East Asia Today

Three things today. A review of the policy and data releases in Japan the last few days. Some charts on Taiwan's property market before next week's CBC meeting. And I've reworked my China dashboard for tracking trade flows, to make it faster, and incorporate auto data for Japan, Korea and the EU.

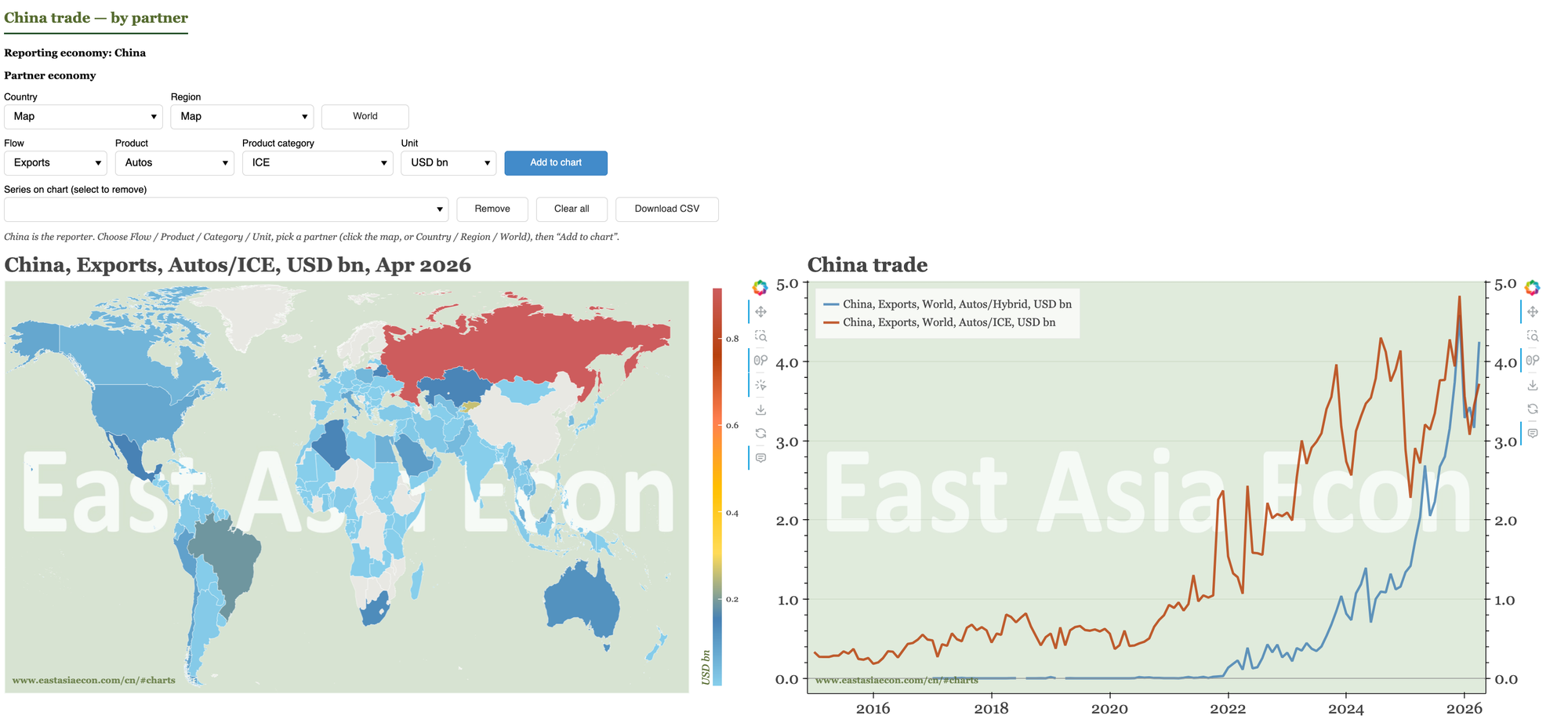

I've improved my dashboard for mapping, charting and downloading data on regional trade flows. It now has China data in autos, semi, robots, rare earths, lithium batteries and solar, and Japan/Korea/EU data on autos. Data cover trade with every country of the world and aggregate region (Africa, ASEAN etc), and for autos, are broken down by powertrain (Hybrid, ICE and so on).

If you aren't yet a subscriber, please consider becoming one! This daily product is designed for individuals, but we also have data services and a much more comprehensive offering for financial institutions. If you have any questions or feedback, please get in touch with me directly.

