East Asia Today

More on inflation pressures in Asia, with the details of the Japan Tankan, and Korea March CPI. Also, export price deflation in China being less than often supposed, one of the highlights of February trade in volume and price terms.

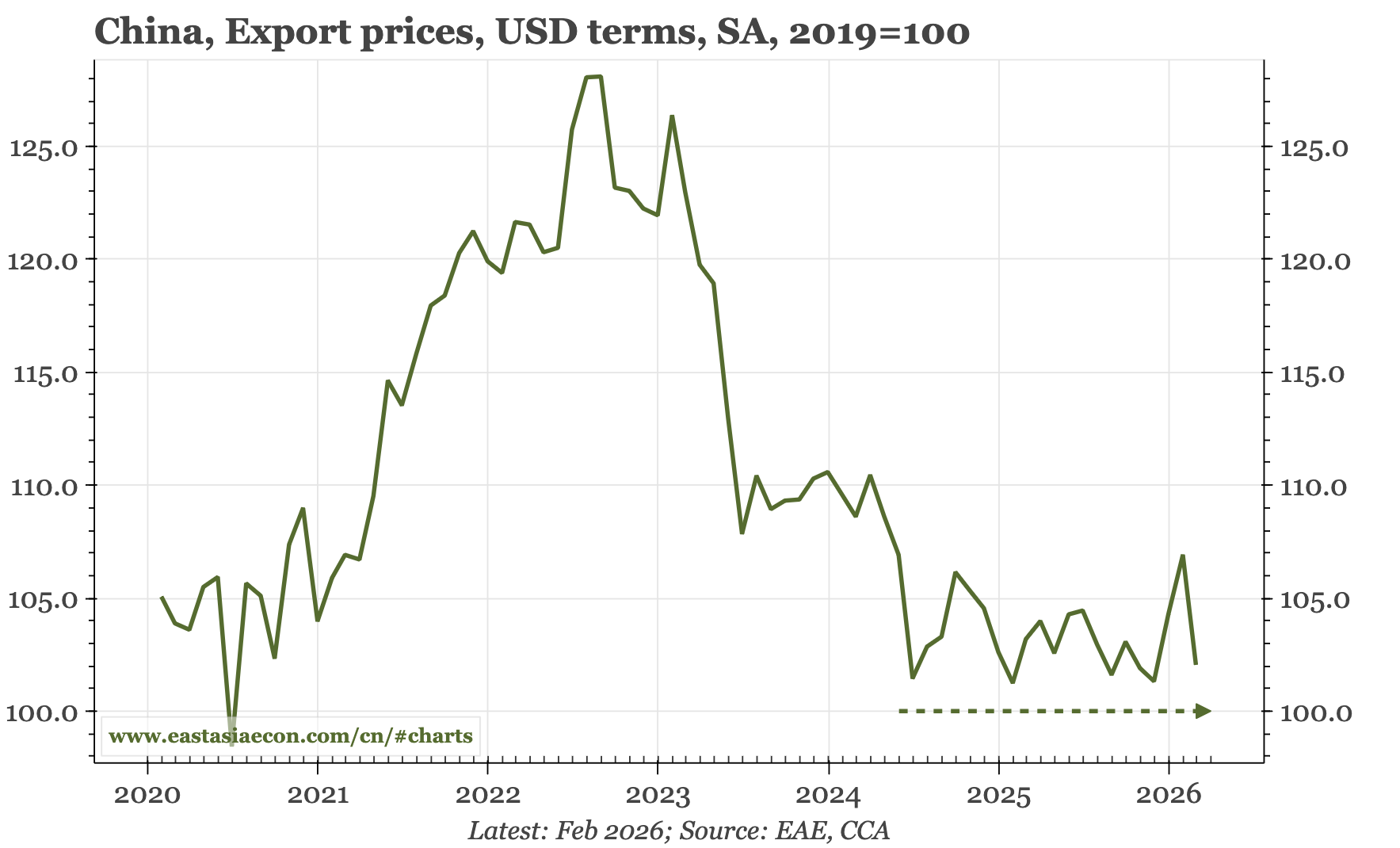

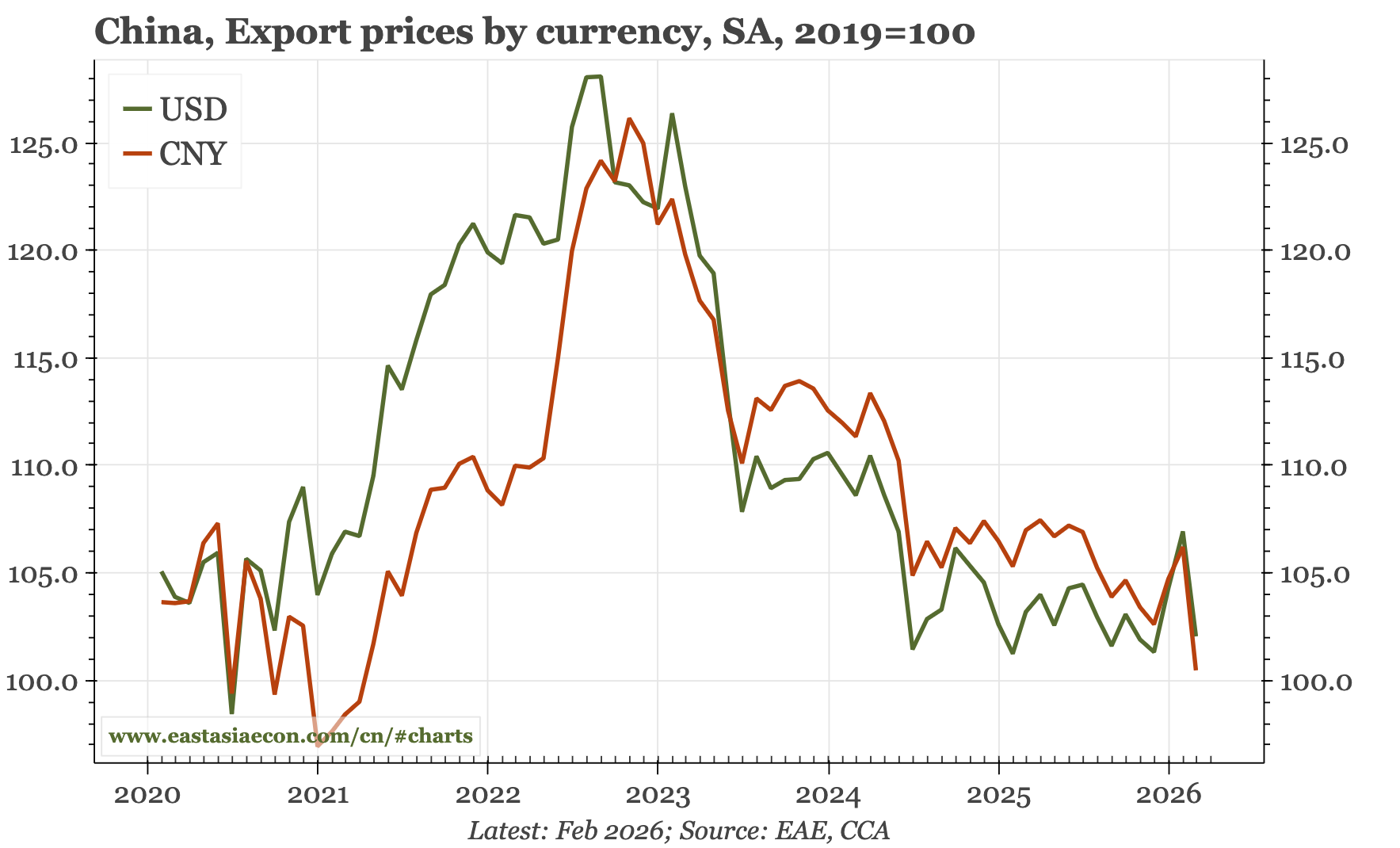

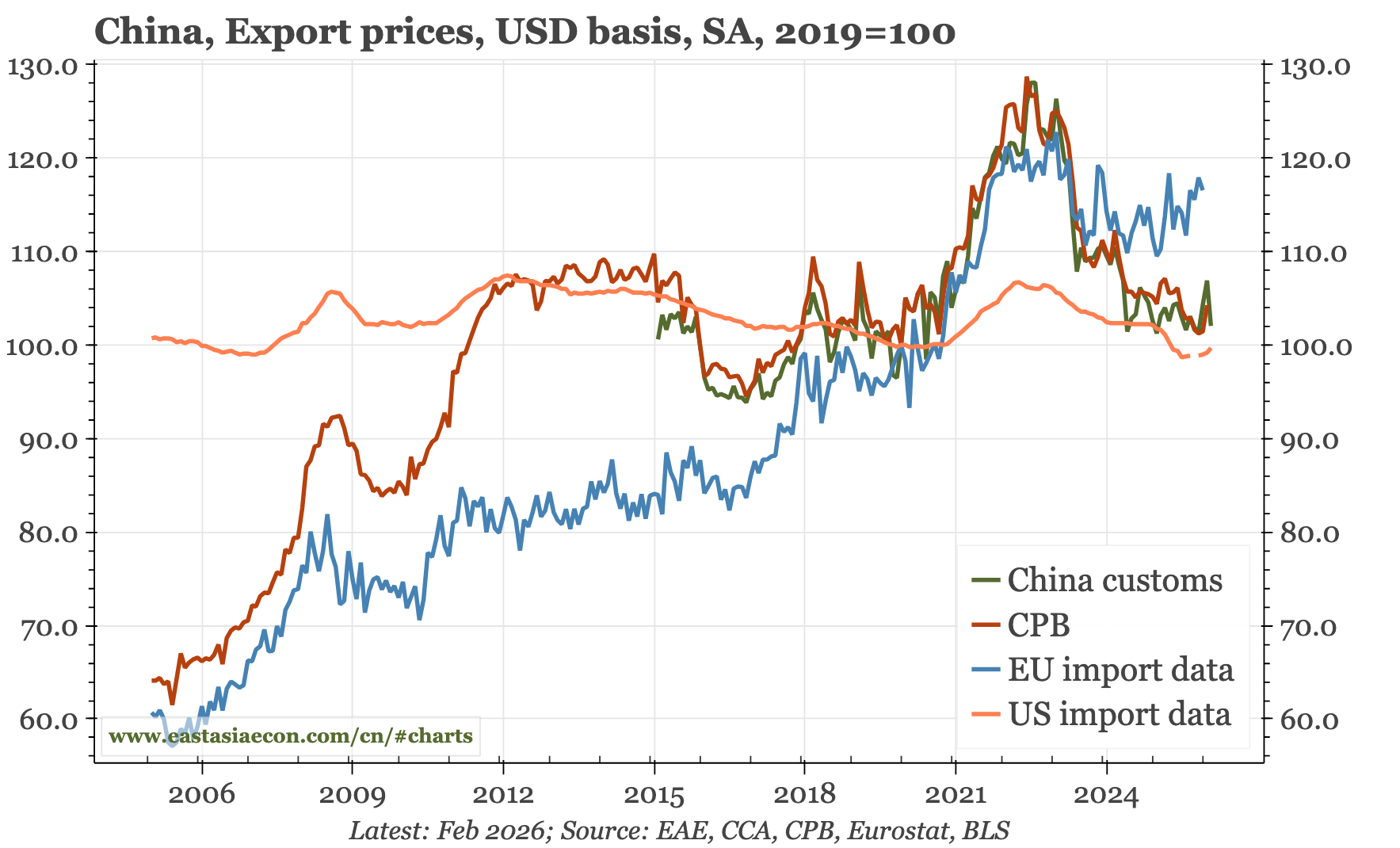

