East Asia Today

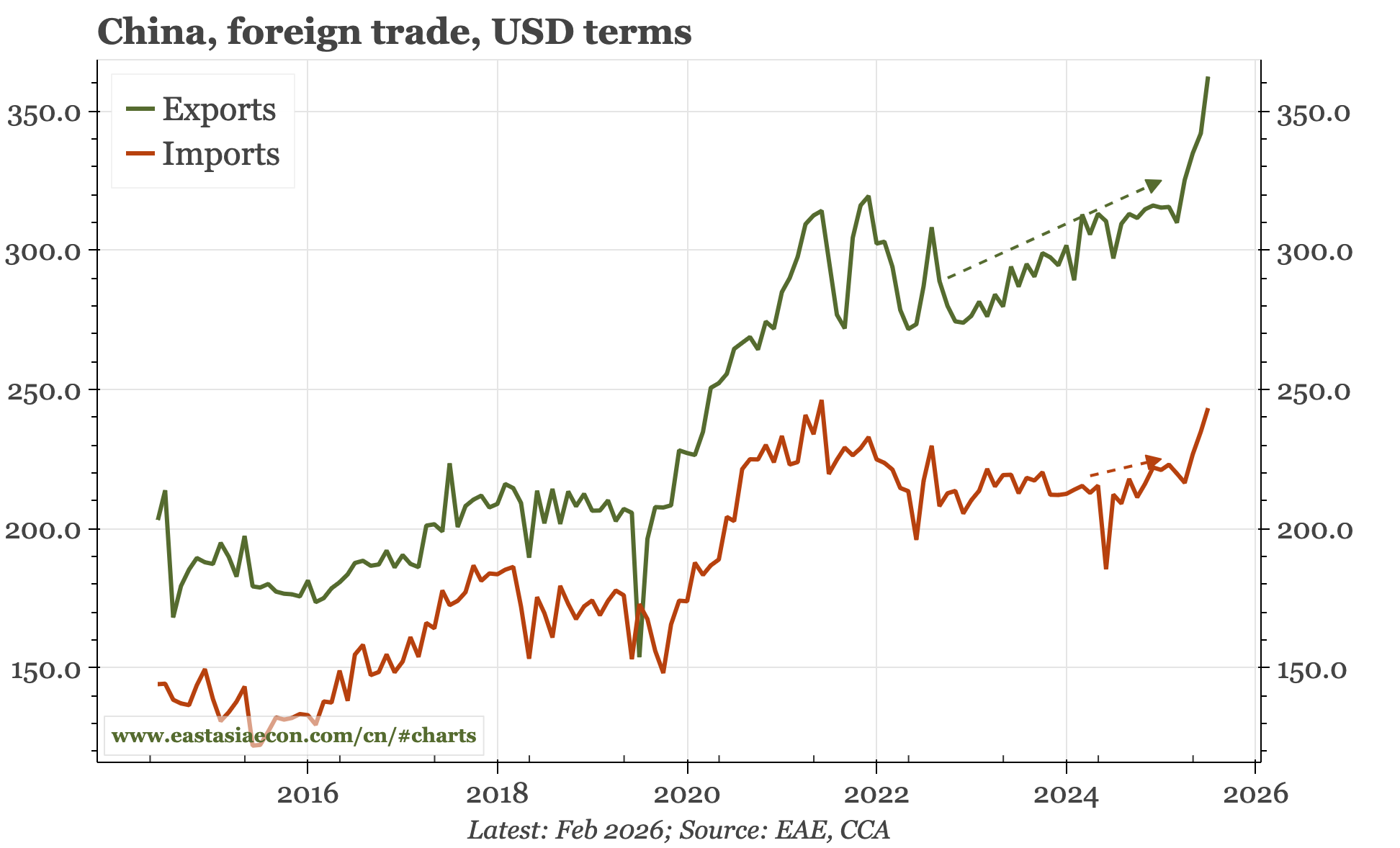

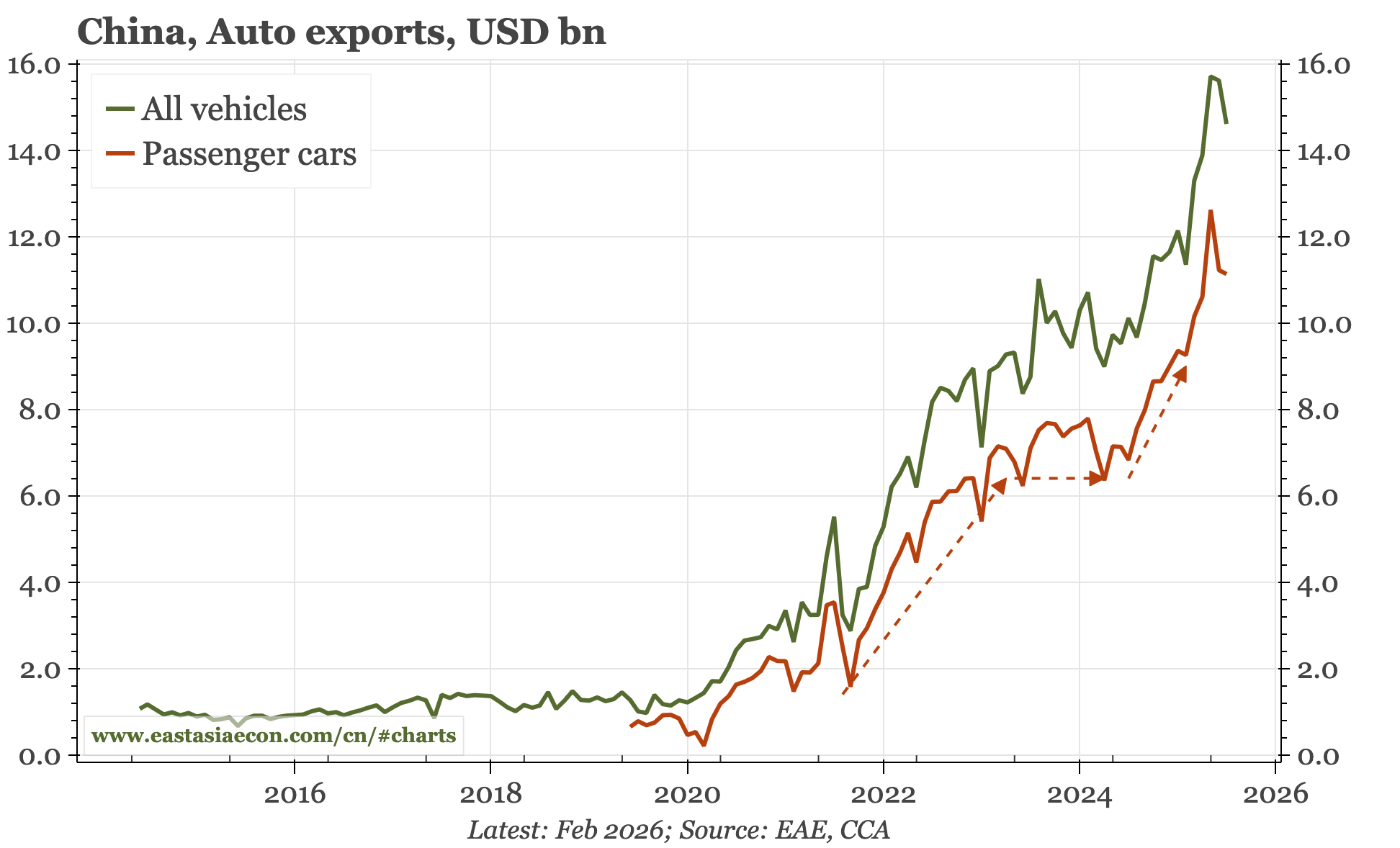

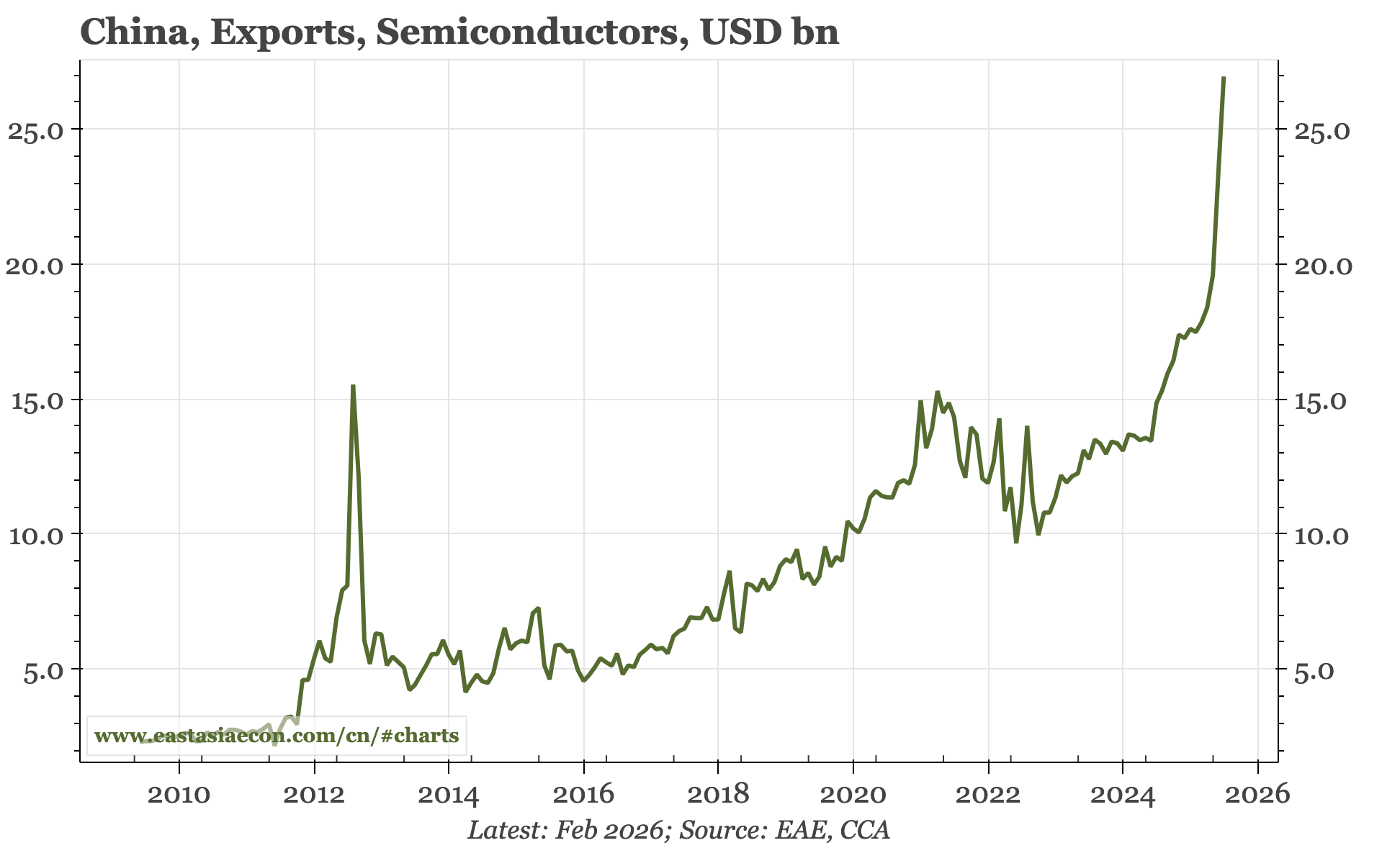

It isn't worth paying too much attention to China's detailed trade statistics for Jan-Feb, given new year distortions. That said, the trend rise in capital goods imports is an under-appreciated shift. Tourist arrivals in Japan remained strong in February, as did Taiwan export orders.

