Subscribers Only

Japan – Ueda stresses inflation risks

Some highlights from governor's speech today: his remarks about strong bank lending, higher prices being a bigger burden to firms than rising rates, the link between low policy rates and the rise in market yields, and the upside risks to prices now that the "deflationary mindset has been dispelled".

Subscribers Only

Japan – offsets to Iran

Tuition as well as energy subsidies make inflation look particularly low relative to the likely upside from the Iran war. The conflict will also slow growth. However, both export data for April and Koeda's speech yesterday indicate that growth downside will be limited if global tech demand sustains.

Subscribers Only

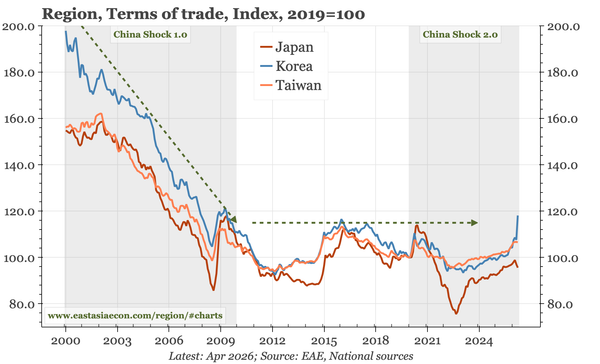

Region – import prices up, export prices up more

Data today for Japan and Korea show the inflationary impact of the War, with import prices in both economies rising at double-digit rates. However, such rises have been seen before. By contrast, export price inflation is setting records, offsetting the hit from energy prices to domestic growth.

Subscribers Only

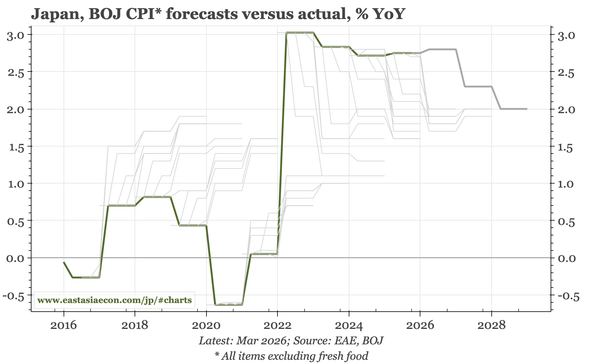

Japan – upside risks to inflation

With the Iran War meaning both uncertainty and a negative terms of trade shock, the BOJ can justify some caution in moving rates. But the bank's detailed analysis last week was heavy on upside risks to inflation. Not addressing that means underlying upwards pressure on $JPY likely persists.

Subscribers Only

Japan – can the BOJ afford to wait?

The BOJ seems to be messaging that it will stay on hold next week. That seems risky to me, given that while the Iran War might dent growth, it is highly likely to raise inflation. A BOJ that is further perceived as too slow will put pressure on the $JPY to pass through the artificial barrier of 160.

Subscribers Only

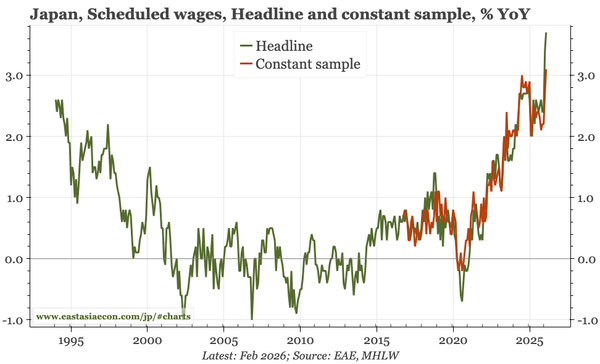

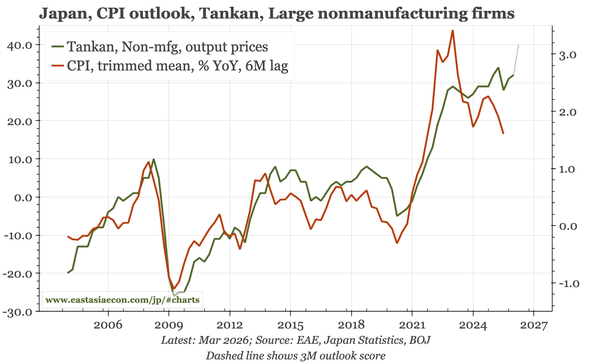

Japan – output prices rise more than input

The inflation risks evident in the Tankan can be blamed on energy prices, but output prices actually rose more than input, suggesting that firms think they can pass costs through. That's important, when the BOJ has been warning that changes in firm behaviour mean upside risks to inflation.

Subscribers Only

Japan – more signs of higher inflation

Today's summary release of the BOJ Tankan shows output prices rising, inflation expectations up, and the labour market tight. At the same time, business sentiment – at least for now – remains solid. Upside risks to inflation are growing again.

Subscribers Only

Japan – more hints of upside risks to inflation

More interesting than today's data releases were yesterday's BOJ documents, on trends in underlying inflation, and the summary of opinions of the March MPB meeting. The BOJ is concerned about the negative TOT shock from the Middle East, but sounds more worried about upside risks to inflation.

Subscribers Only

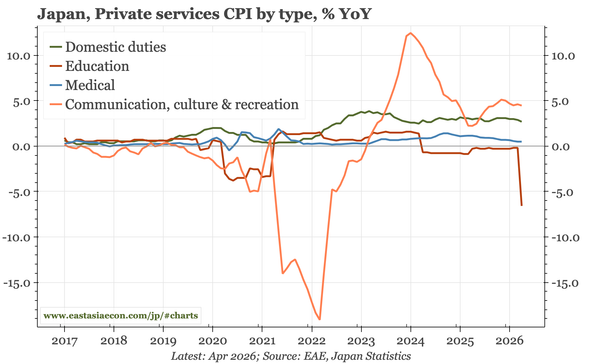

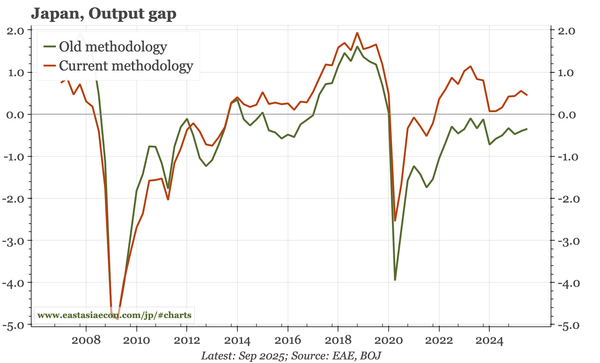

Japan – underlying dynamics still solid

Headline inflation data continue to be affected by policy measures to control energy and public services prices. The underlying picture is more stable, with core private services inflation of around 2%, PT wage growth of 5%, and PMIs above 50. The big risk, of course, is the impact of the Iran war.