Last week, next week

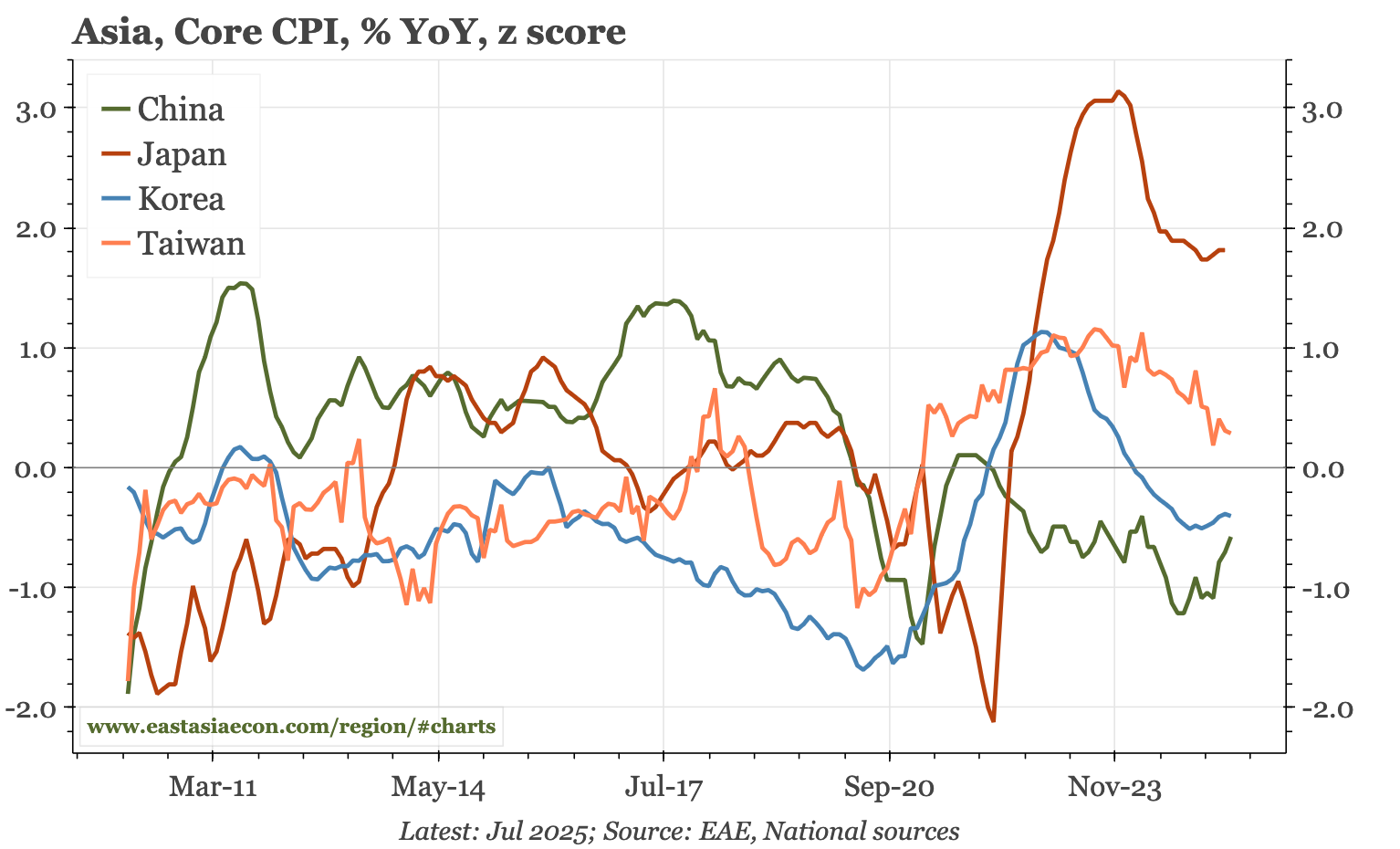

Data themes remain unchanged. As tariffs – perhaps – stabilise, official sentiment is catching up to the data in Japan, with growing concern about inflation. In China and Korea, market sentiment has improved ahead of the data. Given Trump's desire for a deal, that's probably more justified in China.

As we move into the later months of the year, there are some signs of a shift in market themes. In Japan, the change is a more hawkish attitude towards stubbornly high inflation, seen most clearly in last week's summary of opinions of the July MPC, and other official comments. In Korea and China, market sentiment has improved. Taiwan is the one economy where the big dynamic of 1H25 – crazily strong exports – is persisting. However, even here, the details show some modification, with July's data being more about shipments of non-tech to ASEAN, whereas in the 1H it was all about exports of semi to the US.

The shift in Japan has happened in part because of less uncertainty about US tariffs. Though to be clear, uncertainty remains, with Japan fretting that the US still hasn't put in place measures that stop the "stacking" of tariffs to levels above the 15% that Trump had reportedly agreed to. That discrepancy is in turn further weakening the position of prime minister Ishiba – given he has yet actually to secure the treatment for Japan that he'd claimed to have won – and so contributing to domestic political uncertainty too. So, the road to further BOJ hikes still isn't without obstacles. But I think there's now a sense that the continued strength of inflation is starting to become the priority.

