East Asia Today

Many updates today. In China, property prices and the outlook for CPI, as well as the official activity data for July. The overall tone remains weak. By contrast, the first estimate of Q2 GDP data for Japan was solid. And detailed Q2 data for Taiwan, together with 2H25 forecasts, were more bullish.

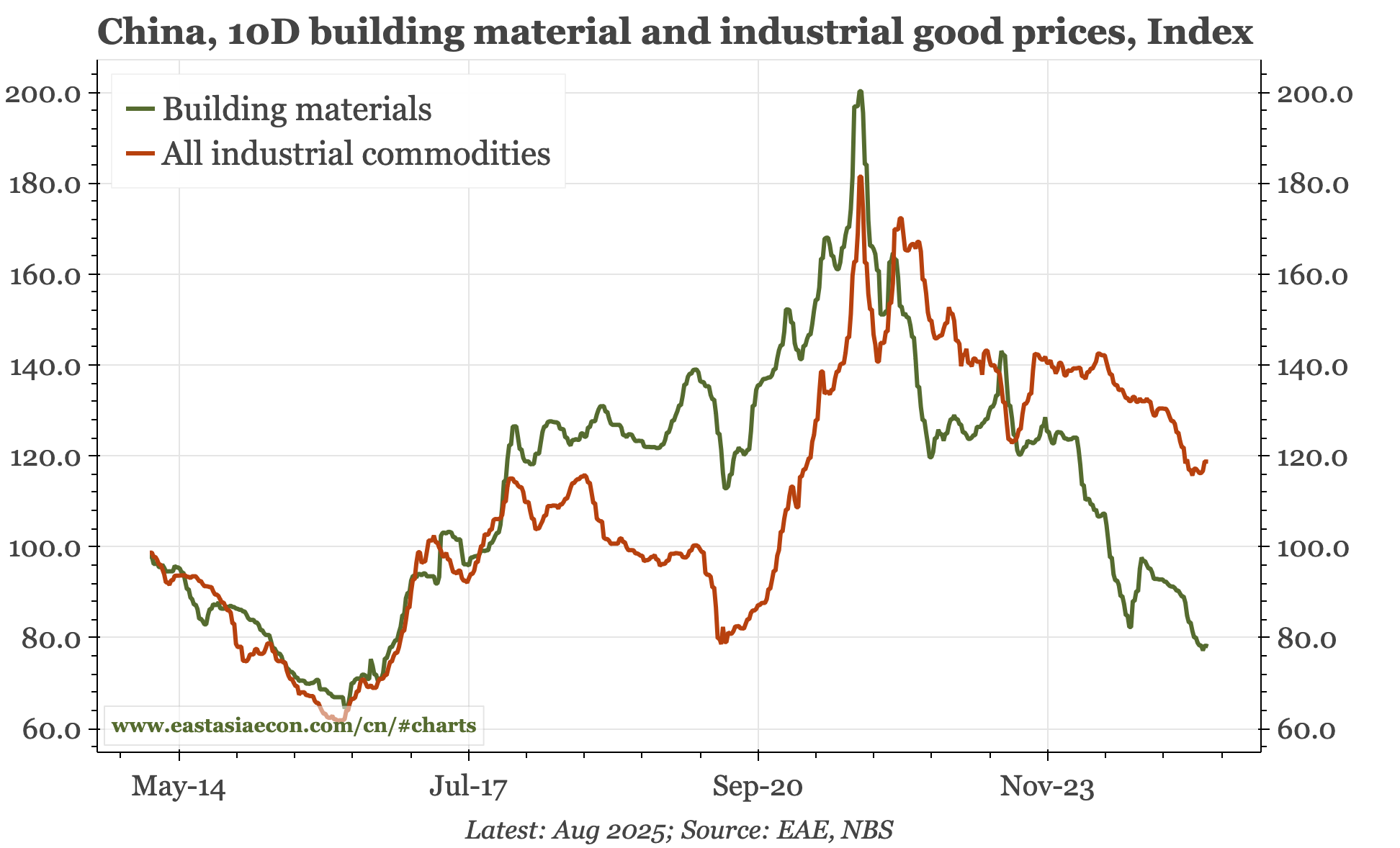

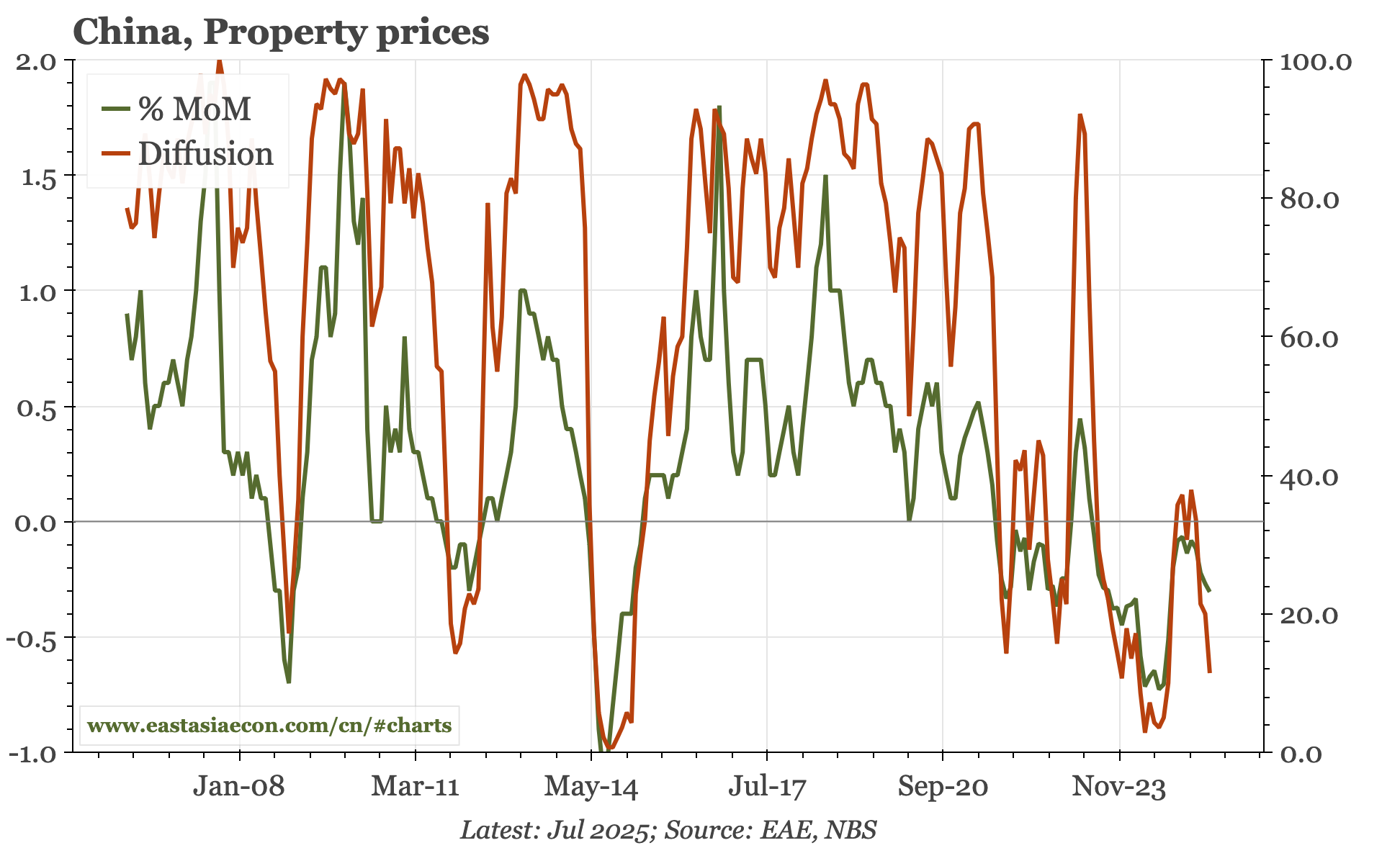

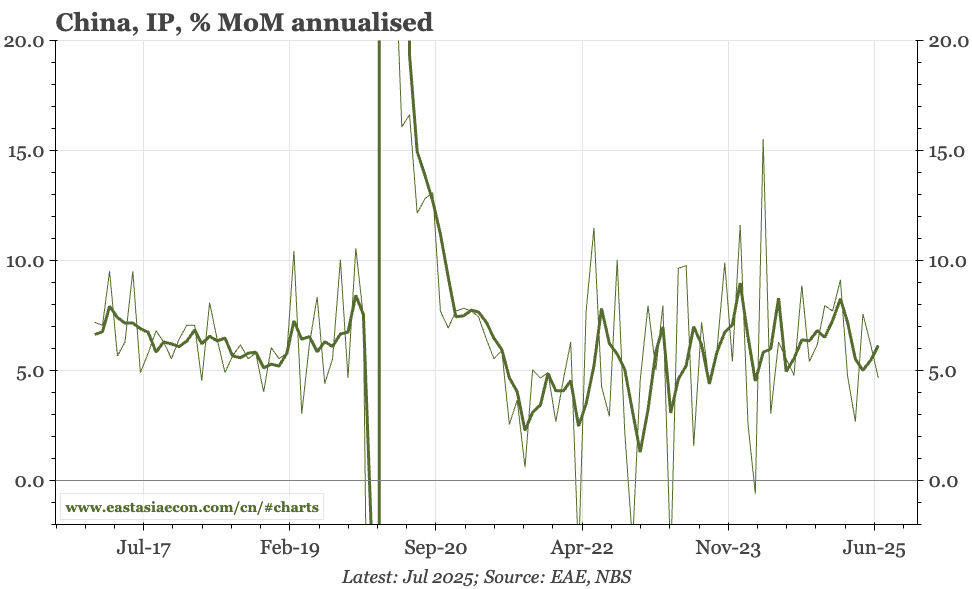

