Japan - sluggish

In Q3, the economy contracted. Leading indicators suggests that this is noise, and that a mild rate of growth should resume. But corporate sentiment remains unstable, and consumers continue to feel the pressure of rising prices.

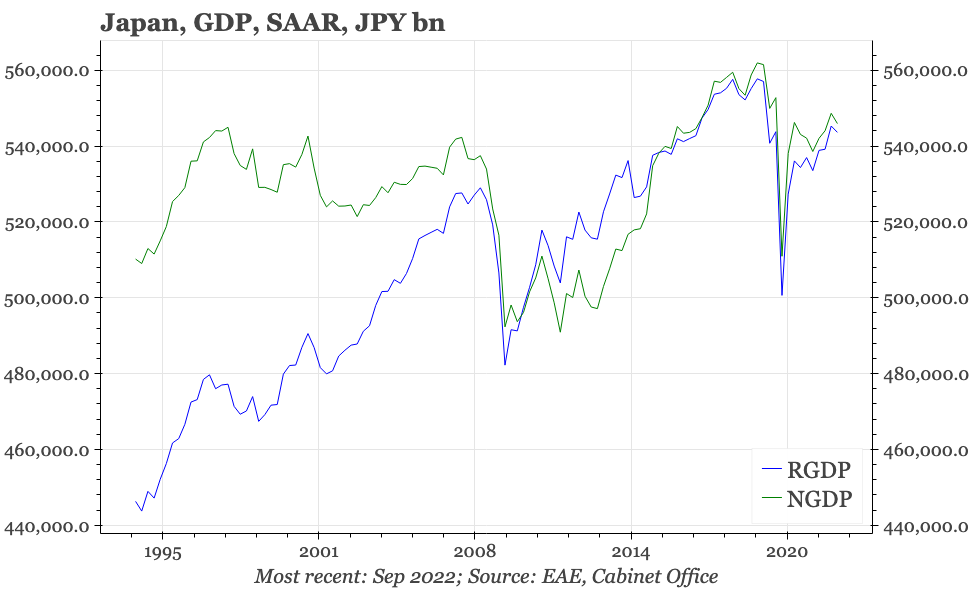

Q3 GDP data

The first cut of Q3 GDP data show that Japan's recovery out of covid remains sluggish. Indeed, in the three months to September, the economy contracted once again. The economy does continue to be larger than it was in Q419 before the pandemic hit, but that is misleading. Because of the sales tax hike in October 2019, the economy was already in recession when covid came along. As of September this year, real GDP was 2.4% smaller than it had been three years before.