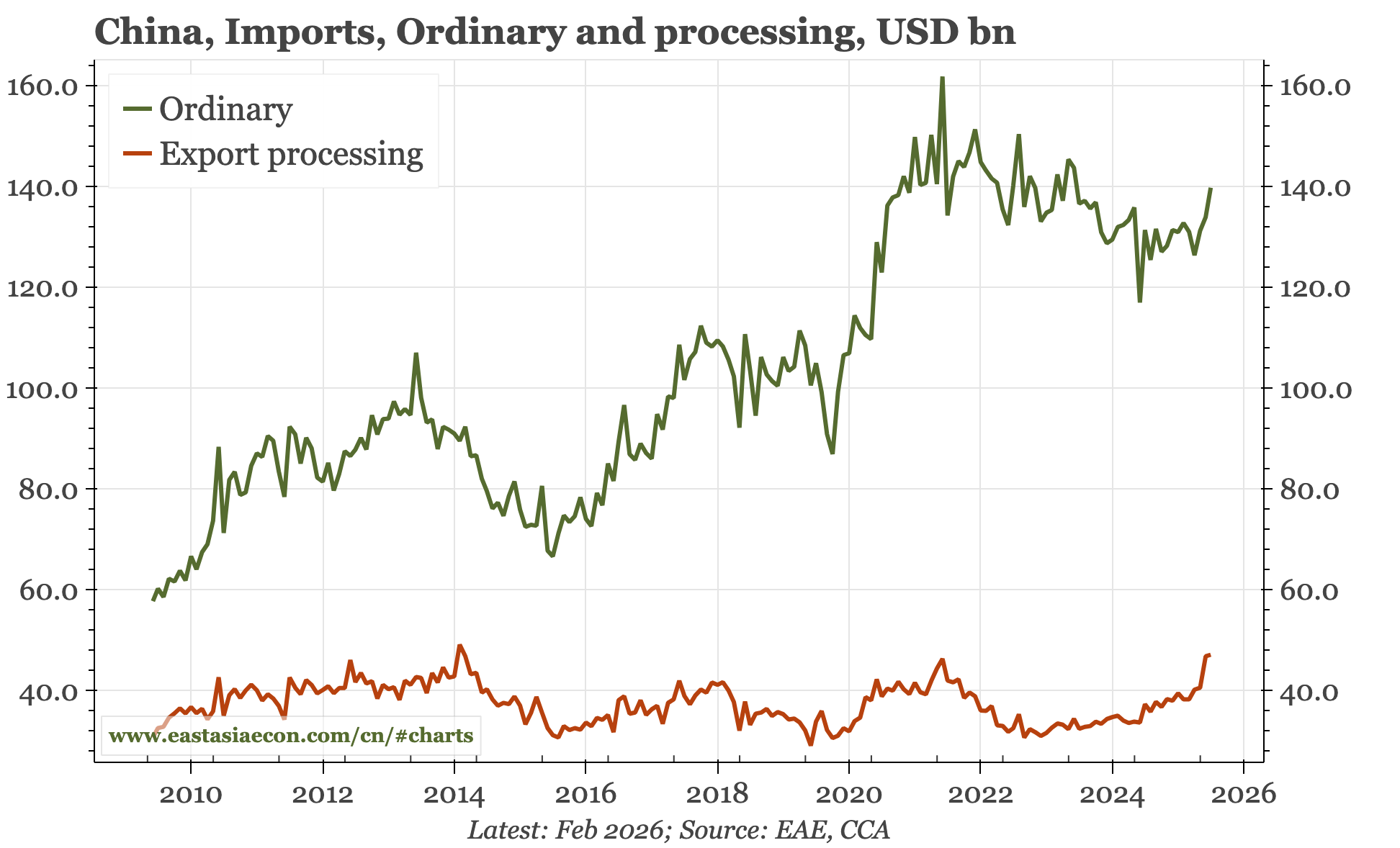

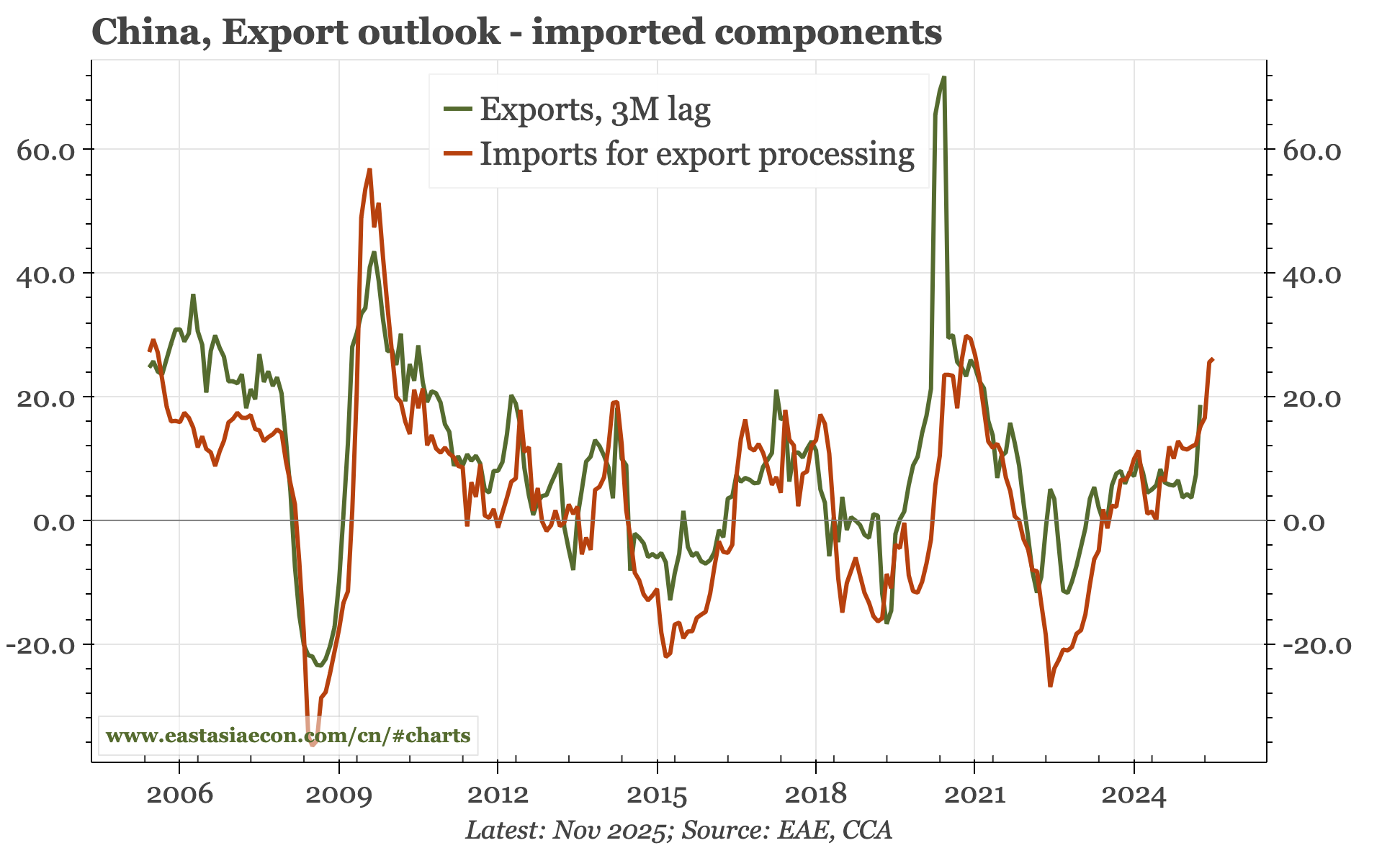

China has now released most of its detailed trade data for January and February. The apparent logic of releasing the data for both months at the same time is to lessen the confusion from the big swings in the data for any one month caused by Chinese New Year. Personally, I don't think that reasoning is persuasive, especially because the distortions in the trade data in particular tend to persist through March. It seems likely that for overall exports and imports, a fall-back is likely this month after the surge in the first couple of months. Conversely, auto exports are likely to bounce. That said, there are a couple of aspects of import demand which look more durable, with imports of components and capital goods both trending up in recent months.

You can map and chart a lot more of China's trade data in the China Trade Mapper dashboard here:

