East Asia Today

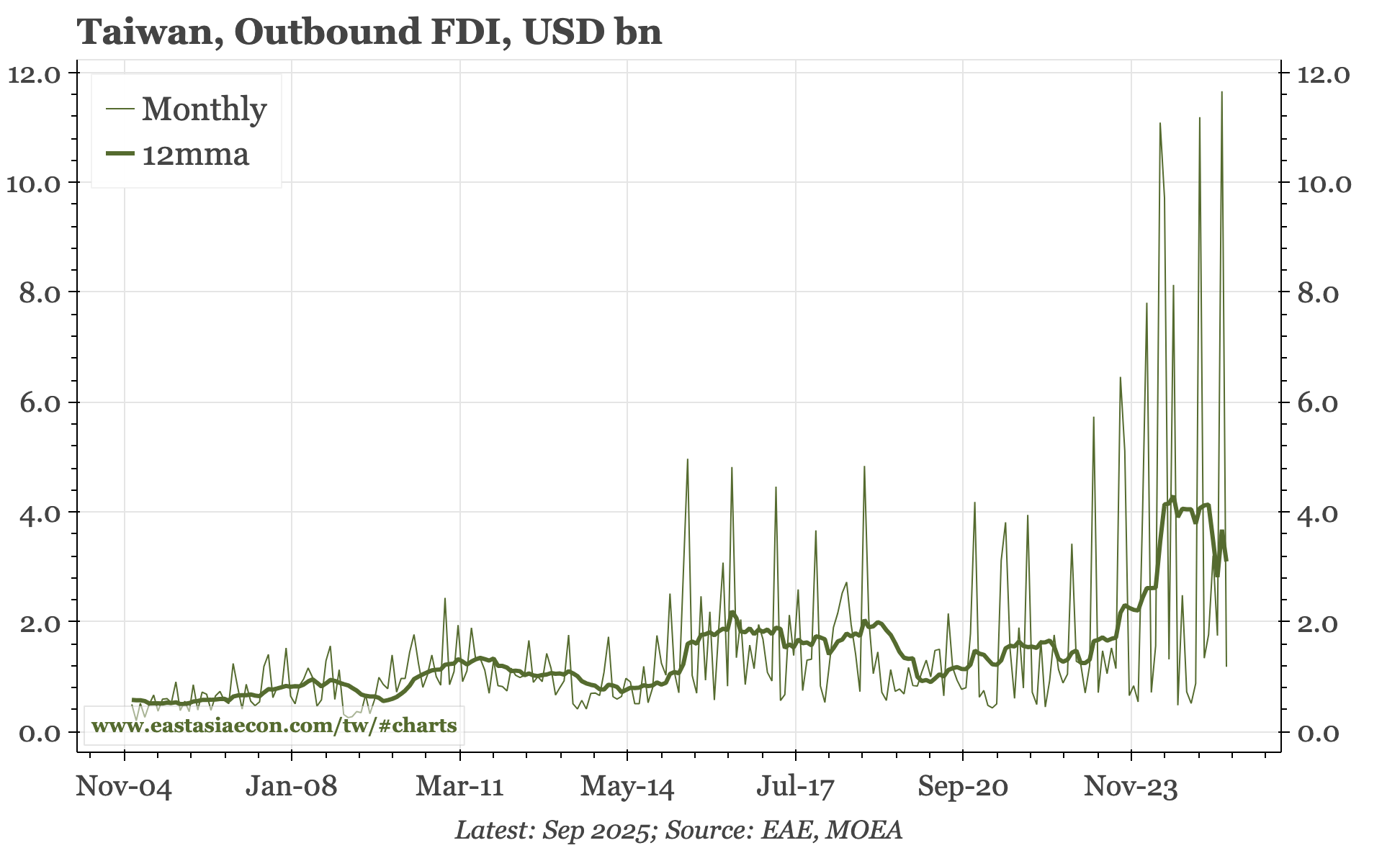

A couple of notes on China today, one covering today's inflation release, and the other a slide pack making the case for higher rates. Elsewhere, Taiwan released FDI data for September. Outflows have eased in recent months, but the clear shift away from investing in China is persisting.

