Korea - CPI

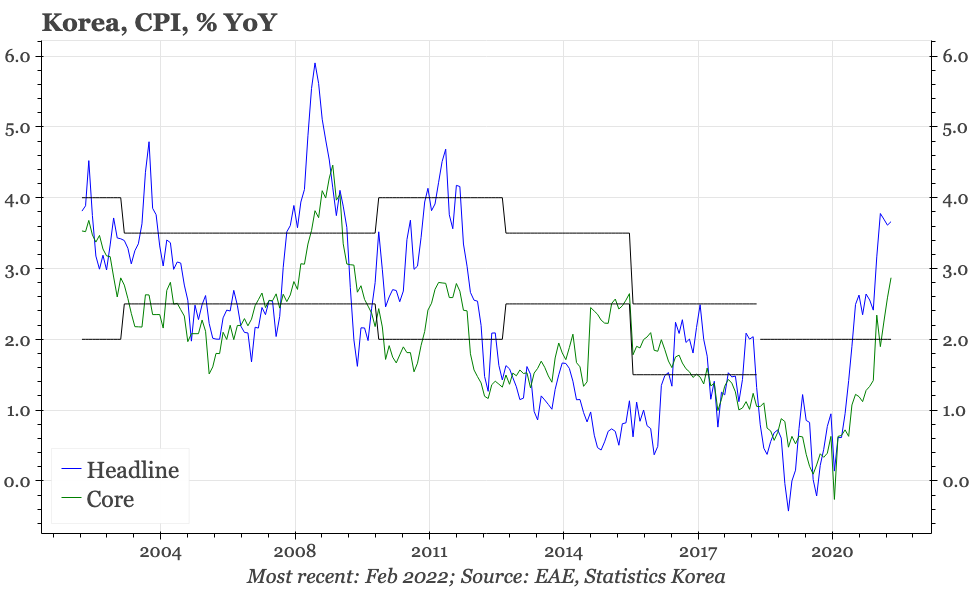

There's no sign yet that headline inflation is about to fall. As for core, without renewed cuts in public services prices, it is likely to prove stickier to the upside than in the period preceding the covid pandemic.

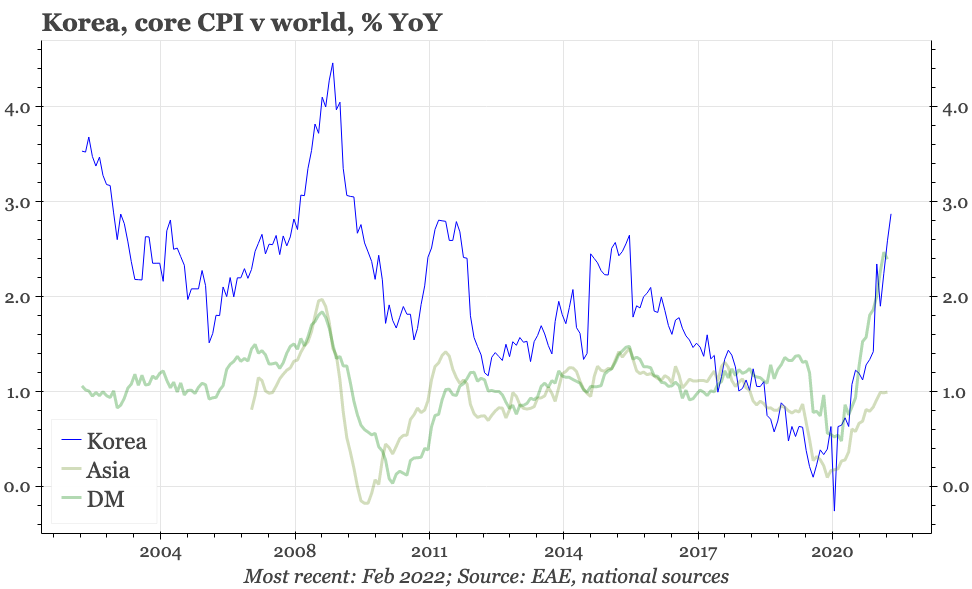

Korean headline inflation was more or less unchanged in February. Core inflation though accelerated again, reaching 2.9% YoY, comfortably above the BOK's 2% target for overall inflation, and the highest rate since 2009.

