Japan – still sluggish

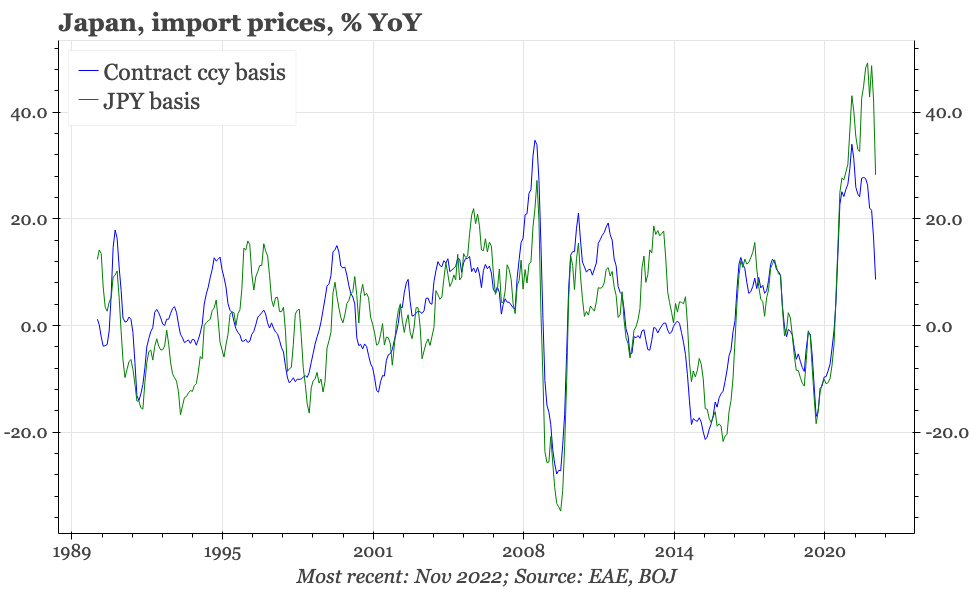

Japan's cycle remains sluggish, partly because of import price inflation, though that receded in November. In theory, post-covid opening up of the economy should add momentum to the modest wage and service price inflation being seen. But that feels optimistic given softening business sentiment.