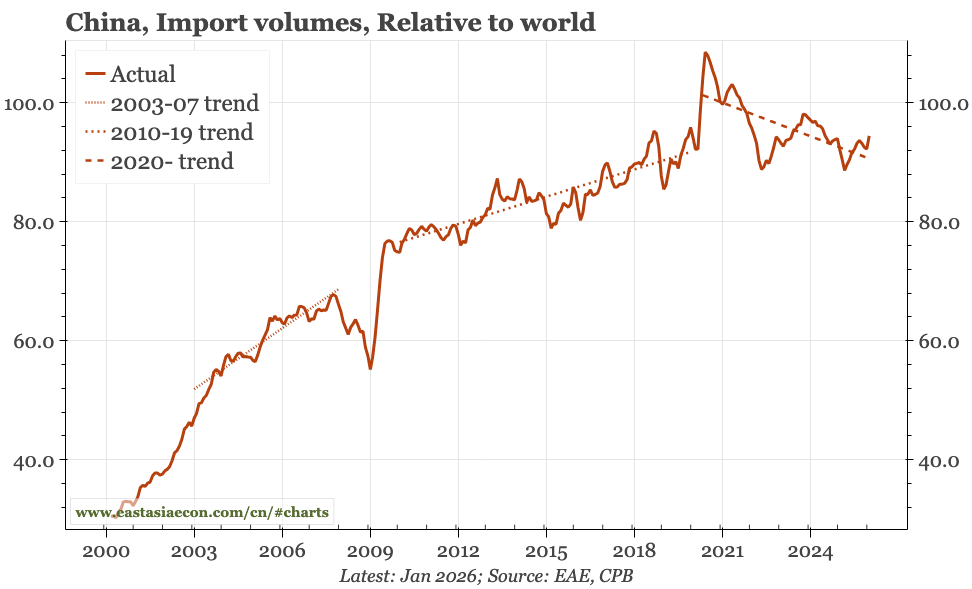

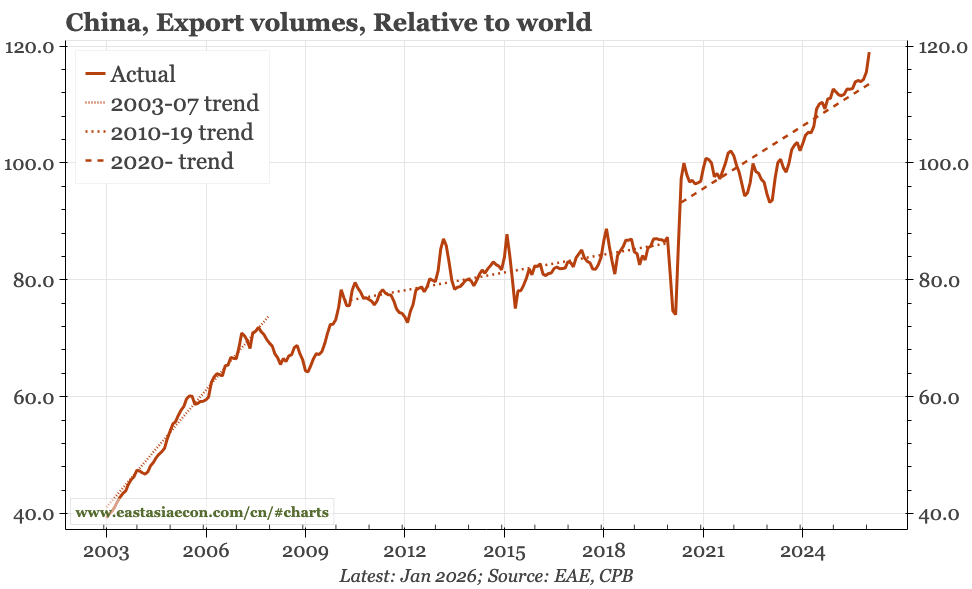

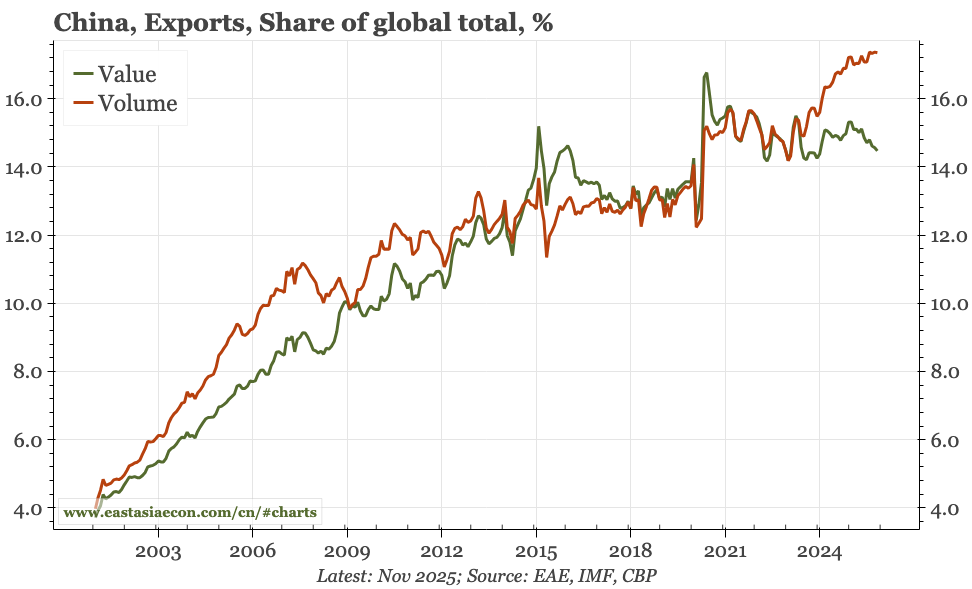

While PPI will likely rise YoY in March for the first since 2022, the stabilisation of prices actually began in June. One driver has been the rise in import prices, a trend that continued in February. Export prices also aren't falling; indeed, while there is always volatility at the beginning of the year, export prices in USD terms remain in the same sideways range they've been in since 2024. That isn't inconsistent with the continued rise in export volumes; while not falling, China's export prices might still be below those of other counties for the same product.

