Japan – tariffs matter, but so does inflation

Like most other observers, I think it unlikely that the BOJ changes policy this week. But given domestic price developments, there isn't much room for dovishness. And if the US really wants to tackle global imbalances, it has an interest in creating the conditions that allow the BOJ to hike further.

With a BOJ leadership focused on avoiding the tightening-too-early mistakes of the past, the risk from tariffs and US policy more generally is highly likely to keep the bank on hold this week. Policymakers will be openly worried about global growth, and privately concerned about the prospects for JPY strength.

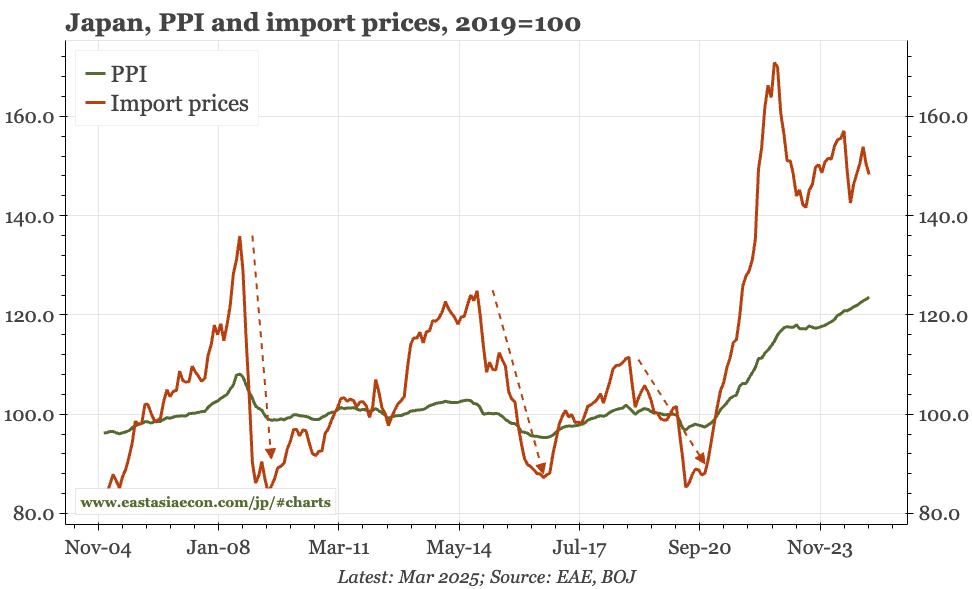

However, it is worth emphasising that domestic price and wage developments since the BOJ's last meeting have been overwhelmingly constructive, with highlights including the Tankan, the pent-up inflation shown by the gap between rising PPI and falling import prices, a jump in part-time wages, and higher rental inflation.

If there isn't a permanent moderation of tariffs, against Japan and other Asian economies, recession seems likely. Historically, it has been combinations of global downturn and JPY appreciation that have helped end previous upturns in inflation. From here, import prices and PPI remain important to watch.

If recession and lower PPI are the outcome this time, then we've probably seen the peak in the policy rate. However, given the strength of domestic indicators, further BOJ hikes remain possible if the risk of tariffs moderates. And, given their apparent desire to see the USD weaker, some officials around Trump will presumably be arguing to the president that it is better for the US to create circumstances where the BOJ does indeed continue to hike.

