East Asia Today

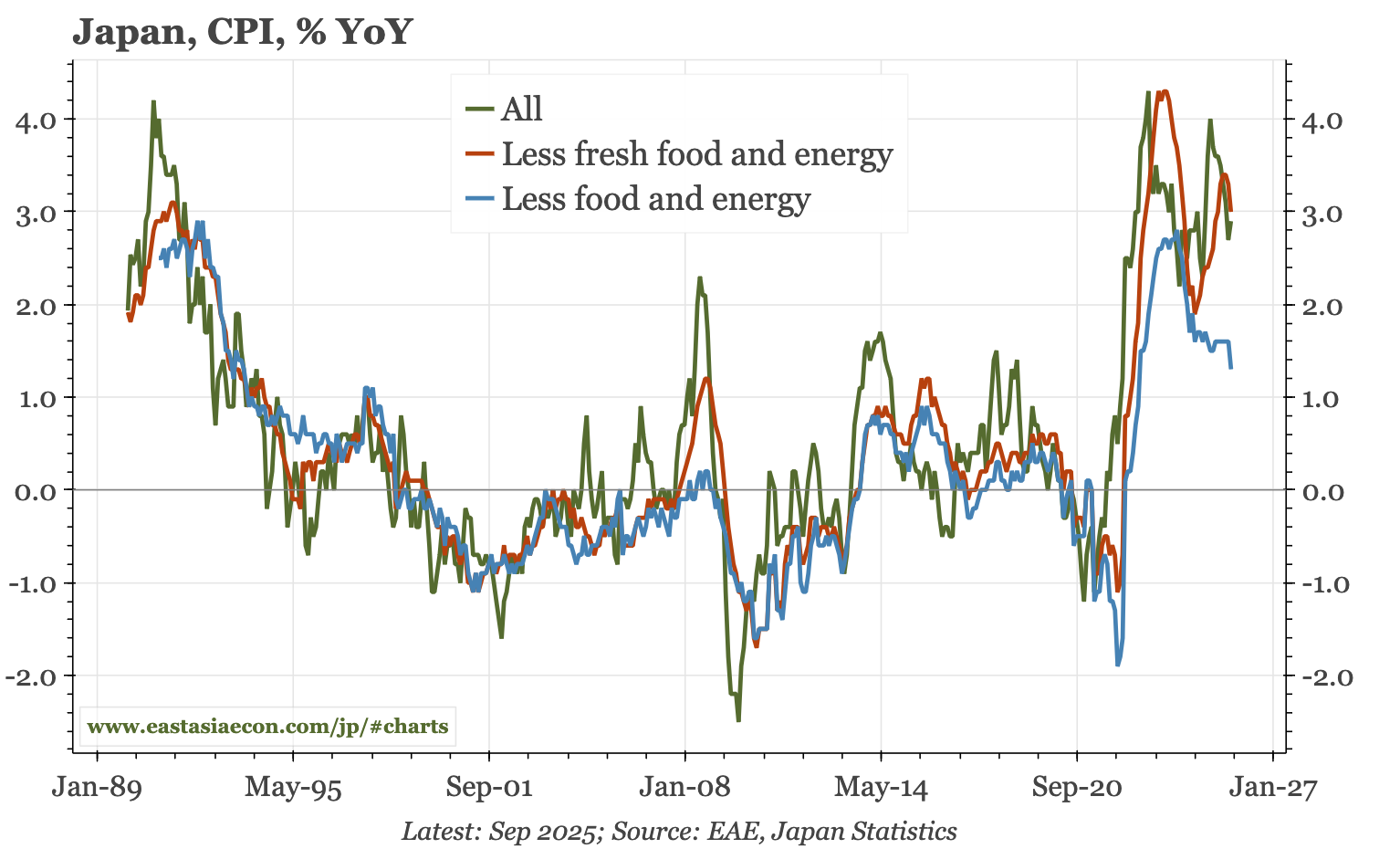

Japan CPI data showed headline near 3% and rising (inflation!), but core near 1% and falling (deflation!). Price data in China, by contrast, are stable, which is at odds with weak FAI. Finally, my updated trade mapper dashboard, which now covers autos and the battery and rare earth supply chains.