If you aren't yet a subscriber, please consider becoming one! This daily product is designed for individuals, but we also have data services and a much more comprehensive offering for financial institutions. If you have any questions or feedback, please get in touch with me directly.

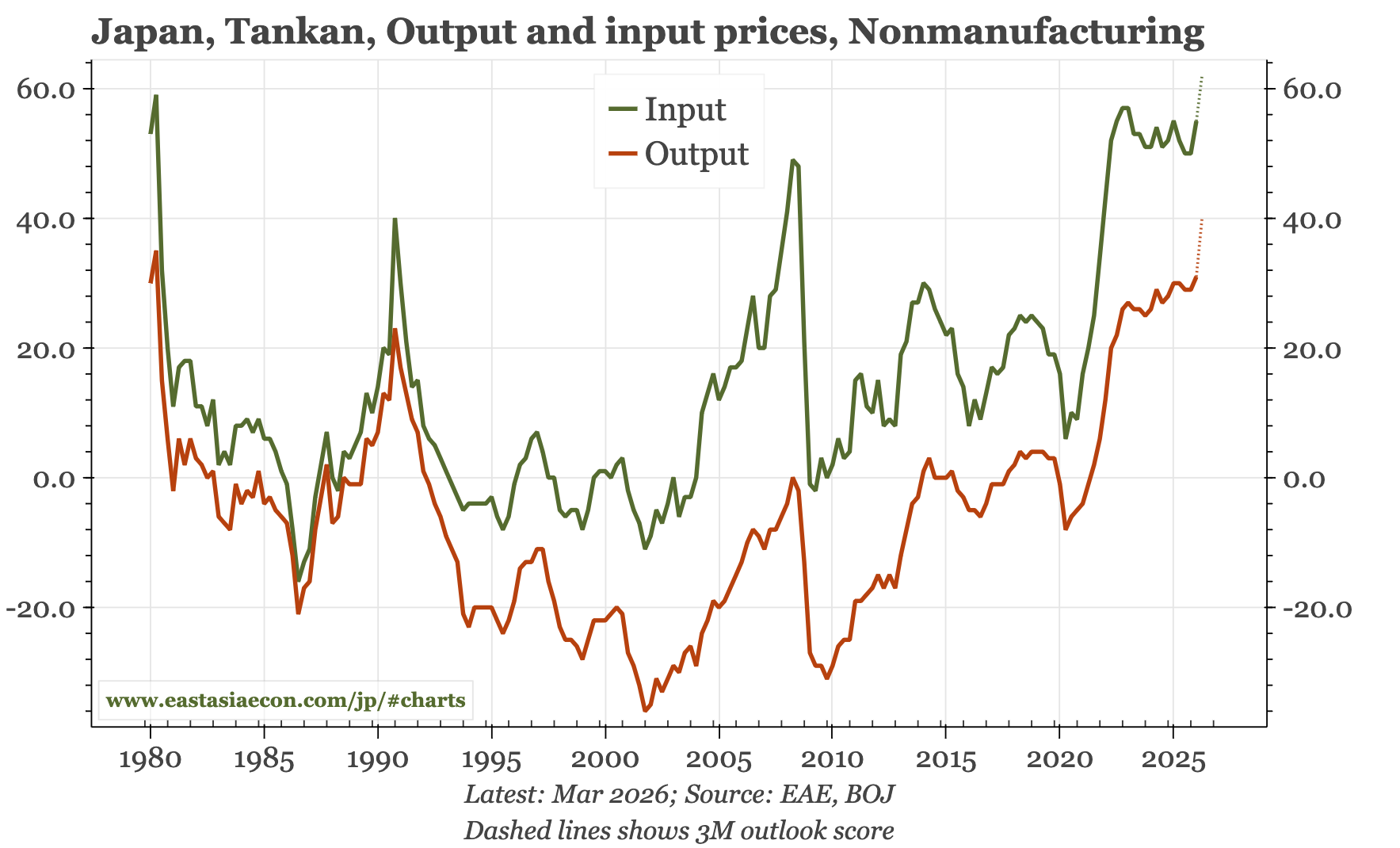

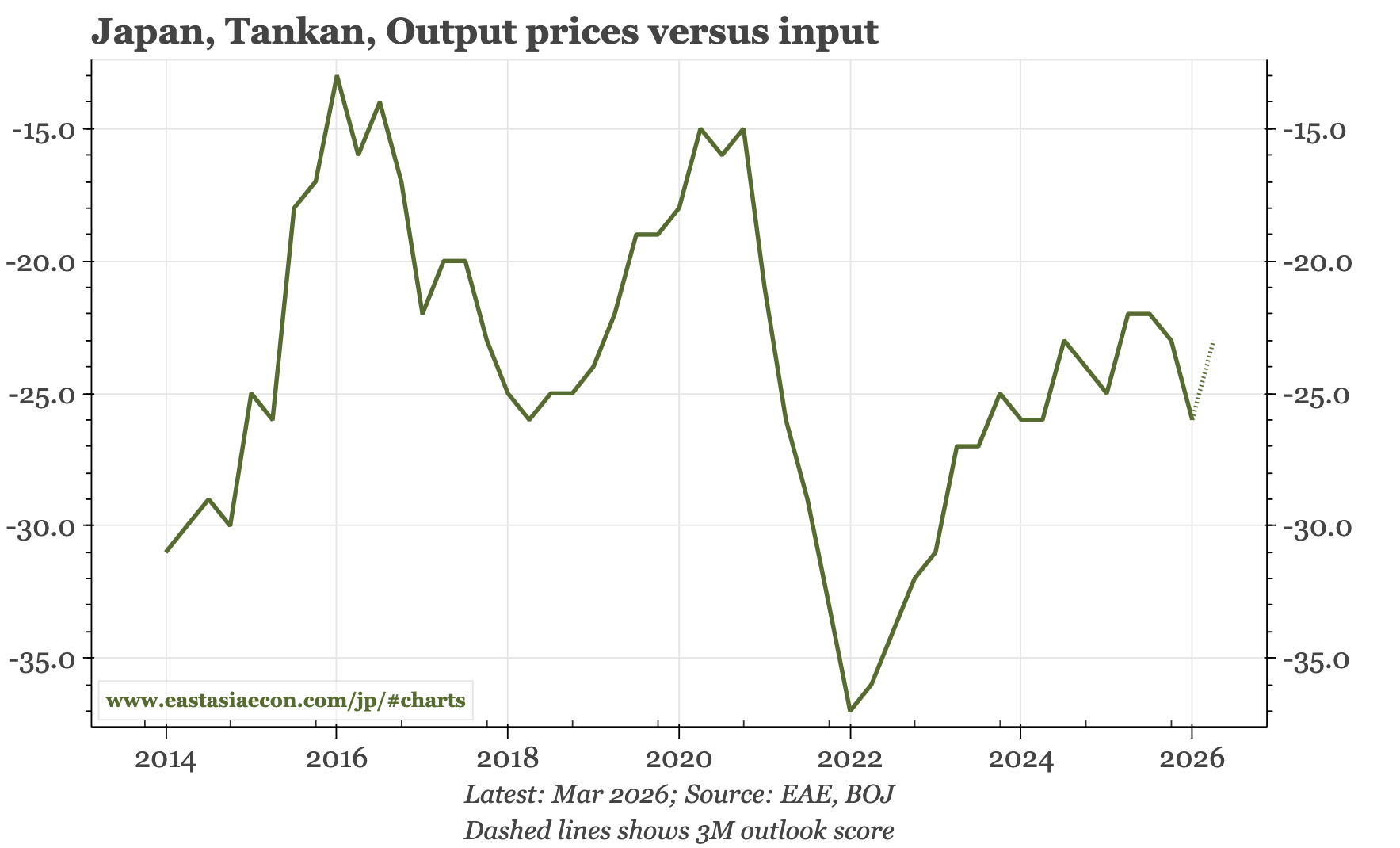