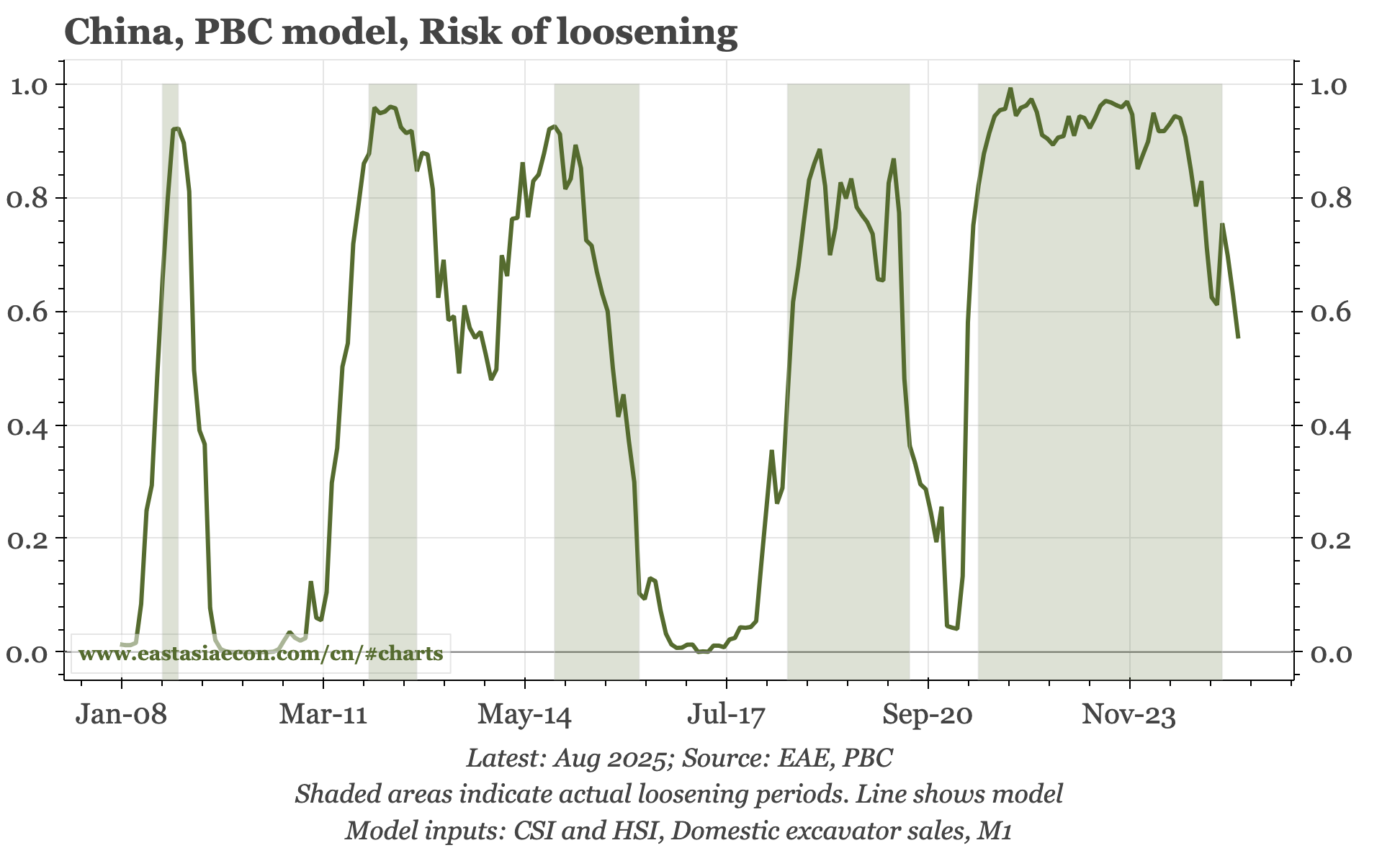

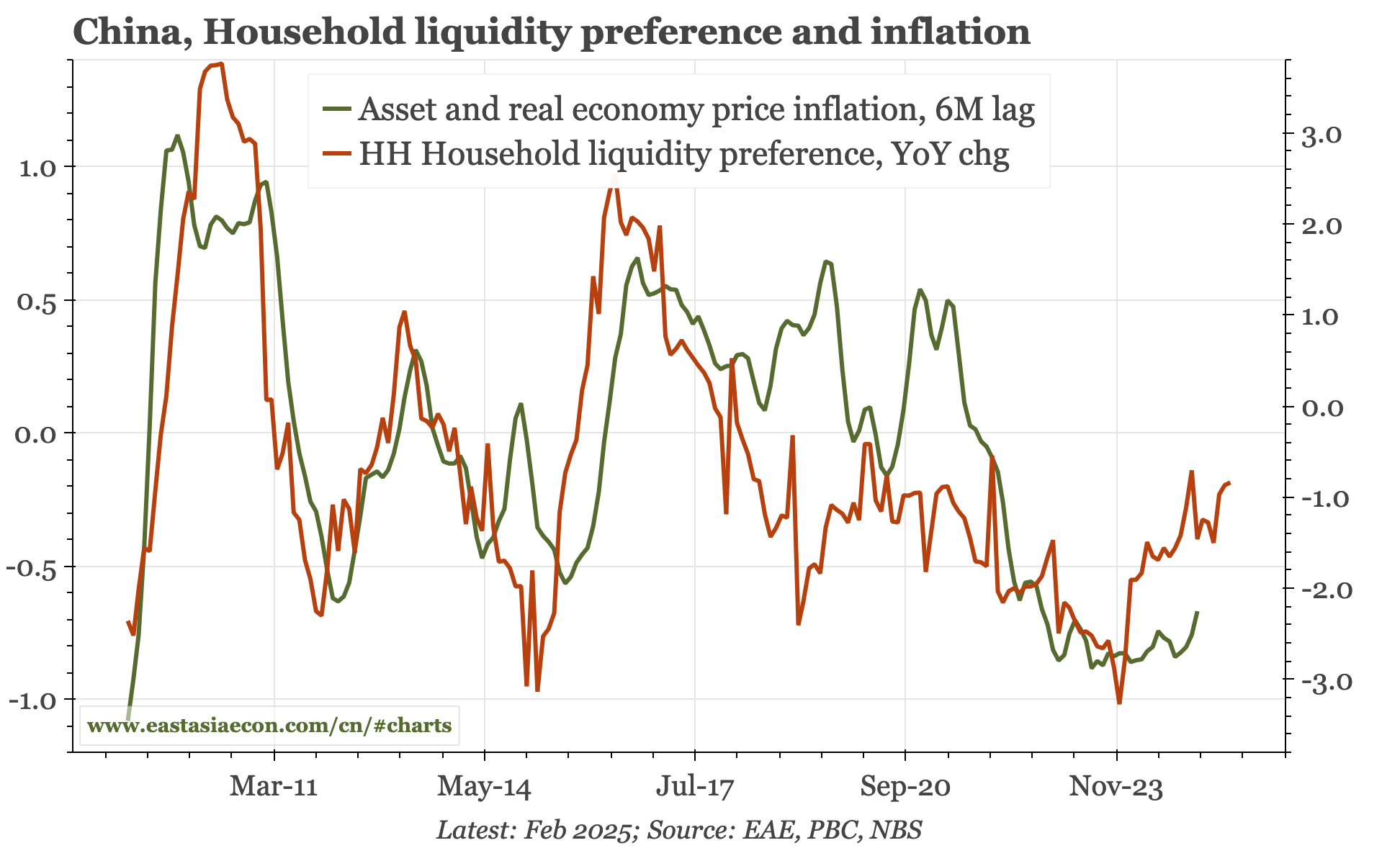

Thematic – the case for higher rates. For the first time since 2021, my models show a fall in the probability of easing. The backdrop is effective monetary policy: inflation is low, but there aren't signs of rising real rates. For now, my base case is rates stop falling. For rates to rise, inflation needs to show up outside of equities.