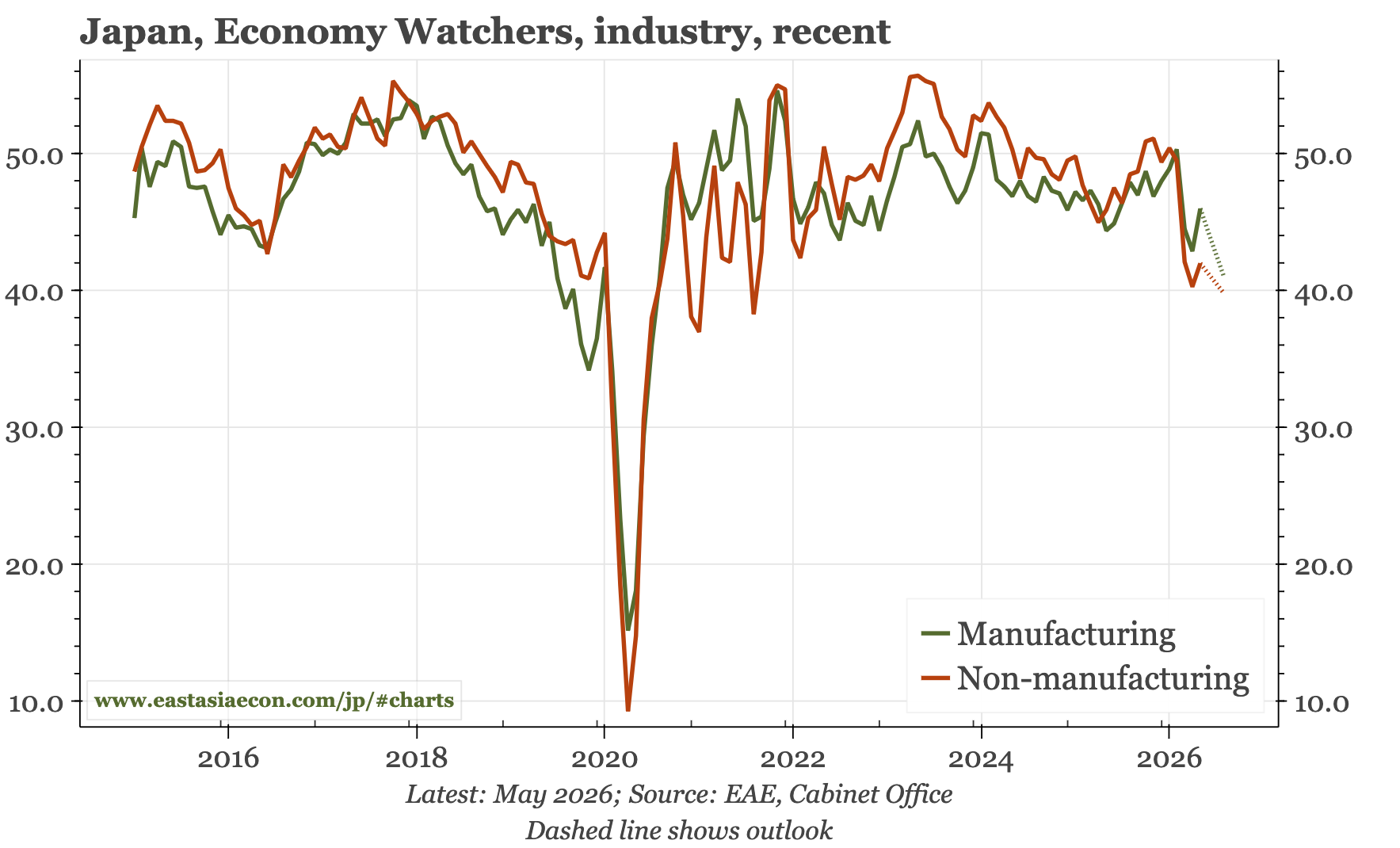

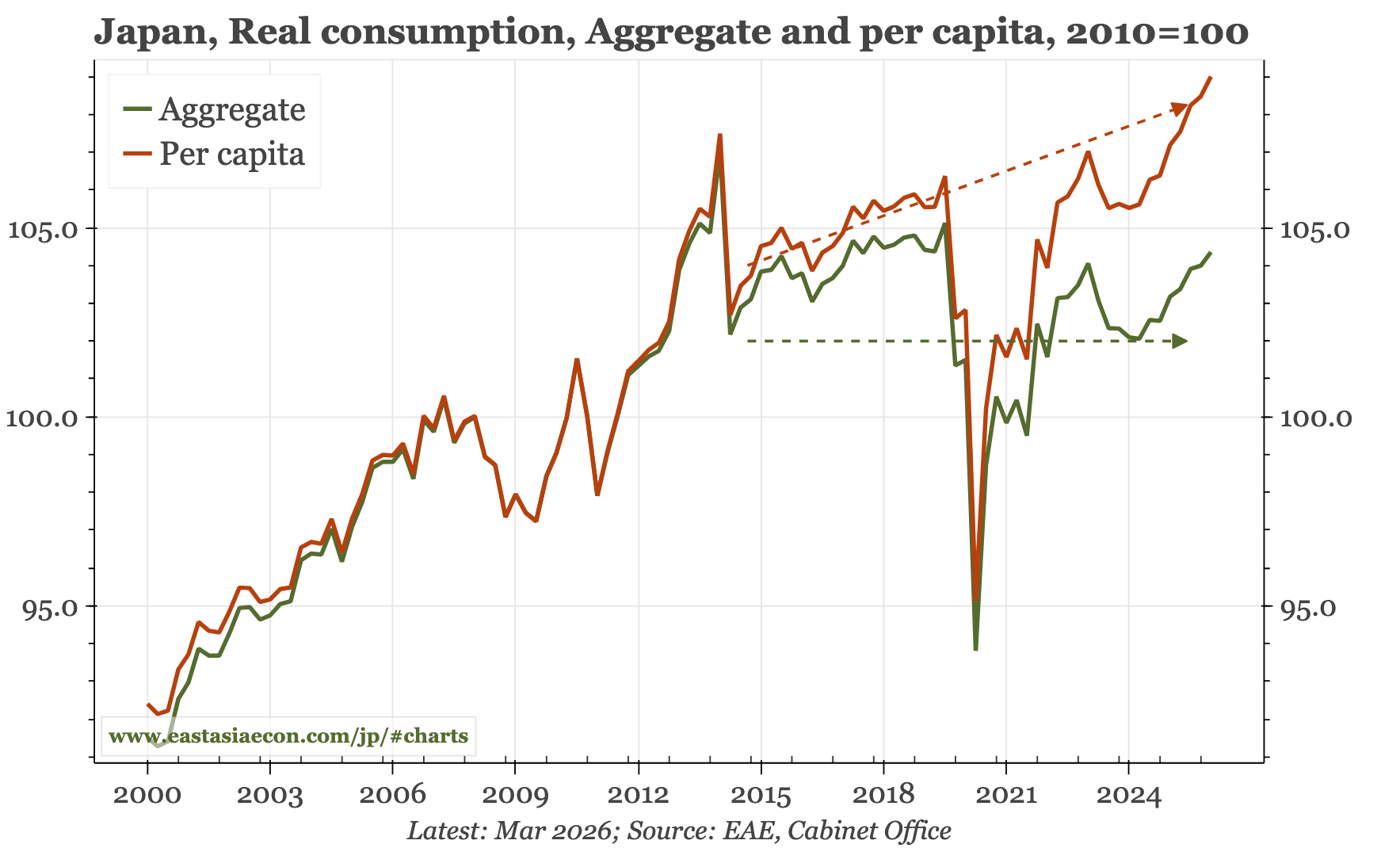

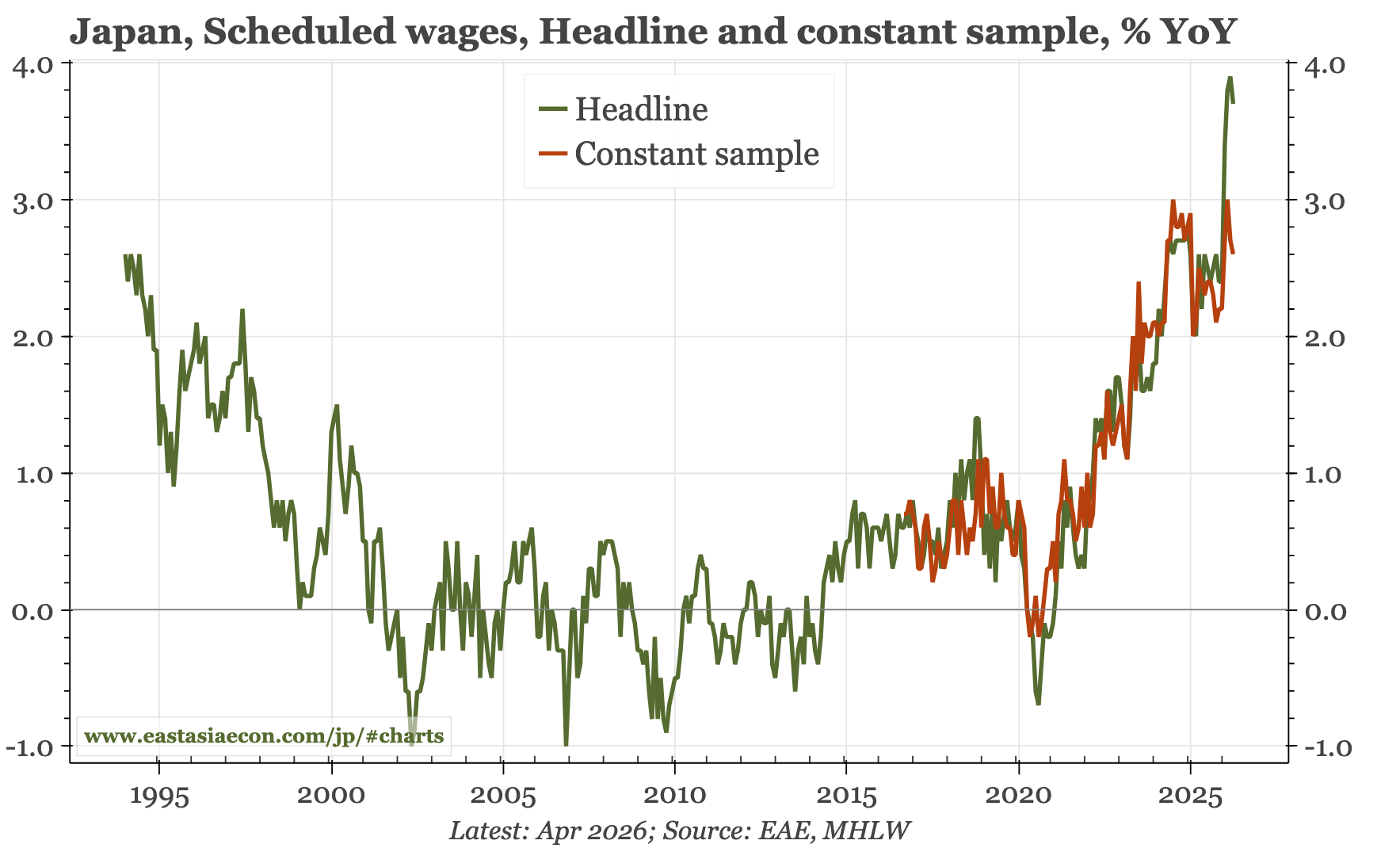

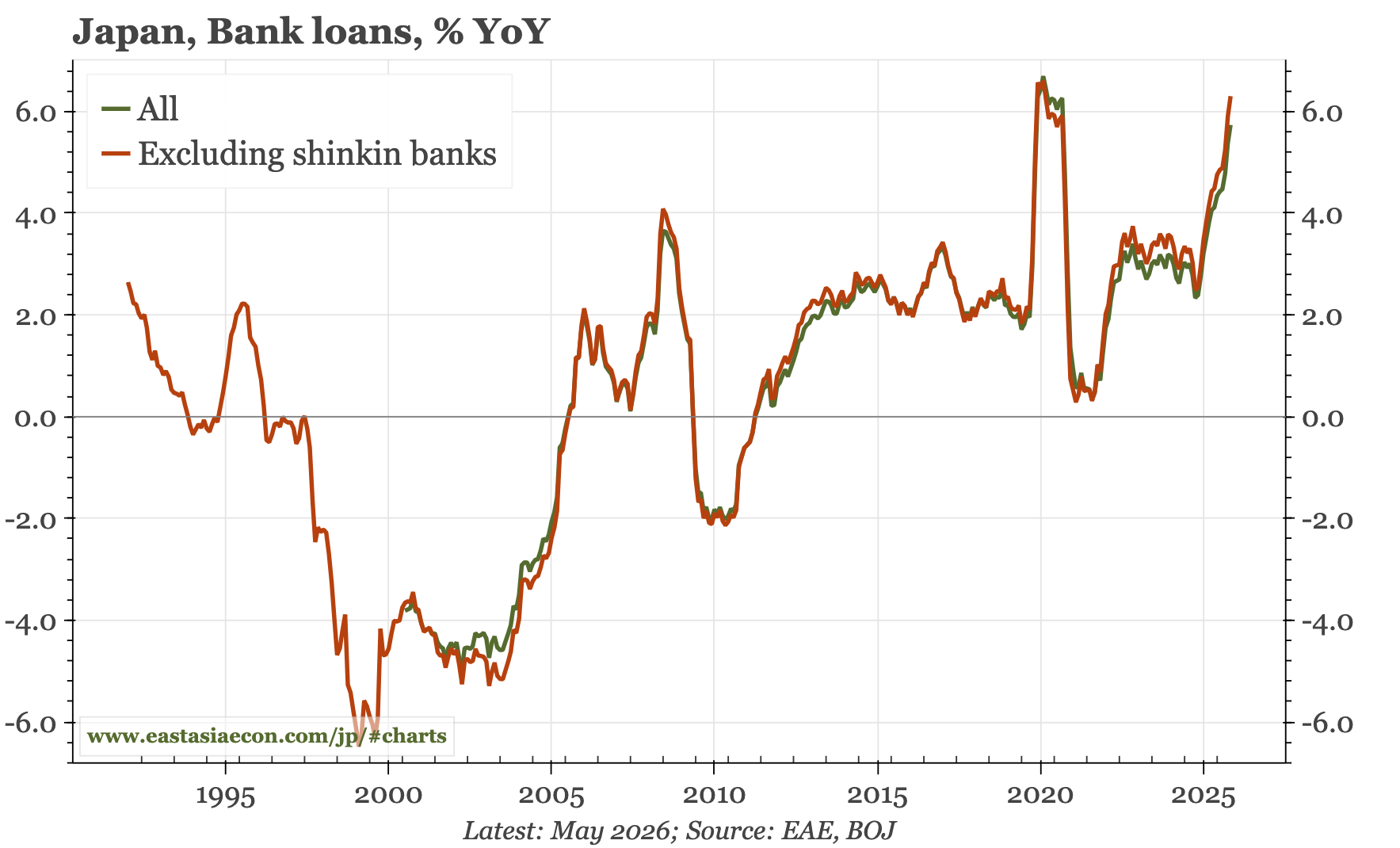