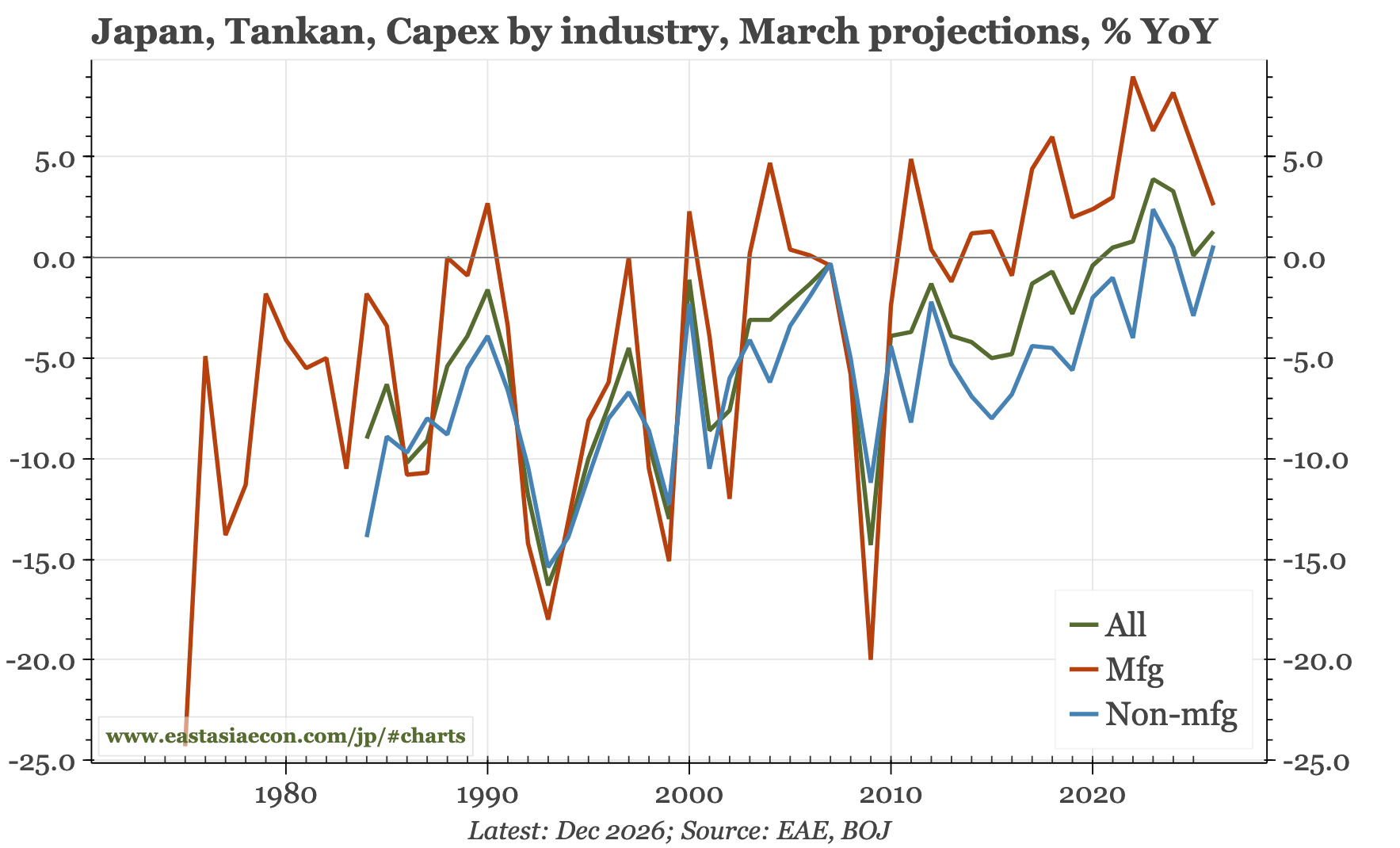

Cycle update – output prices rise more than input. The inflation risks evident in the Tankan can be blamed on energy prices, but output prices actually rose more than input, suggesting that firms think they can pass costs through. That's important, when the BOJ has been warning that changes in firm behaviour mean upside risks to inflation.