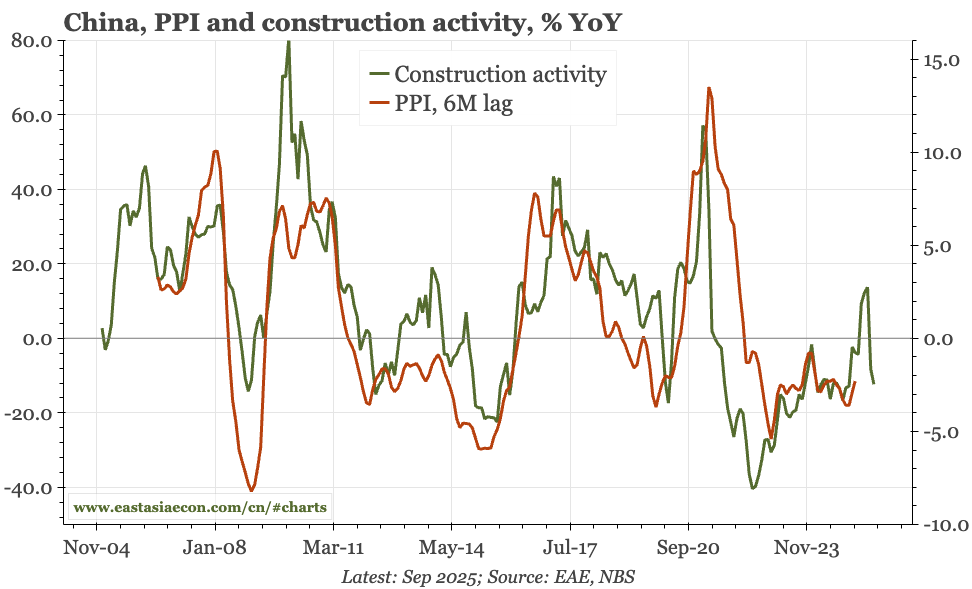

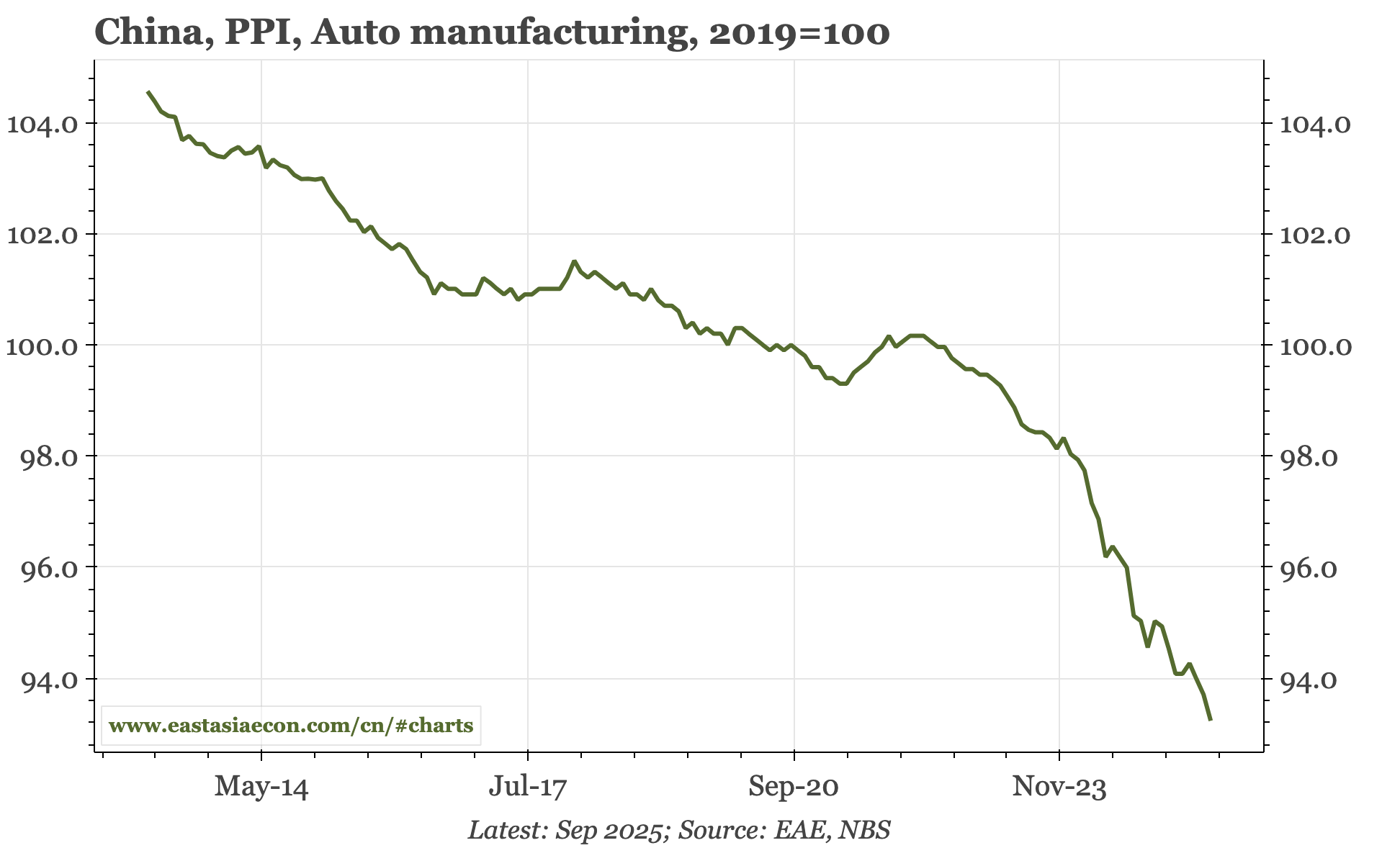

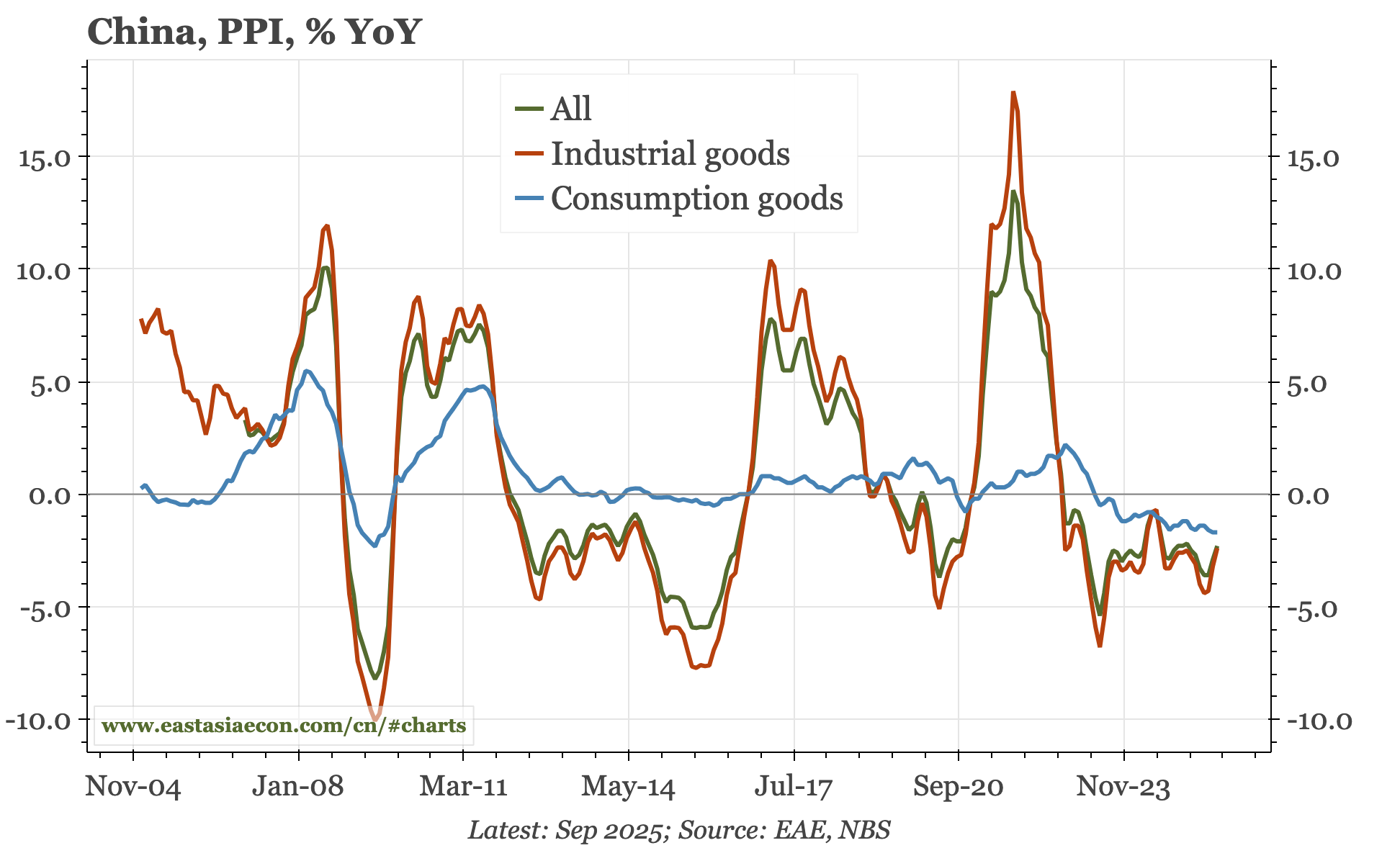