Prices and wages

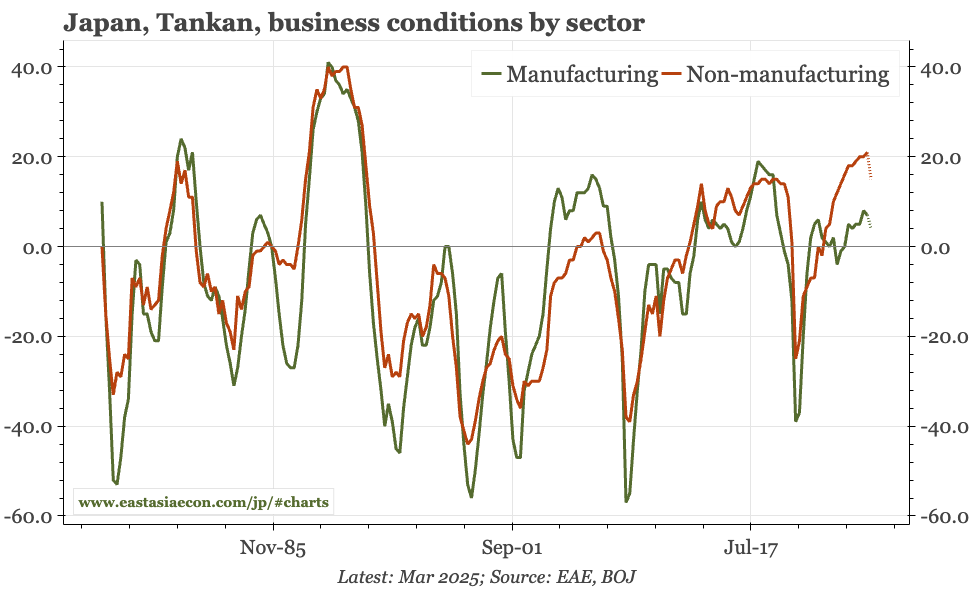

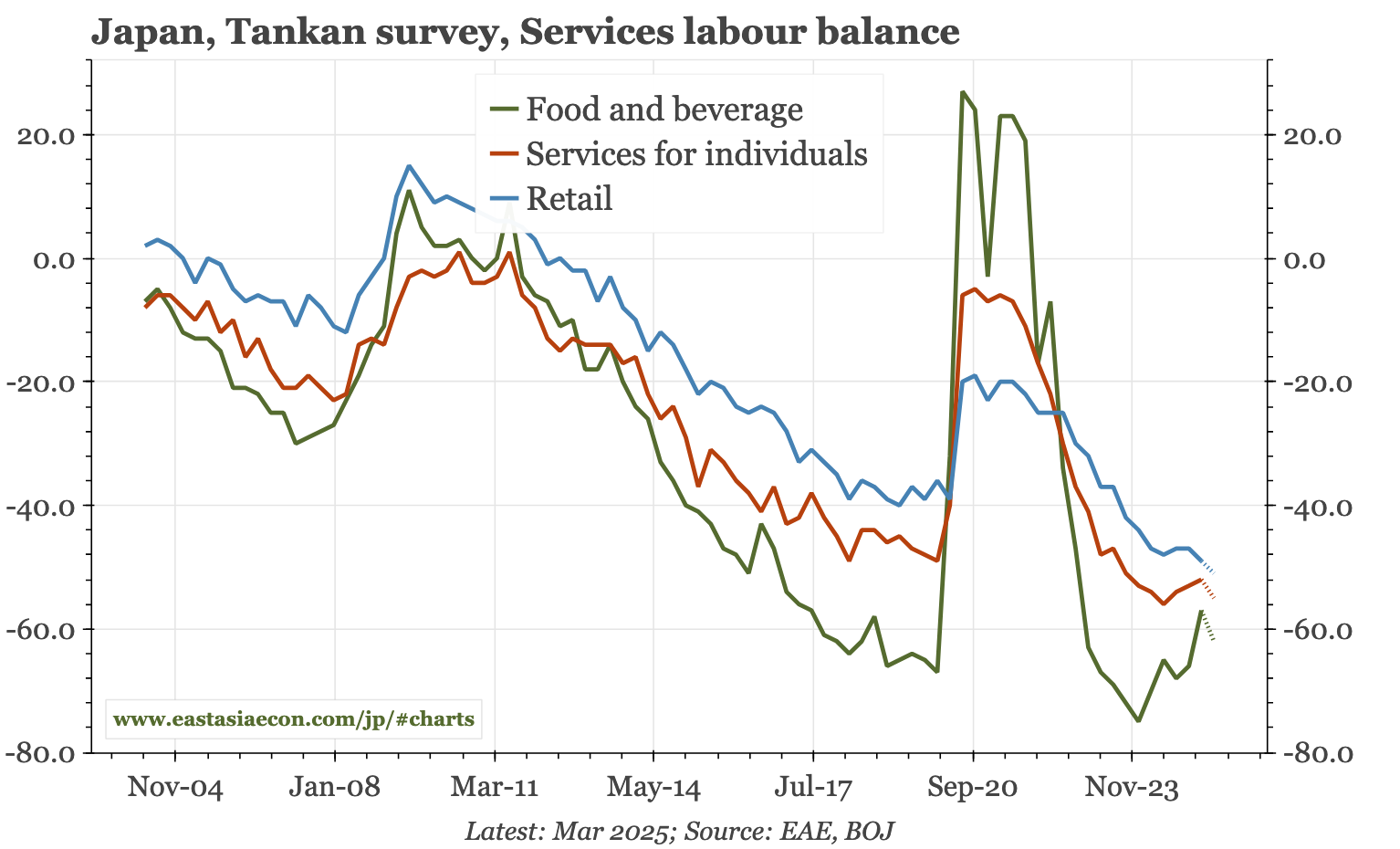

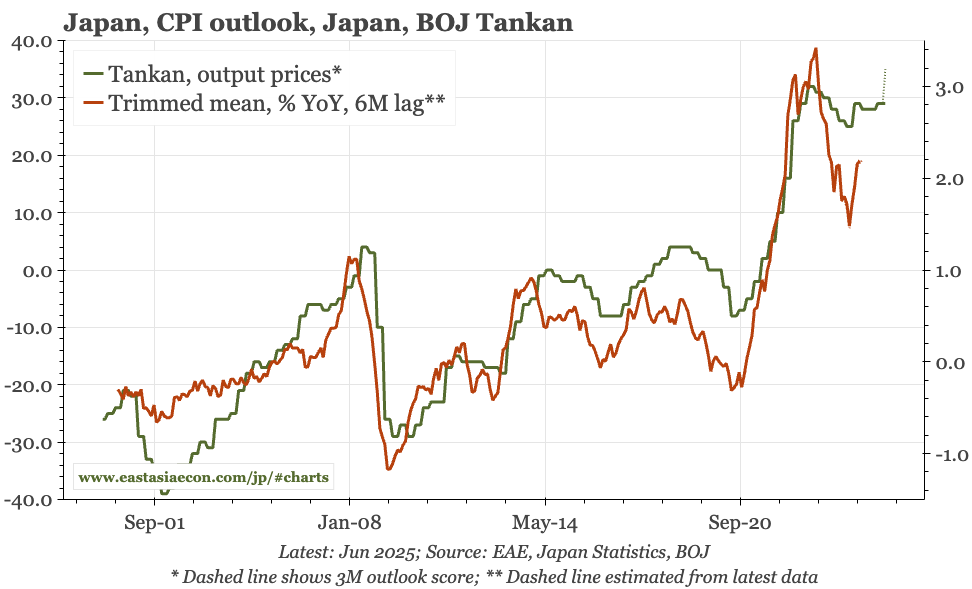

The Tankan showed the BOJ's base case remaining very much alive. The main dynamic for the central bank is structural labour market tightness feeding into faster growth in wages and prices. The Tankan showed the labour market remaining tight, especially in the more labour-intensive services sector. At the same time, price intentions in the Tankan continued to move up, and historically, they have been a good guide to the direction of trimmed mean inflation.

The idea that Japan remains in a positive price-wage cycle has been supported by other recent data. The BOJ's consumer confidence survey showed inflation expectations remaining elevated. The first cut of part-time wage growth for March reached 5.6% YoY, with the commentary attributing the acceleration partly to a push from this year's shunto. In a sign of pent-up inflationary pressure, PPI inflation has continued to move up in recent months, even though import prices are now falling.

