Korea – core CPI still high

Core inflation remains elevated, but the BOK is signalling it is near done with hiking. That's because of the deterioration in activity. That slowing of growth is sharp enough to make cutting a possibility, though the BOK likely needs to first see a fall in employment.

November CPI

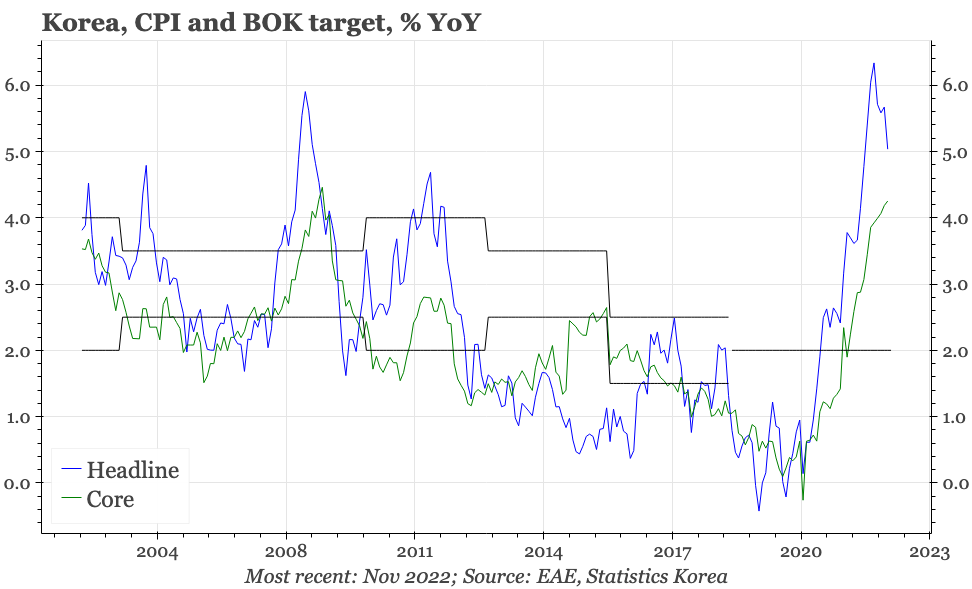

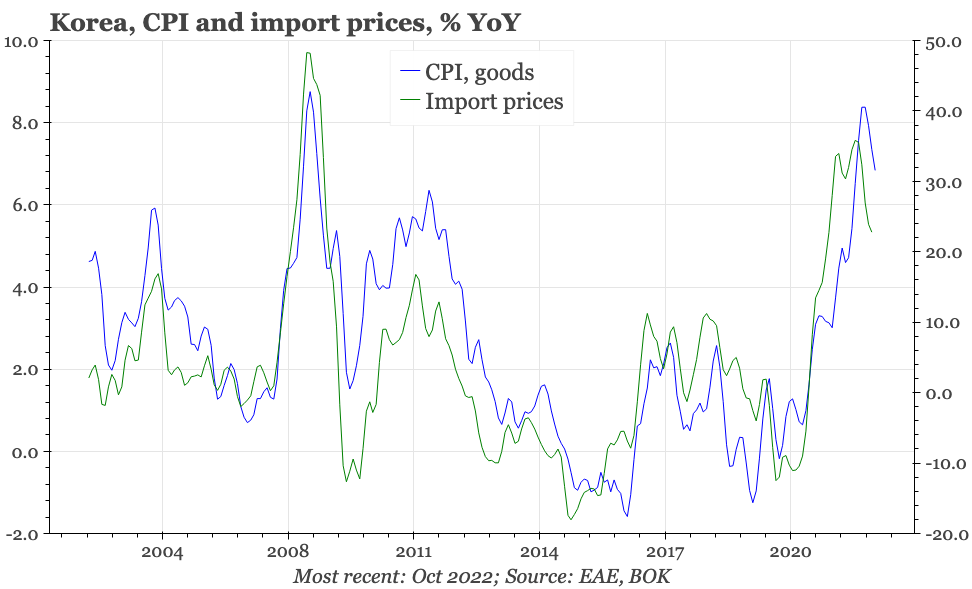

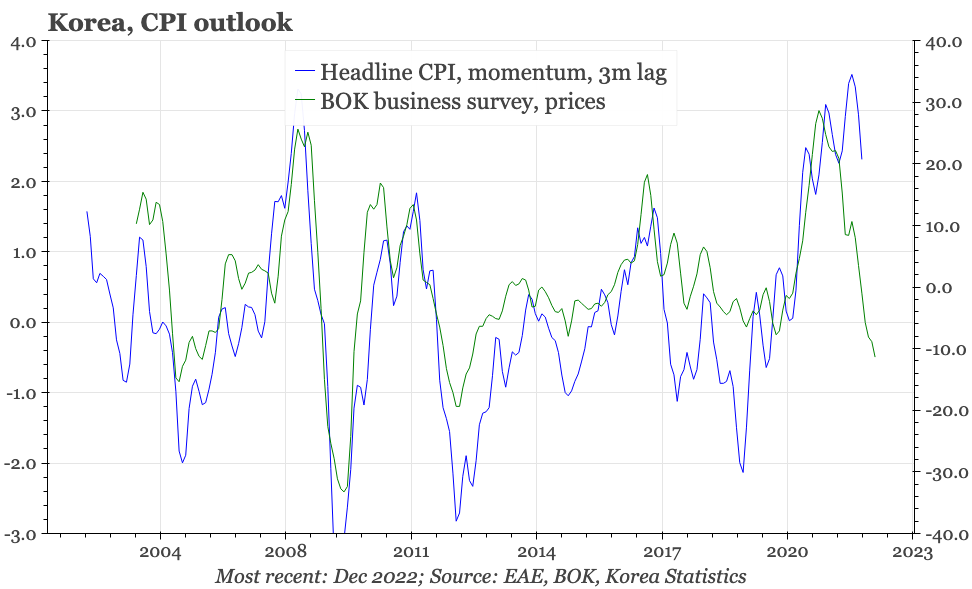

Overall CPI inflation in Korea fell back to 5% in November. That is still a long way above the BOK's 2% target, but is at least down from the peak of 6.3% in July. Moreover, leading indicators suggest the decline should continue.