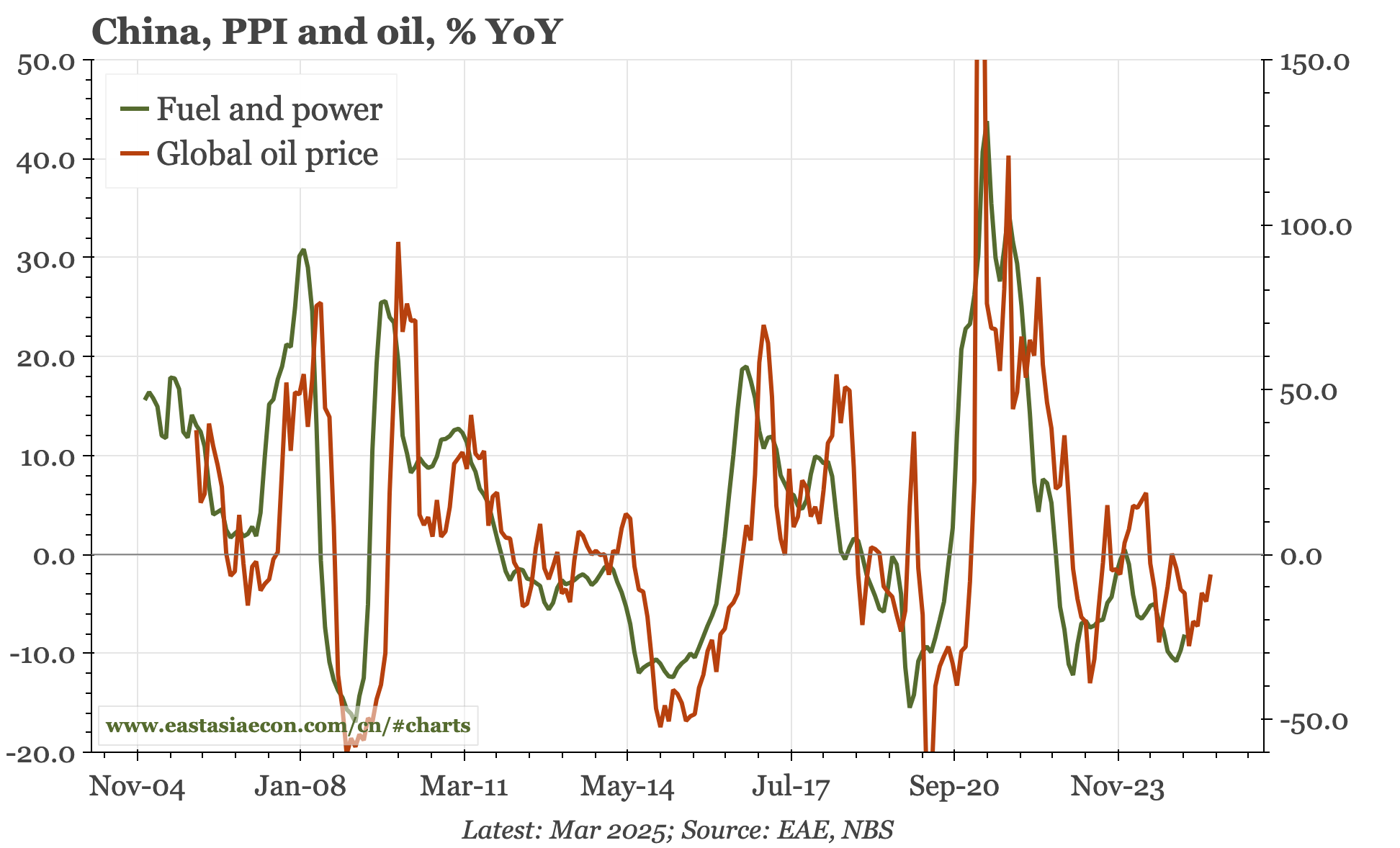

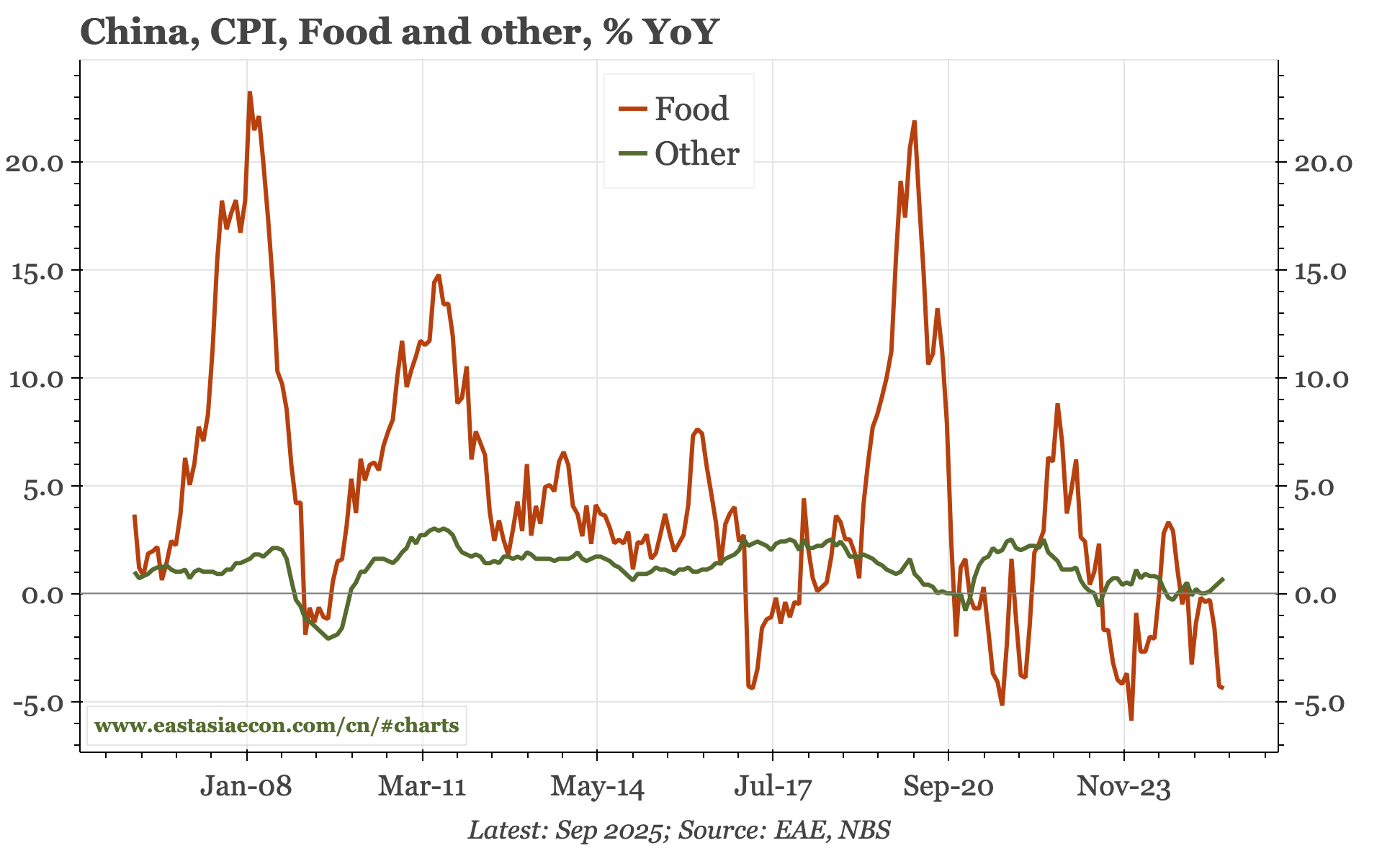

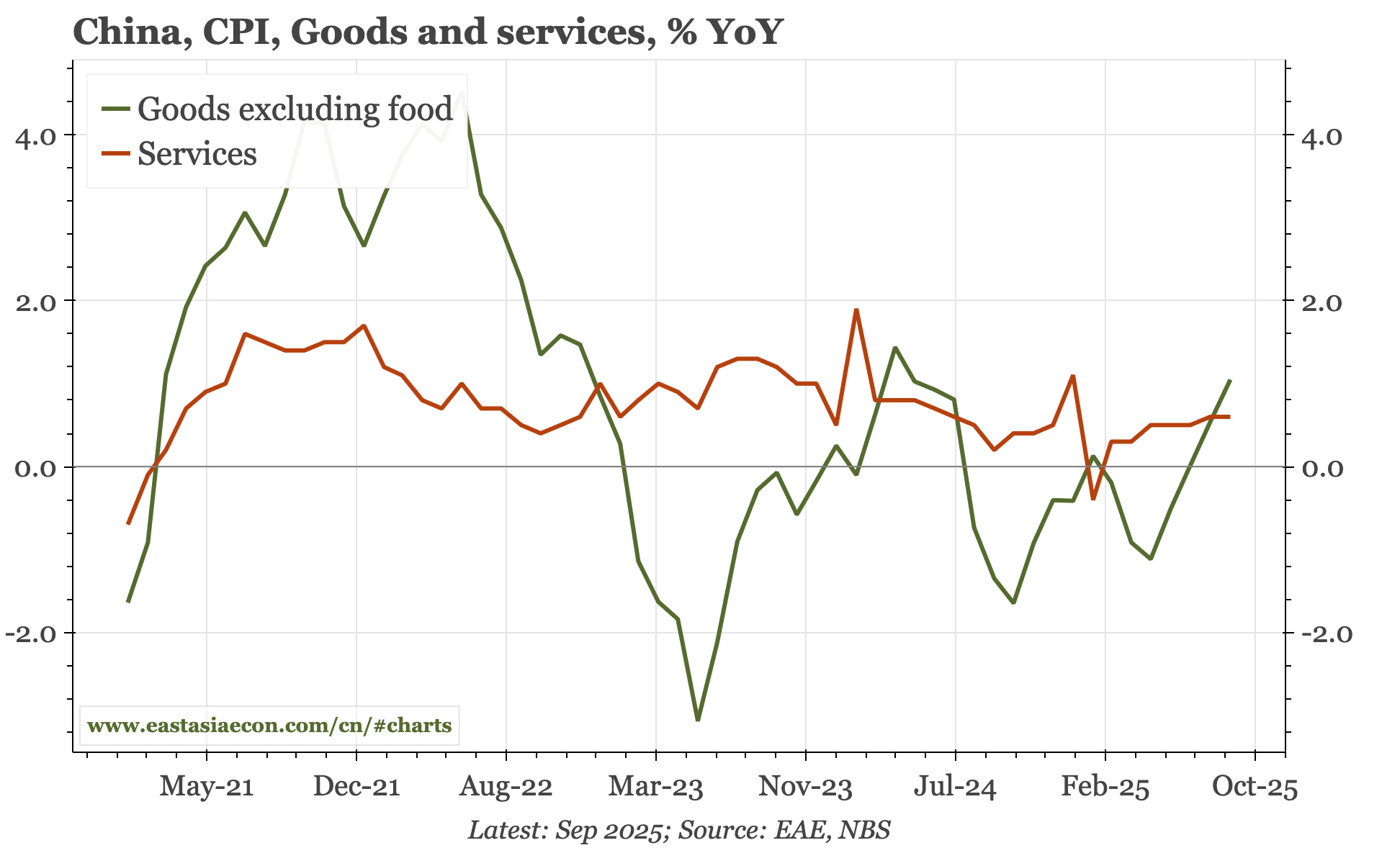