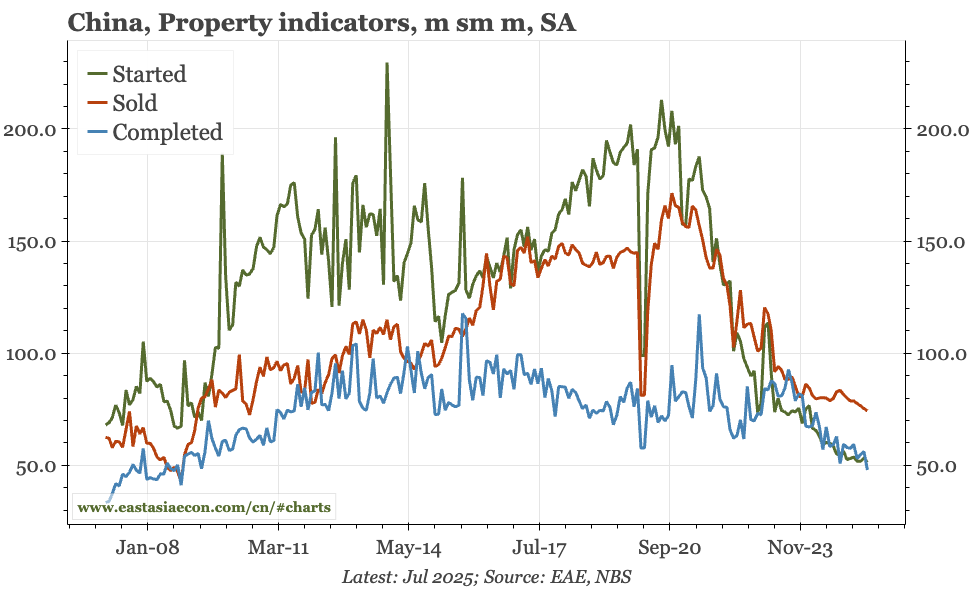

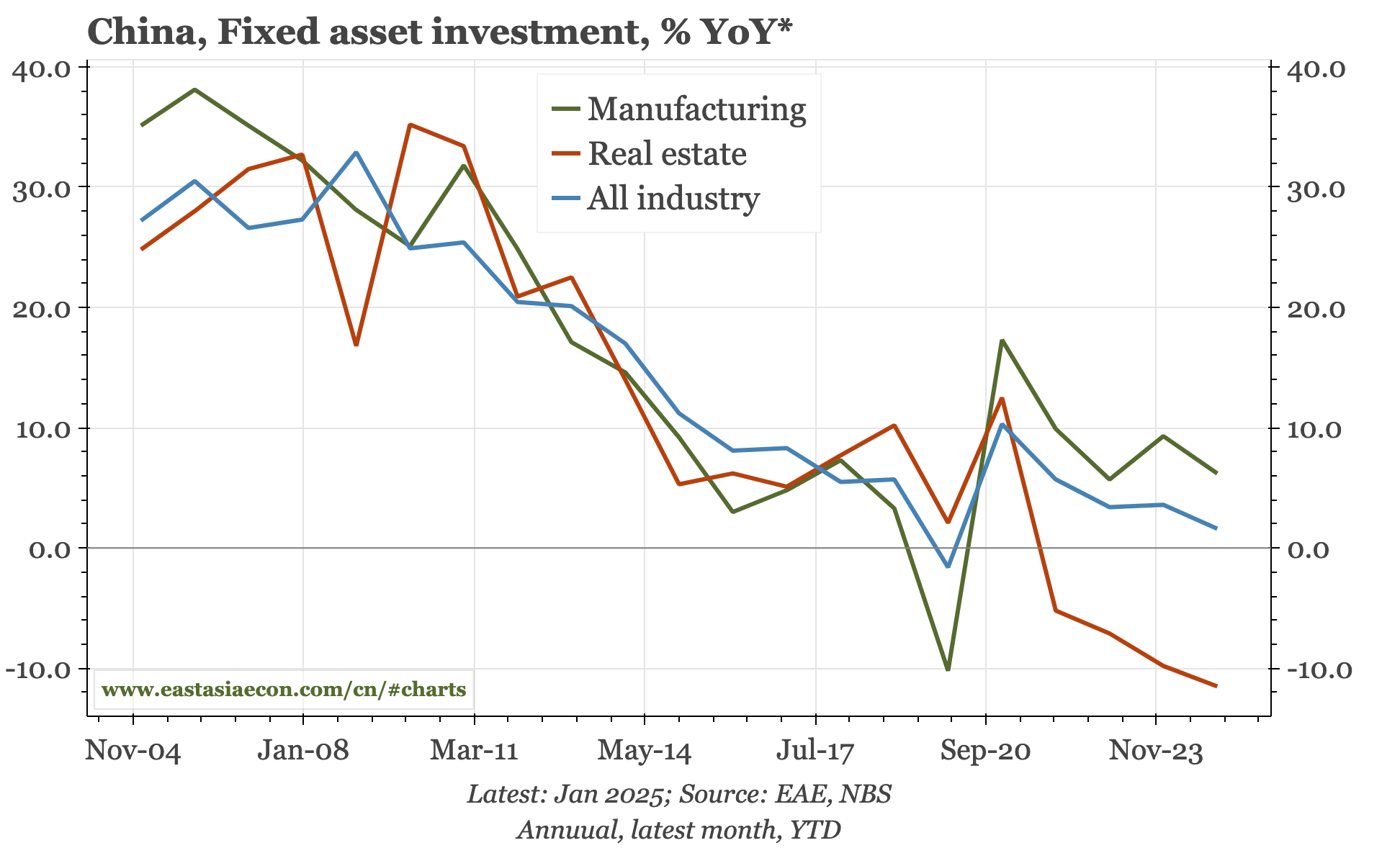

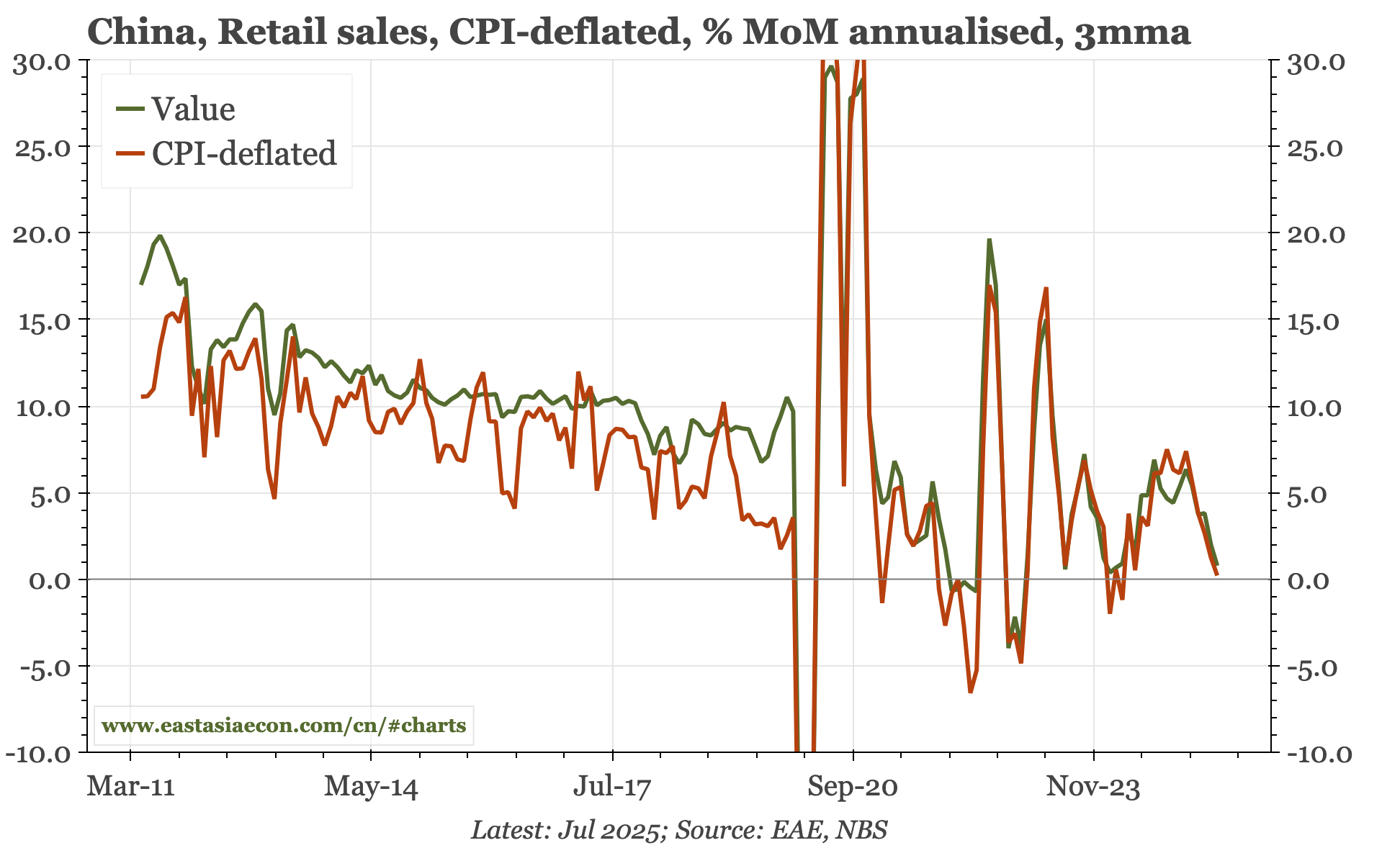

Softer again. Property prices and sales, investment and retail sales all deteriorated in July. It is at least possible to argue that the worst of the drop in property activity is now completed. That creates room for second-derivative improvement, but even that could be offset by slowing manufacturing capex.