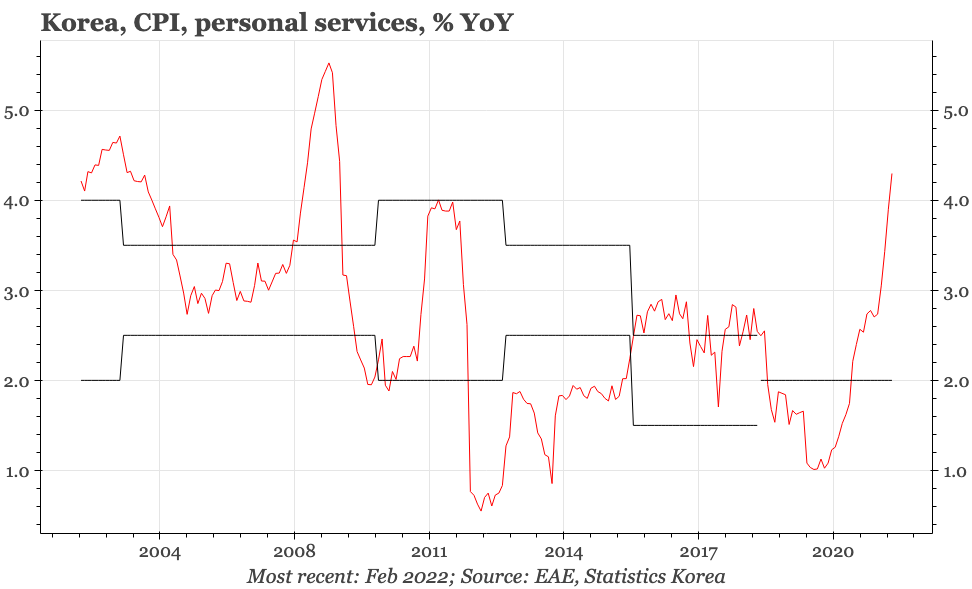

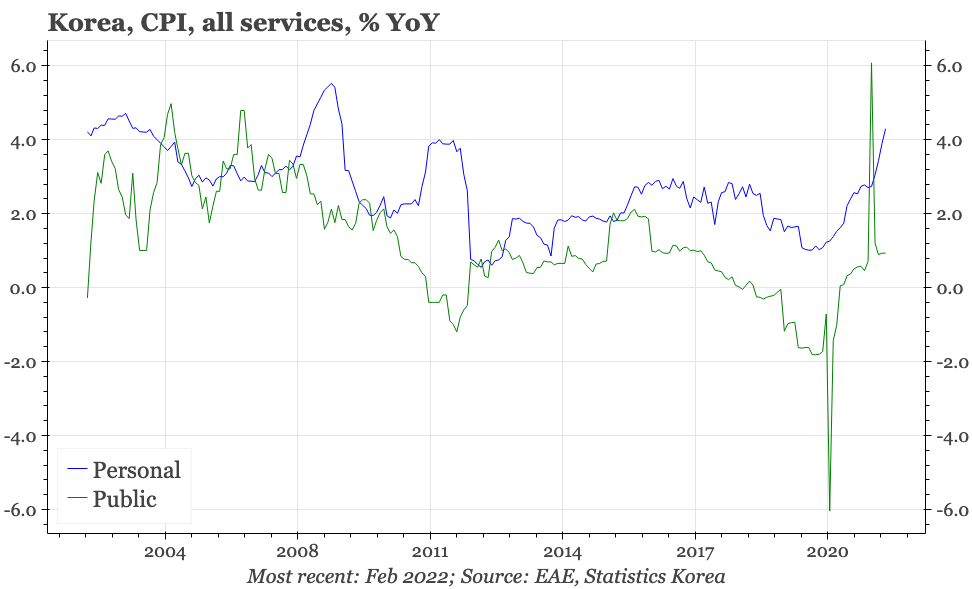

Apart from the high rate that is now being recorded, the move up in core inflation is notable for a couple of reasons. First, the acceleration in core has been much sharper than the pick-up in headline. Second, a big driver of the rise in CPI excluding food and energy in Korea has been a surge in private services price inflation.

The rise in this component of CPI reflects a short-term factor, namely a lessening of the negative impact of covid on domestic services businesses. But it is probably also due to a longer-term dynamic. In recent years government subsidies that had pushed public service inflation below zero also dampened private services prices. The impact of that subsidy programme is now reversing, with public services prices rising 0.9% YoY in February, allowing private services inflation to normalise.