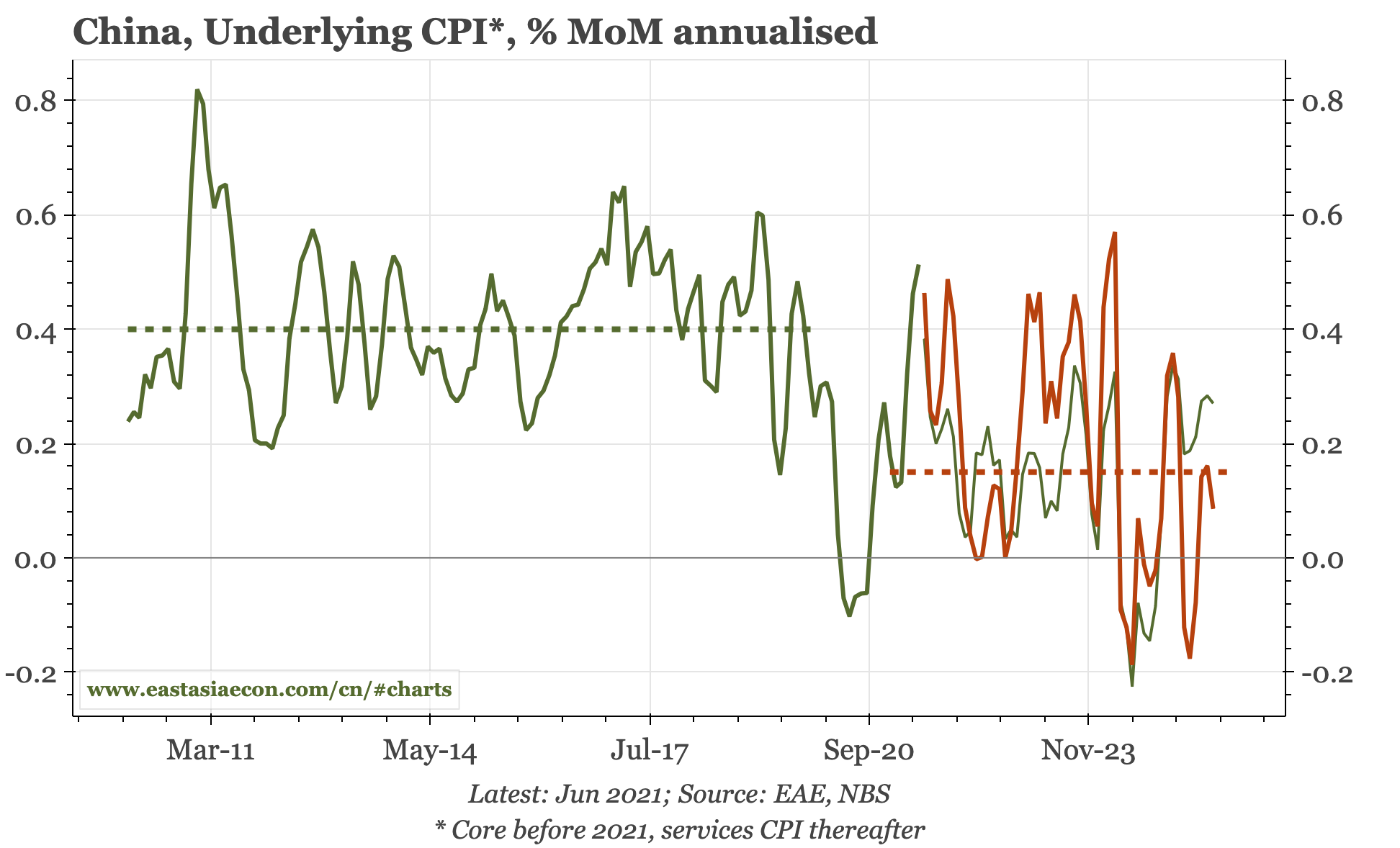

Cycle update – PPI stabilises, but not firmly. The stabilisation of PPI is fragile, with continued sharp falls in some of the sectors targeted by anti-involution, as well as continued weakness in building materials prices. In CPI, falling food prices will eventually reverse, but soft services prices shows underlying CPI inflation remains weak.

