Japan – the BOJ focuses on tariffs and food prices

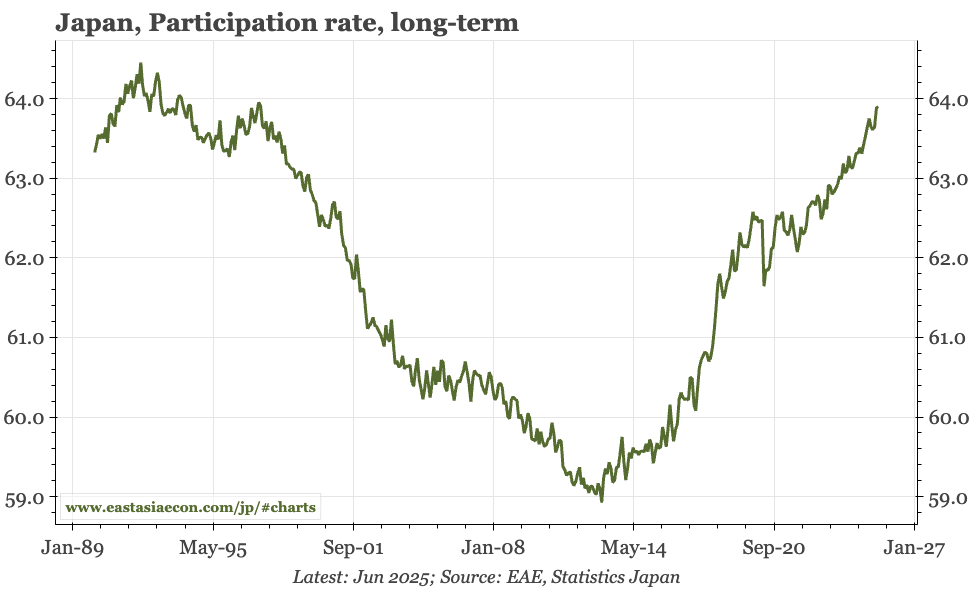

Unusually, the BOJ's quarterly outlook report doesn't focus on wages and inflation. Instead, it looks at this year's two shocks – tariffs, and food prices. The bank argues that the rise in the part rate, seen again in today's June labour market data, has helped offset the impact of food prices.

Today's full quarterly outlook report from the BOJ was the first one in quite a while that didn't include focus on underlying price and wage developments. This isn't because the BOJ is suffering a sudden loss of faith in its own process. Summarising the outlook, the bank expects

underlying CPI inflation is expected to increase gradually, since it is projected that a sense of labor shortage will grow as the economic growth rate rises, and that medium- to long-term inflation expectations will rise.

In the body of the report, the BOJ continued to refer to changes in firms' wage- and price-setting behaviour.

However, right now, there are more pressing issues facing the economy, in particular the twin shocks that have hit Japan this year – tariffs and related uncertainty, and food prices. Rather than wages and general inflation, it was these issues that the BOJ addressed in its special analytical boxes.

Tariffs and uncertainty

In terms of tariffs and uncertainty, the bank's analysis doesn't offer a new lot. So far, the impact has been absorbed by Japanese companies in the form of lower export prices. Even if some of that is temporary, it is likely that corporate profits will fall in 2025 – a decline already seen in corporate capex projections in the July quarterly Tankan. If that is what happens

firms' wage-setting behavior could also be affected, including bonuses and base pay increases; it is therefore necessary to pay close attention to future developments.

The bank then goes on to analyse the impact of uncertainty on corporate capex. It does argue that corporate capex intensions have so far held up, which in the context of the falls in profits that firms are expecting means they

have not changed their active stance on making investment in digital transformation to address labor shortages and in research and development related to growth areas, mainly for projects that are, for example, in their medium-term strategic plans.

However, the bank (reasonably) argues that this might not last, and

As the impact on business fixed investment of heightened uncertainties over trade policies may materialize slowly, it is necessary to carefully examine data and information gathered in interviews with firms.