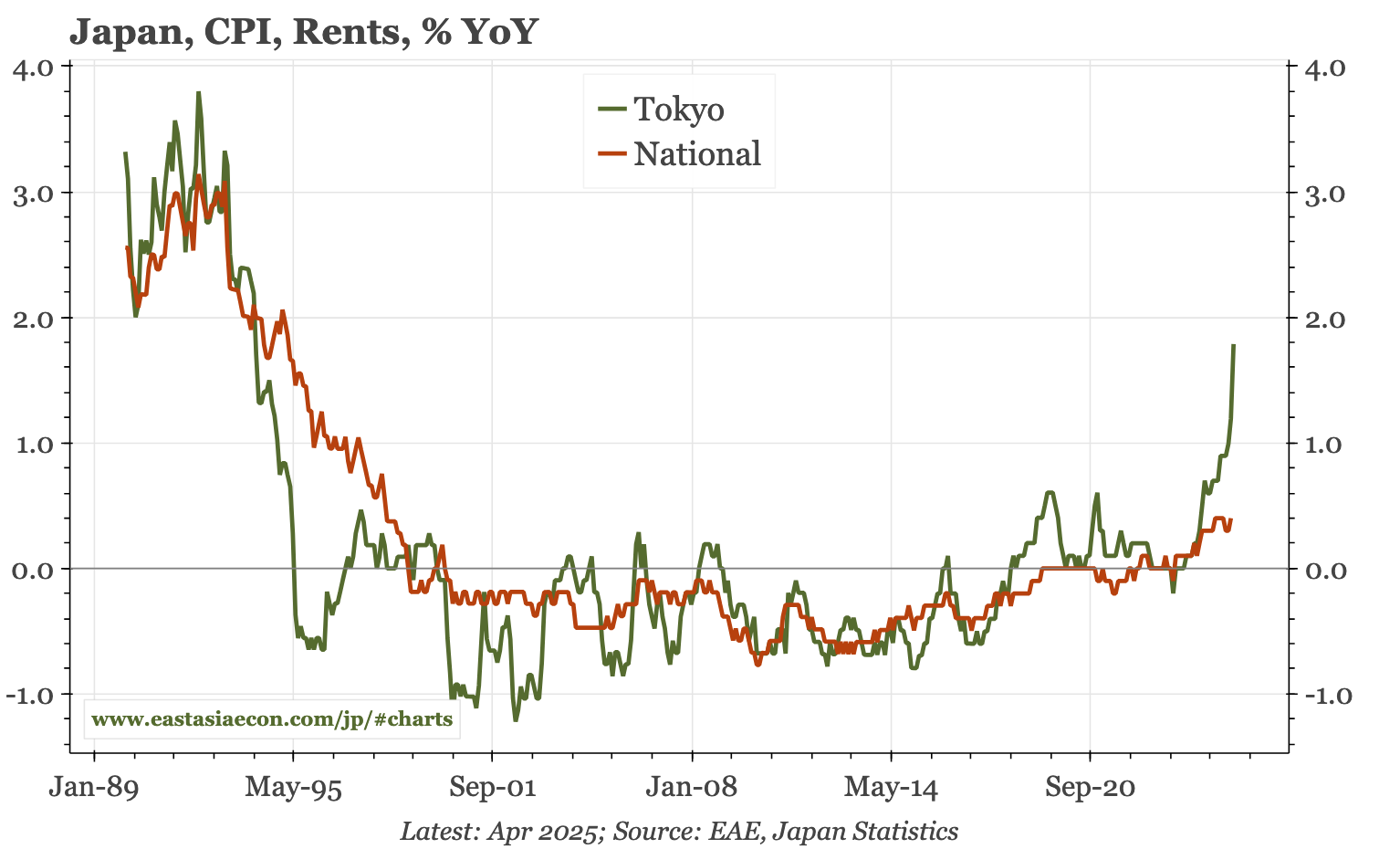

Last week's Tokyo CPI for April was particularly important. That wasn't because of the headline, even though that accelerated back to 3.5% YoY, the highest since early 2023. More significant were the signs that inflation continues to become more broad-based. In that respect, the star of the show in this last release was rental inflation. That rose to a new multi-decade high of 1.8% YoY, up from 1.3% the previous month. That rise matters because rents have a weighting of almost 25% in the overall index – it is highly unlikely that overall inflation can sustainably reach 2% if rentals continue to fall as they did between for the 20 years from 2000.