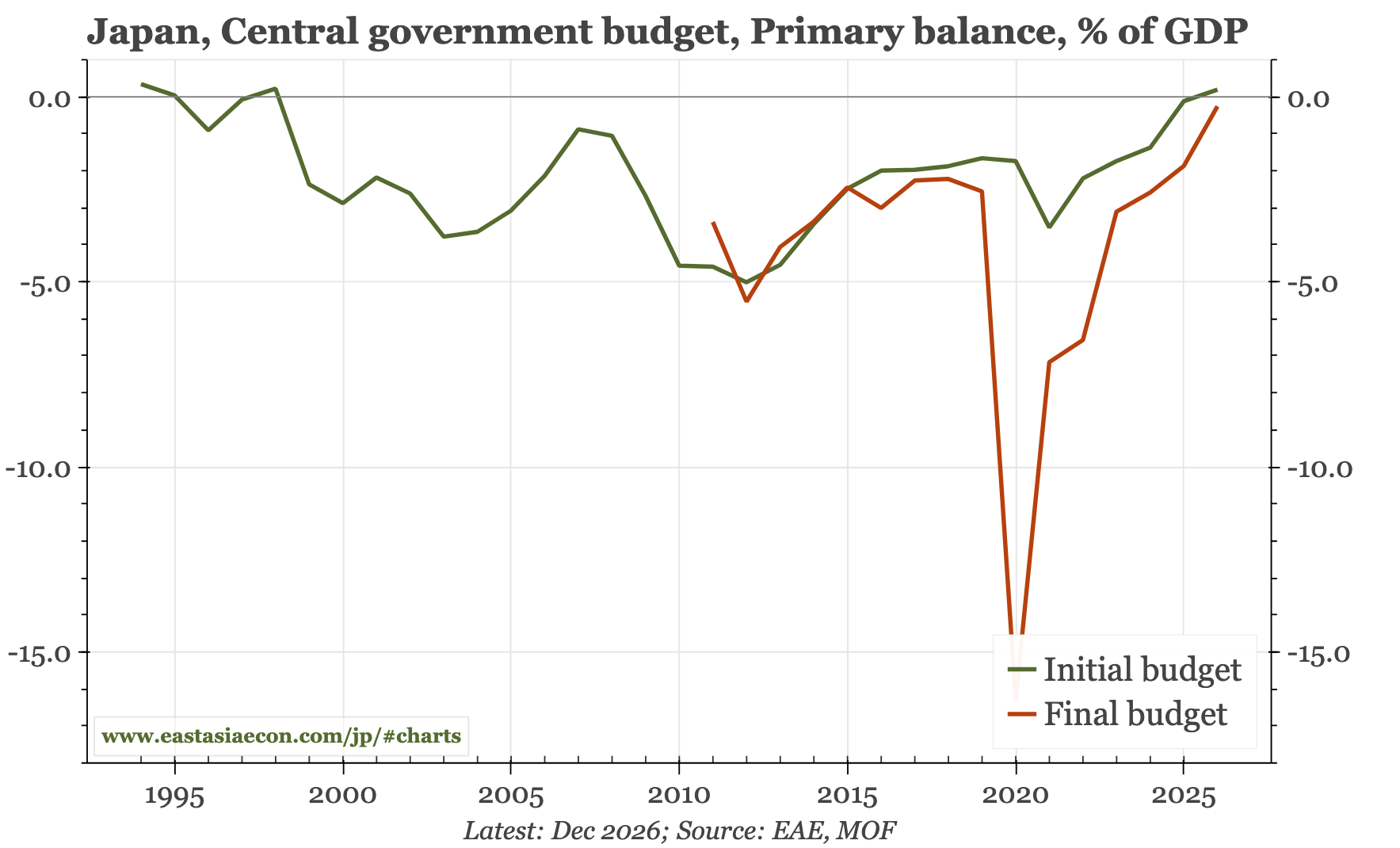

Cycle update – enough, if the BOJ decides it is. The narrowing budget deficit and widening BOP surplus