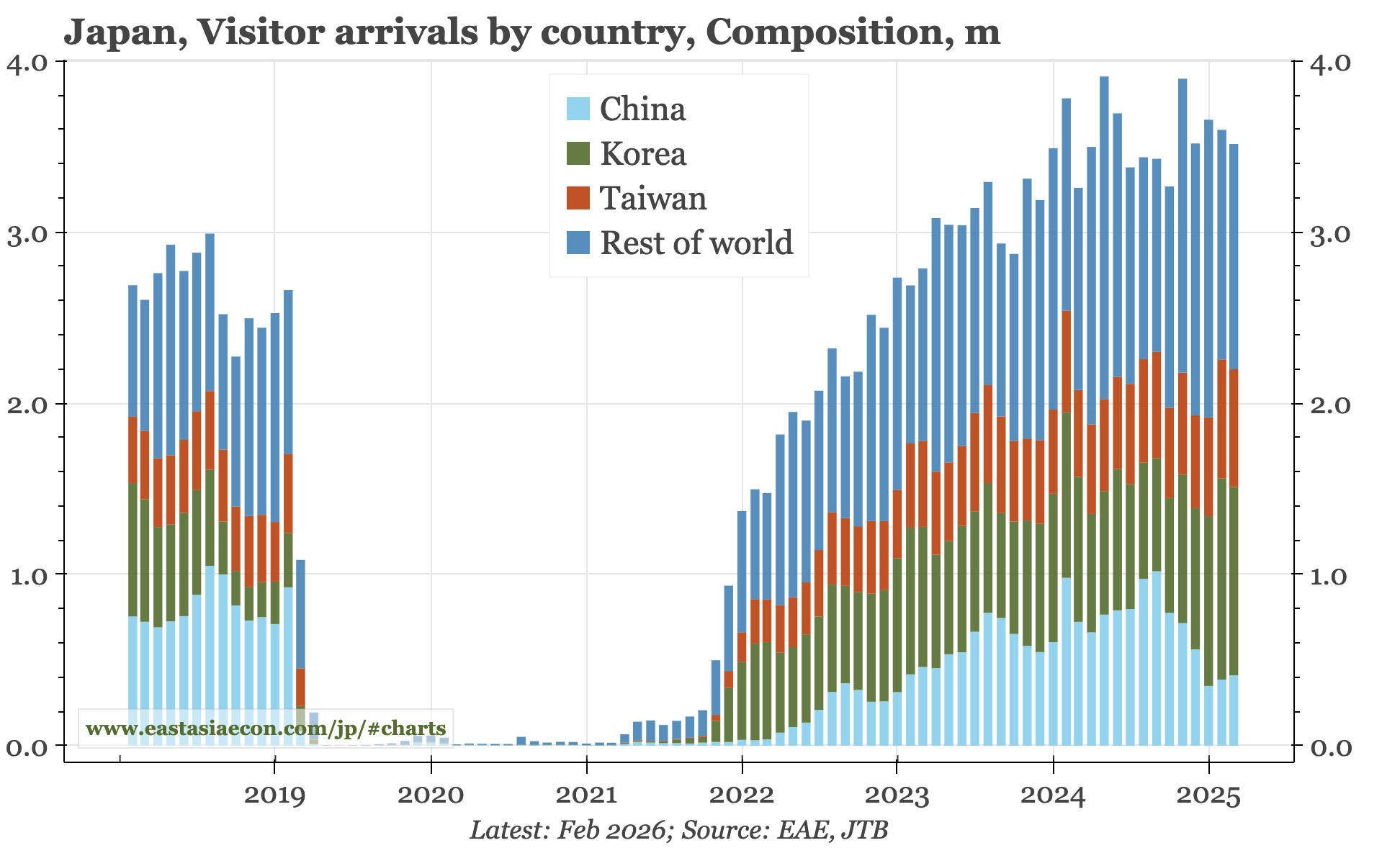

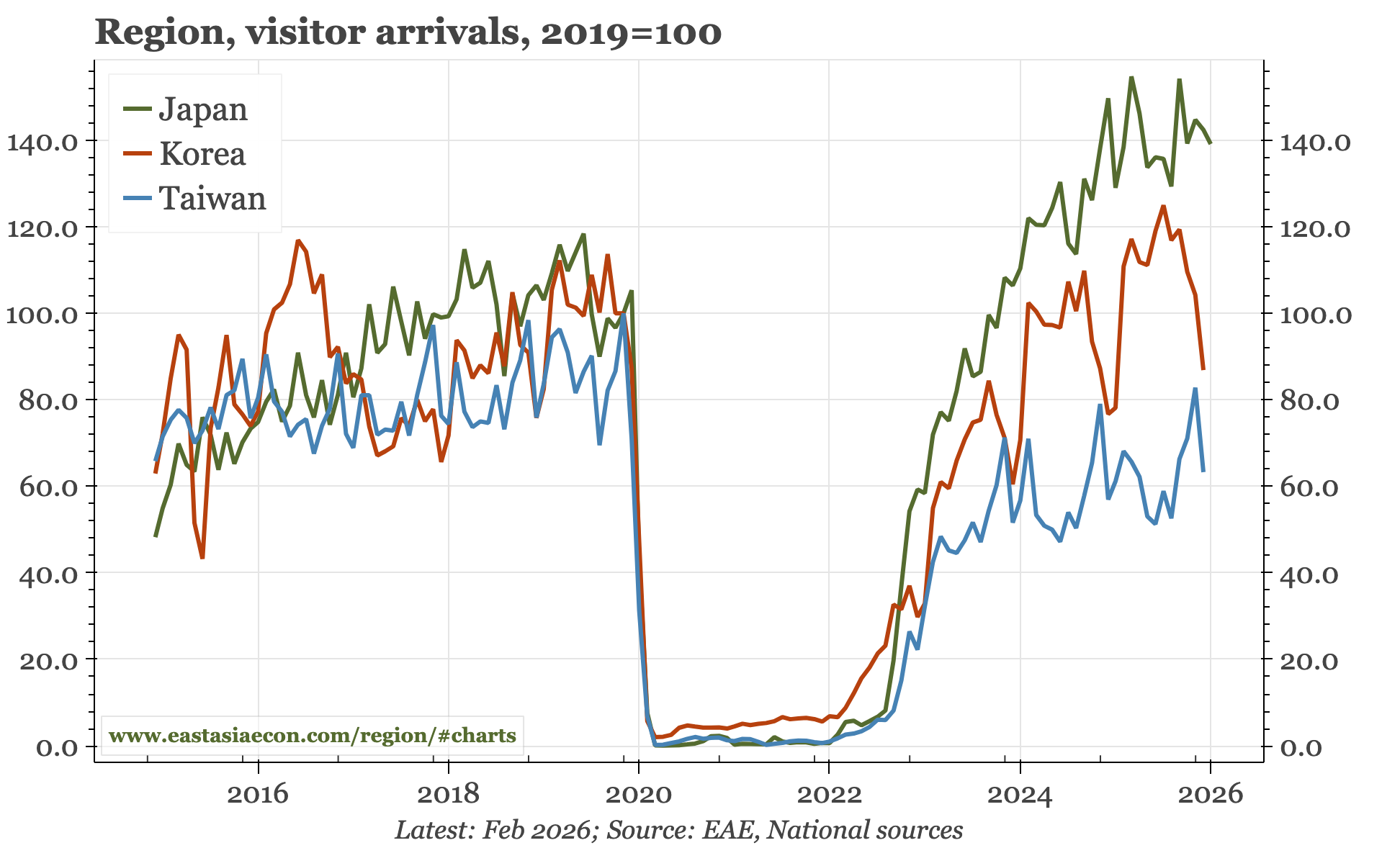

The strength of services activity has been one of the stand-out features of this cycle in Japan, and one driver of that has been the rise in inbound tourism. That has been dampened somewhat by political tensions with Beijing, a falling out that has resulted in arrivals from China halving in the last few months. However, some of that has been offset by rising arrivals from Korea and Taiwan, and overall, the damage resulting from the dispute with China hasn't yet been substantive.

