East Asia Today

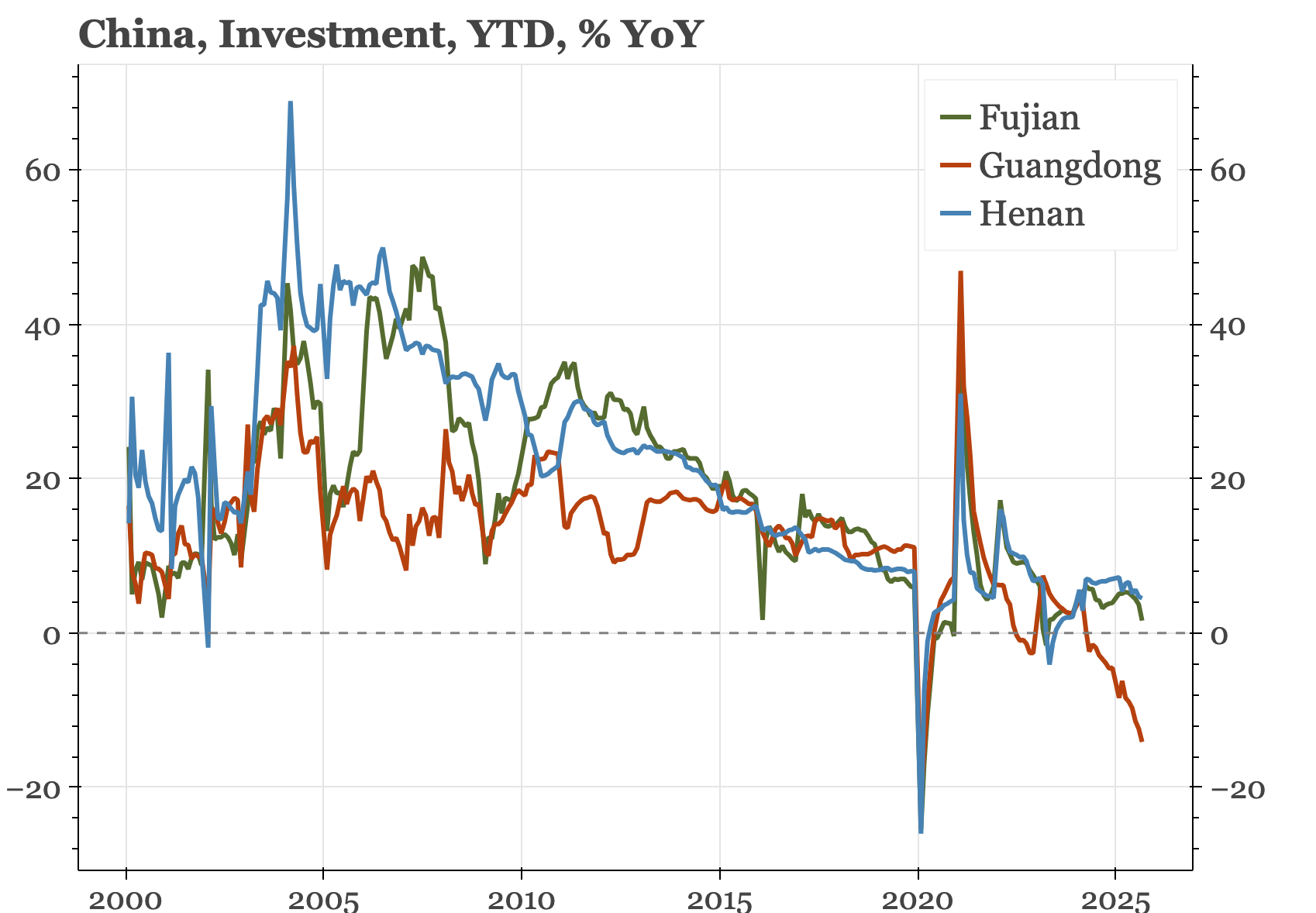

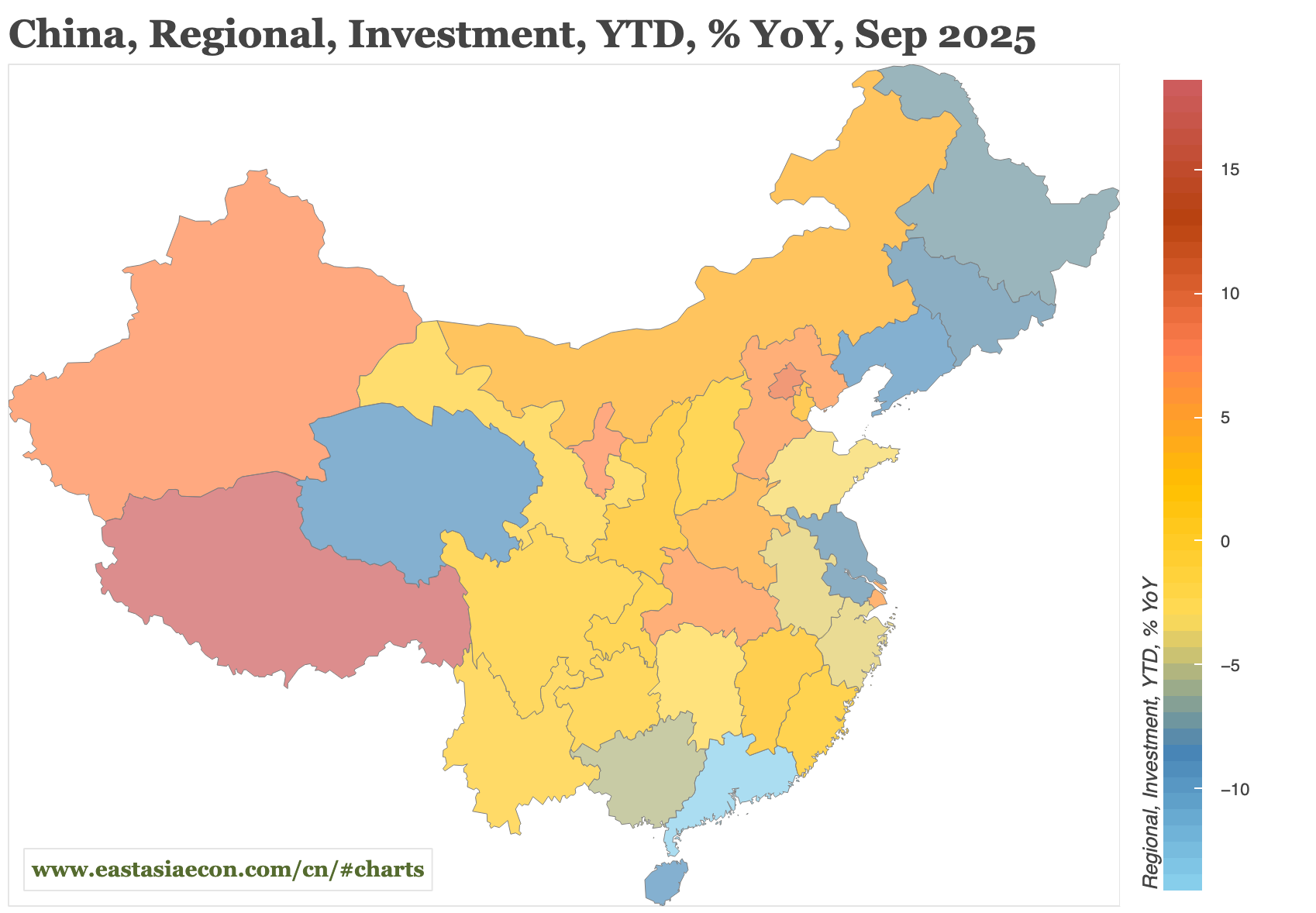

Today's releases show Japan PPI turning up, and China credit growth slowing down. Also today, my latest data visualisation tool, mapping China's provincial data. The first data covered is FAI, showing the weakest province in September to be Guangdong, which would usually be regarded as a powerhouse.

If you aren't a subscriber yet, please consider becoming one. We have a comprehensive service for financial institutions, but also this daily summary and data products that are more suited to individuals.

China's provincial economic picture. I've started collecting provincial data. That's for a research piece I am working on, but I am also showing the data in a dashboard which, for now, isn't behind a paywall. You can find that here, along with my other two visualisation tools for the region, one that allows charting of macro data across the four economies, and the other that maps China's exports.

