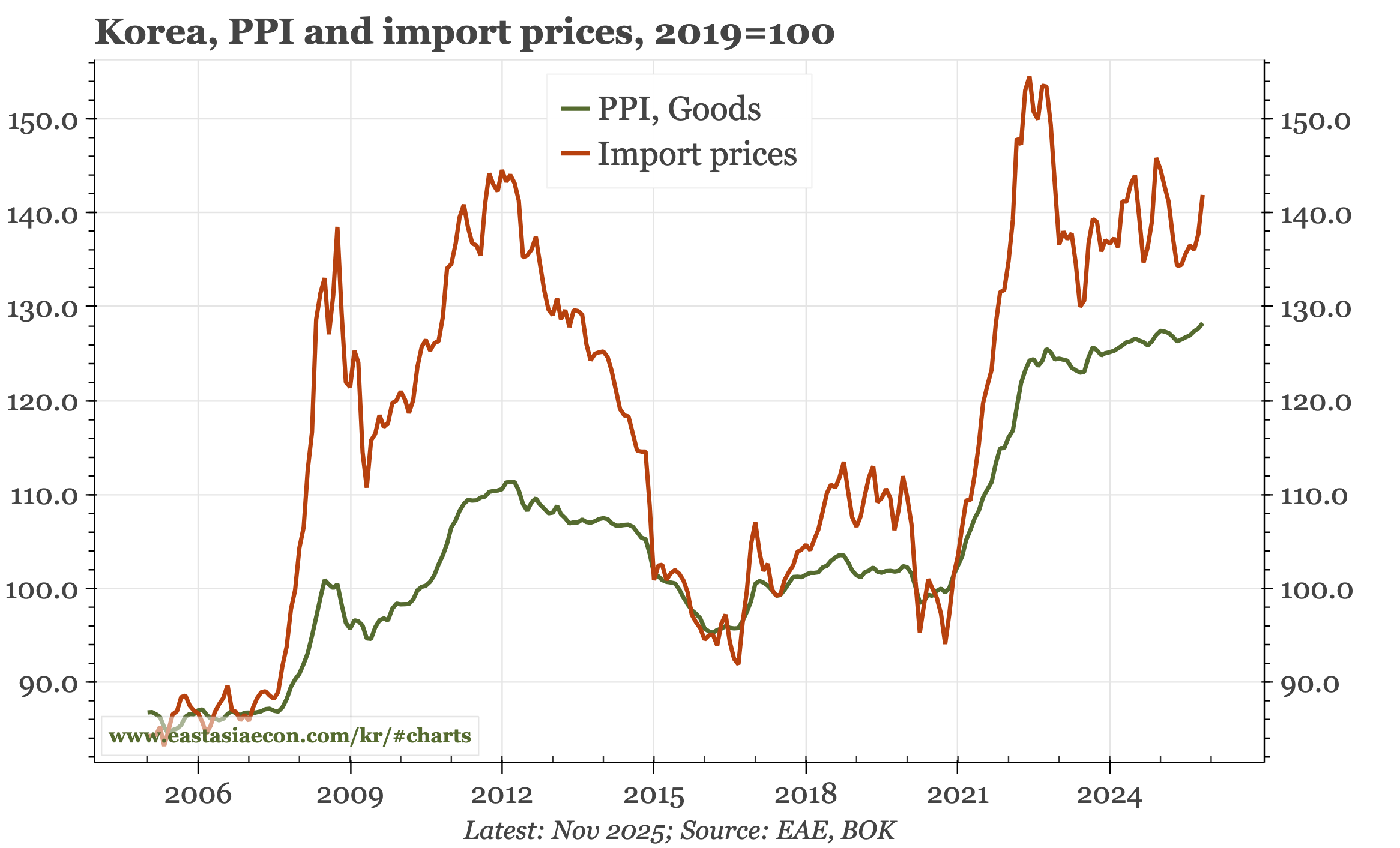

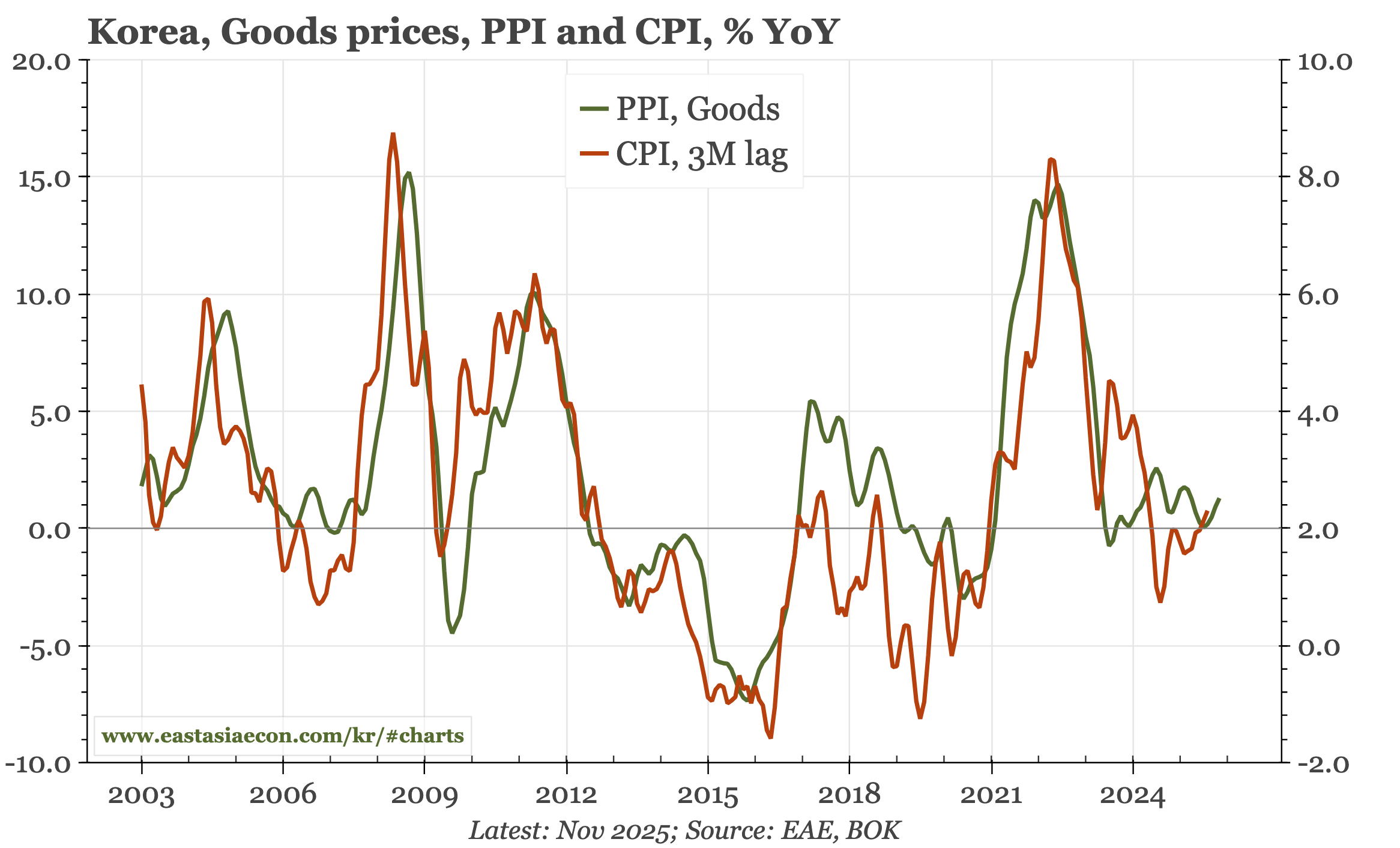

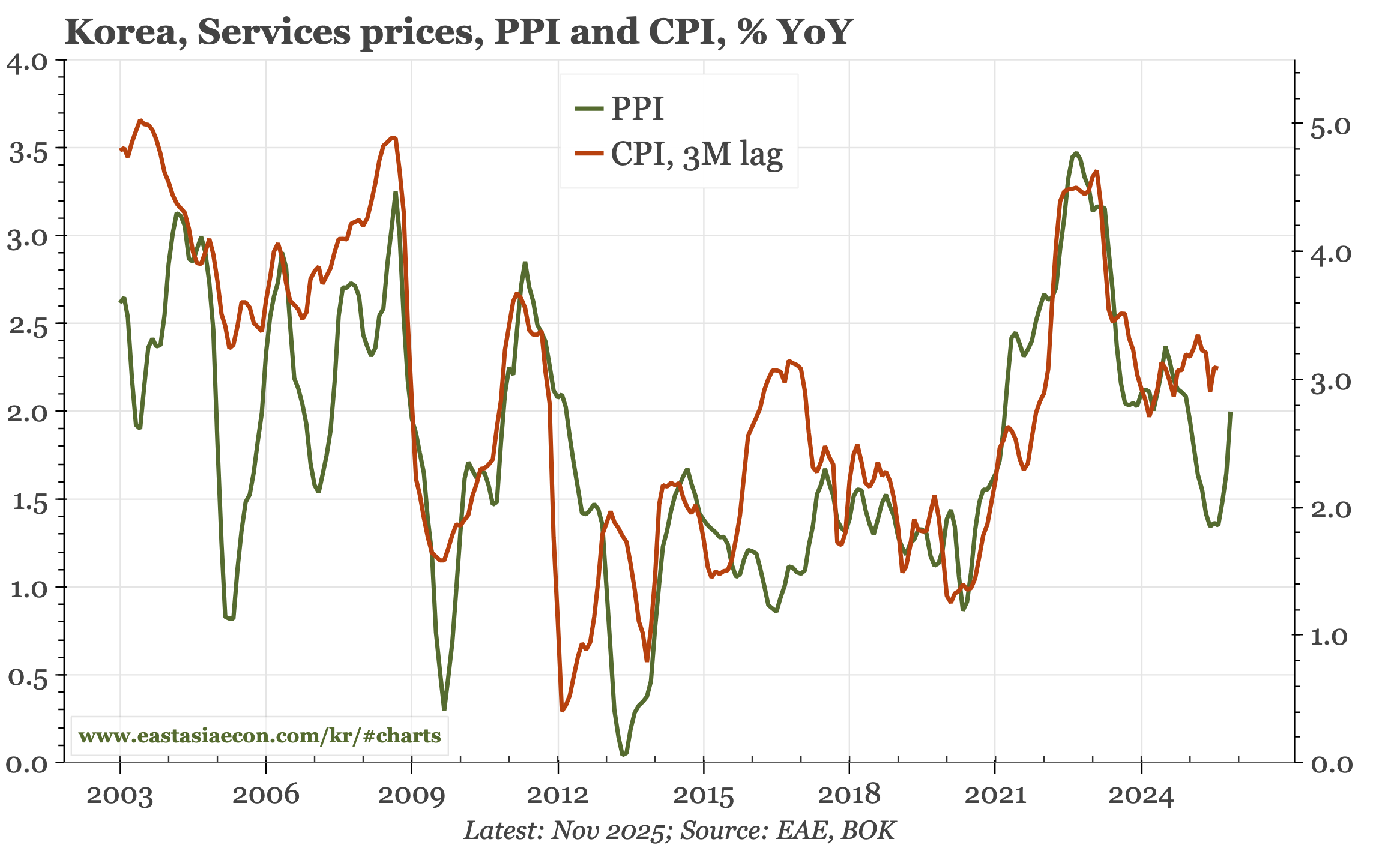