Taking stock

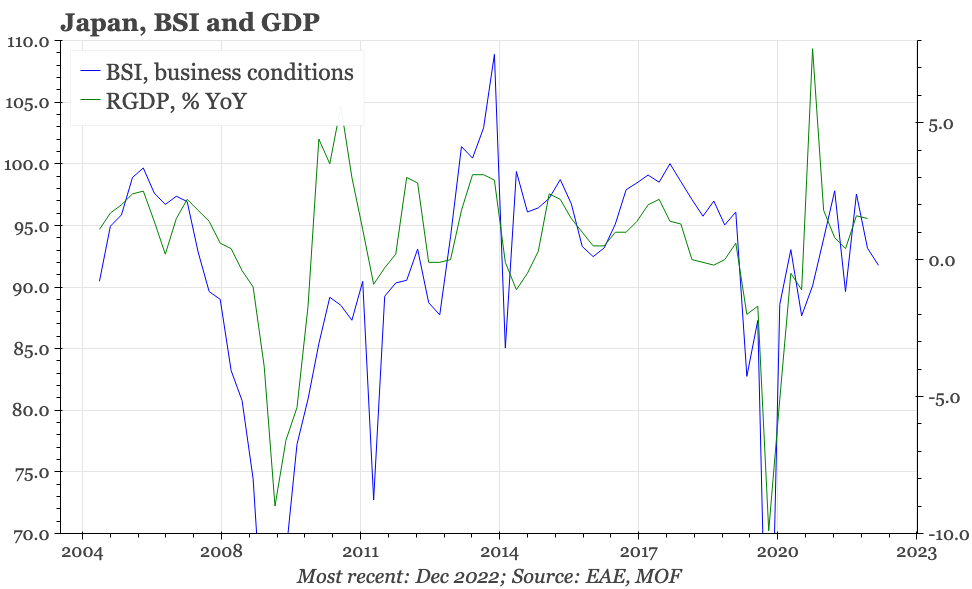

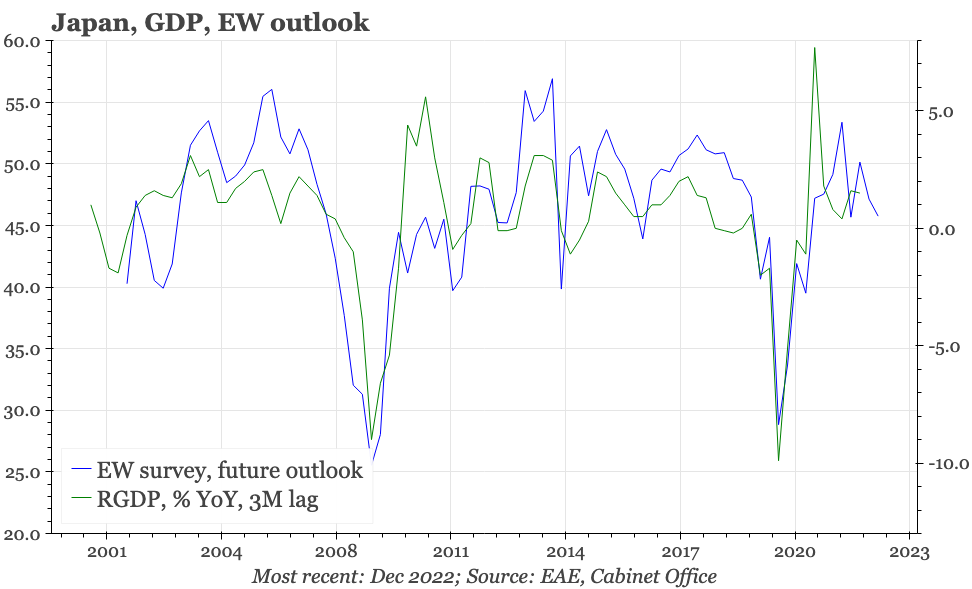

Japanese business sentiment is soft, but not terrible. In the MOF's quarterly survey that was released today, companies' assessment of current business conditions fell modestly. There were bigger declines in the 3M and 6M outlook scores. Like last week's Economy Watchers survey, this all suggests that the economy into Q4 might be just about growing, but little more than that.

That is disappointing, given Japan's economy has already been struggling to recover after the covid pandemic. Far from gaining momentum, revised Q3 GDP data released last week showed that the economy had contracted again. One driver of this sluggishness has been the sharp rise in inflation, which has largely been driven by import prices, and has greatly outpaced domestic wage growth. That has resulted in a collapse in consumer confidence.

Given that, it is good news that the import price squeeze is at last beginning to recede. Data released today showed that import price inflation in November slowed to 28% YoY, easing from more than 40% in October – which itself was down from the peak of nearly 50% through the Japanese summer. The modest appreciation of the JPY in recent weeks has contributed to this drop, reinforcing the impact of falling global USD commodity prices.