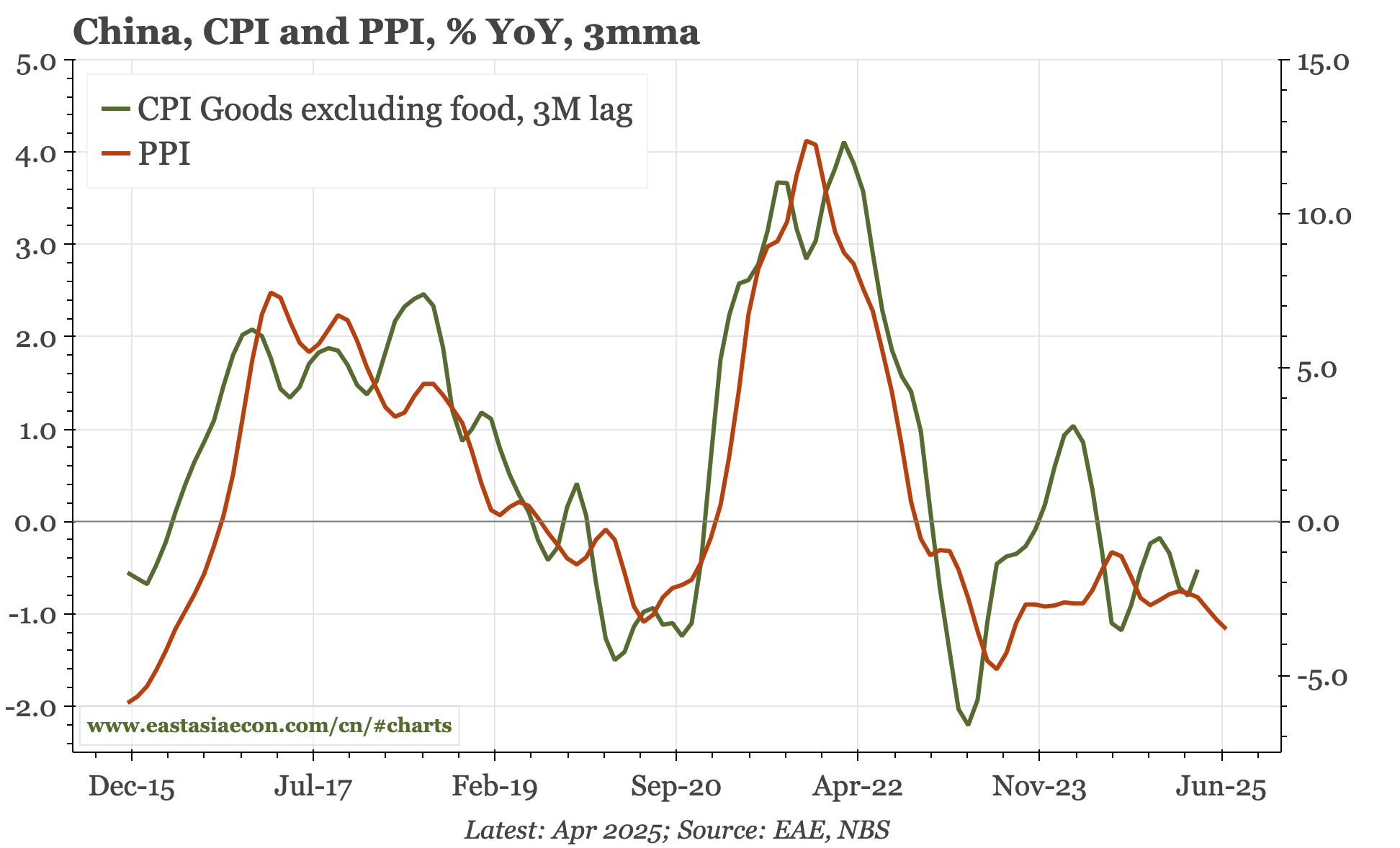

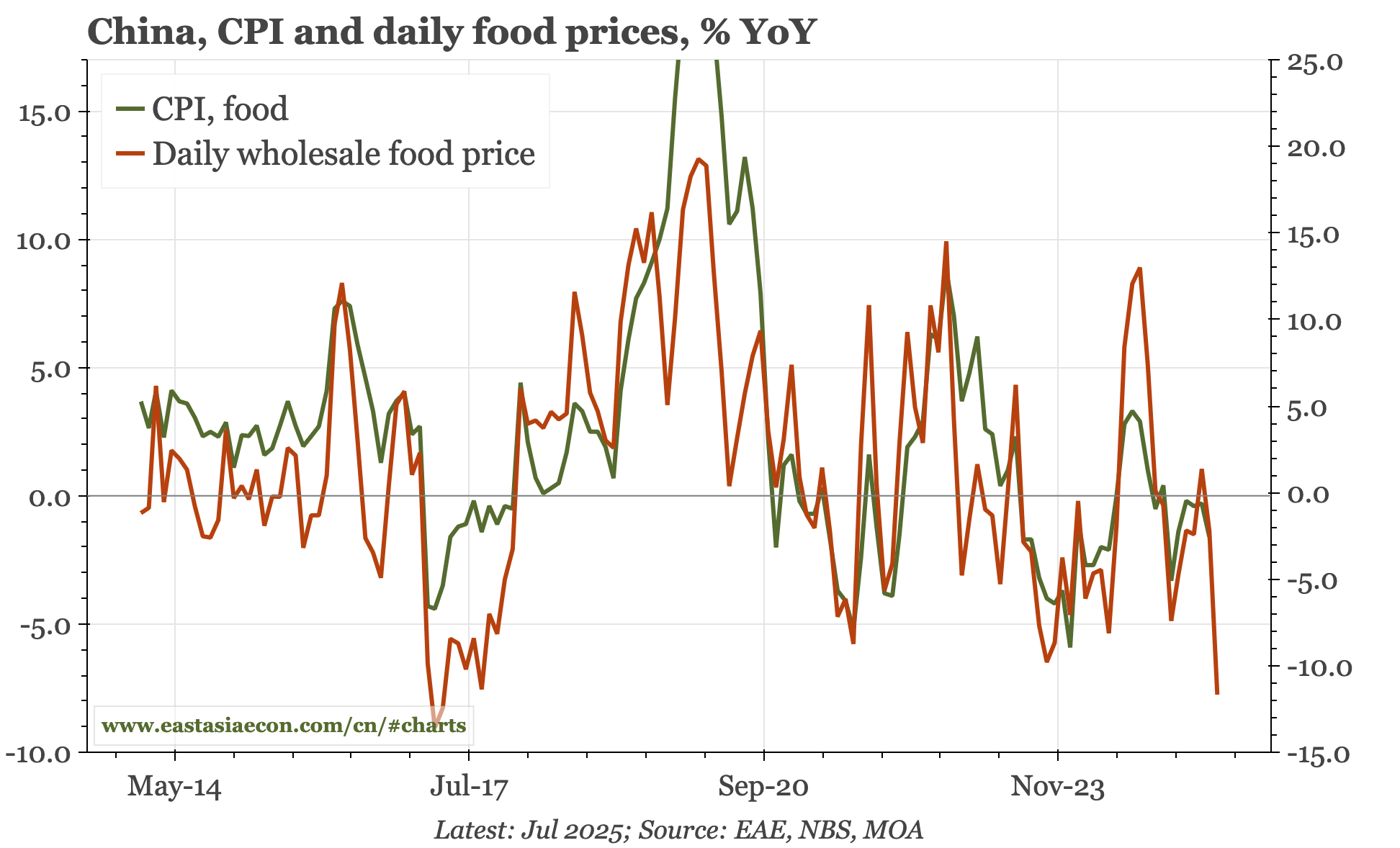

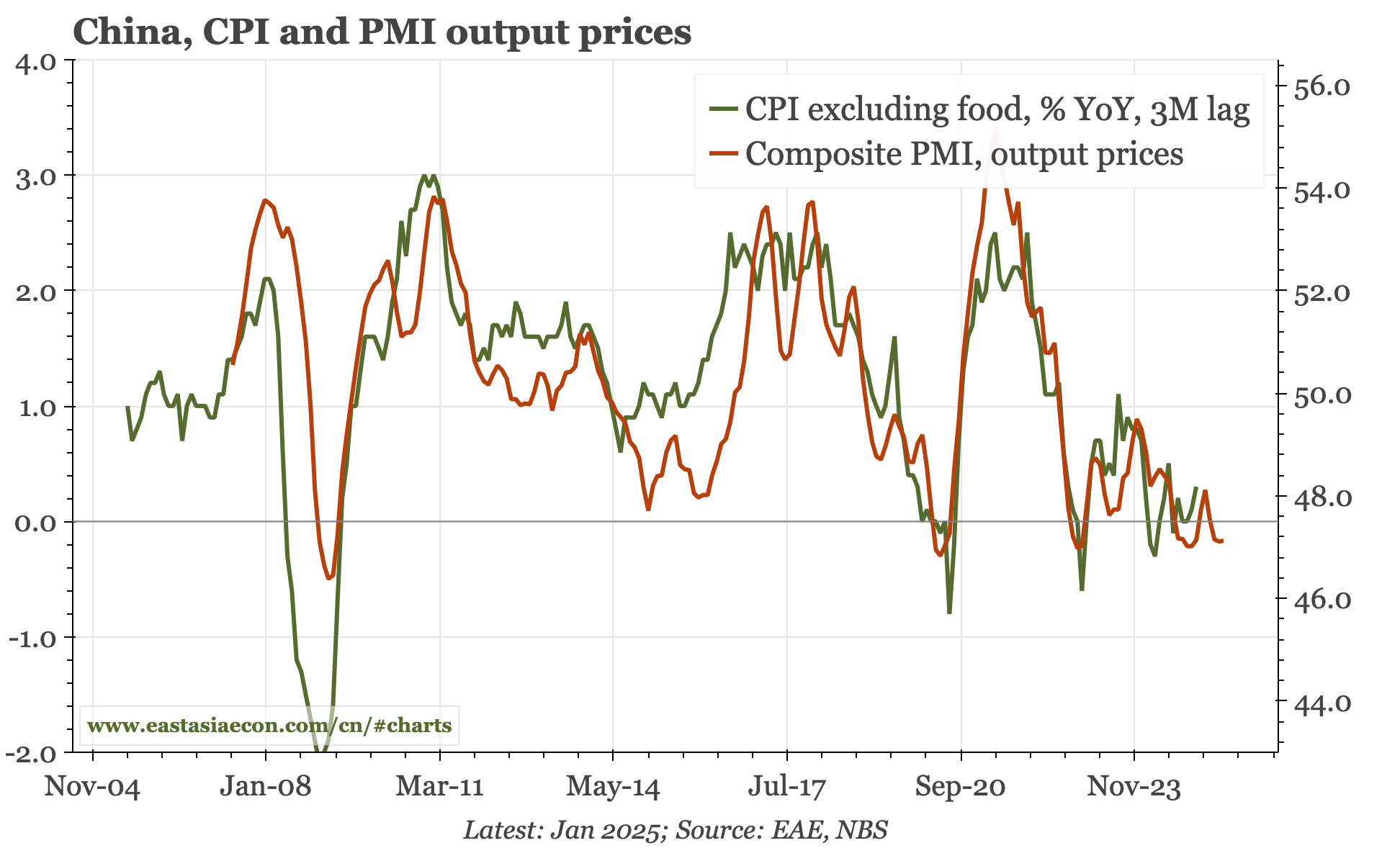

Prices

