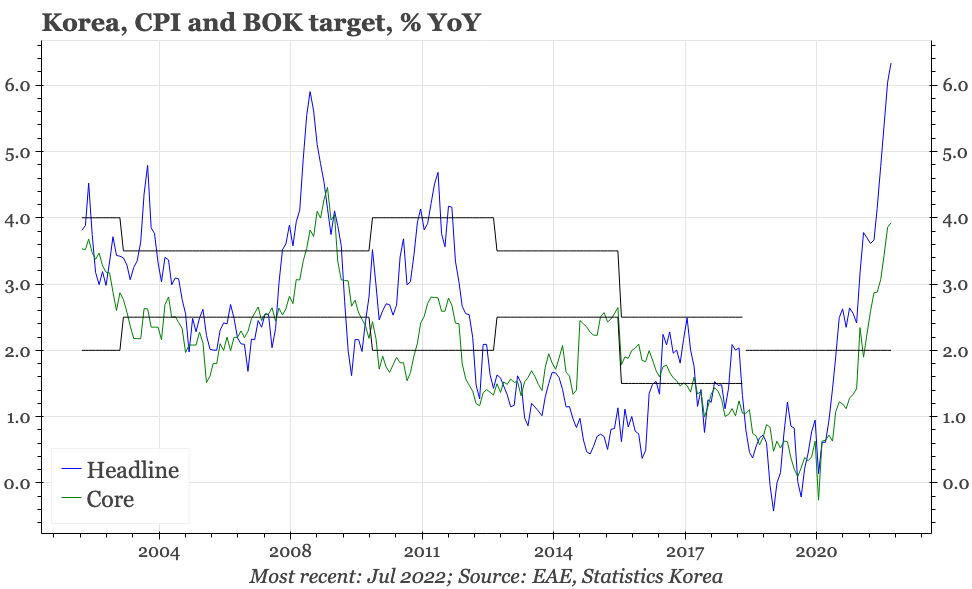

Korea – July CPI

Korean inflation is probably close to peaking as the rise in goods prices starts to decelerate. But services price inflation remains firm, and while that continues, there isn't much room for the central bank to be able to relax.

The BOK seems minded to go a bit more slowly with tightening from here, with the BOK governor saying 0.25ppts hikes would be appropriate if inflation develops as the bank expects. On the surface, today's CPI data offer some justification for that, with headline YoY inflation rising by 0.3ppts, only about half the acceleration of the previous few months.