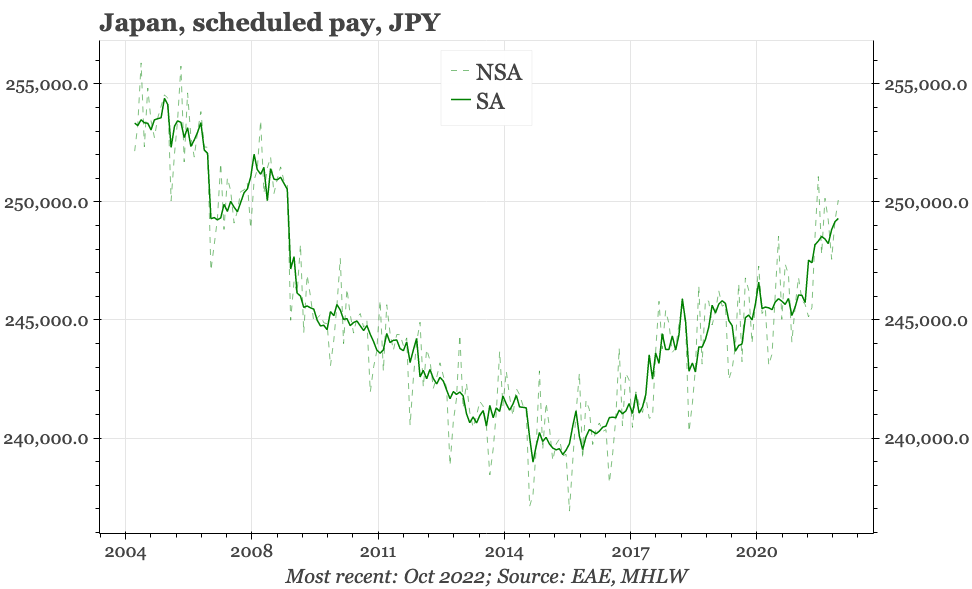

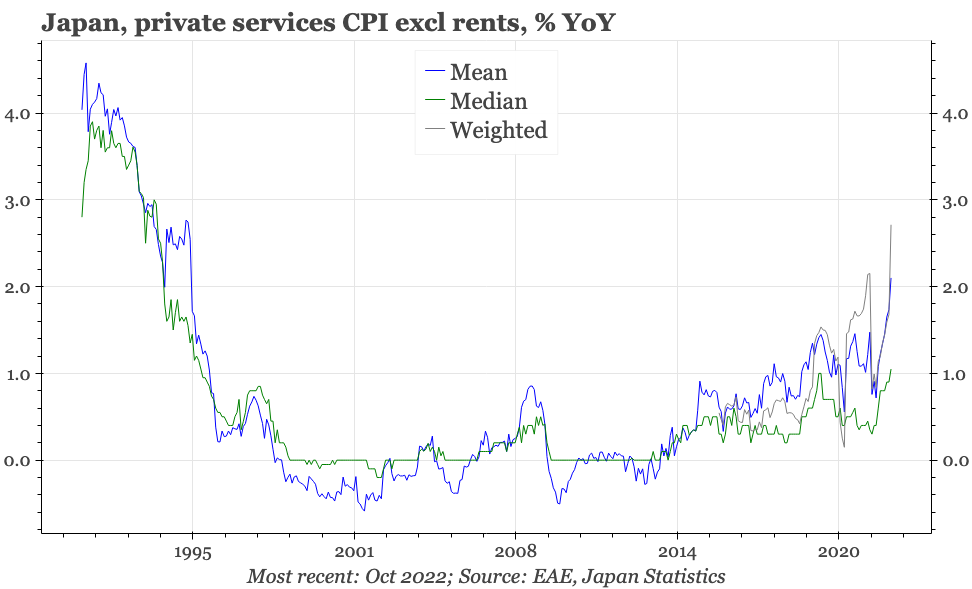

Again, it is the sharp rise in JPY commodity prices that can explain most of Japan's inflation. However, there have been some signs though that domestically generated inflation is beginning to appear: wage growth has been picking up, and services price inflation has started to emerge. This is the sort of process the BOJ would like to see, hinting at some possibility for wage-price reflation to take over from the import price real wage squeeze of 2022.

