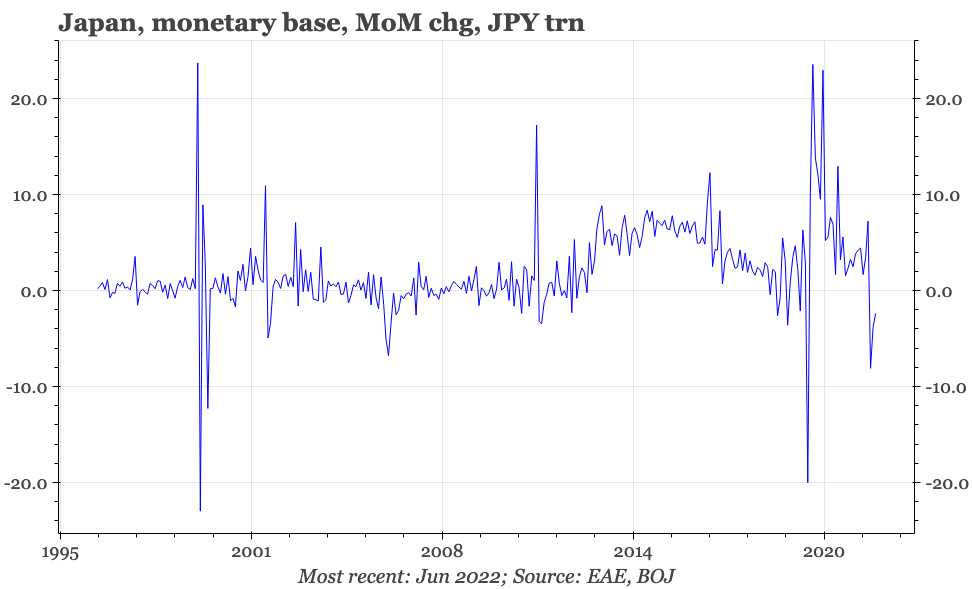

Japan - June monetary base

Despite all the JGB buying in June, Japan's monetary base actually contracted in the month. That was because of the winding down of the Covid-19 lending programme, and shows monetary expansion isn't as wild as headline data alone would suggest.

Given all the BOJ's buying of JGBs in June, it would be easy to imagine that the economy last month was flooded with money. And yet, the monthly data from the BOJ show the monetary base actually contracted, continuing a trend that first appeared in April.