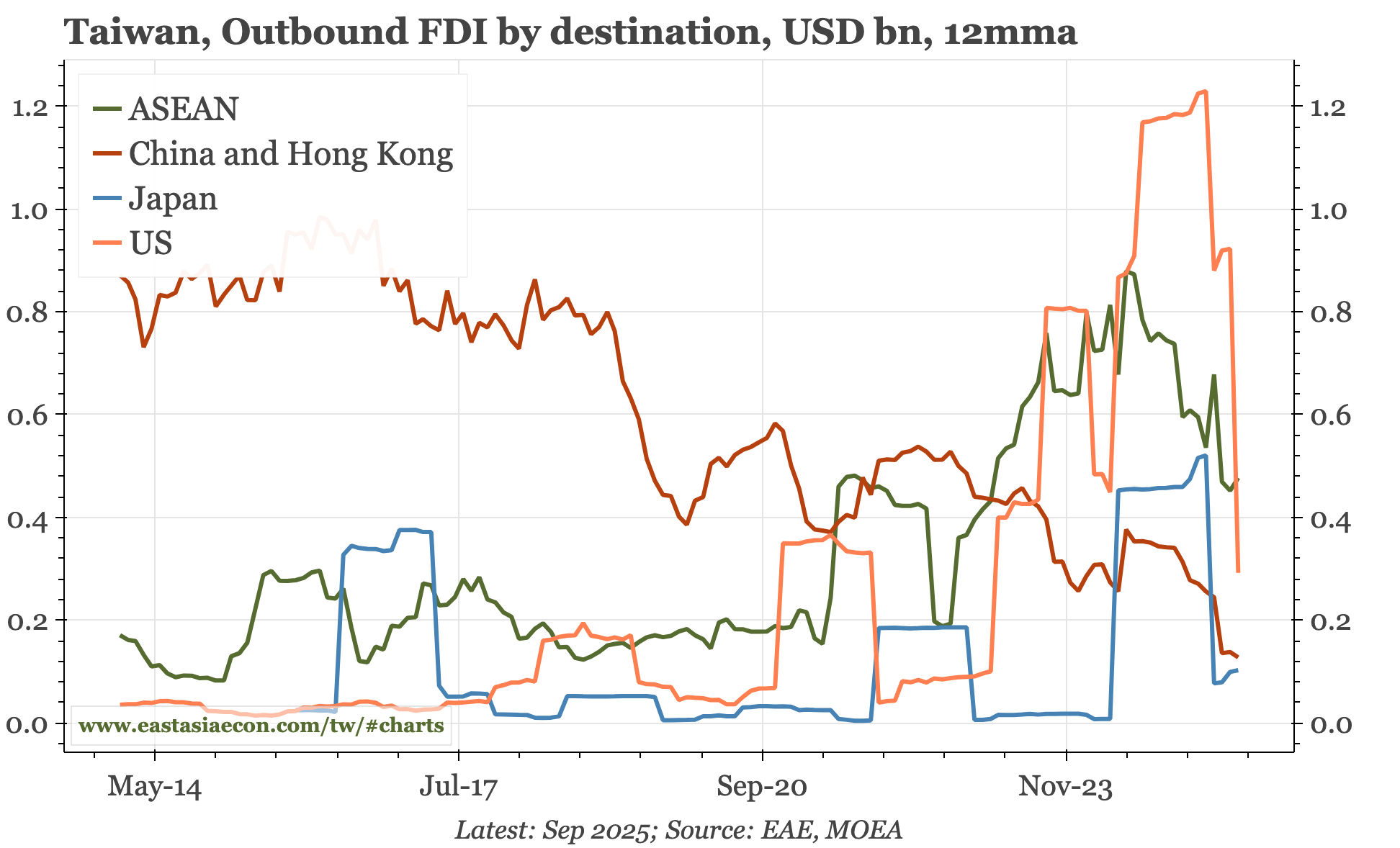

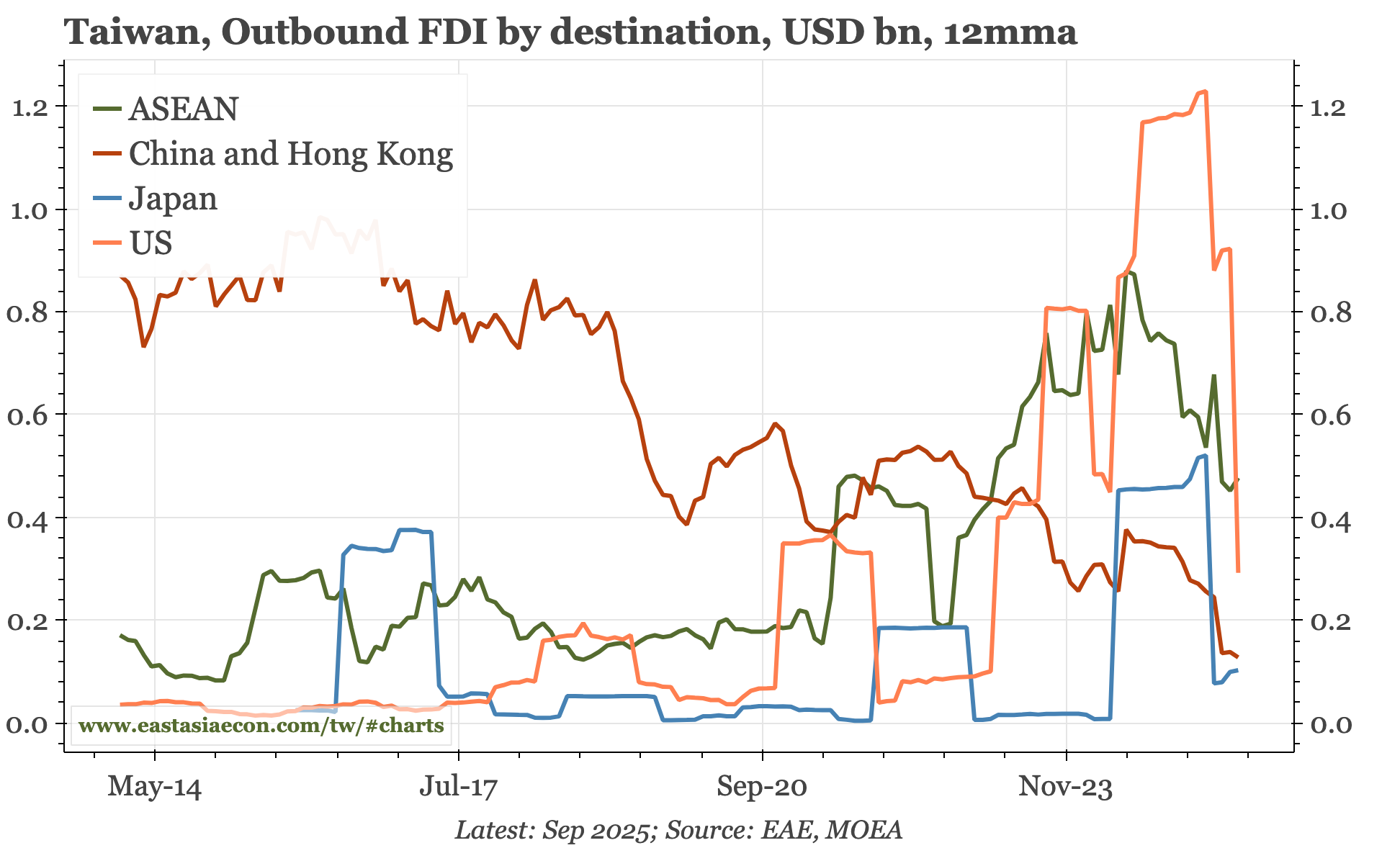

Today's FDI data for September show the pace of overseas investments has eased off in recent months, but remains high relative to the historical flow, and is significant enough to play a role in the recycling of the current account. Through 2015 the focus of overseas investment was China. Now, there is much more diversification. Some of that is because of TSMC's investments in the US and Japan. But Taiwan firms are now putting more money in ASEAN than in China.