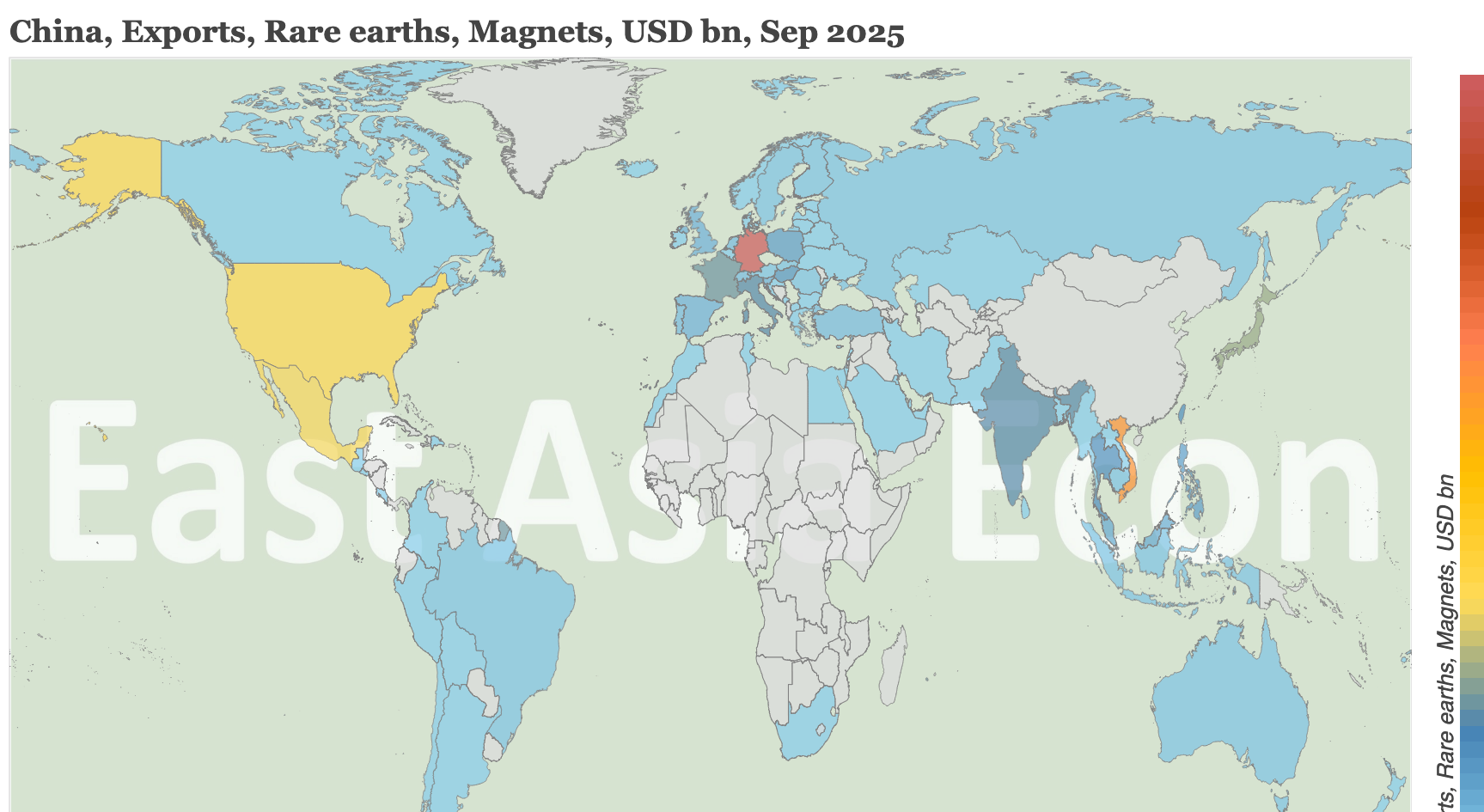

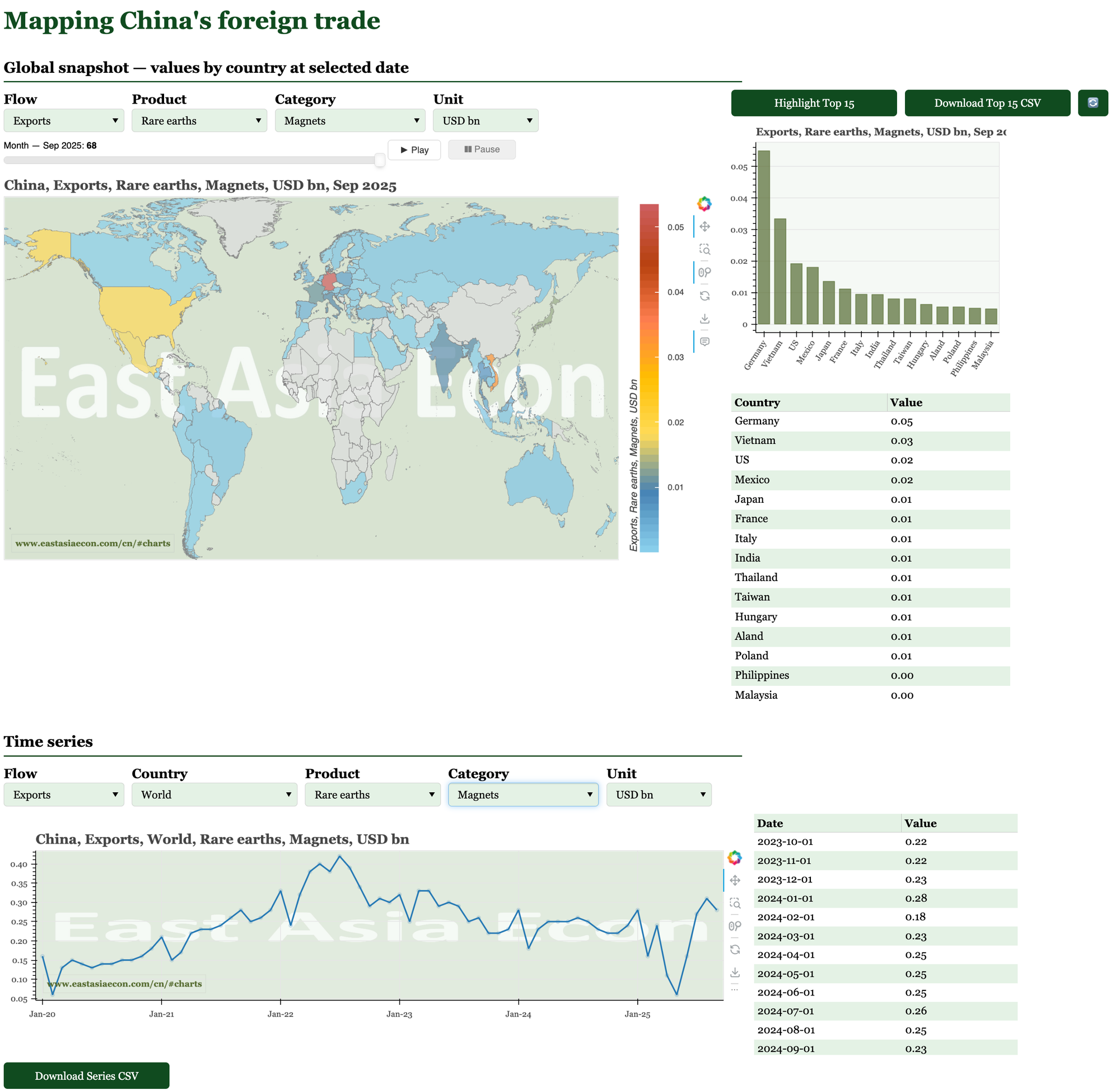

I've been improving my dashboard for tracking China's exports. It now includes auto volumes by country and type, as well as data on China's exports of batteries and rare earths (end products, as well as the inputs targeted by Beijing's latest export controls), and unit prices. The data start in 2020, and can all be downloaded. It takes around 10 seconds to load the app, and currently it isn't behind a paywall. Let me know if you want more data added and I'll try my best to do so.