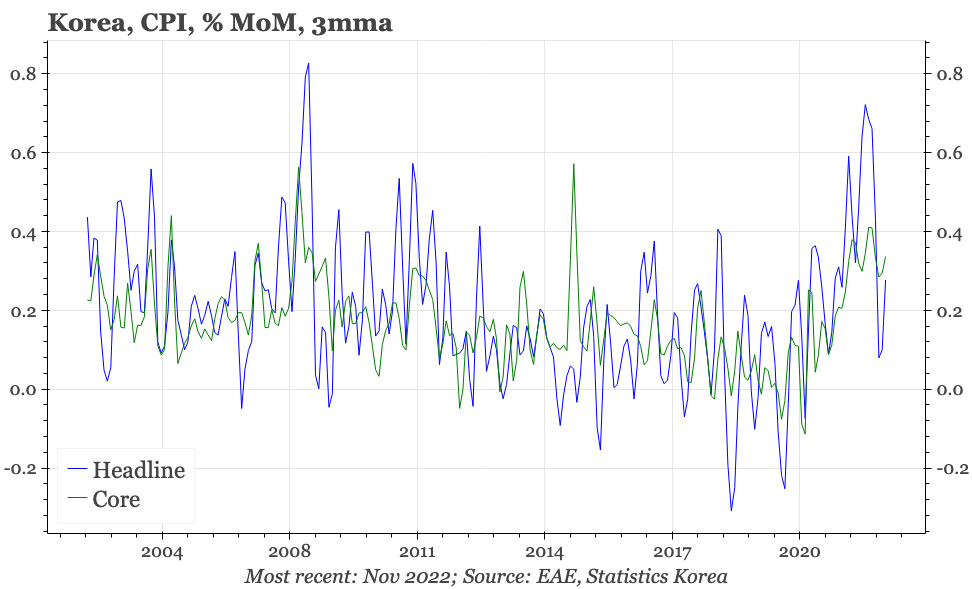

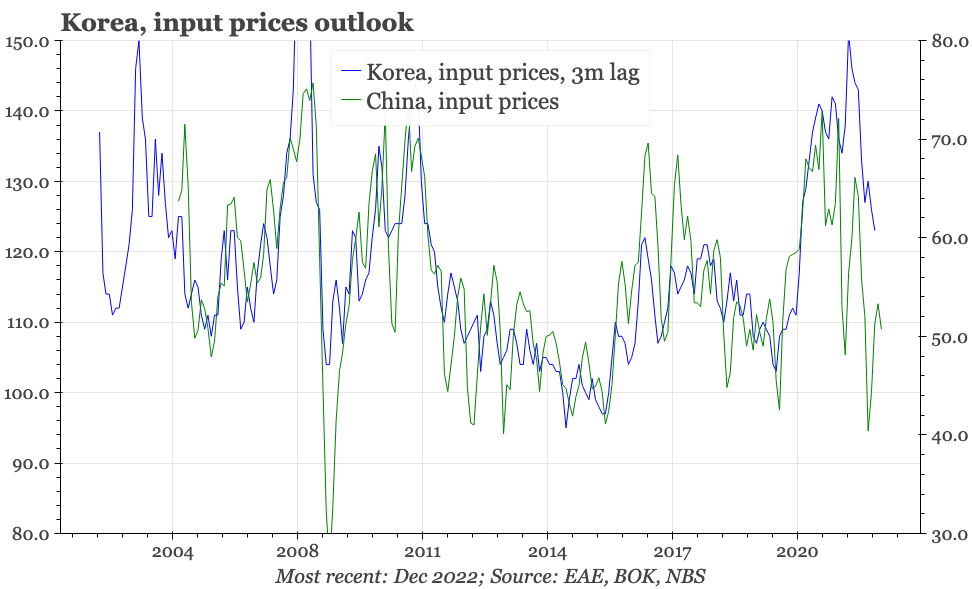

Core inflation, however, continued to rise, increasing slightly to 4.3% YoY in November, a new post-2008 high. That was partly base effect, but on a MoM basis, core CPI also remains elevated, continuing to run at the 4-ish% annualised rate first reached in late 2021. Again, that is much higher than the BOK's target, and also significantly above the 1.5% average of 2012-19.

Inflation though isn't the only concern for the BOK. It also needs to think about economic growth, and that now looks to be slowing sharply – exports are contracting, business sentiment is dropping, consumer sentiment is weak, and the property market looks to have cracked.

As a result, and even though inflation is remaining elevated, the BOK is signalling it is close to being done with hikes. The last meeting took the base rate to 3.25%, and in the last few days the governor has said that the terminal rate may well end up around 3.5%.

In terms of markets, the opportunity is probably around if and when the BOK ends up cutting. That certainly is possible, given what seems to be happening with the cycle. But it likely first needs a real loosening of the labour market and a continued fall in inflation expectations. Even if those do fall into place, they would take some time to impact core, so any loosening is probably a 2H23 story.