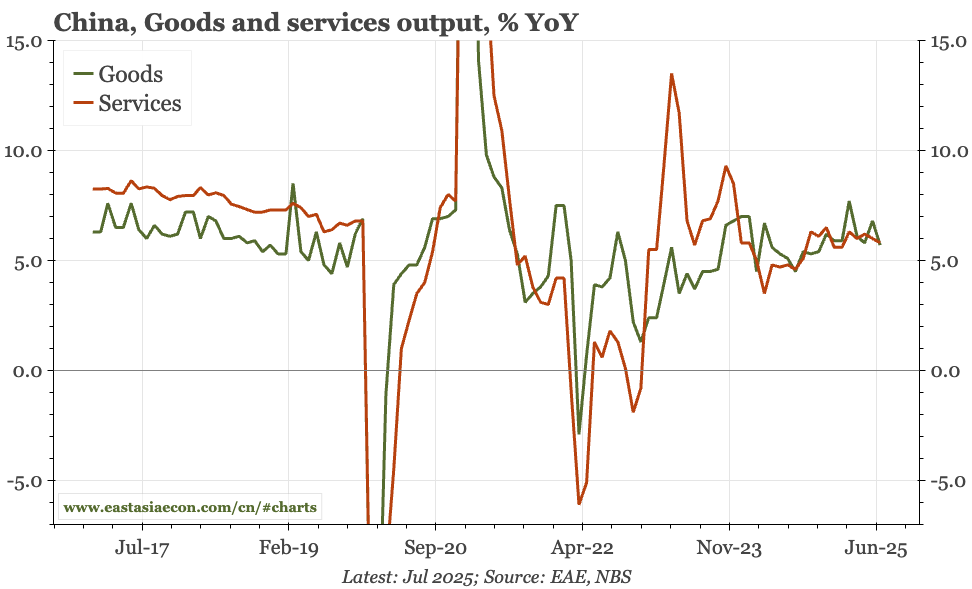

Activity

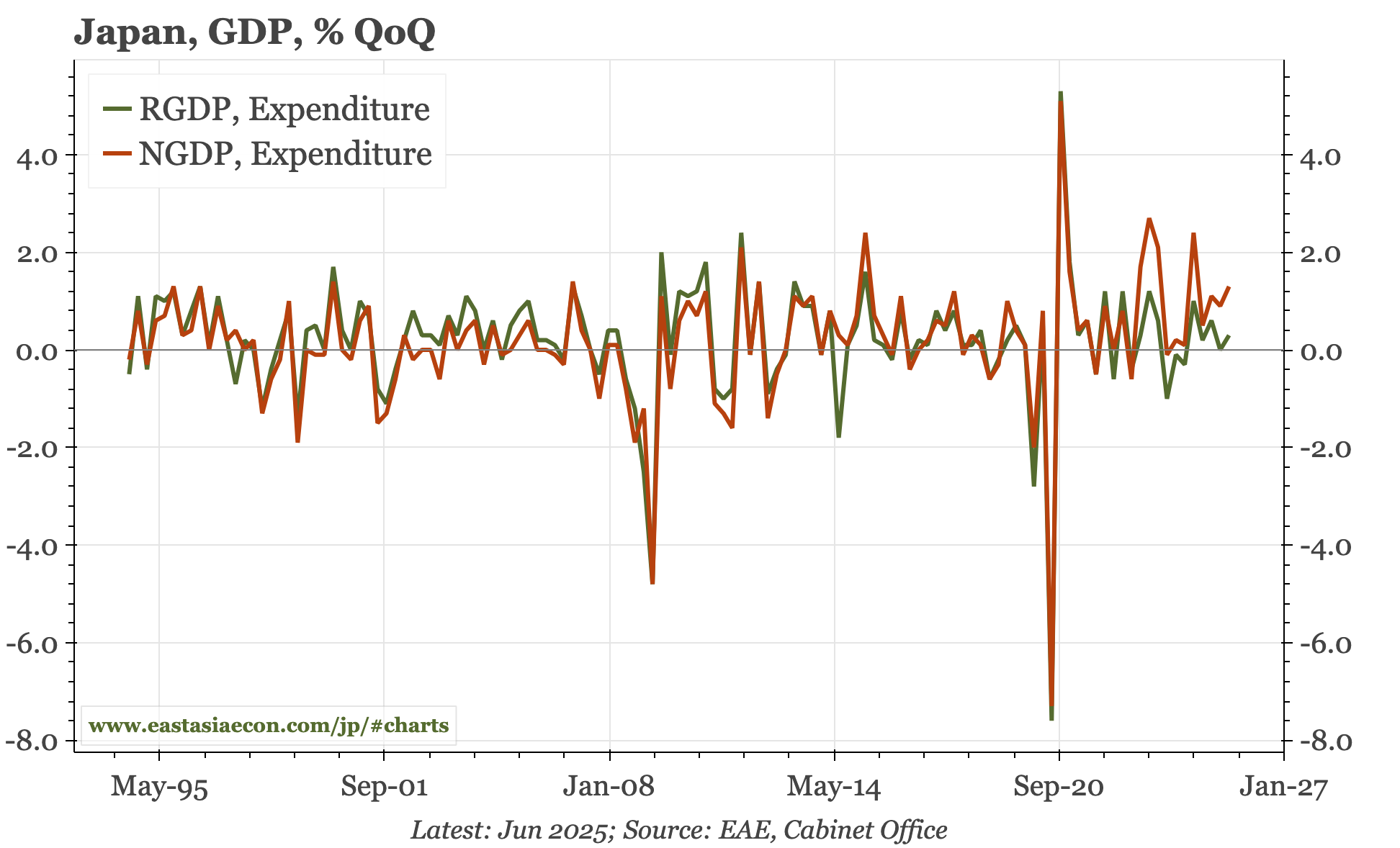

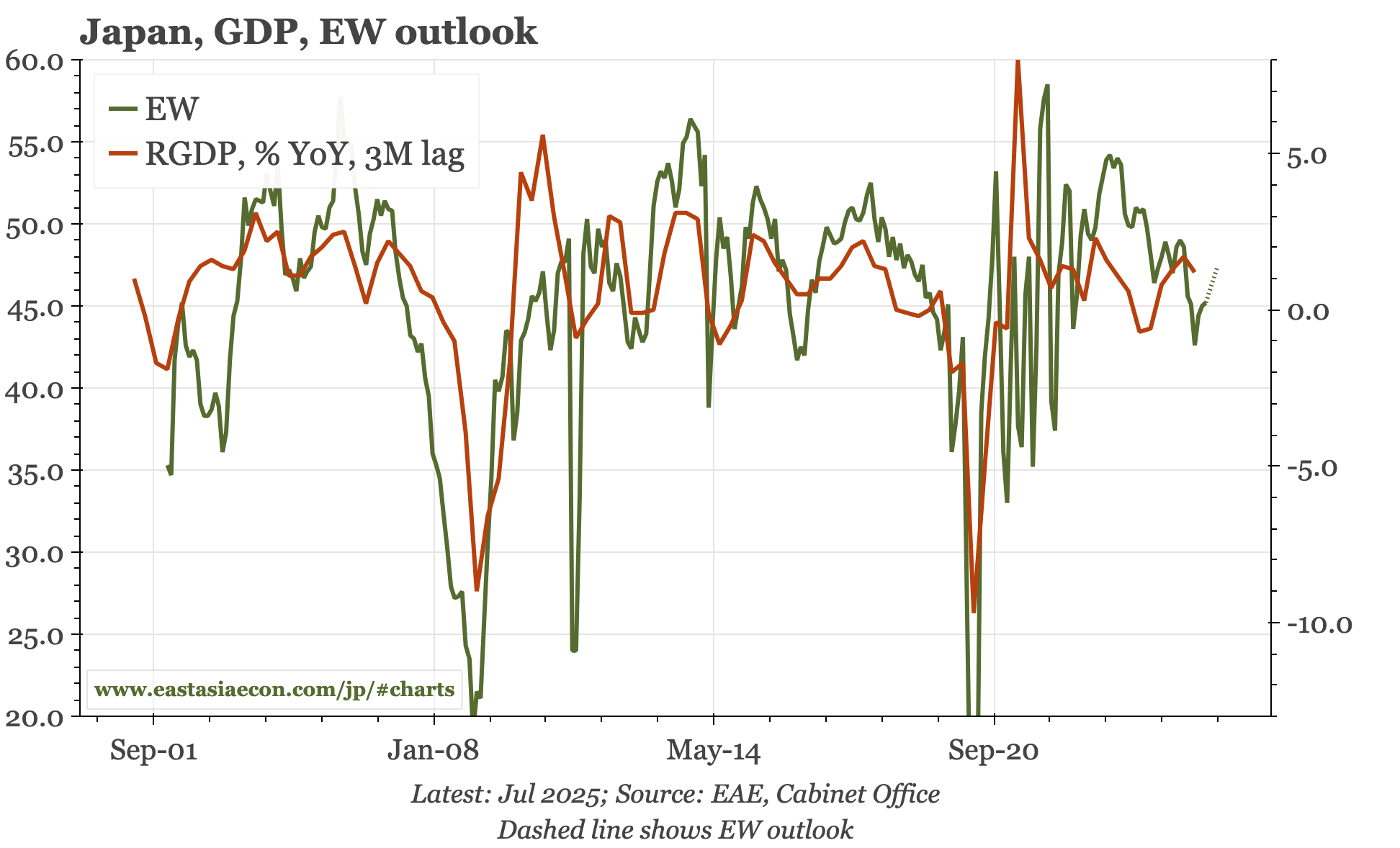

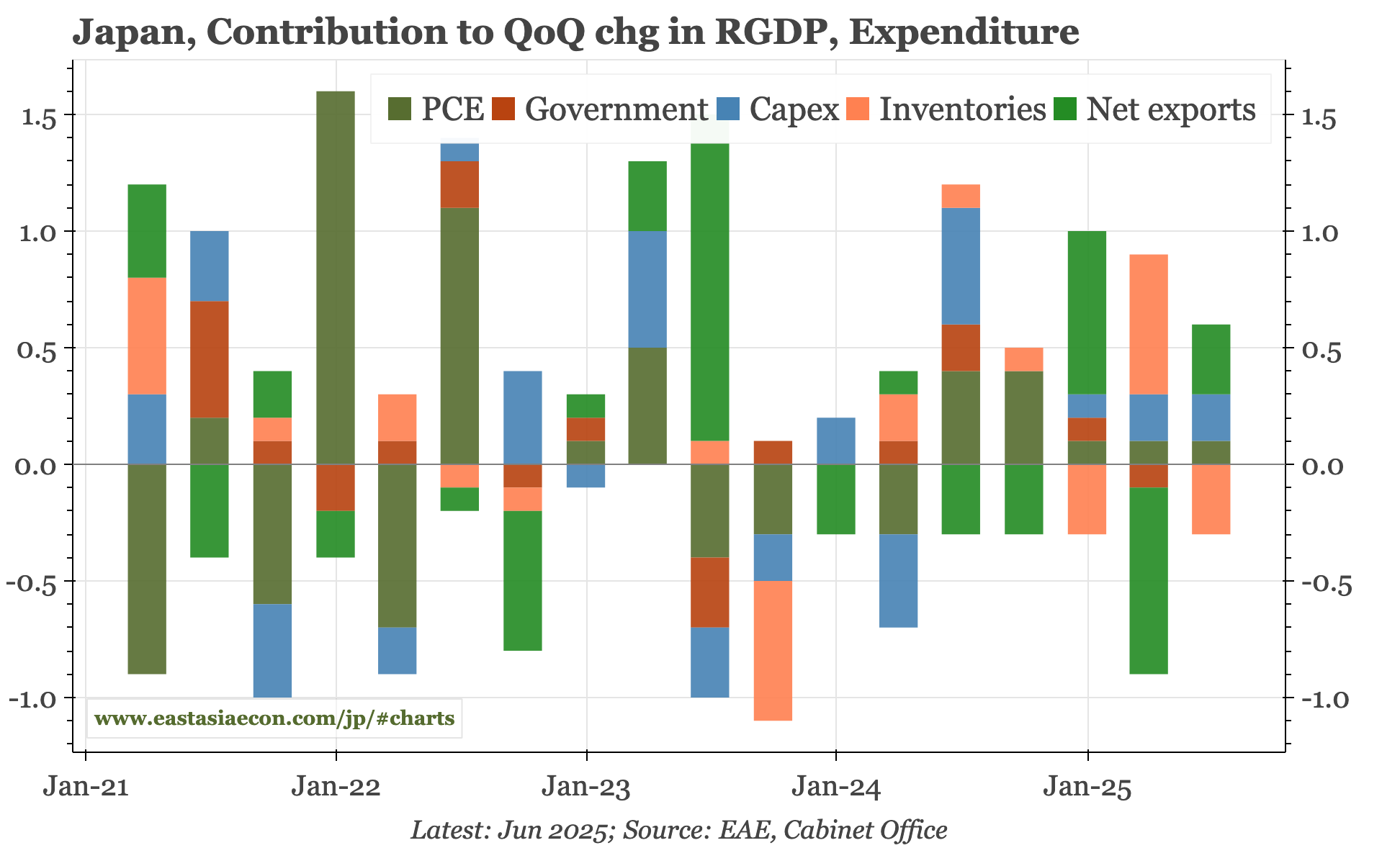