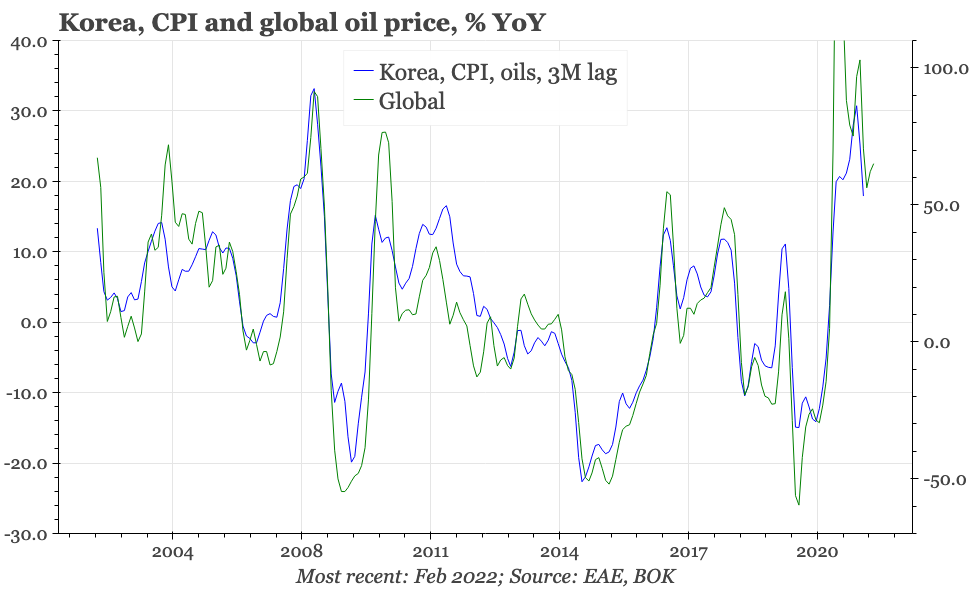

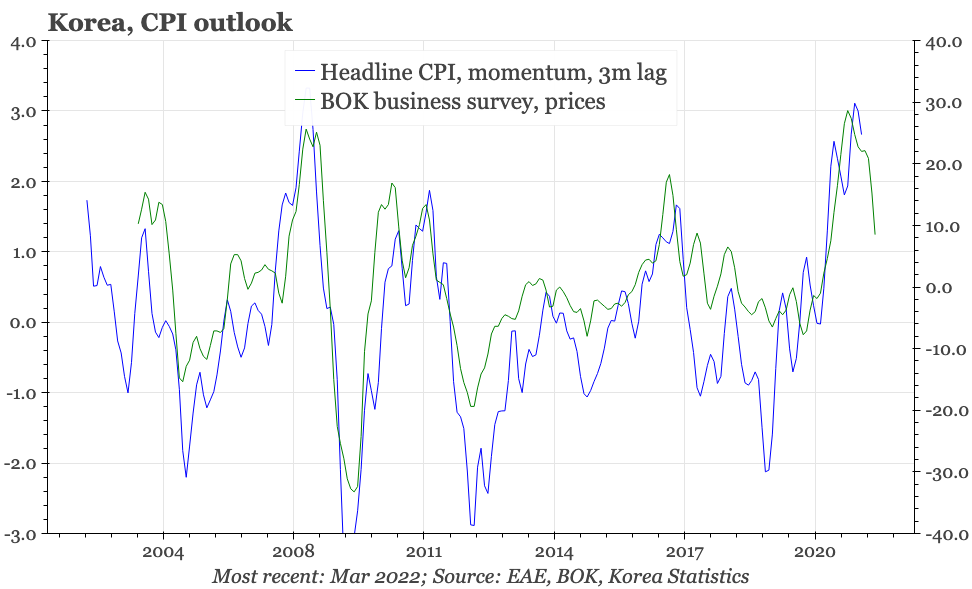

Even with the recent step-up in the global oil price, leading indicators for headline CPI in Korea suggest a lessening of upwards momentum in inflation over the next few months. But there's no sign yet that headline inflation is about to fall. As for core, without renewed cuts in public services prices, it is likely to prove stickier to the upside than in the period preceding the covid pandemic.