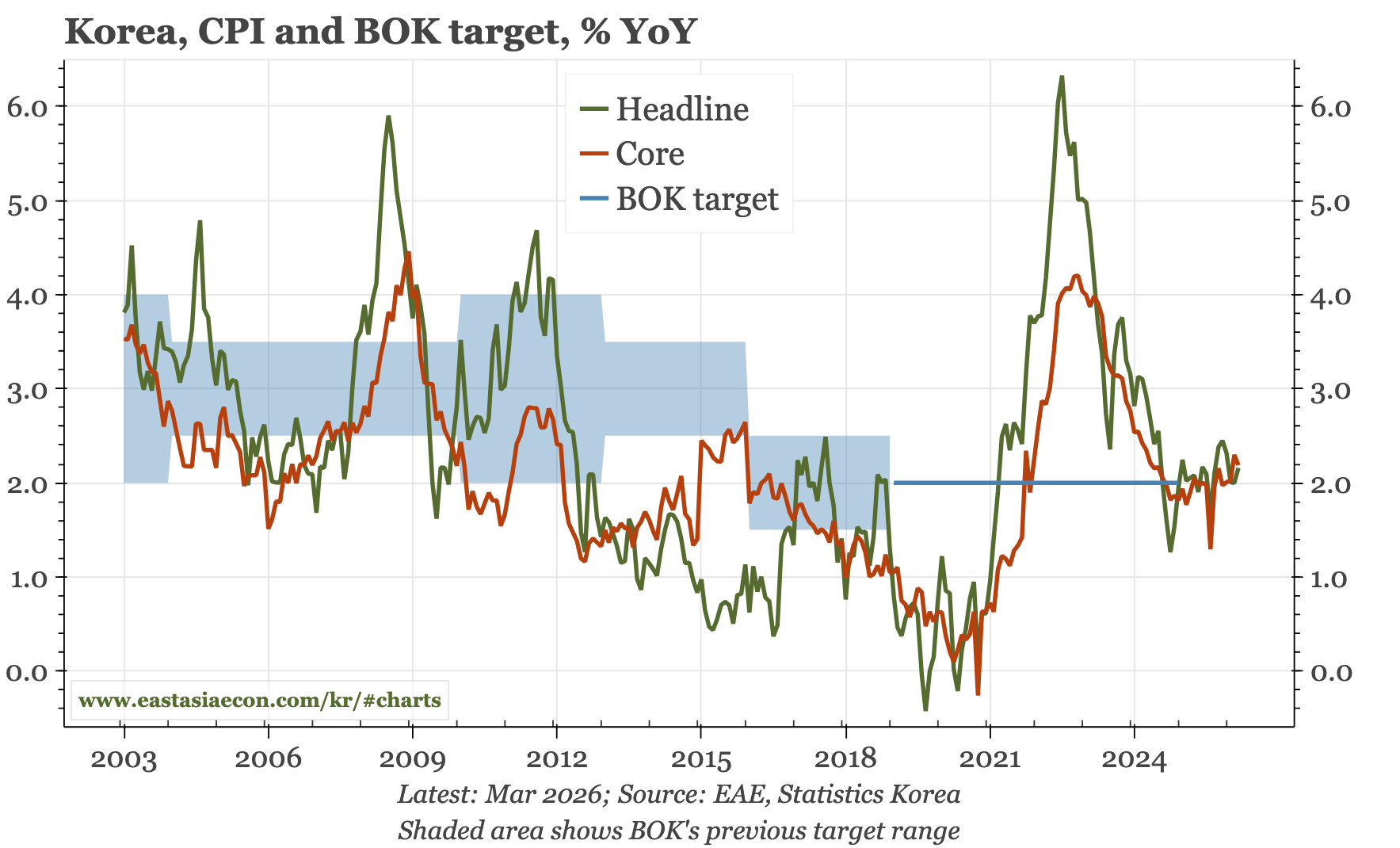

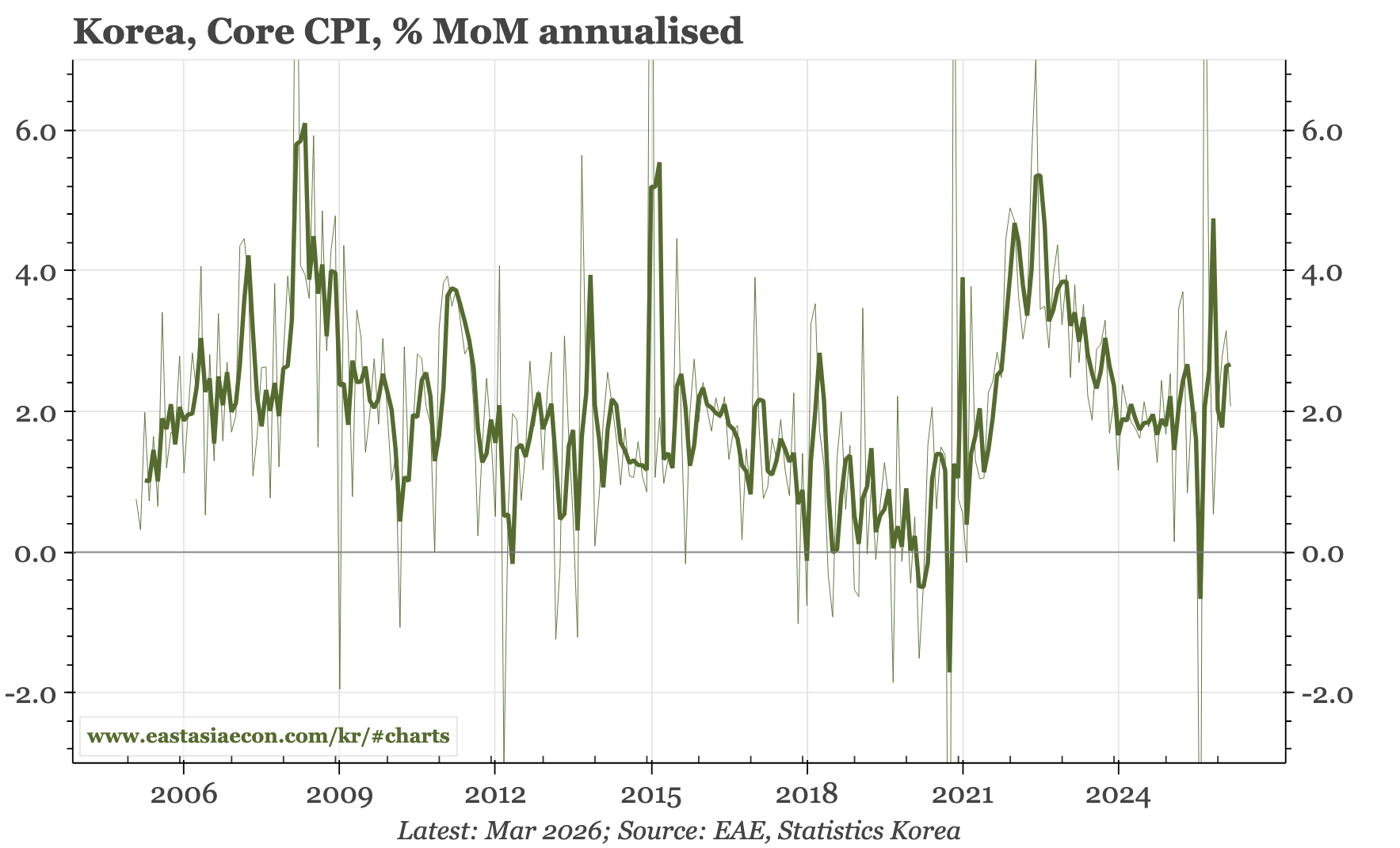

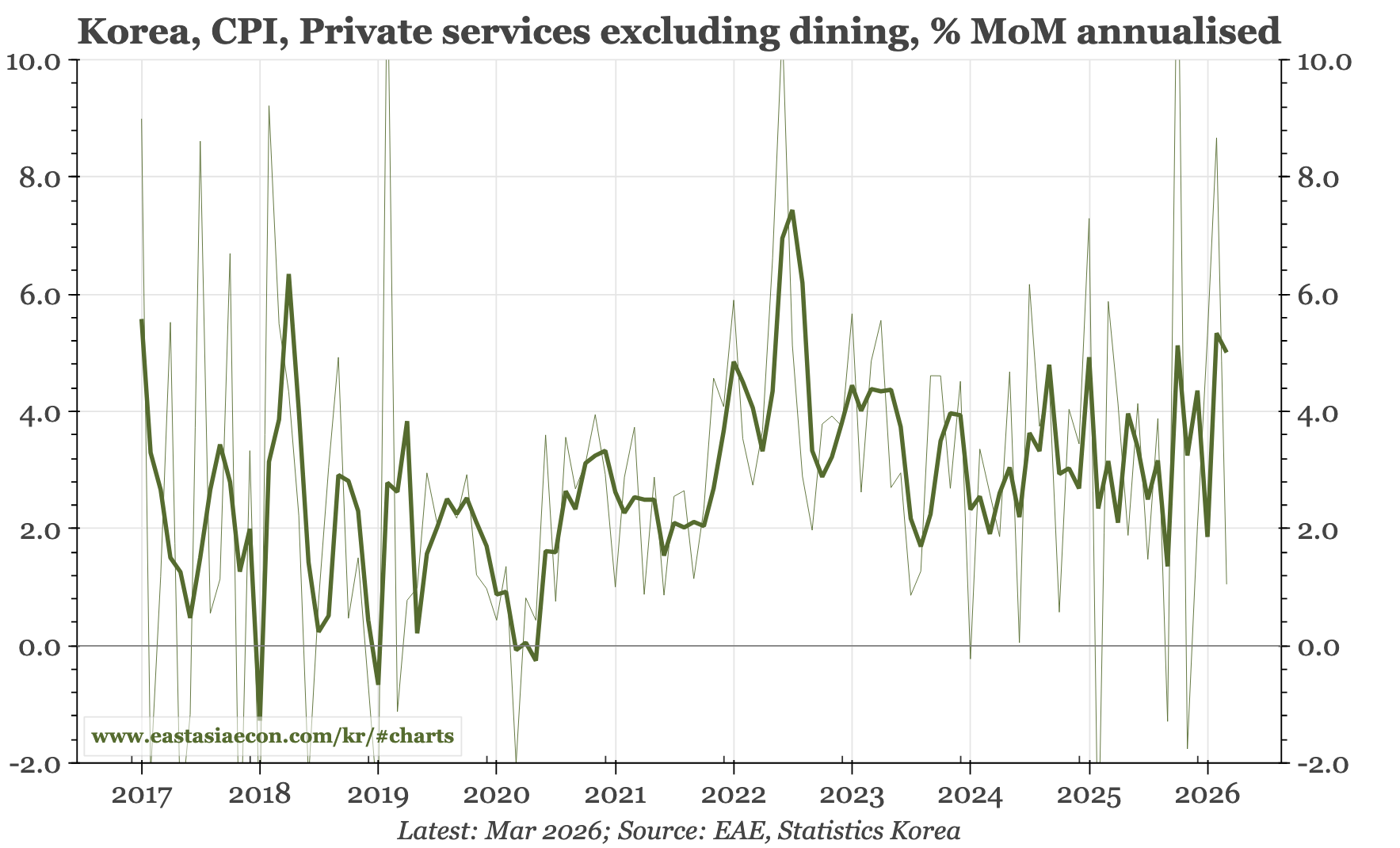

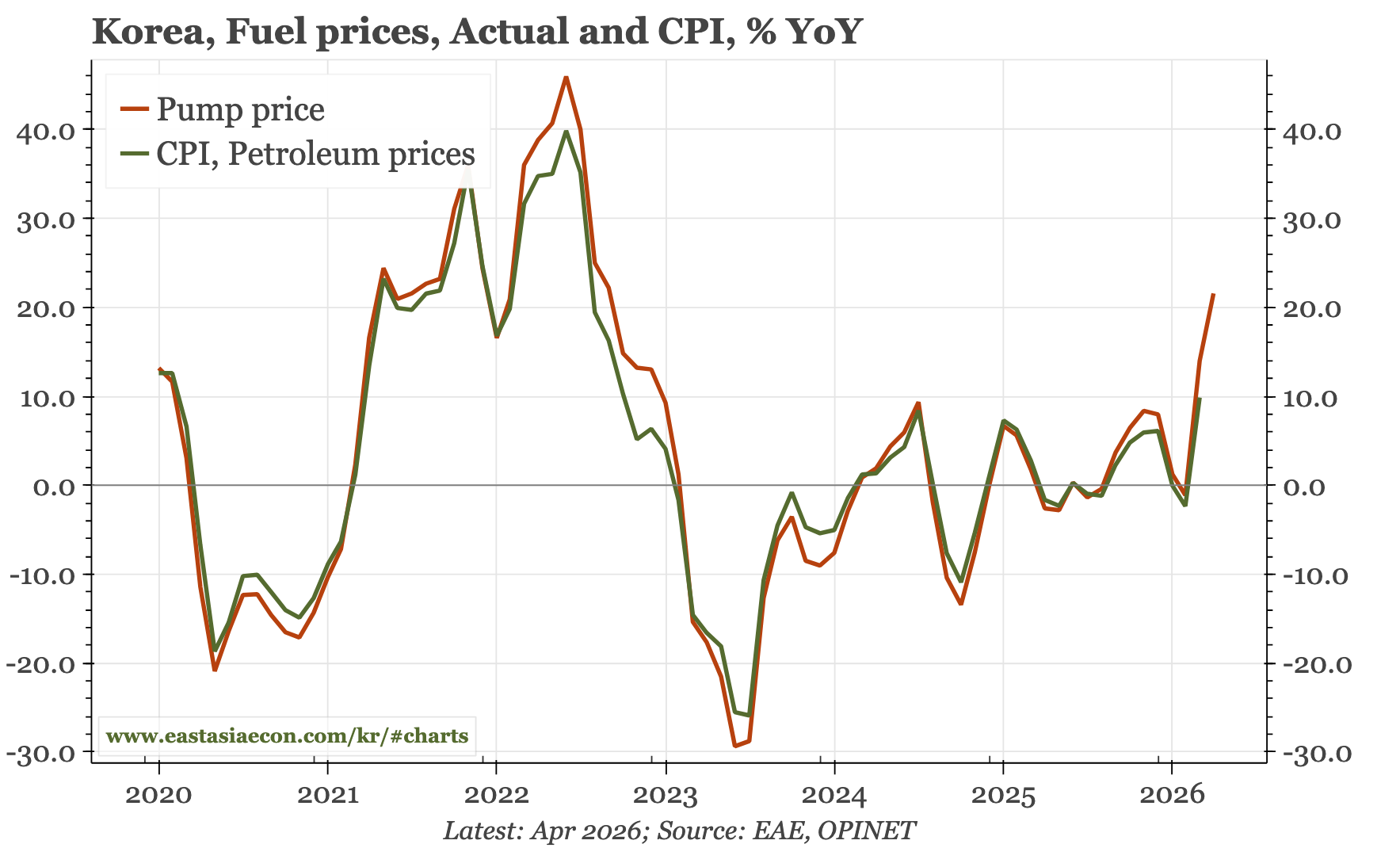

Cycle update – inflation constrained, for now. Government measures are restraining energy prices and so headline CPI. But the war still increases upside risks for inflation. Rising oil prices are pushing up energy and intermediate prices, export growth is strong, and core inflation has been resilient.