likely won't move market opinion on either rates or fx. What is needed remains a more hawkish BOJ. Accelerating credit and wage growth push in that direction, though the wage data aren't great quality, and sentiment surveys are still weak.

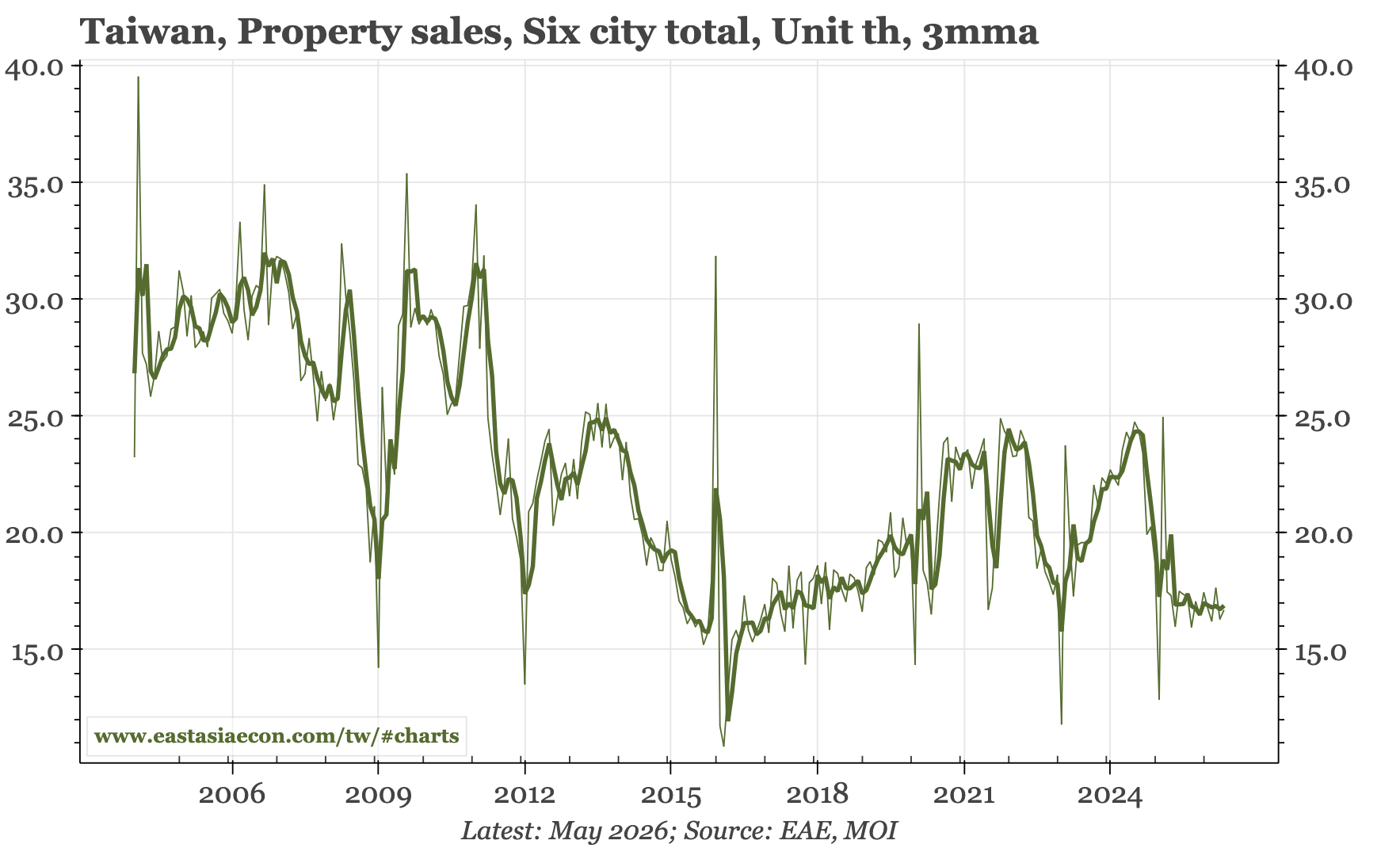

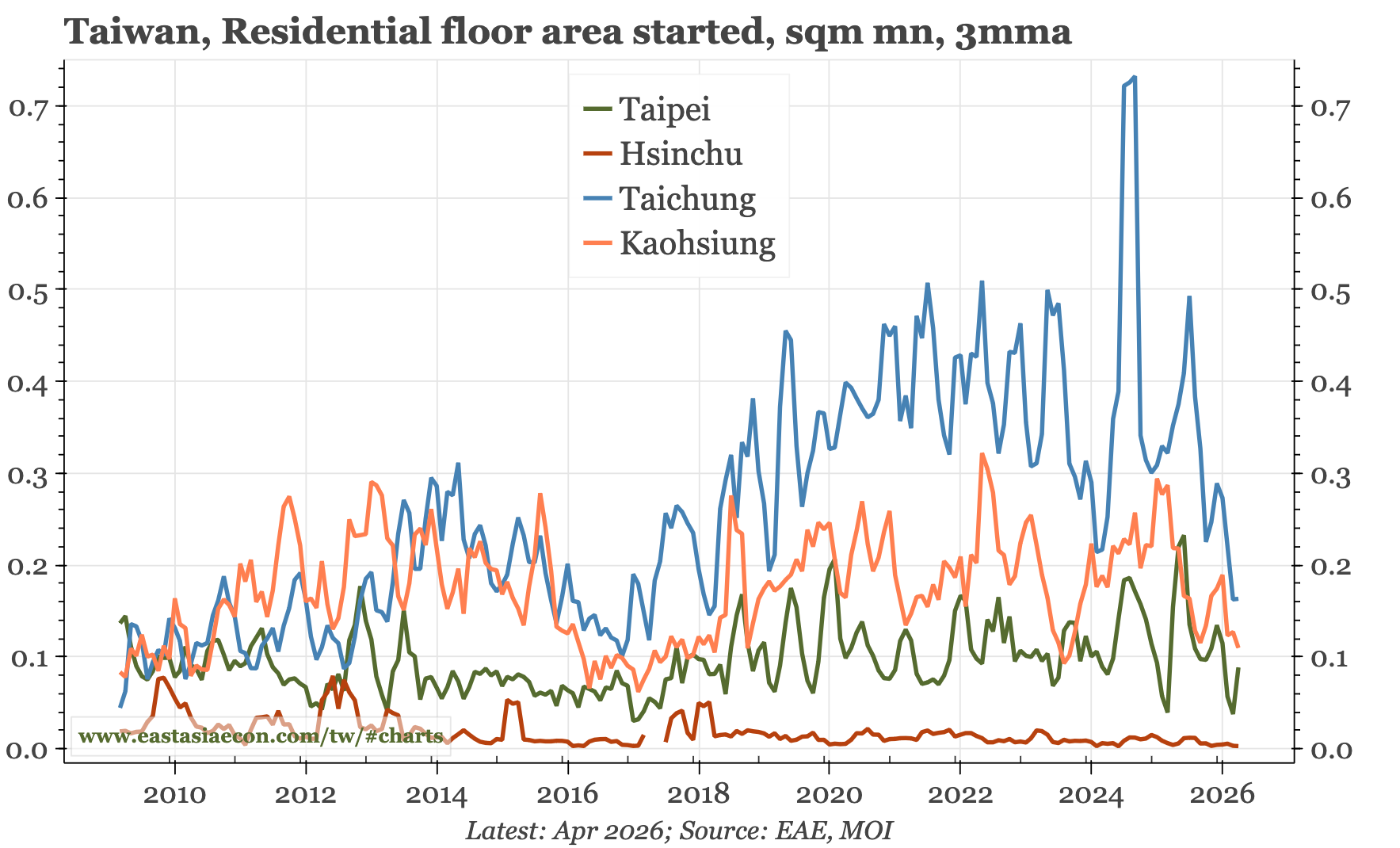