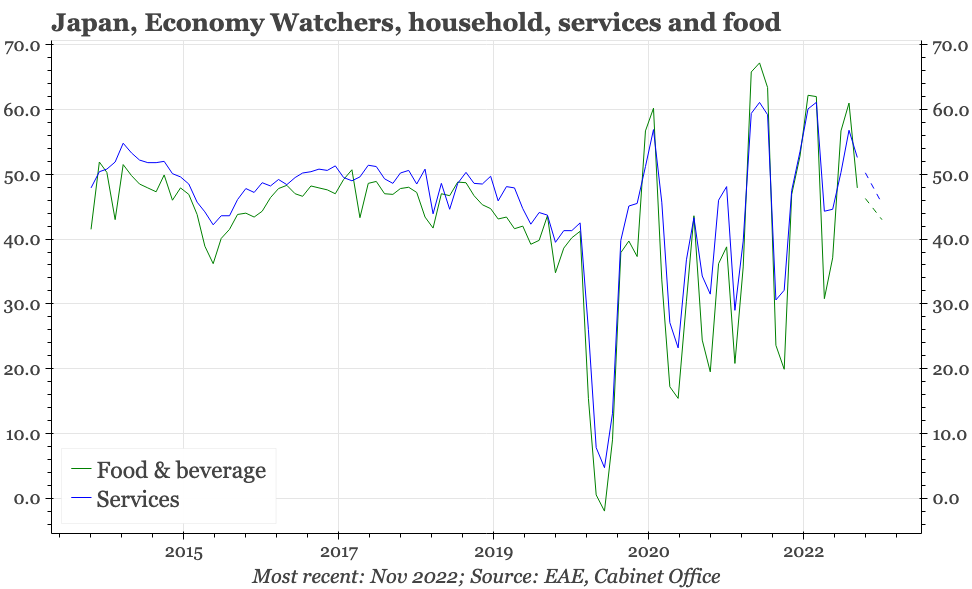

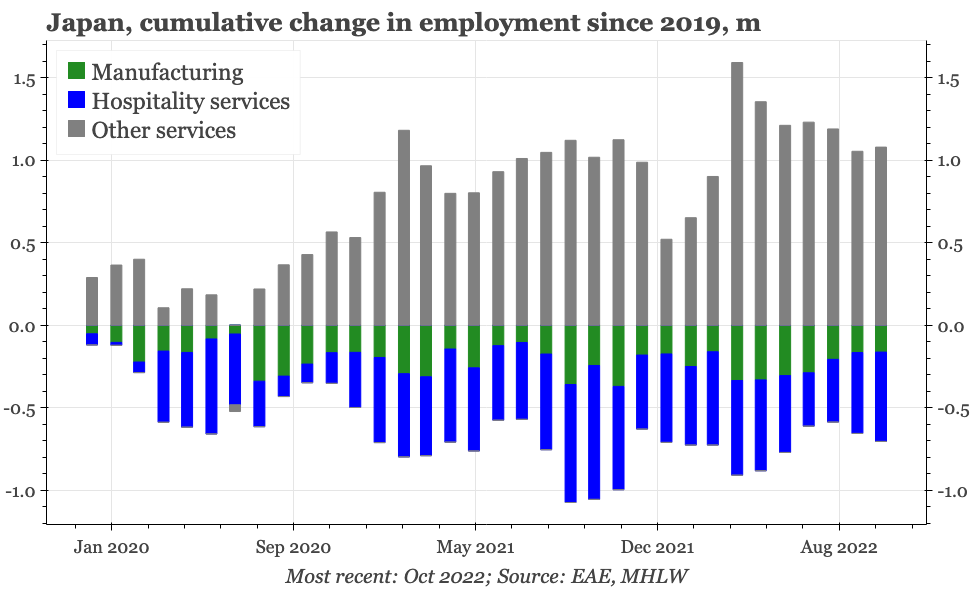

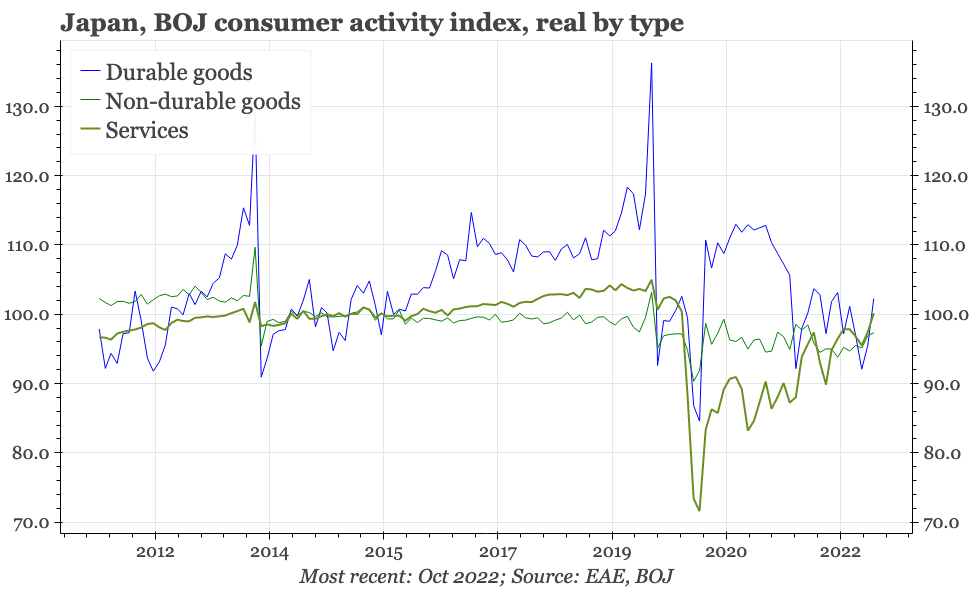

In theory, the seeds of wage-price reflation should be able to grow and bear fruit. Covid border restrictions have only just been relaxed, which should allow an overdue bounce in employment in the hospitality sector, and thus contribute to a further tightening of the labour market. It was encouraging that the BOJ's estimates of consumption in November showed a further rise in spending on services to the highest level since the pandemic began.

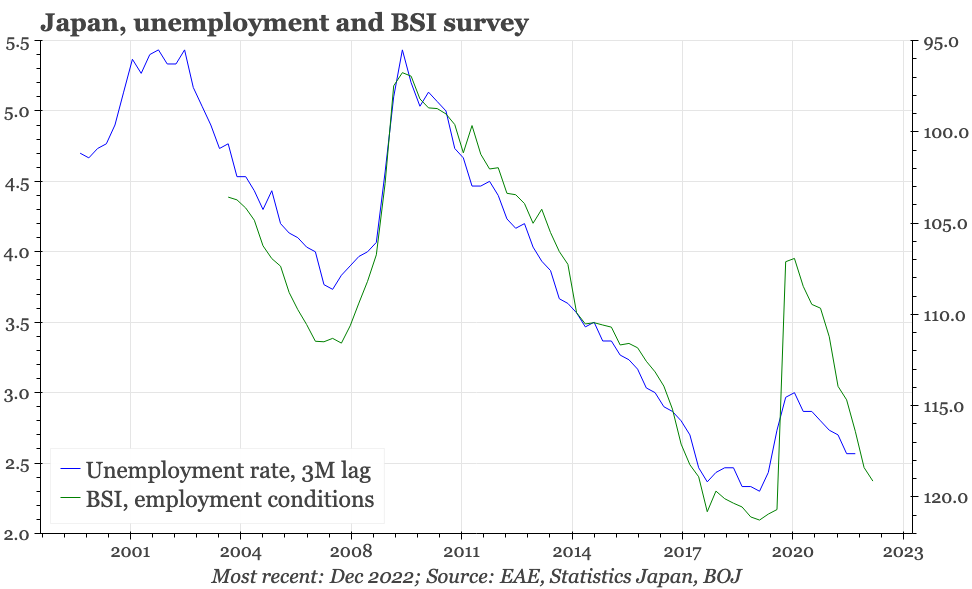

However, while there is some room for optimism, if this next stage in recovery is indeed in play, then companies should be starting to see it happening. And yet, in the Economy Watchers survey, confidence in the hospitality sector eased back in November. Moreover, while companies responding to today's MOF survey did say they expect the labour market to tighten further, they didn't report that the demand-supply balance would reach the levels seen before the pandemic. That would suggest the labour market will be tight, but not to the extent that wage growth is likely to accelerate a lot more.