All told, it isn't surprising that members of the BOJ's monetary policy board have sounded concern about upside risks to inflation. Speaking earlier this month, Junko Nakagawa argued:

The sustained inflation seen thus far has brought about a rise in households' and firms' medium- to long-term inflation expectations, and firms' behavior has shifted more toward raising wages and prices. Apart from the potential impact of trade policy that I mentioned in the first risk, it is likely that firms' price revisions in response to past inflation are still in progress, as I explained earlier. In this context, upward pressure on wages could intensify further with labor market conditions remaining tight, and moves to reflect the past inflation and higher wages in selling prices could strengthen to a greater extent than expected.

Tariffs

It is important that these remarks were made after Trump's Liberation Day announcements. But nobody would argue that all the positive domestic developments don't now need to be analysed alongside the possible impact of his tariff barrage. Indeed, for a BOJ leadership that clearly doesn't want to repeat the tightening-too-early mistakes of the past, Trump's tariffs are especially important.

The transmission from the trade war to Japan's economy is two-fold. First, a sharp decline in global trade would risk pushing Japan into recession. Second, flight from the USD pushes up the JPY. Historically, global recession and exchange rate appreciation, by reducing JPY import prices, have often been the combination that has ended upswings in Japan's inflation.

Different governments have rushed to send delegations to the US with the hope of negotiating the tariffs away, with Japan's being the first to get a meeting. Perhaps these talks will be successful. The Trump administration would seem to have an incentive to announce that the Liberation Day pain has been worth it, and that other countries are yielding to US demands. Perhaps Trump will announce something today in his speech to mark the first 100 days of his second term.

As for Japan, it probably wouldn't be too painful for Japan to sign on to the Alaska LNG deal. Given high food prices, it should be somewhat easier for Japan's politicians to allow bigger agricultural imports from the US than would have been the case in the past. For that, though, it would be helpful if Japan's government was in a strong position at home. But that clearly isn't the case. The popularity of Prime minister Ishiba, already leading a minority government, has been dragged down further by the sort of political scandals that are very common in Japan. Given that, he will be under pressure not to take risks that would further reduce LDP support in the run-up to this year's Upper House election, due to be held before the end of July.

Risks

It could be that tariffs are applied, but Japan manages to avoid a big downturn. The probability is small, but it isn't impossible. That's because Japan's cycle since the end of the covid pandemic has clearly been led by services: the manufacturing PMI has already been below 50 for all but four of the last 30 months. Of course, it is partly because of the weakness in industry that Japan's overall growth has remained sluggish since the end of the covid pandemic. But service activity has been stronger, and has been the big driver of the continued tightness of the labour market. A big further drop-off in manufacturing would throw Japan's economy off course, but further incremental weakness likely wouldn't.

There is a school of thought that if a recession is in the offing, the US administration wants to have it sooner rather than later. That may be true, but if the Trump administration really wishes to resolve the US's external imbalances, then a recession is unlikely to be helpful. Japan, and Taiwan too, are right now running generationally high rates of price and wage inflation. If these trends remain in place, the outcome should be a narrowing of the structural interest rate differential with the US, which in turn would drive sustainably stronger Asian currencies.

With Trump himself seeming to want a weaker USD dollar, this kind of interest rate normalisation in Asia would thus be in US interests. However, as the debate around this week's BOJ meeting shows, the process of normalisation is likely to be thrown off course by tariffs that induce global recession.