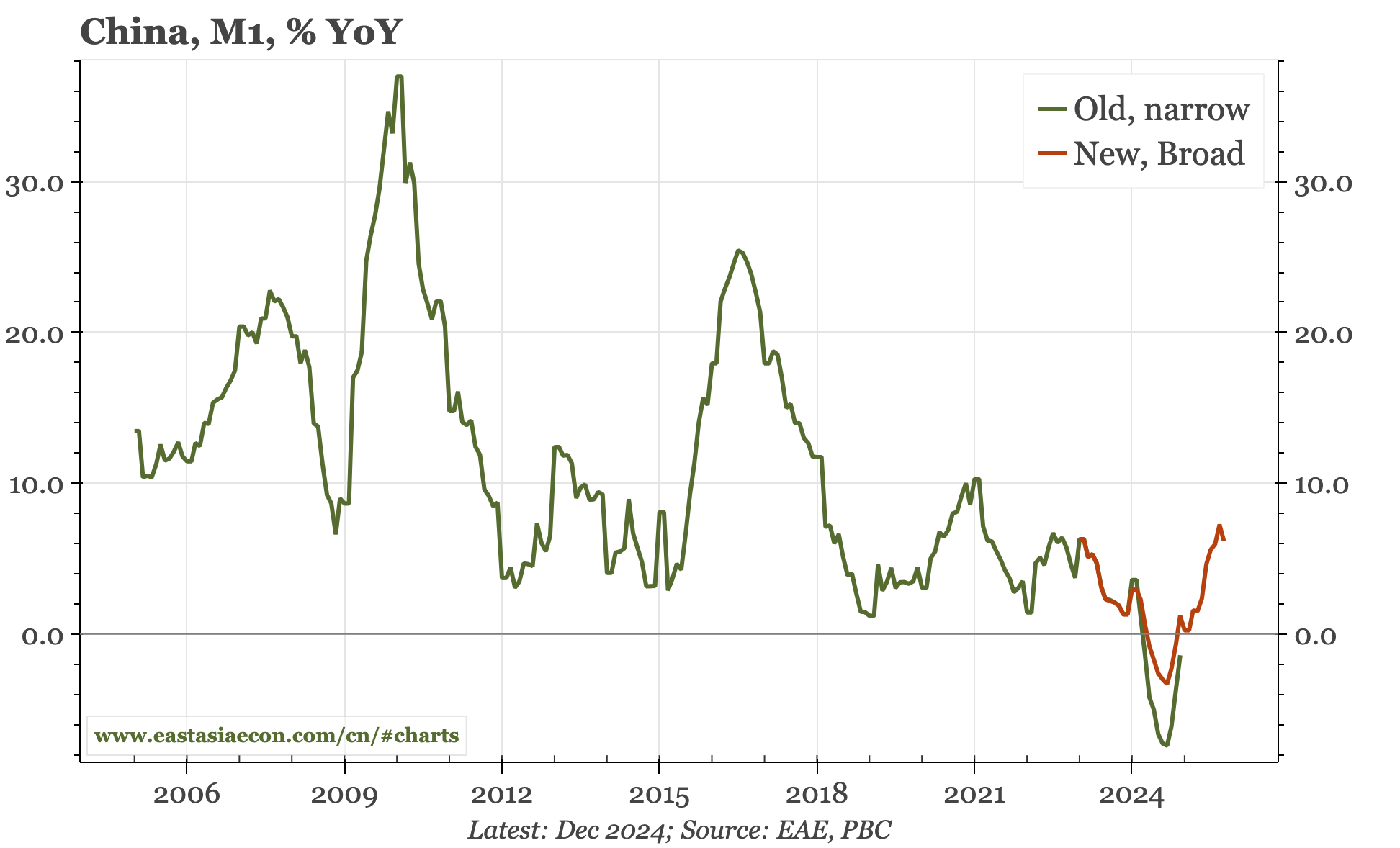

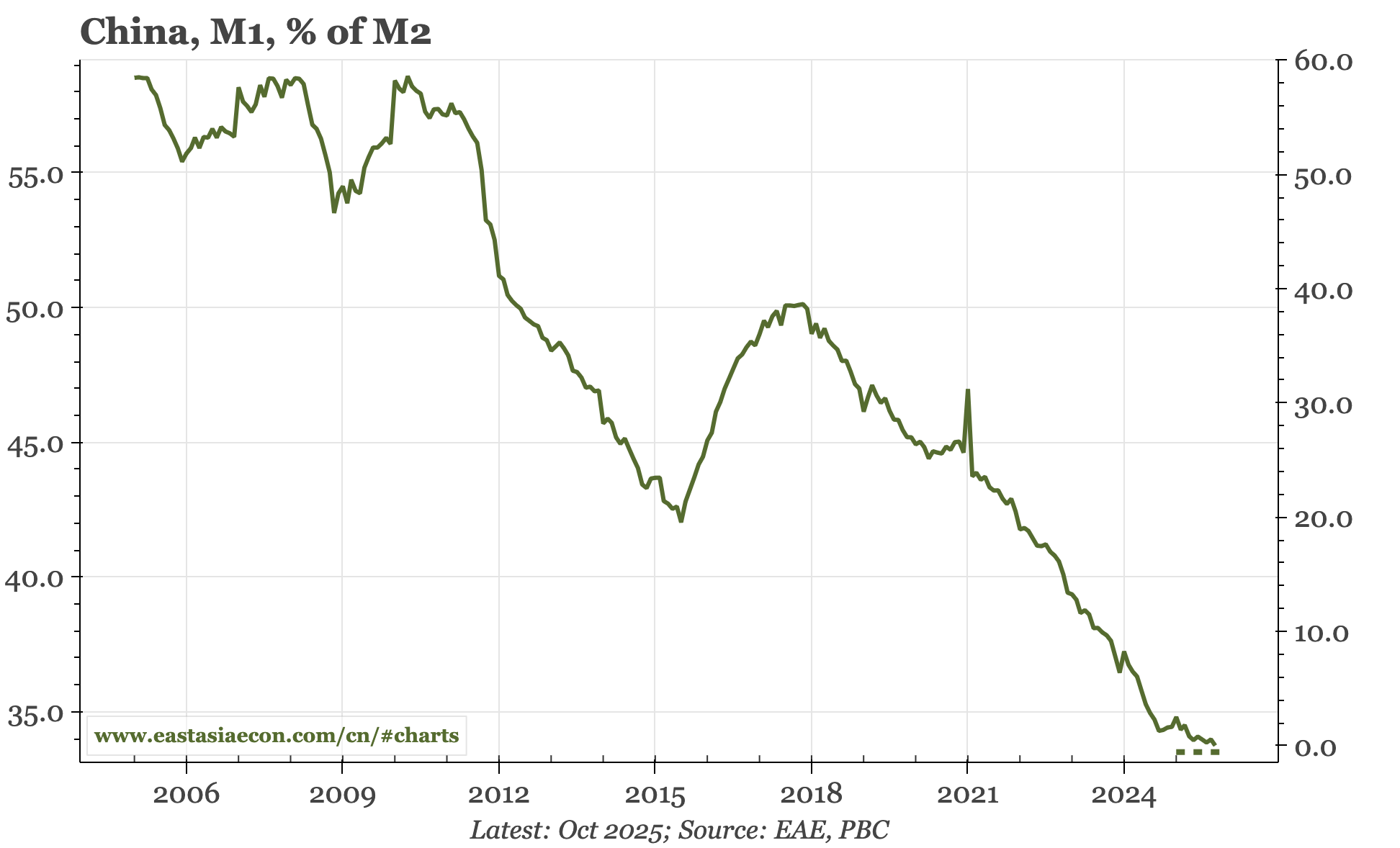

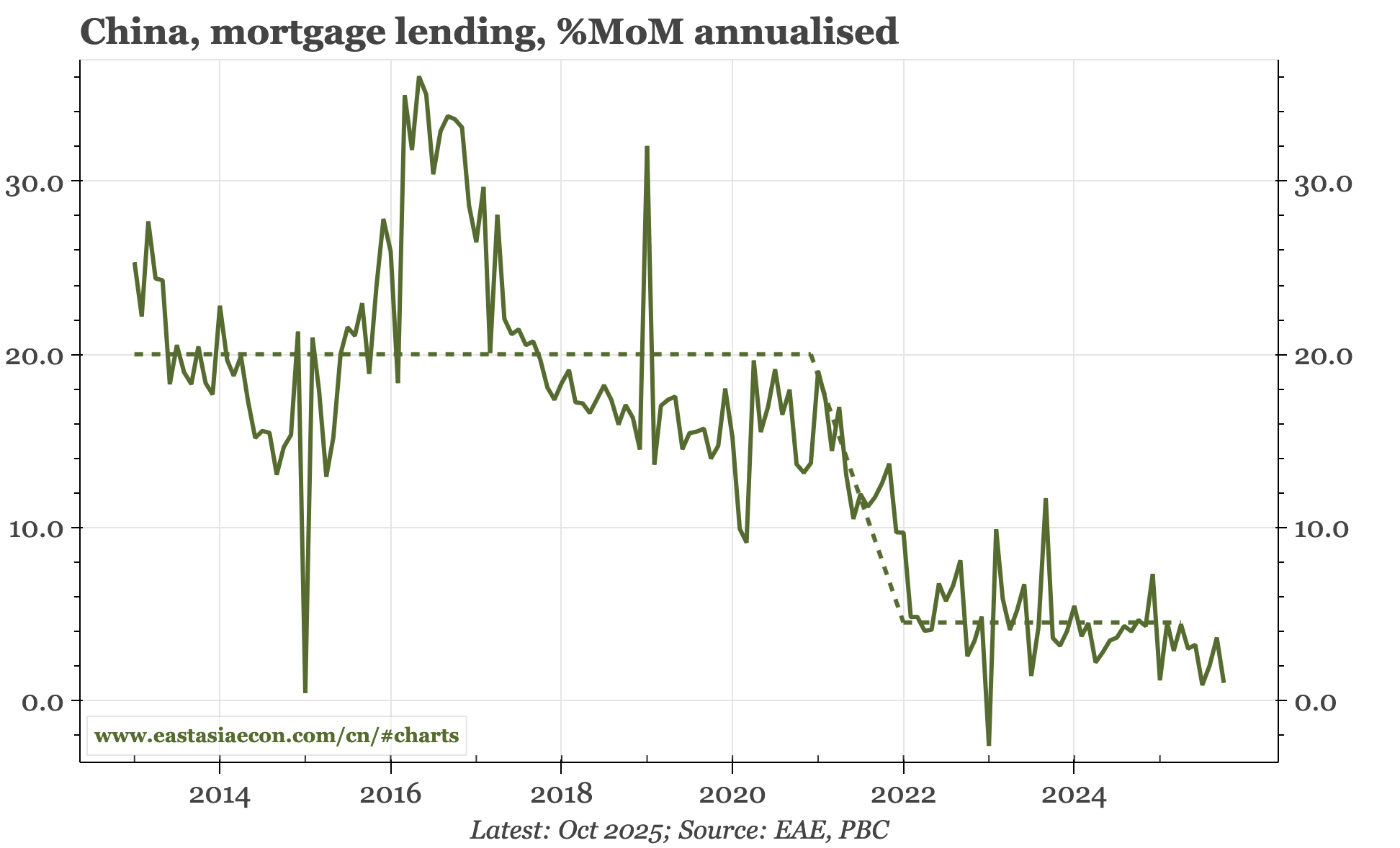

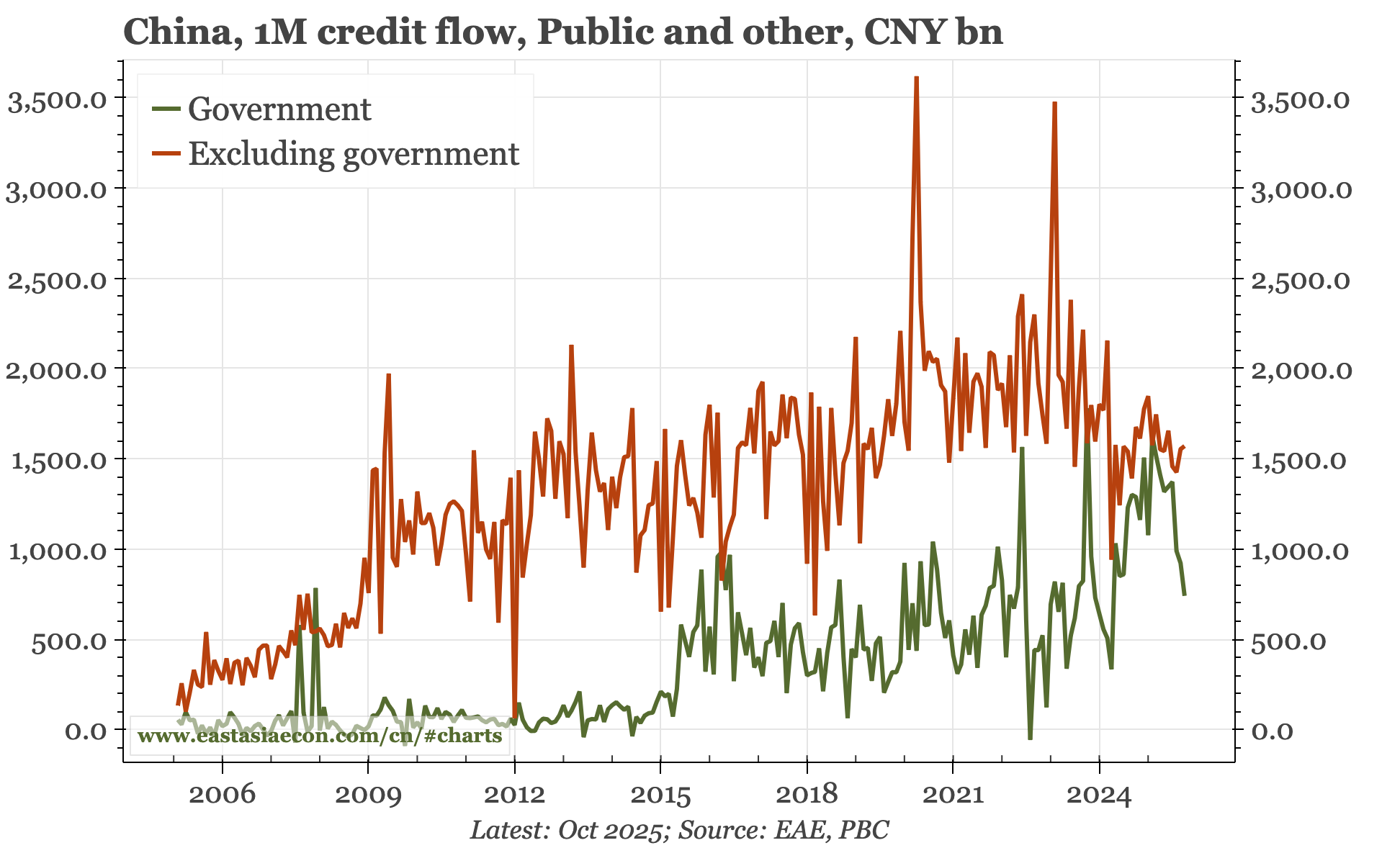