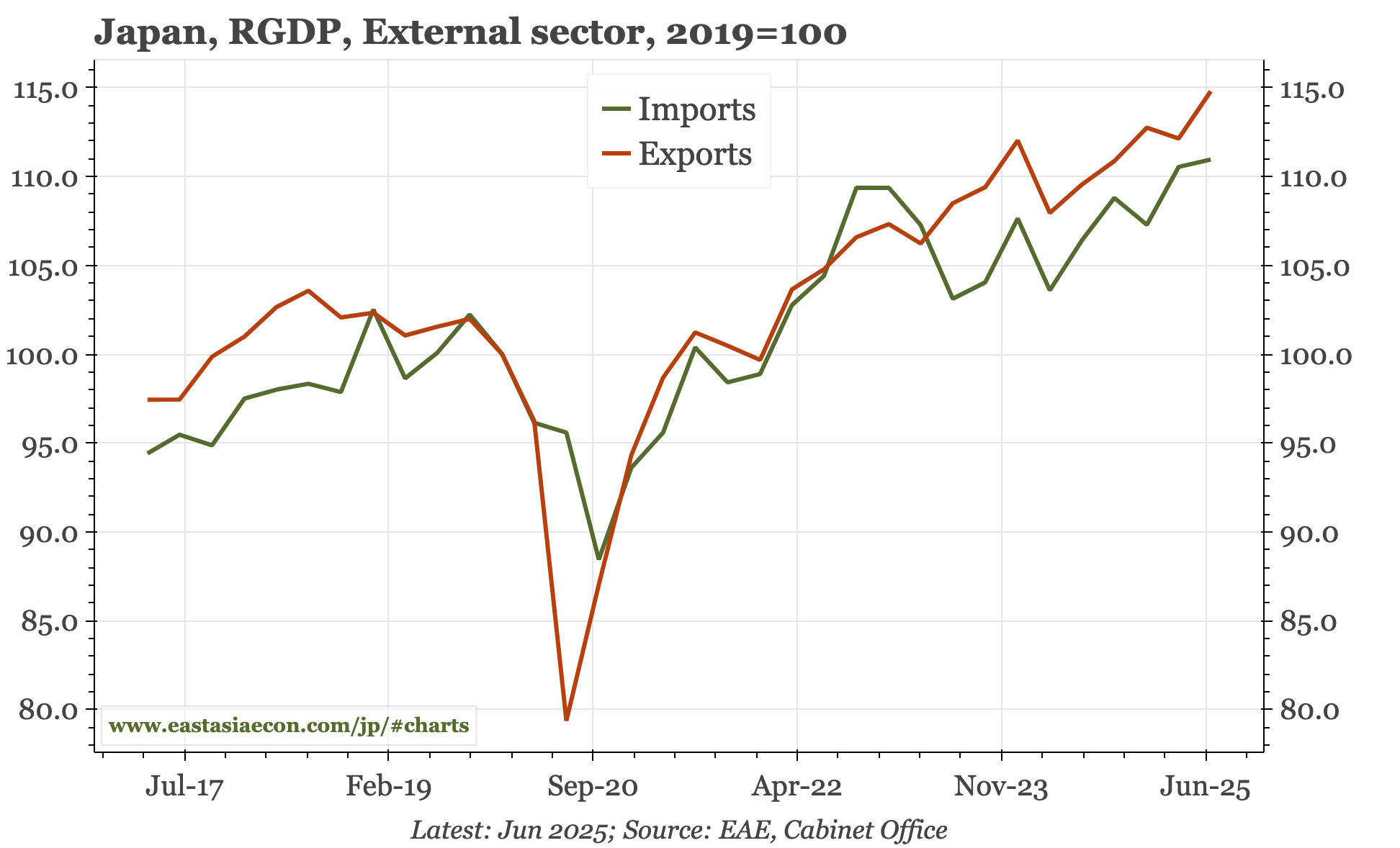

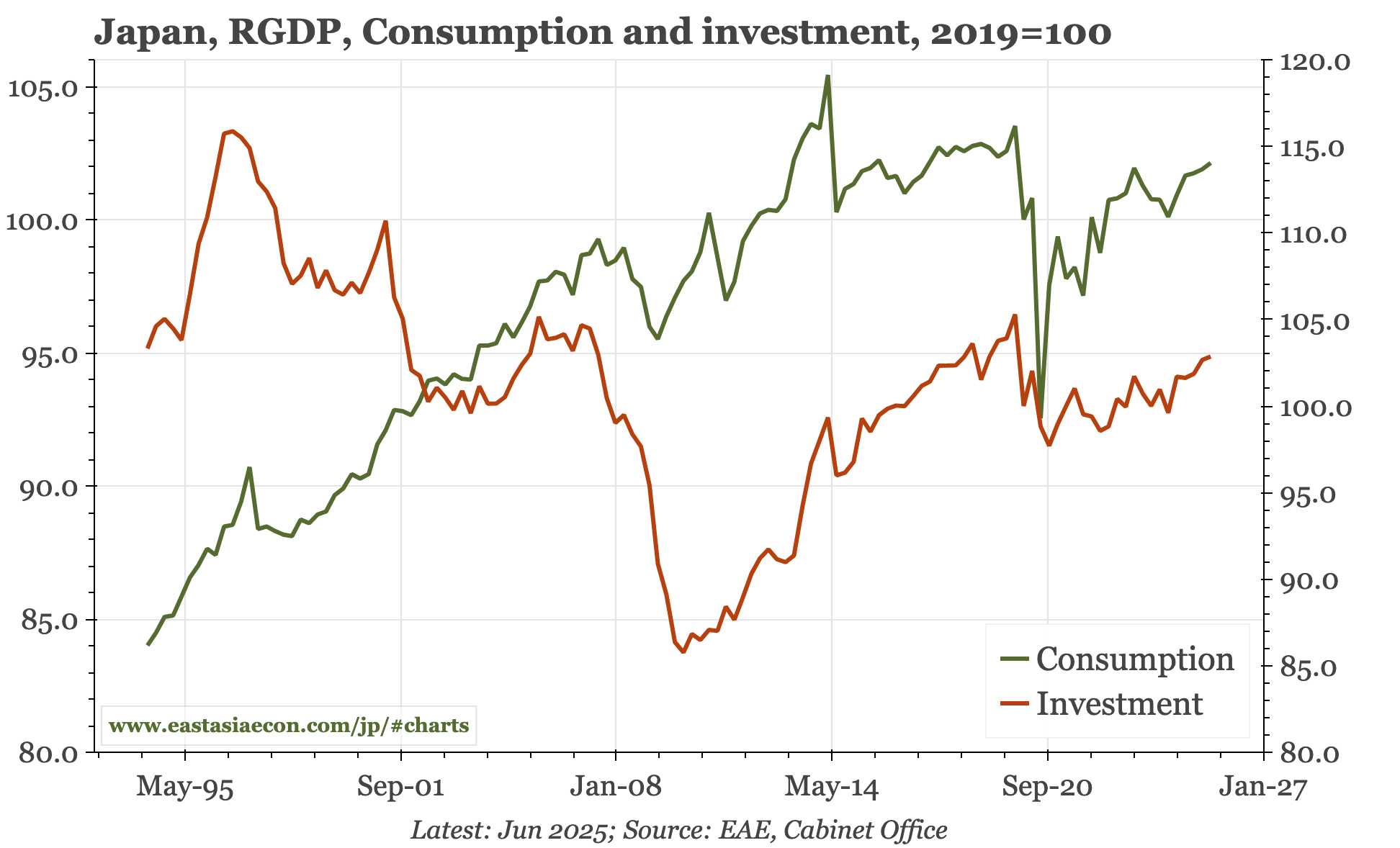

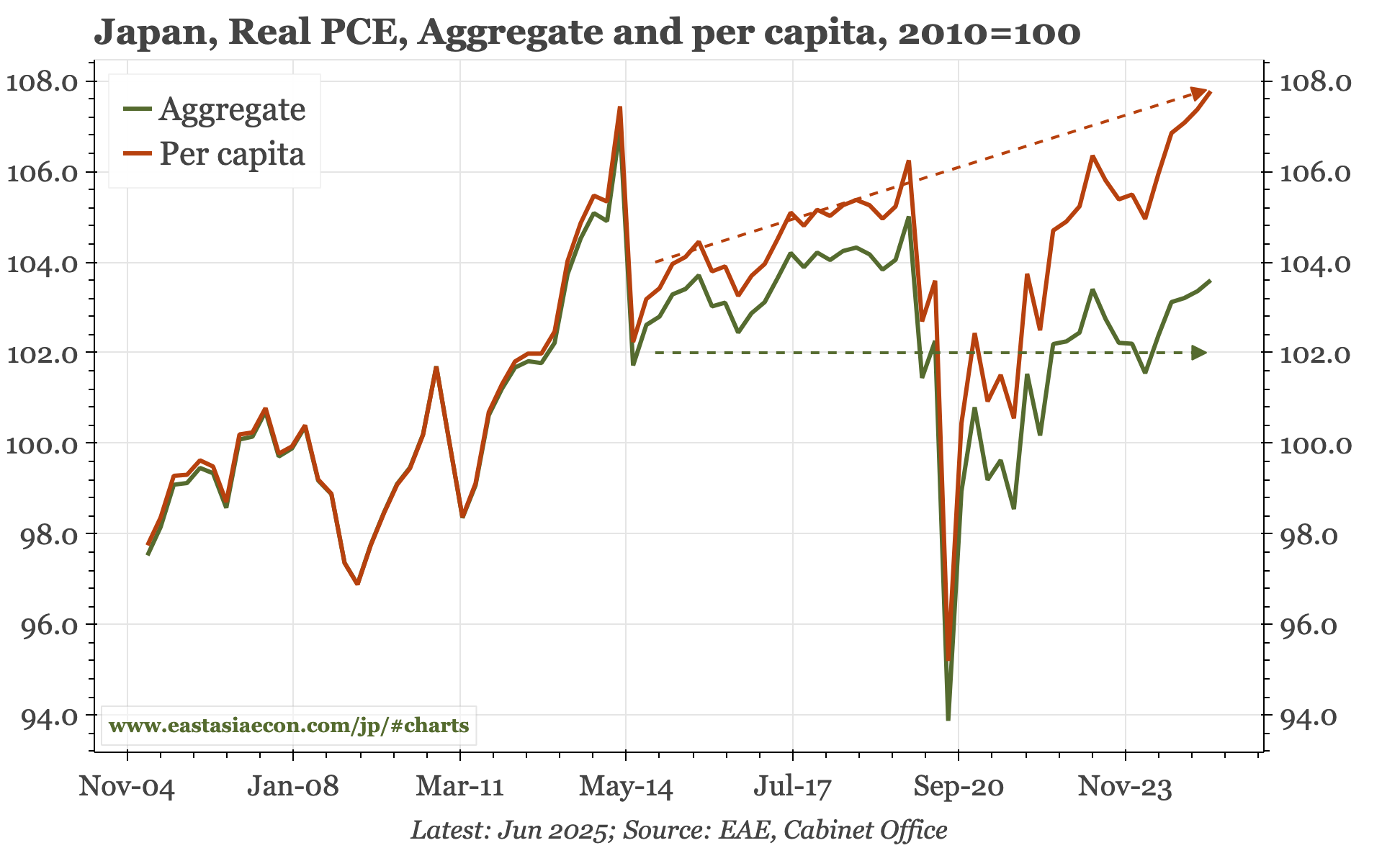

Solid GDP. Q2 GDP wasn't particularly impressive at headline level, but the details were firmer, with both consumption and investment rising. The recovery in aggregate consumption does remain sluggish, but that is partly because of population loss. I estimate per capita consumption in Q2 reached a record high.