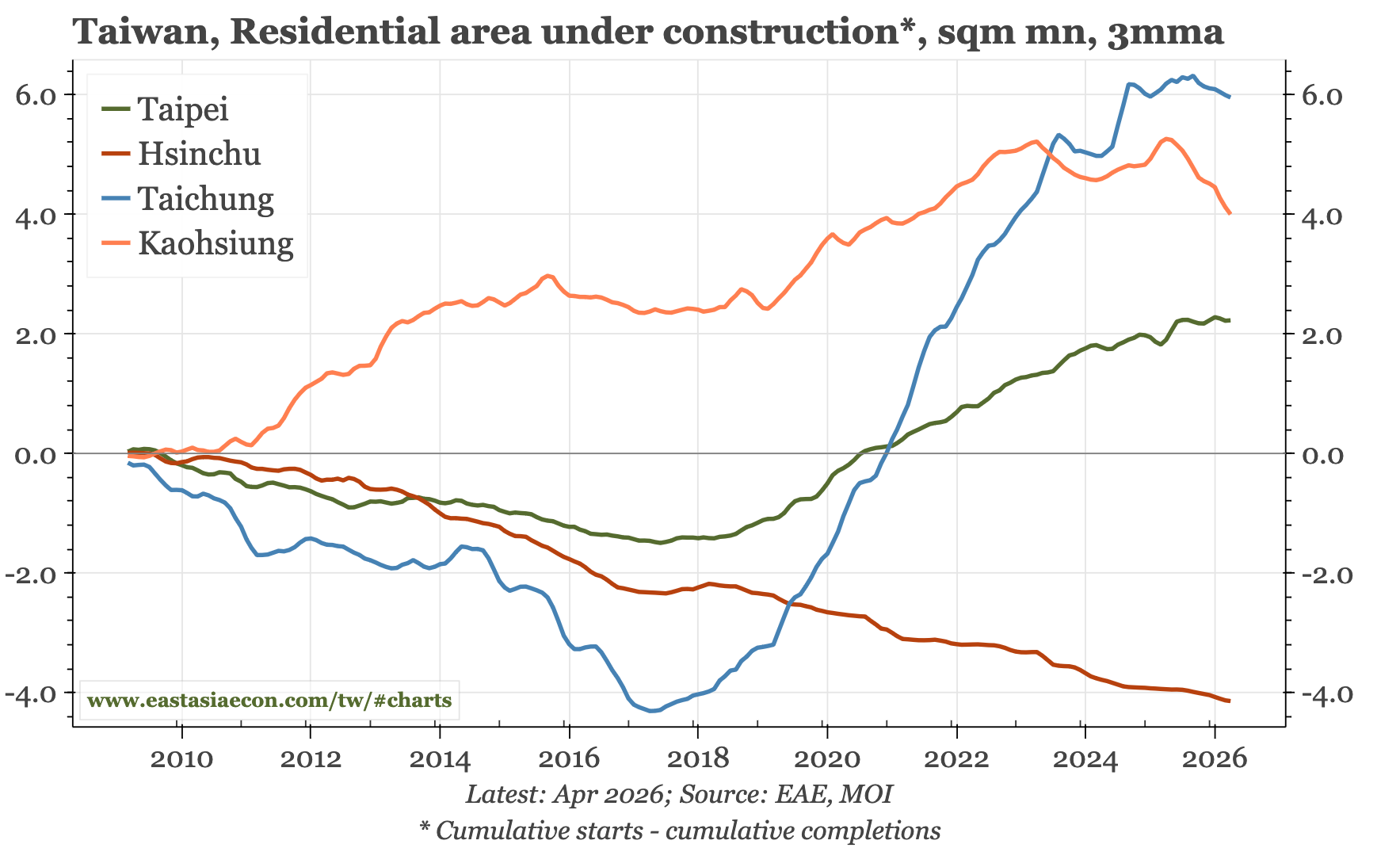

To get ready for next week's CBC meeting, some data on the residential property market. In the 2022-24 tightening cycle, real estate was a specific target for the bank. Hit by all the macro-prudential measures, property transactions did slow sharply through 1H25. Since then, they've reached a floor, though the same isn't true of building starts, with some cities continuing to struggle with a real supply overhang.