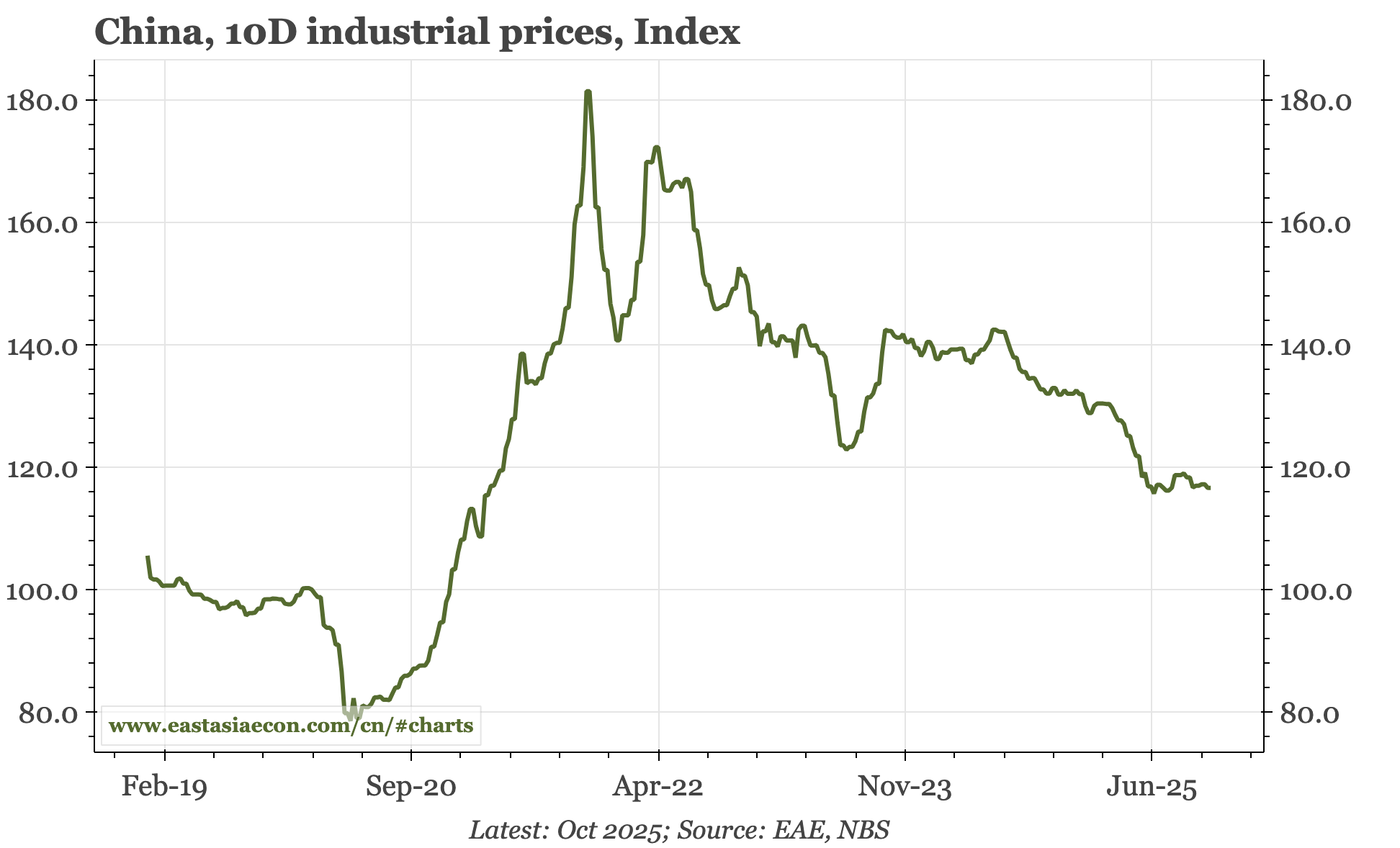

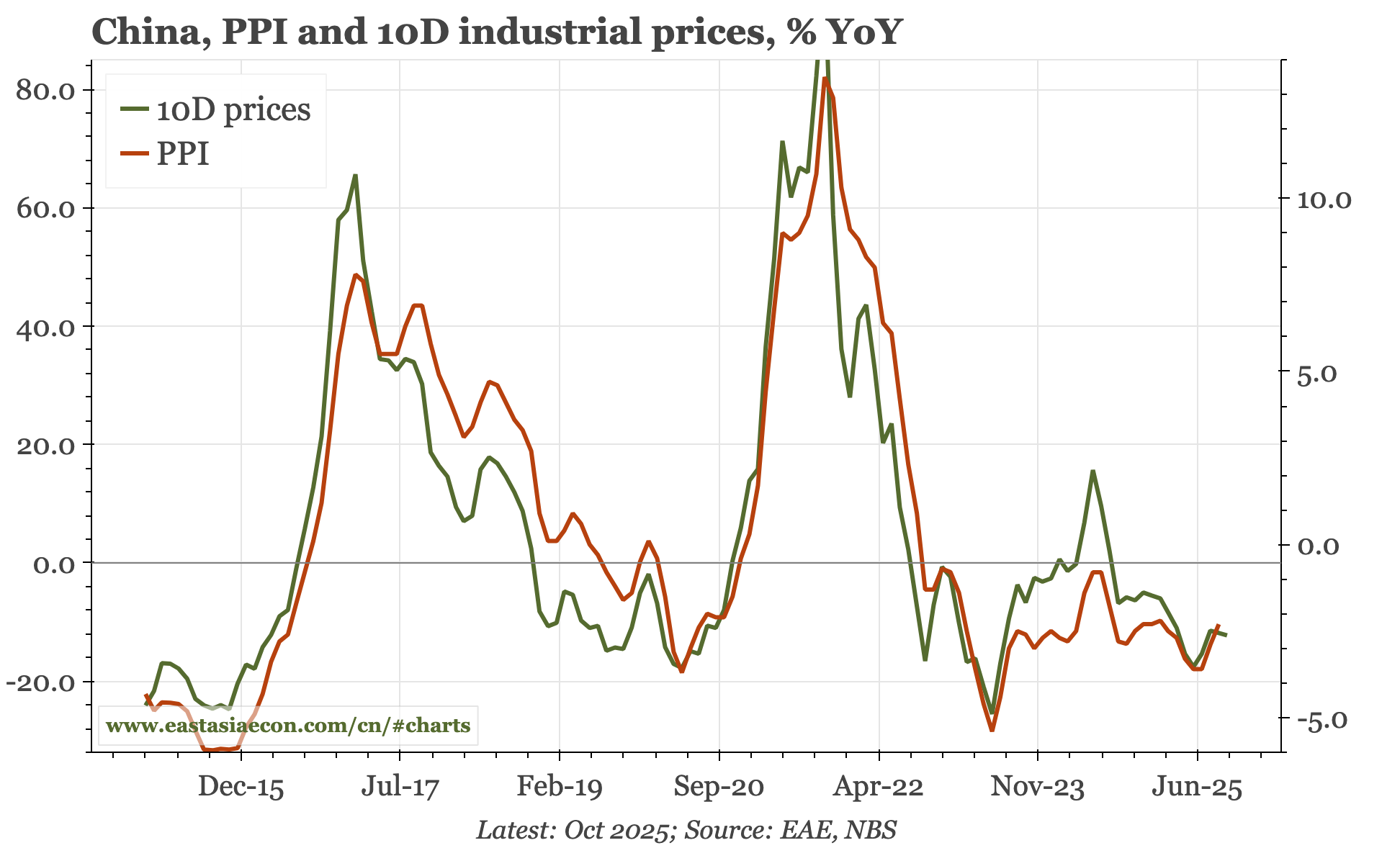

I am still mulling over this week's macro data, particularly the weakness in monthly FAI and quarterly construction. The drop in activity is at odds with some of the other indicators for the economy. One example is the monetary data I highlighted yesterday. Another example is today's 1o-day series for industrial prices. After dropping sharply in the first 6M, through Q3 it has been stable. There has even been some recovery in the long-suffering building materials sector. One implication is PPI inflation will likely be more or less unchanged this month.

