Subscribers Only

Region – BOJ and CBC

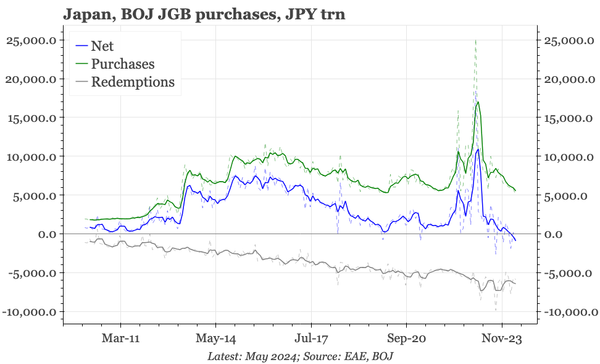

Given the confidence the bank has been expressing, the BOJ meeting this week was disappointing. By raising the RRR, Taiwan's CBC, by contrast, was somewhat hawkish.