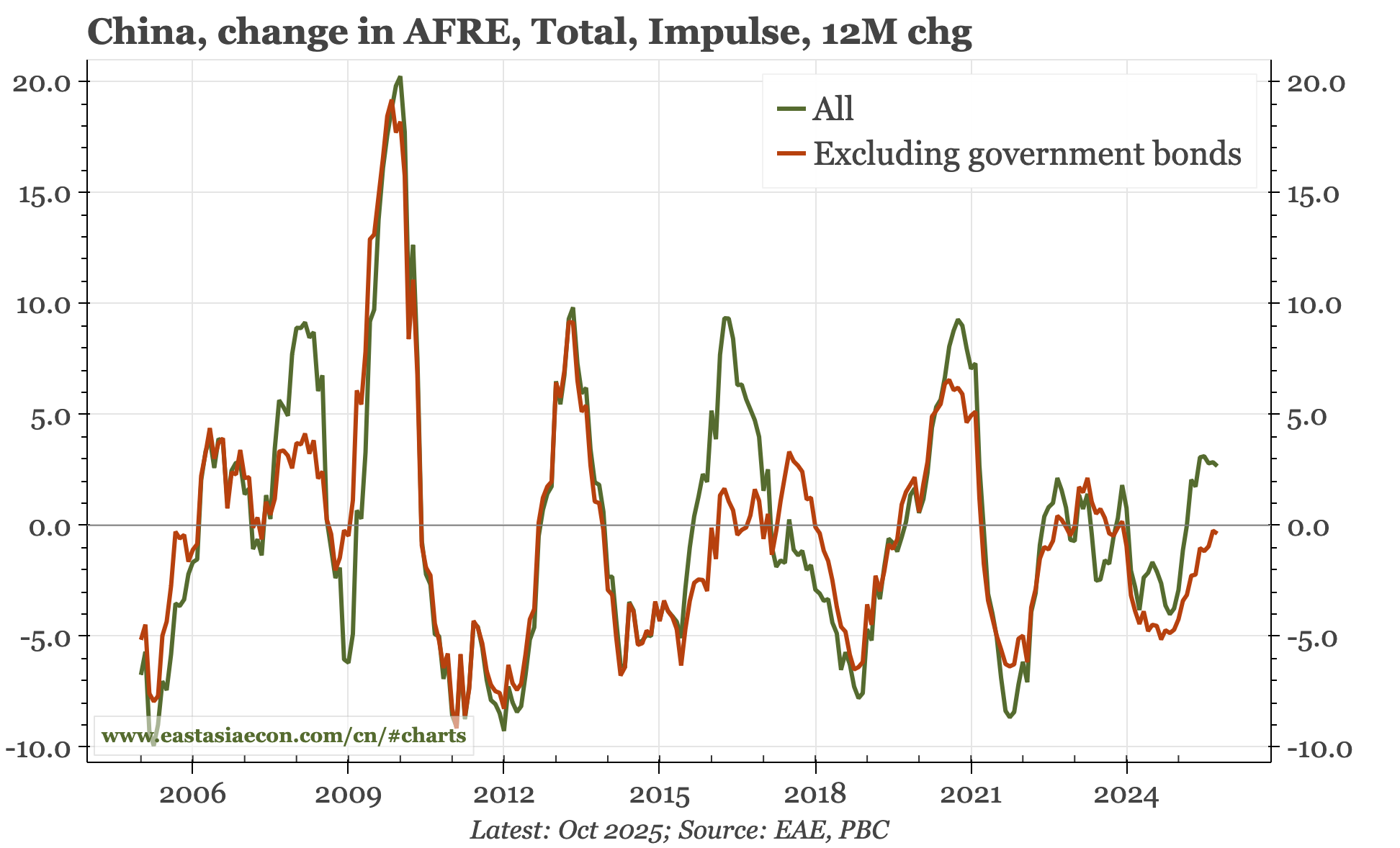

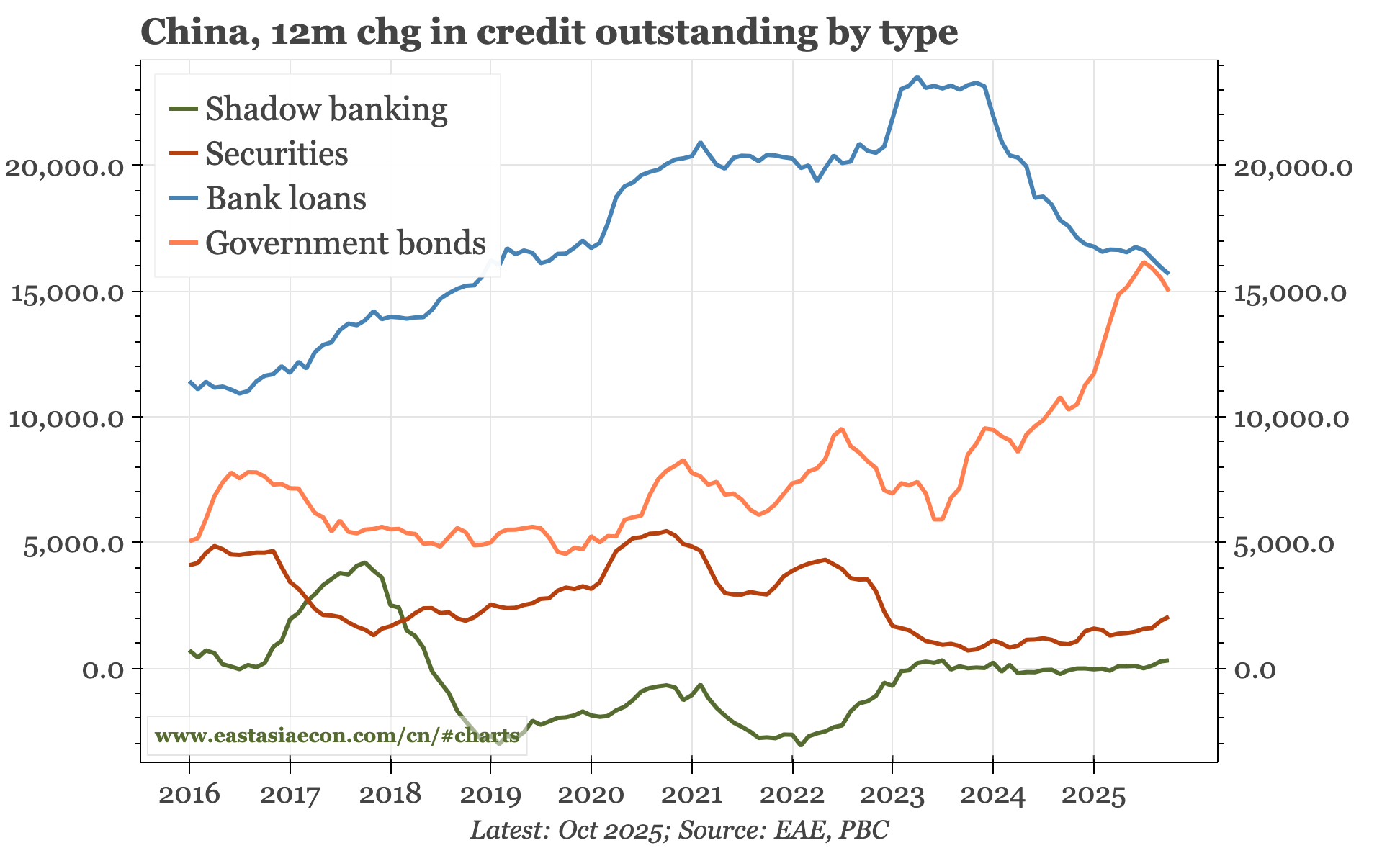

Cycle update – monetary data a bit softer in October. Relative to my idea that the underlying economy could be stabilising, today's monetary data for October are a little soft. In particular, both M1 growth and the M1:M2 ratio ticked down, and mortgage lending also slowed. Credit growth also dropped, but only because of less government borrowing.