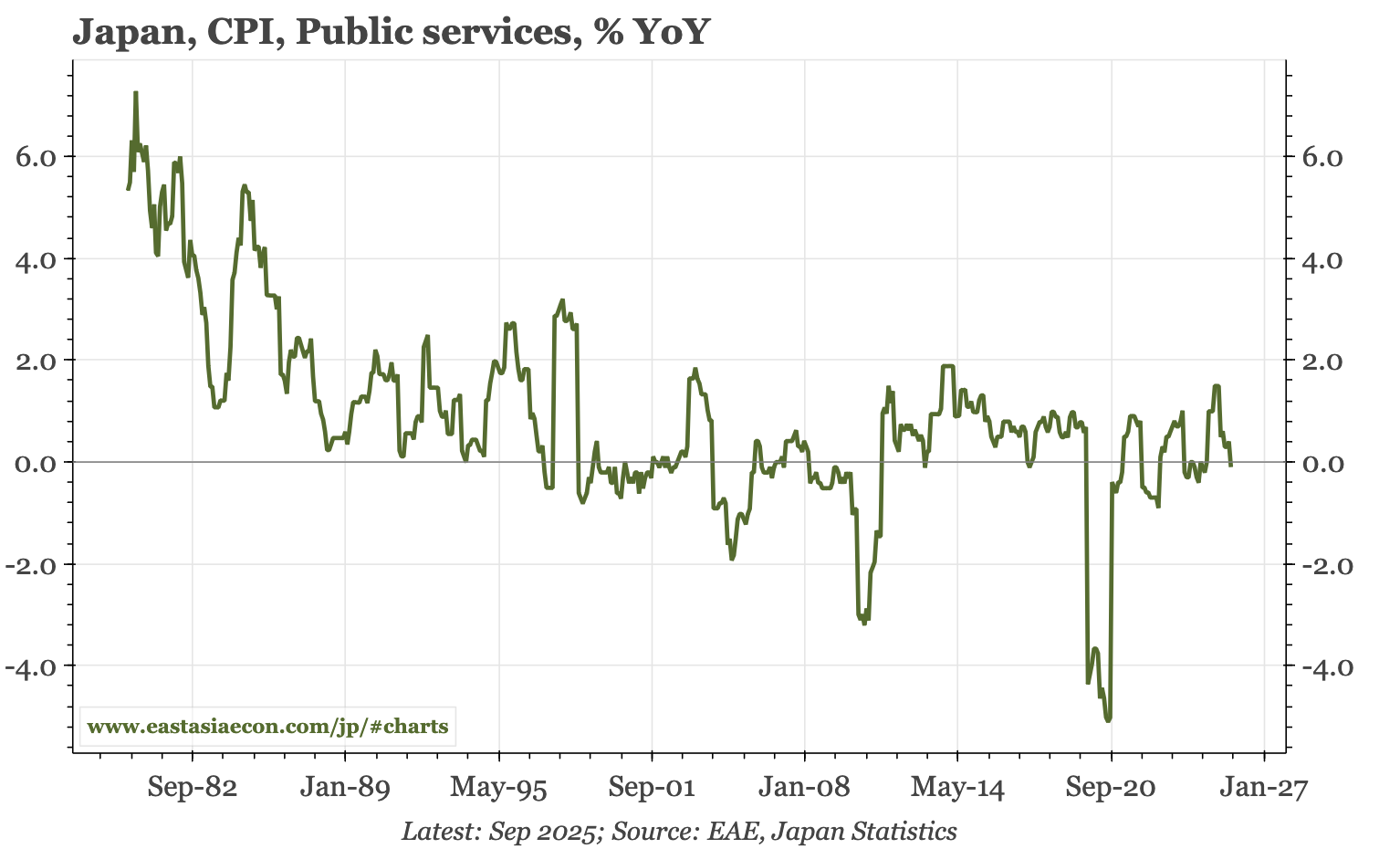

Cycle update – another noisy month for CPI. National inflation data for September was messy again. One reason was public service prices falling, a development that stands out when a theme of recent BOJ speeches has been pent-up inflation pressure in the public sector. Overall, the inflation picture still looks solid.