Subscribers Only

Japan – confident but not dogmatic

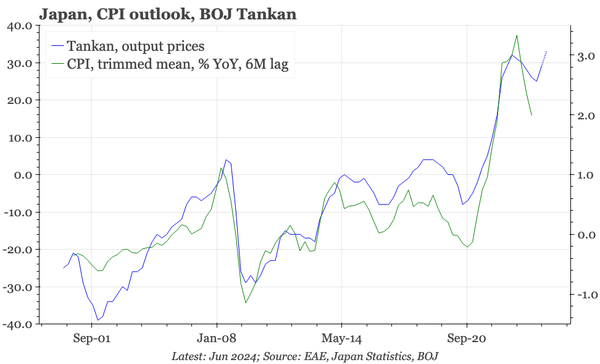

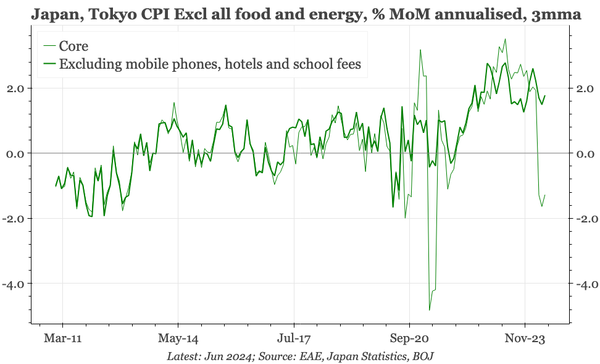

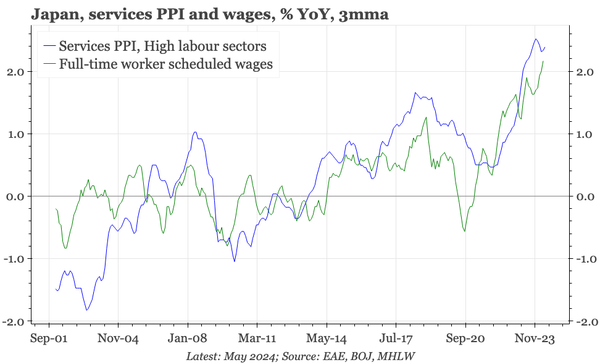

In the BOJ's first comments since last week, Uchida says that policy is dependent on the economic outlook, which could be affected by market moves, particularly the JPY. However, he also reiterates confidence in the underlying changes that the BOJ has been talking about throughout this year.