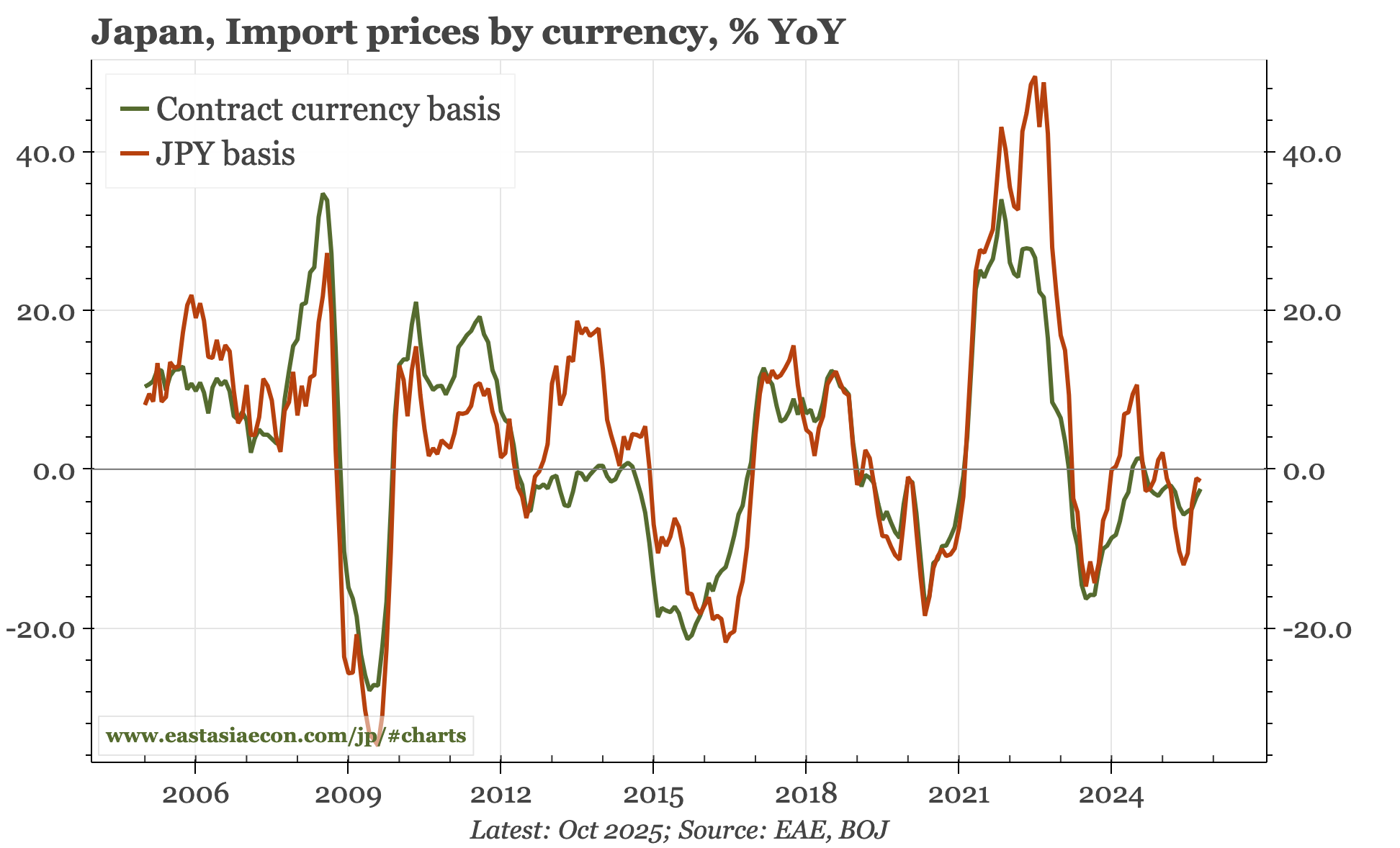

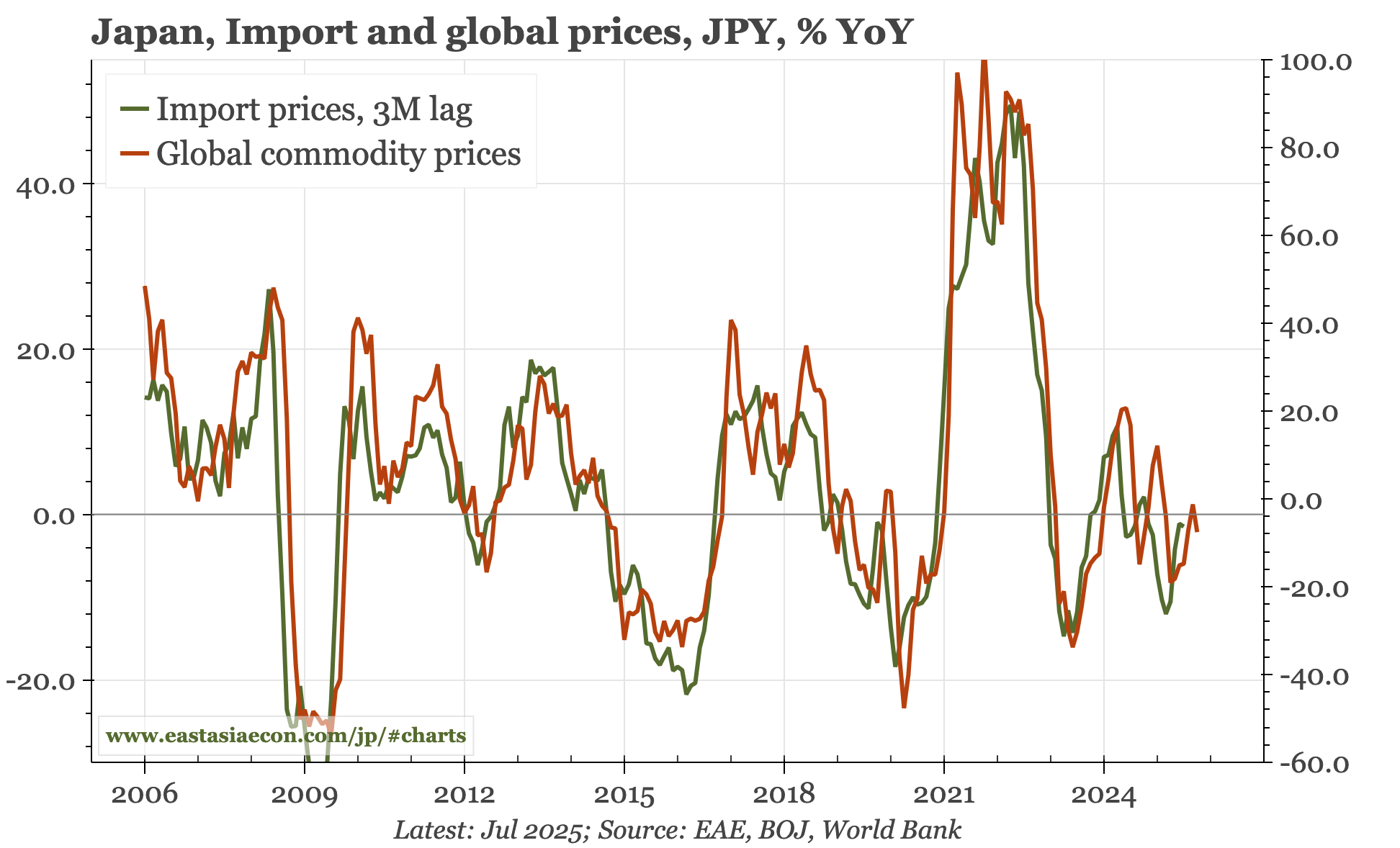

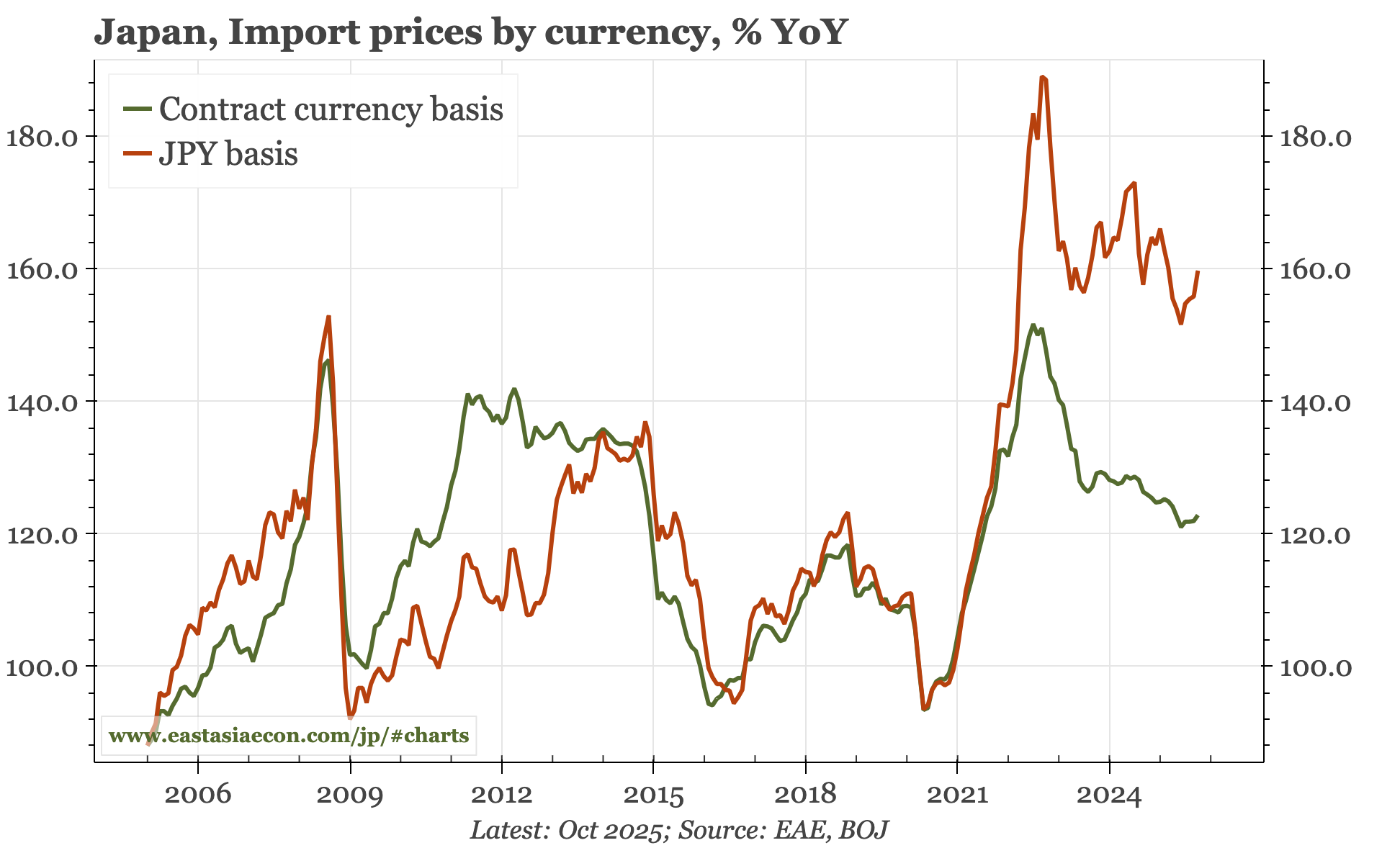

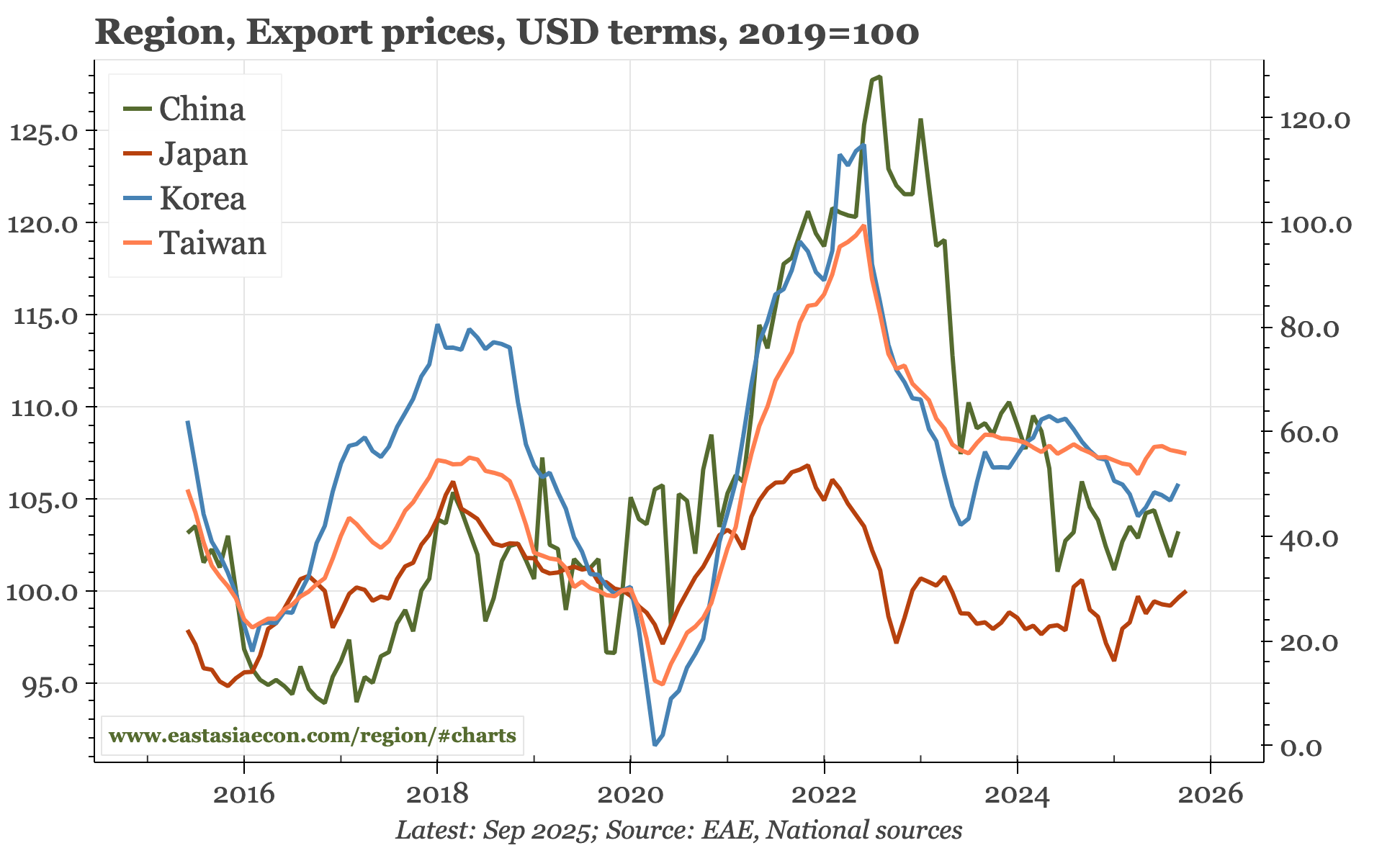