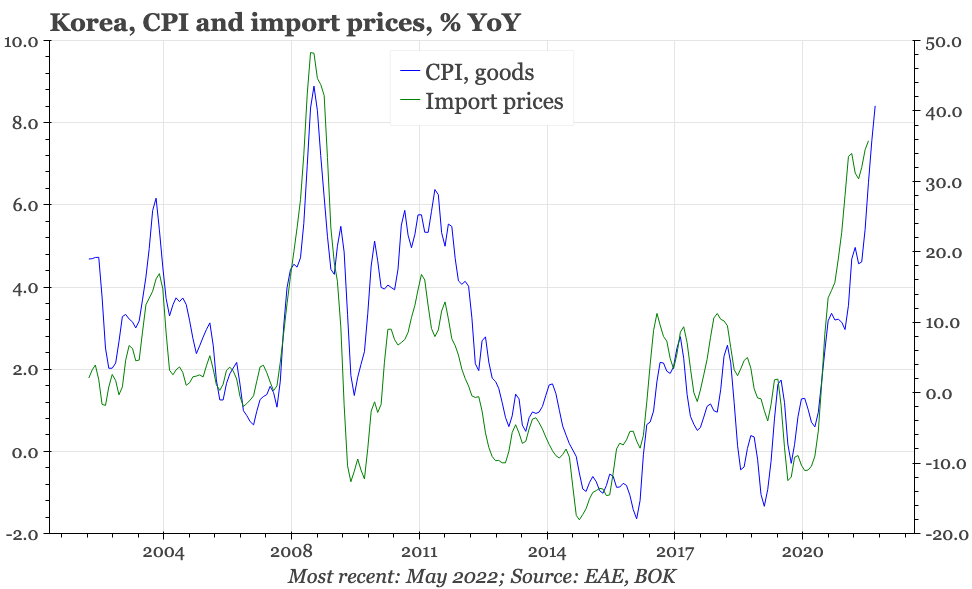

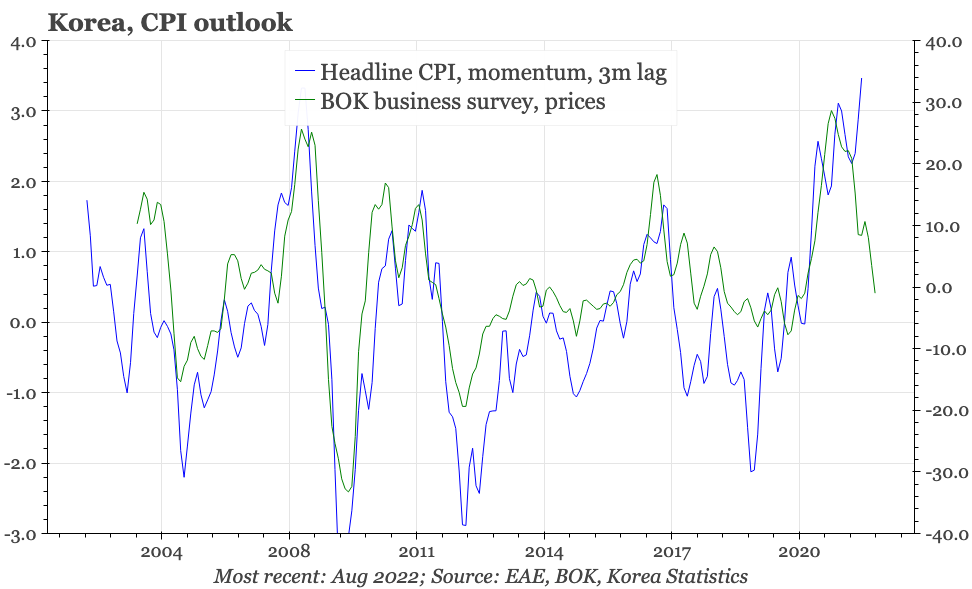

Usual leads would suggest headline inflation doesn't rise further from here. Indeed, there are some signs that goods price inflation will decelerate quite sharply over the next 3M.

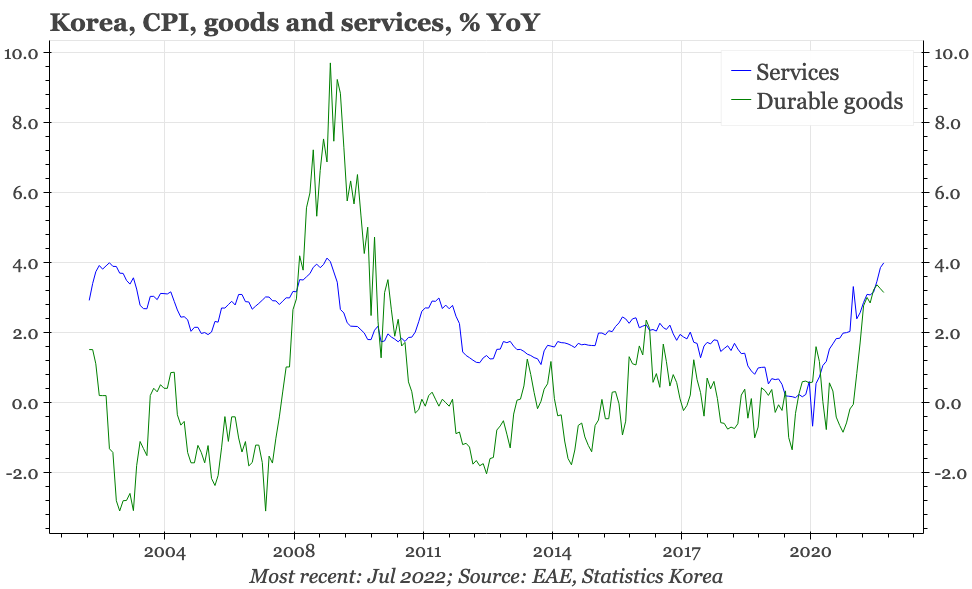

That said, usual leads have been suggesting that overall inflation momentum in Korea should have declined further by now. The disconnect could be that while goods price inflation is starting to decelerate, Korean inflation is now being led by rises in private service prices. While they didn't increase quite so quickly in July as in June, at 0.5% MoM, the pace of change is still not slow.

Service price inflation is unlikely to be powerful enough on its own to push overall inflation up if goods prices continue to weaken. So, the pace of BOK tightening is likely to slow. However, there's not much room for the central bank to relax if services price inflation remains so stubbornly high.