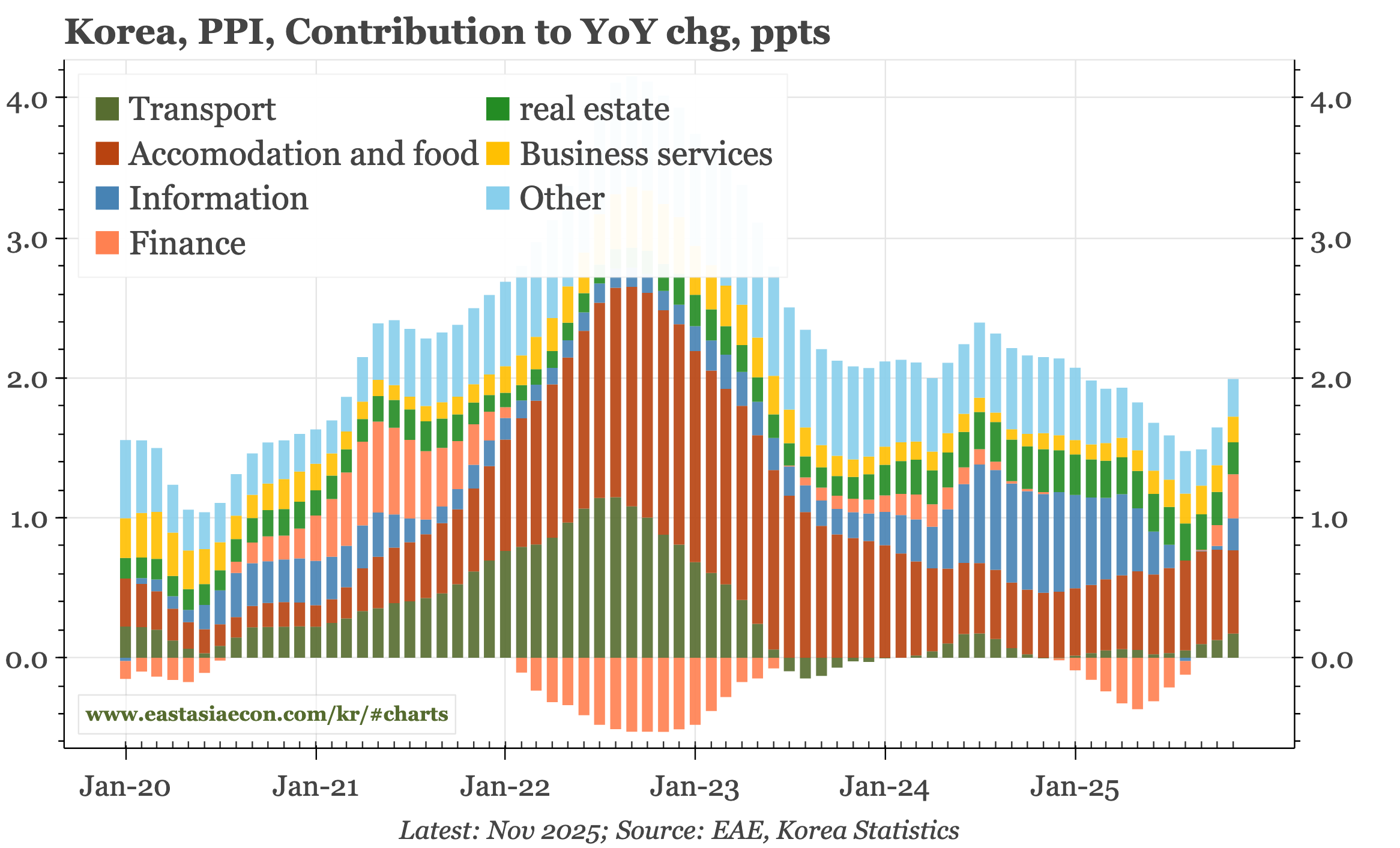

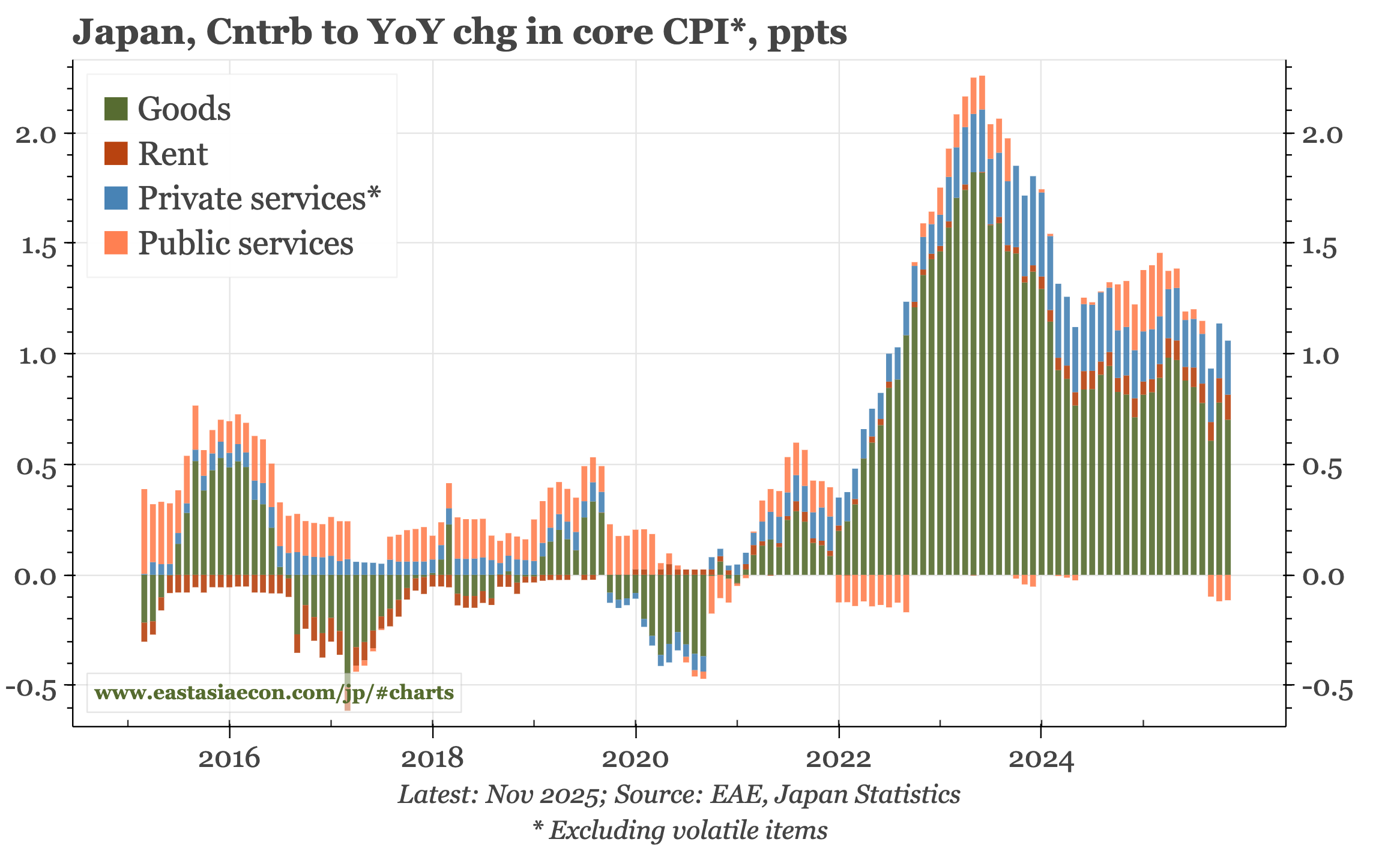

Cycle update – PPI inflation picking up. The mild rise in PPI goods inflation reflects the continued strength of import prices. Services PPI inflation is picking up too, reversing the sharp fall of 1H25. Neither development yet suggests CPI inflation is about to accelerate, but the bounce in services PPI removes downside risk for CPI.