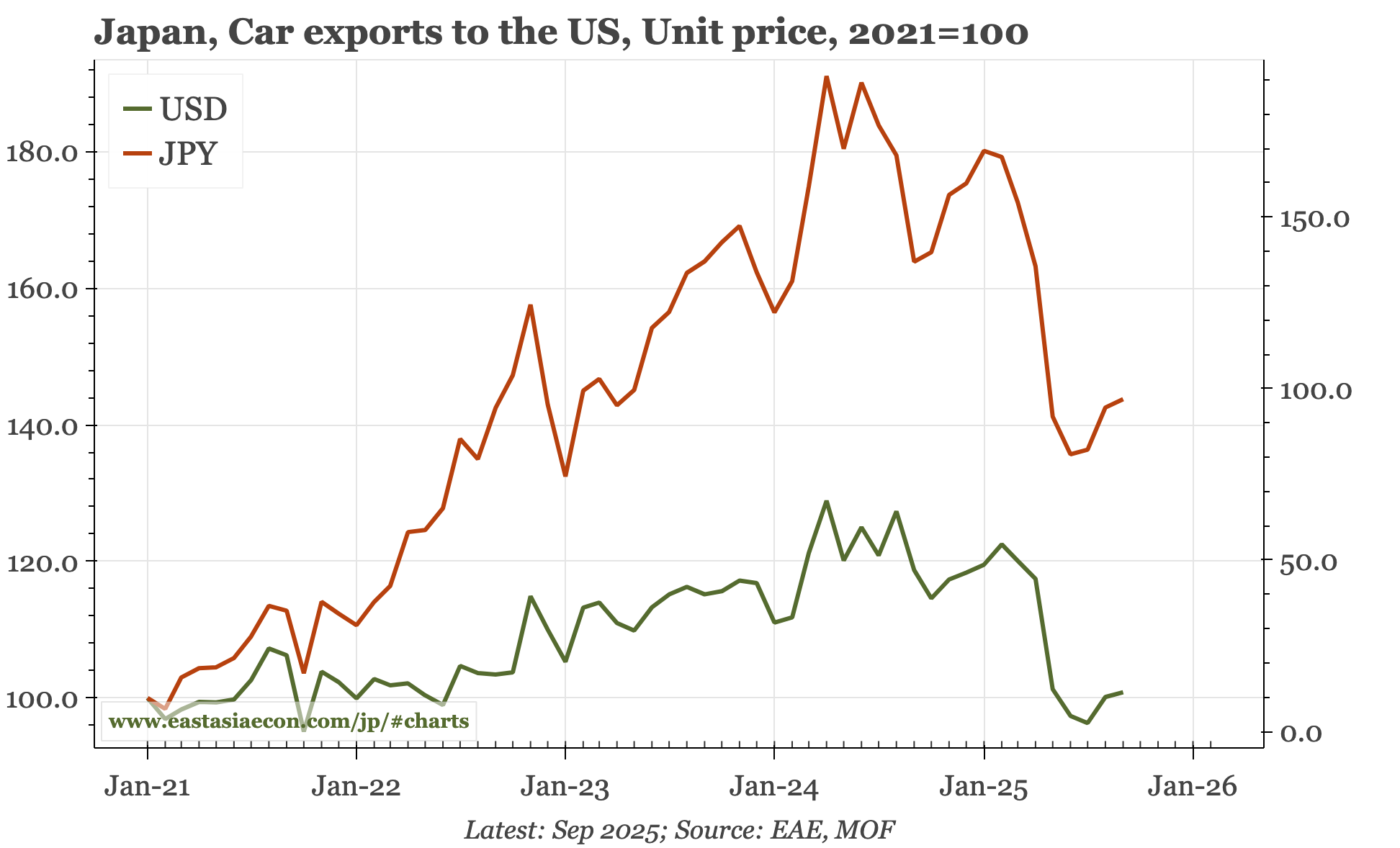

Cycle update – PPI still rising. The gap between import prices and PPI in the October data illustrates the sort of pent-up inflationary pressure in Japan that is likely to be exposed if the JPY remains so weak. Today's data also show a decent rise in auto export prices, but to a level that is still 6% below the pre-tariff level.