Japan – CPI rising, BOJ on hold

BOJ trimmed mean inflation continues to rise, but the BOJ is keeping policy unchanged. With rates remaining anchored, the JPY continues to sell off. The MOF has been talking about "stealth intervention", but it is unclear if that includes pressure on the GPIF to unwind some of its foreign holdings.

Trimmed mean CPI; BOJ meeting

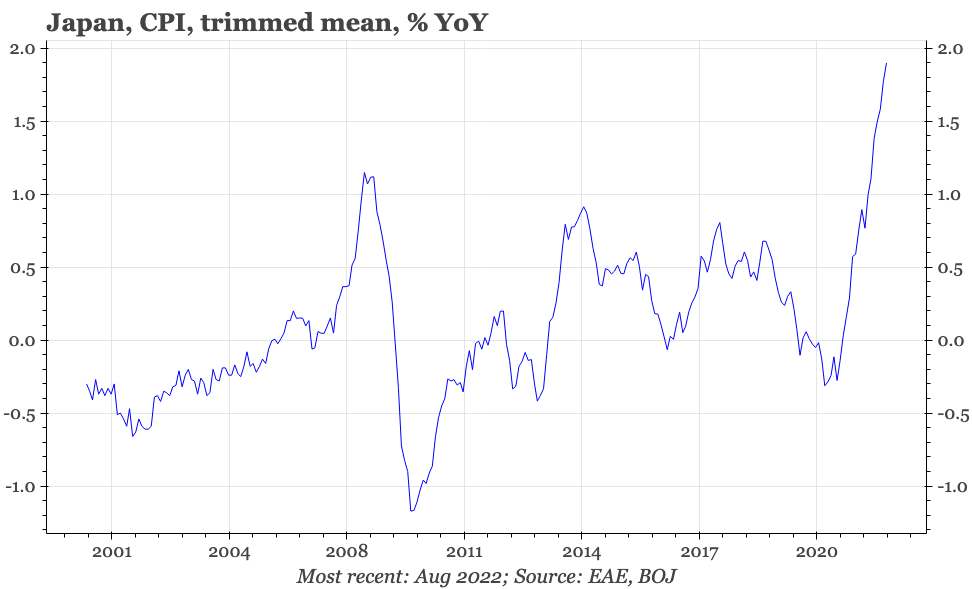

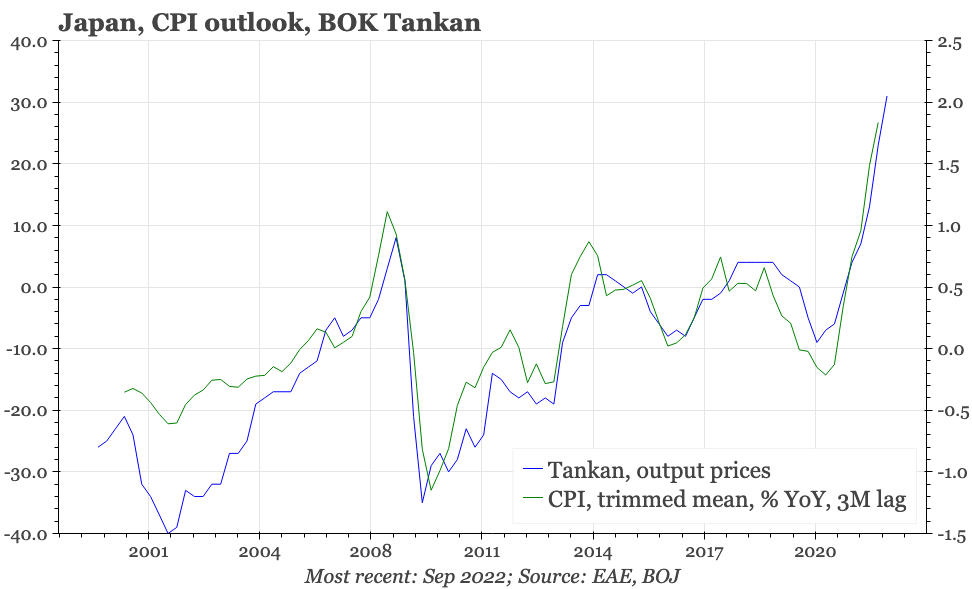

According to the BOJ's calculations of trimmed mean CPI, released today, this measure of underlying inflation reached 1.9% YoY in August. That's another record high since the series started in the early 2000s. On this basis, inflation continues to follow closely the lead of Tankan output prices, which suggest more upside from here.

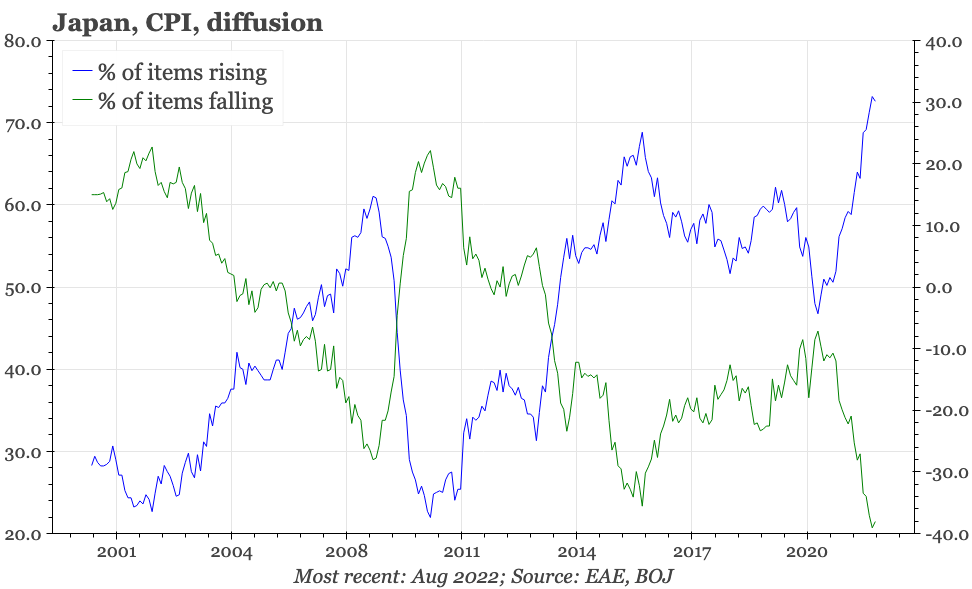

The BOJ's inflation diffusion suggests the prices of most products in the CPI basket are now rising. But the bank's official view remains that inflation isn't yet broad-based; instead, according to the bank's monetary policy statement today, inflation in Japan remains focused on “energy, food and durable goods”, which means it expects CPI inflation to decelerate next year “because the contribution of such price rises to the CPI is likely to wane”.

The bank likely needs to see the labour market tightening – unemployment is still above pre-pandemic levels – and inflation expectations holding up, to change its view. The challenge until then, of course, is the huge gap between the monetary policy direction in Japan and the US, and the resultant downwards pressure on the JPY. That has been seen in the last 24 hours, with $JPY reaching new highs on the back of both the BOJ's persistent dovishness, and the Fed's continued hawkishness.

This weakness of the JPY is rightfully becoming more of a concern for policymakers. The BOJ continues in its statements to refer to the need to “pay due attention to developments in financial and foreign exchange markets and their impact on Japan's economic activity and prices”. And the MOF, which in Japan has responsibility for fx policy, seems to be making its way up through the usual list of its FX management measures.

The problem for the MOF will be that unilateral intervention is unlikely to have a big impact while the monetary policy divergence is so wide. The MOF today has been talking about "stealth intervention". It isn't clear what that means, but it would be interesting if it includes pressure on the GPIF to unwind some of its (now highly profitable) foreign holdings.