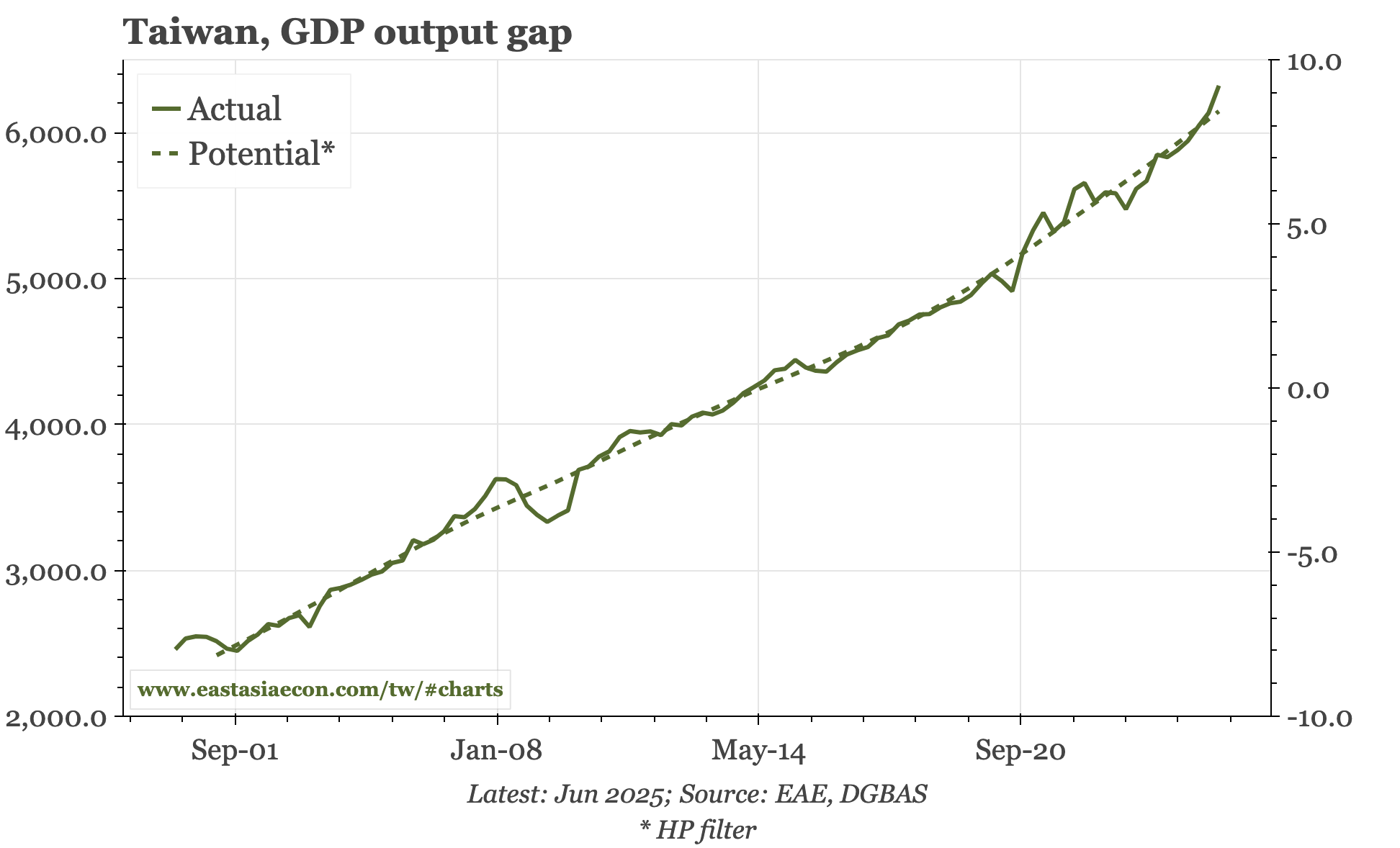

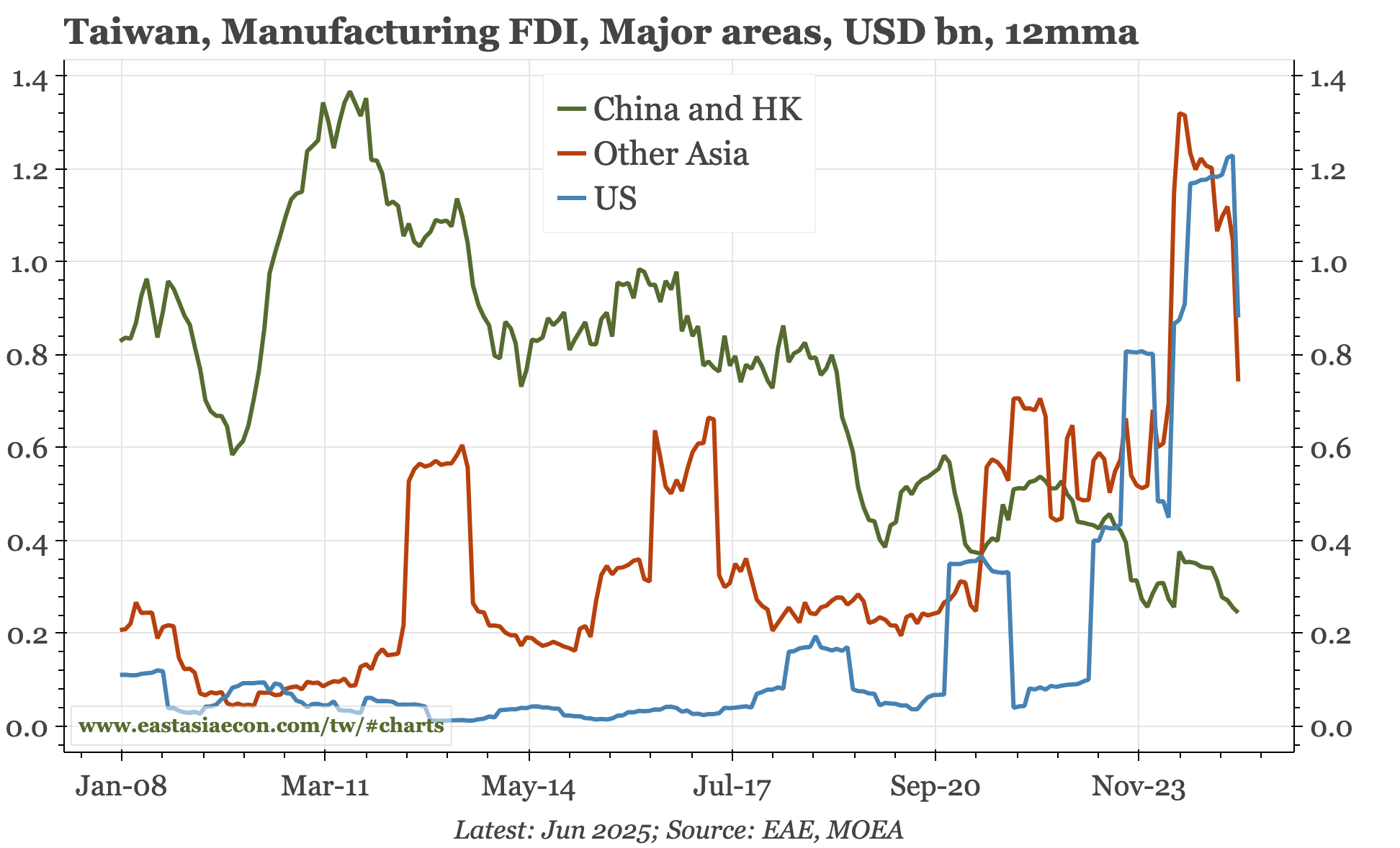

Less worried on exports. The government today confirmed the export surge of 1H – and released much less pessimistic forecasts for 2H. The underlying story is simple: AI-related demand offsetting the impact of TWD appreciation and tariffs. Exports are now expected to grow almost 25% this year, and GDP by 4.5%.