Food prices

The BOJ then looks at the sharp rise in food prices. A major factor here has been the rise in the rice price, which the bank says is

mainly from excess demand caused by an overlap of a decline in supply due to weather conditions and an increase in demand following the Nankai Trough Earthquake Extra Information....In addition...(1) production costs in agriculture, such as fertilizer and fuel, had been passed on only to a limited extent; and (2) the price of rice had decreased considerably relative to that of bread and noodles.

The bank also notes that import food prices have risen, and that both phenomena have pushed up food prices in the CPI. This feed through reflects

food manufacturers' price-setting stance, which has become more active. Indeed, looking at firms' outlook for general prices in the Tankan, inflation expectations of manufacturers of food and beverages – which had been developing in tandem with those of all industries since the collection of data on inflation expectations began in 2014 – have been rising at a pace clearly above those of other industries since 2022

Two further points are made. First, as food is a frequently purchased item, the rise in prices is likely to have pushed up inflation expectations, adding to more generalised price pressures. Second, the rise in food prices has been enabled by household incomes. That may seem surprising given the fall in monthly real wages. But that is only true on a per capita basis for full-time employees. With part-time wage growth stronger, labour participation rising, and households getting some benefits from the government, aggregate real incomes for households have been rising.

Today's data – employment, PMI and construction

The BOJ does expect the rise in participation to lose momentum, but while today's labour market data for June show again that there has been a slowdown in the number of older people entering the workforce, for women the trend increase remains in place. Employment did dip in June, but only slightly, and so is still close to the record peak of May. The offers:applicants ratio is warning of a mild rise in the unemployment rate, but that hasn't happened yet.

Early anecdotal evidence doesn't suggest much change in labour market conditions in July. The headline in today's manufacturing PMI did fall from 50.1 to 48.9, but

Japanese manufacturers continued to add to their workforce numbers in July. While some firms mentioned hiring additional staff to fill vacancies, others indicated that they had increased headcounts amid forecasts of stronger customer demand in the months ahead.

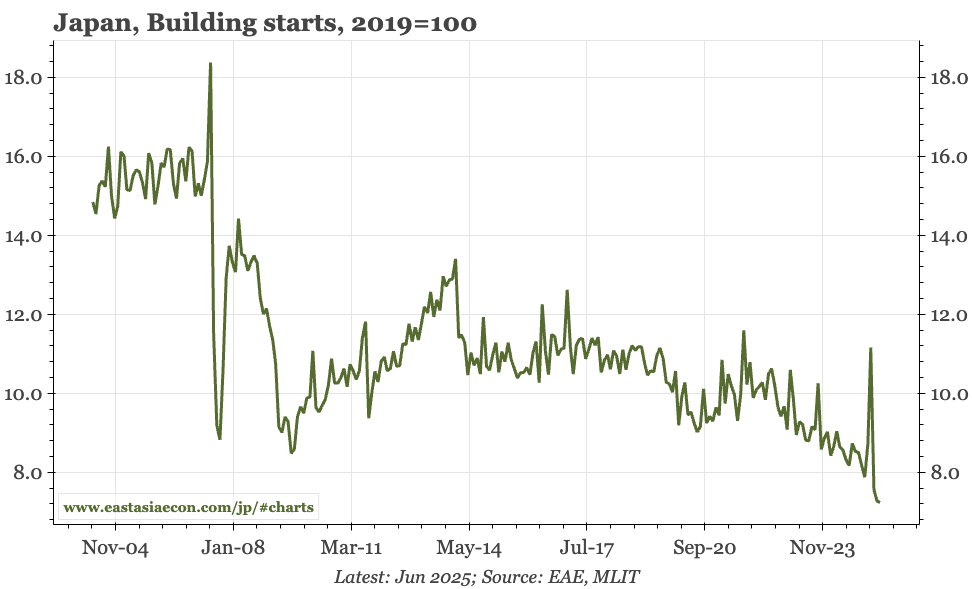

In other data, the regulatory-driven surge in building starts in April continued to unwind.