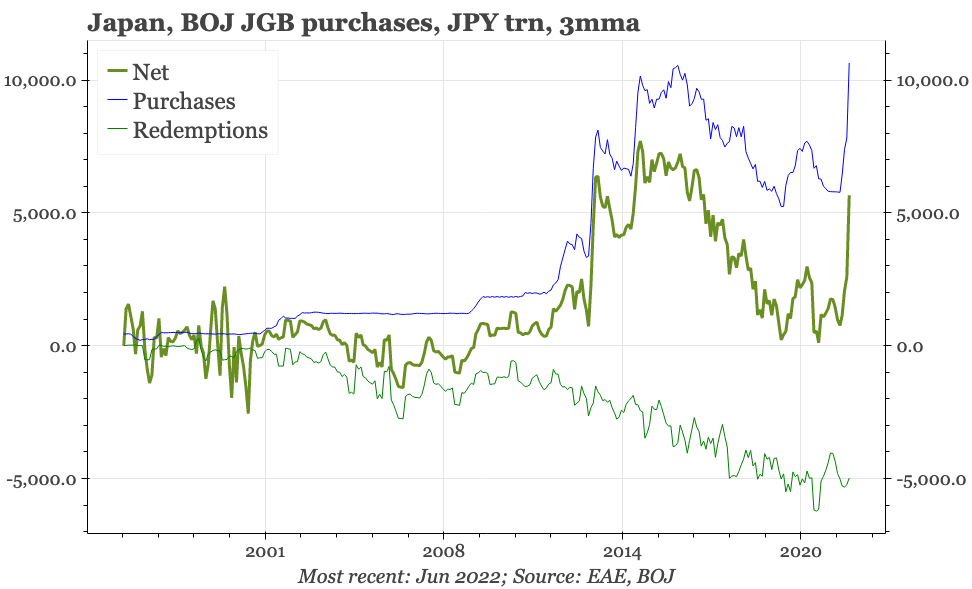

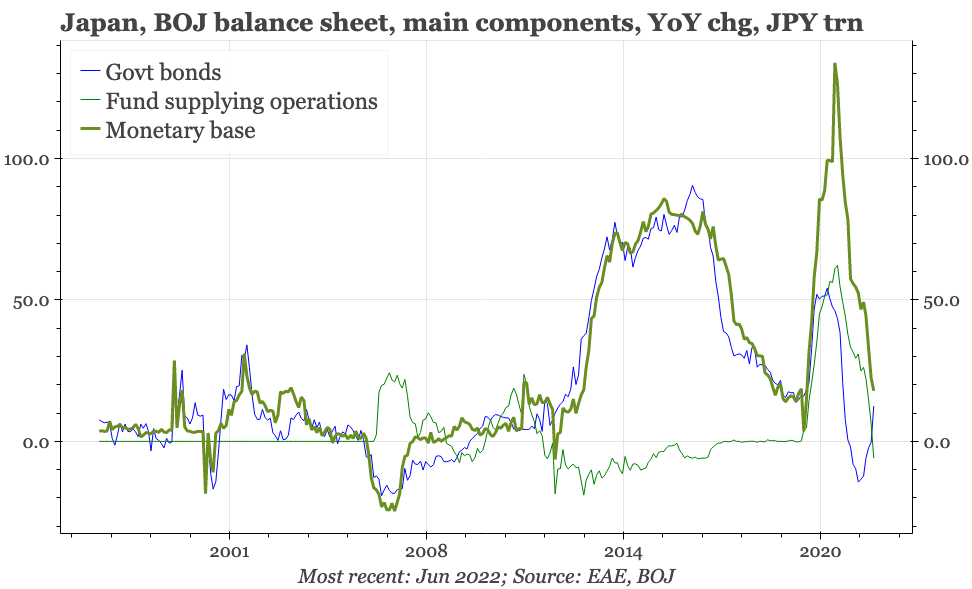

Gross buying of JGBs was indeed immense: the BOJ outright purchased JPY16bn in JGBs last month, by far the highest on record. But while net purchases of JGBs also rose, the increase was more modest at JPY4.2trn. This is because of redemptions, which have grown in recent years in line with expansion in the stock of bonds held by the central bank. At the same time, last month the BOJ's Covid-19 lending programme continued to be down, contracting by JPY11trn.

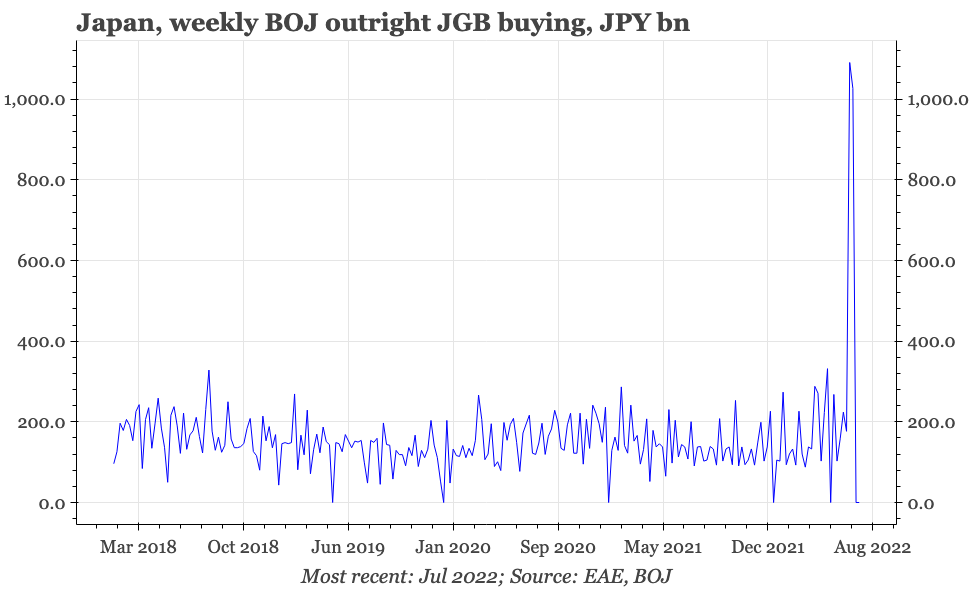

Perhaps needless to say, the reason for JPY weakness in June was more differentials in interest rates between the US and Japan than the rate of monetary expansion. If US interest rate start rising again, the JPY will once again be in trouble. However, there's reasons to think that if the recent fall in US rates persists, then the debate about the Japan and the JPY can quickly shift. Not only are there factors other than JGB buying that can affect the BOJ's balance sheet, but even for JGBs, the June buying spree hasn't been sustained, with daily data showing a sharp fall back so far through July. So if US rates don't start rising again, the story may not be about the BOJ's crazy expansion of central bank liquidity, but rather what the central bank can do to stop the monetary base from contracting.