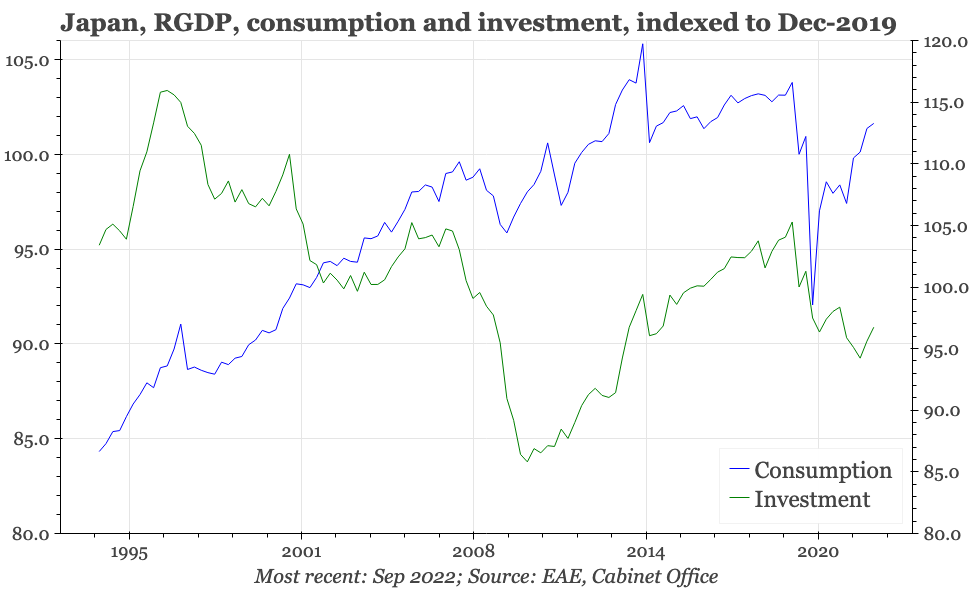

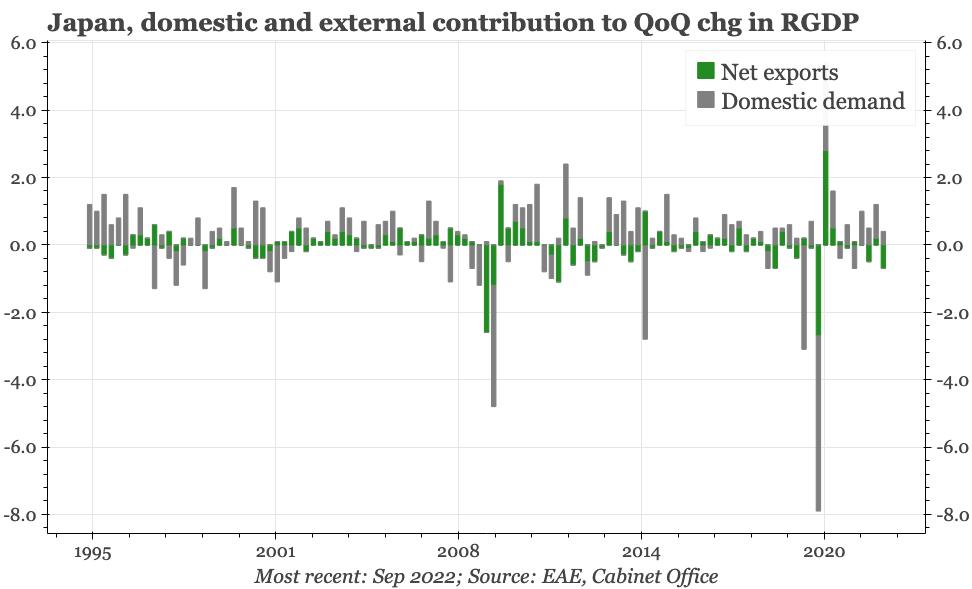

Private consumption did continue to grow in Q3 this year, but the pace of recovery slowed. Investment spending was more buoyant last quarter, but from a lower starting point: while consumer spending closed last quarter 2.9% below the peak of September 2019, the deficit for investment spending is nearer to 10%. The overall mild rise in domestic demand in Q3 wasn't big enough to offset the negative contribution from net exports.

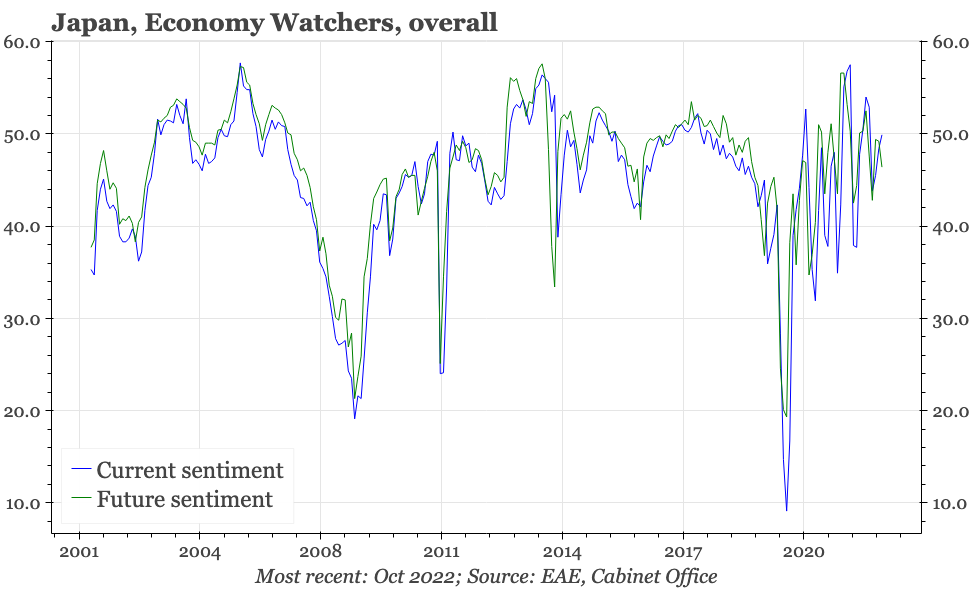

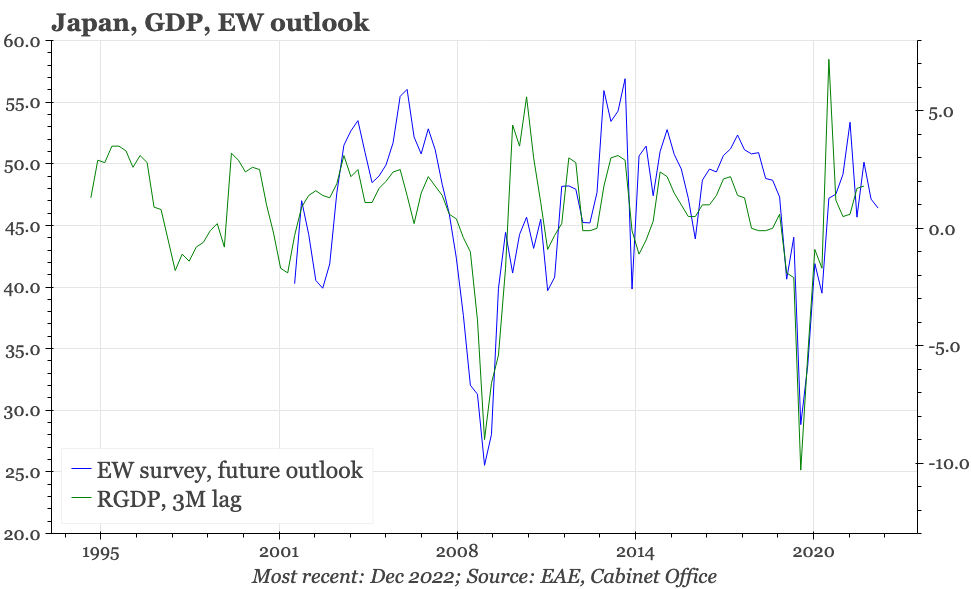

The outlook doesn't look too different. Last week's Economy Watchers survey suggested the economy is continuing to grow, but at a fairly low rate. Sentiment in the survey isn't too bad, but the huge volatility from month to month – a phenomenon that wasn't apparent before covid – suggests that uncertainty remains elevated. That probably has a particularly big impact on corporate investment. For households, the bigger overhang is inflation. Import price data for October don't suggest that price pressures are intensifying, but also don't suggest any real lessening yet.