If you aren't yet a subscriber, please consider becoming one! This daily product is designed for individuals, but we also have data services and a much more comprehensive offering for financial institutions. If you have any questions or feedback, please get in touch with me directly.

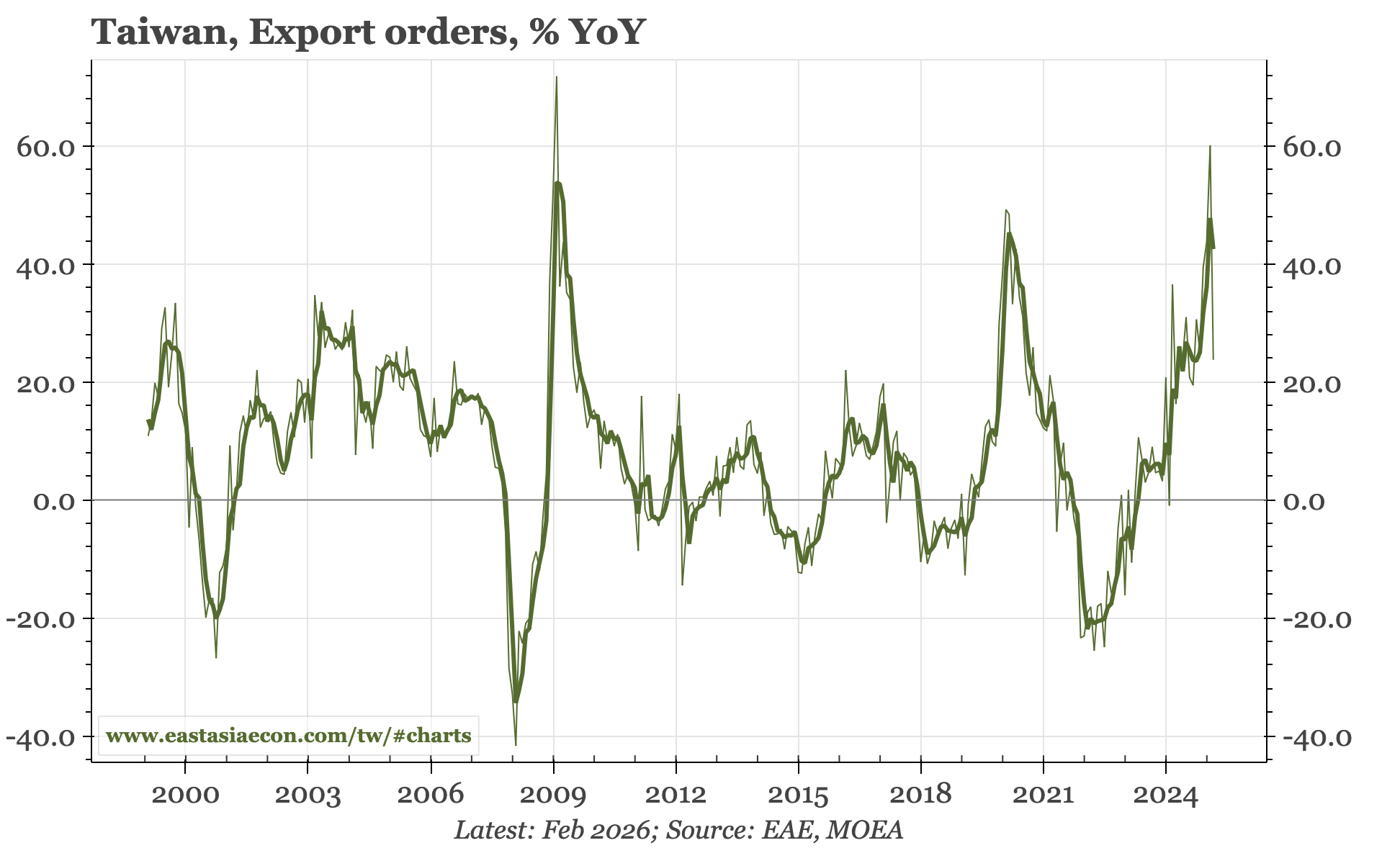

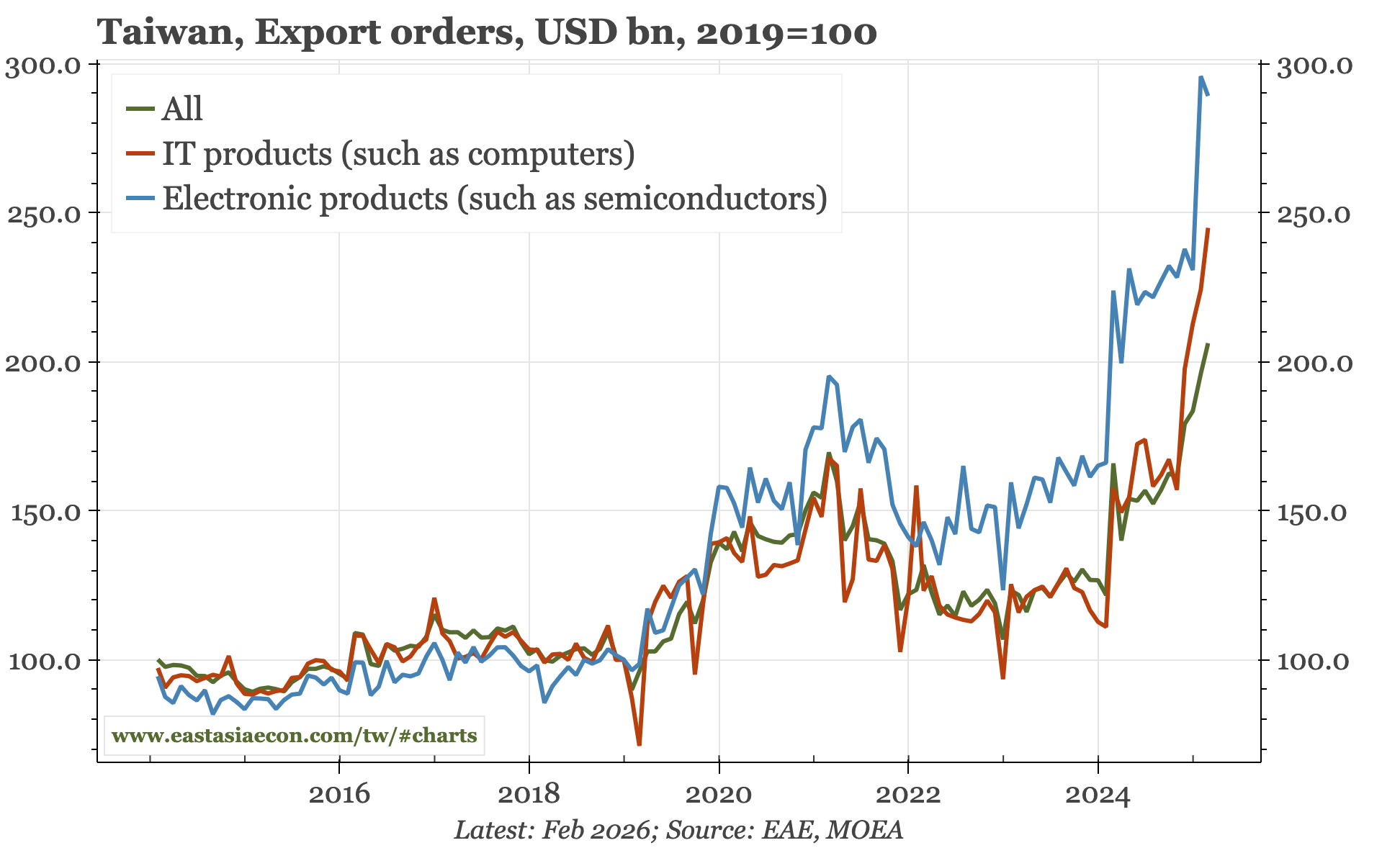

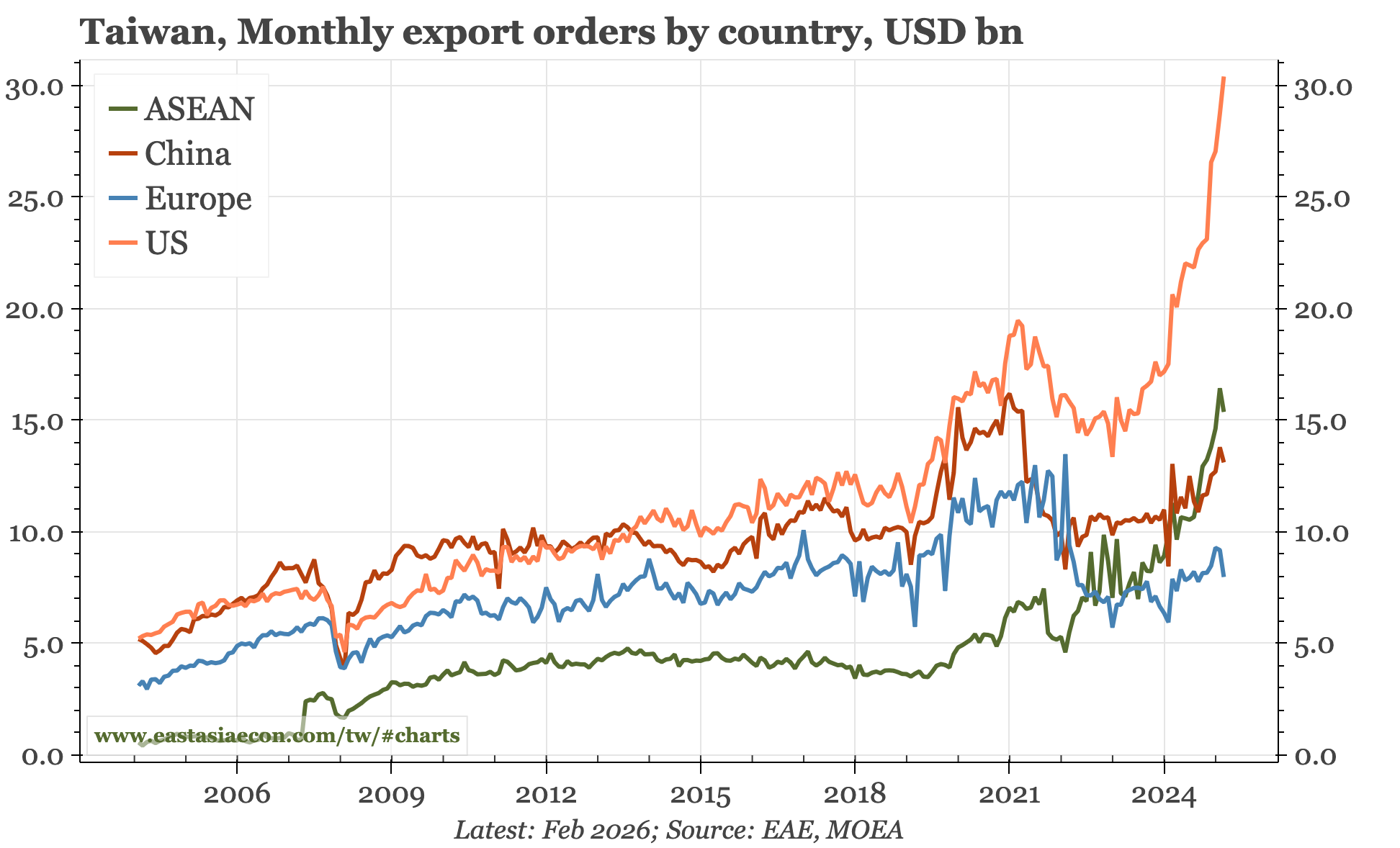

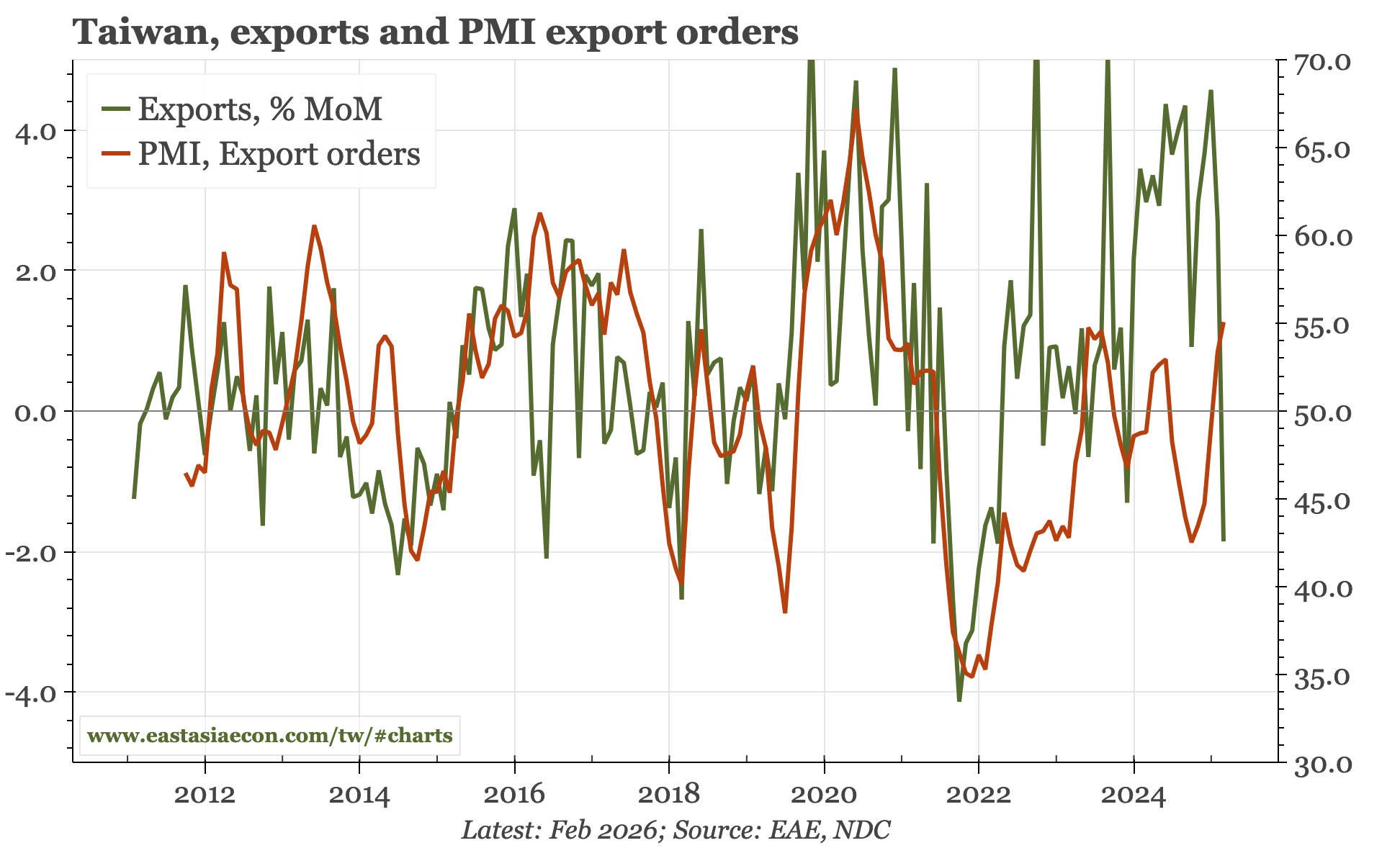

YoY growth in export orders fell in February, but that was base effect. In level terms, orders actually rose, with strength in the US offsetting the ticking down in orders from elsewhere. This suggests that the outlook for exports remains firm. However, the risk is that these data are backward-looking, reflecting the state of affairs before the Iran war.