Subscribers Only

Japan – the hawkish case

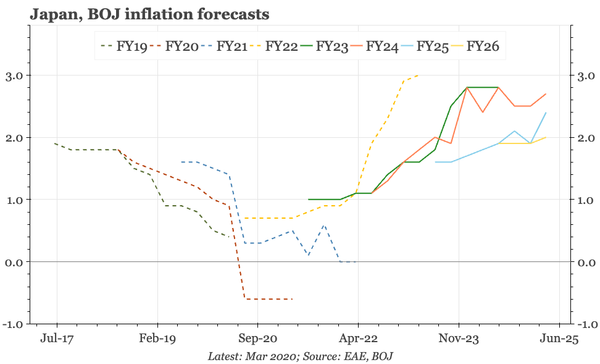

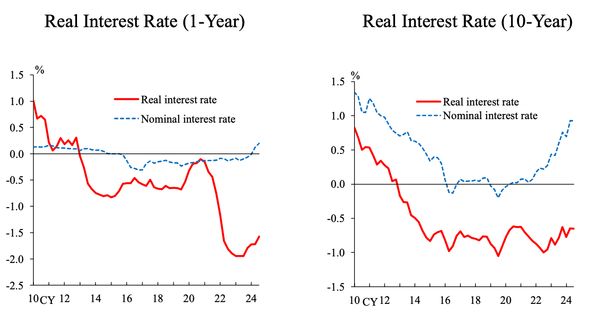

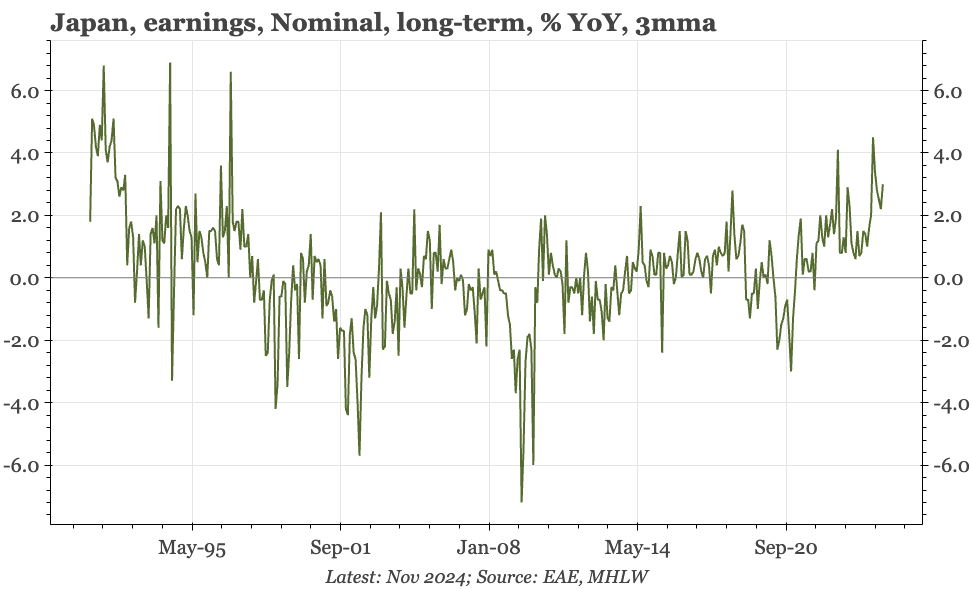

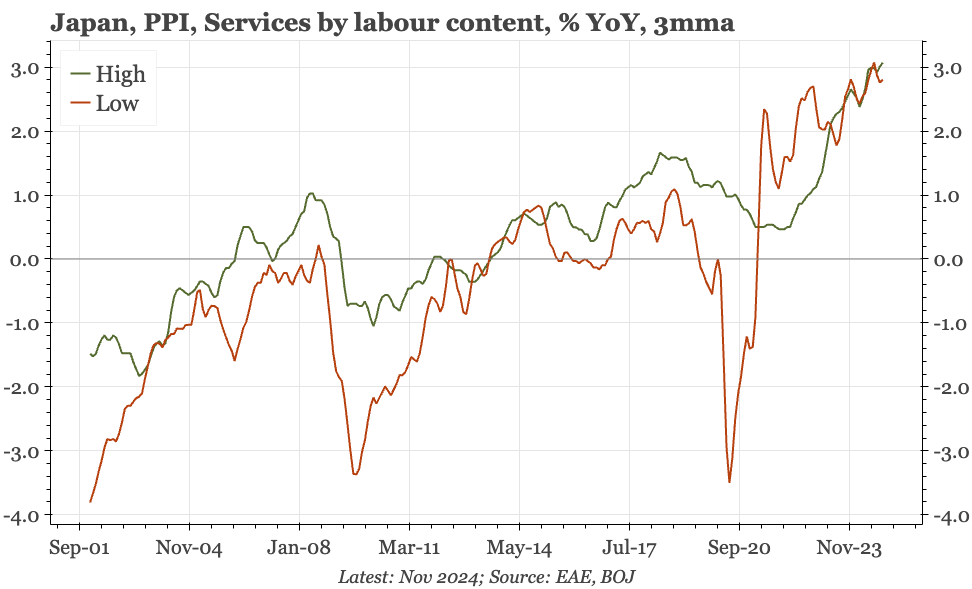

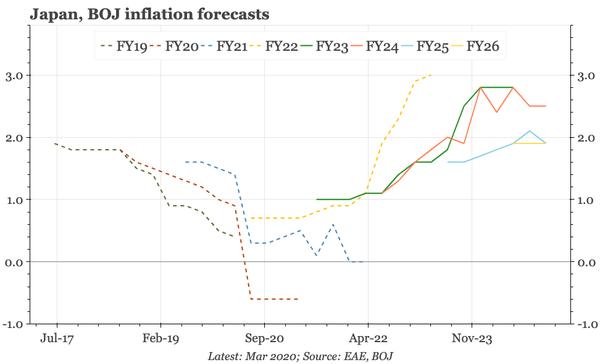

Naoki Tamura is a relative hawk at the BOJ. While that doesn't make him mainstream, his speech today is still worth reading, because it is direct and well-reasoned, and because an upside surprise in inflation and rates is a very reasonable scenario for 2025.