In Korea and China, there's still not much sign of a turn in economic momentum that would justify the improvement in market sentiment. In China in particular, the weakness of inflation in data at the weekend continue to suggest domestic demand is weak. As a result, for both economies, external demand and thus tariffs matter too. But China right now seems to continue to hold the upper hand in talks with the US. As long as that remains the case – and it can do for a while, if reports are right about Trump's desire for a trade deal with Beijing – then the strengthening of sentiment likely has room to run.

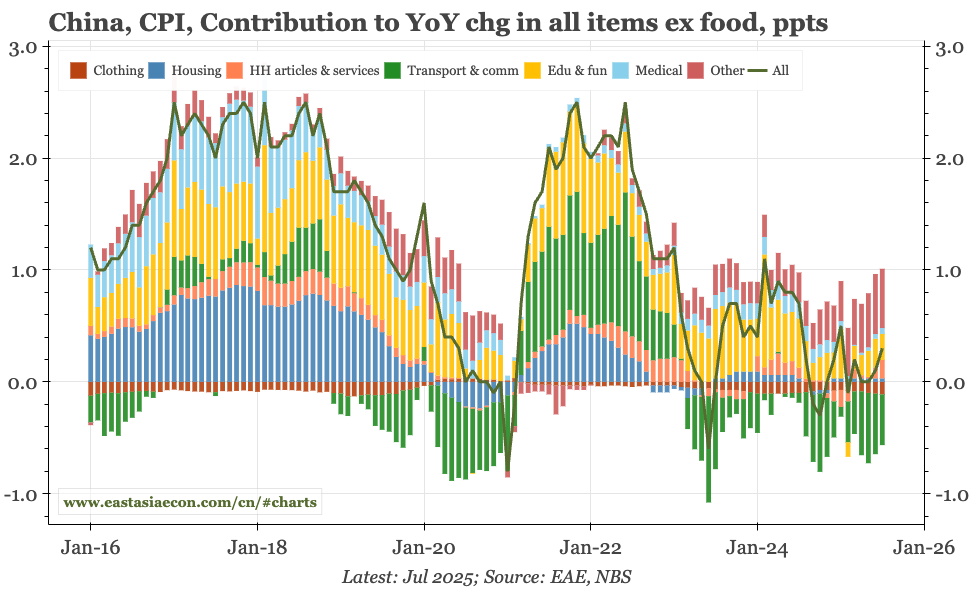

China's cycle will be a focus this week, with the July official data releases on Friday. They will likely show more weakness in retail sales, though the government does now seem to have relaxed the latest crackdown on official dining that contributed to some of the softening of data in June. For Japan, there's Q2 GDP, but more important I think will be Wednesday's PPI. Korea on Wednesday will release labour market for July, and then import prices on Thursday. In Taiwan, the highlight is today's wage data for June.

Thematic

China – the CNY and deflationary equilibrium. Deflation looks like 1990s Japan. But China's exchange rate doesn't. Real CNY depreciation helps exports substitute for the weakness of domestic demand in a way that didn't happen in Japan. It also postpones the sort of stimulus that would ease deflation and provide more direction for markets.

Korea – super-ageing. The BOK recently published a report on the consequences of Korea's "exceptionally rapid" ageing: lower real rates, lower inflation, and weaker financial stability. The report is interesting, but the wide range of reforms suggested shows just how difficult it will be to head off those consequences.

Cycle

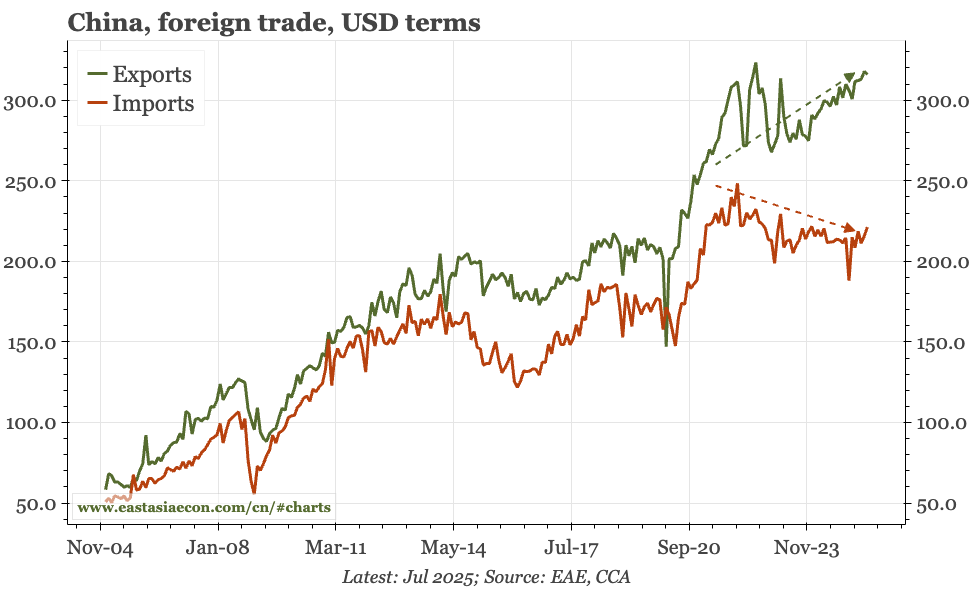

Cycle update – imports perk up. Overall exports still don't show a tariff hit, with shipments to ROW offsetting the weakness of direct sales to the US. Imports are more interesting, with signs emerging of an upturn. That so far is (very) mild, but has been enough to cap the trade surplus, albeit at the high level of USD100bn.

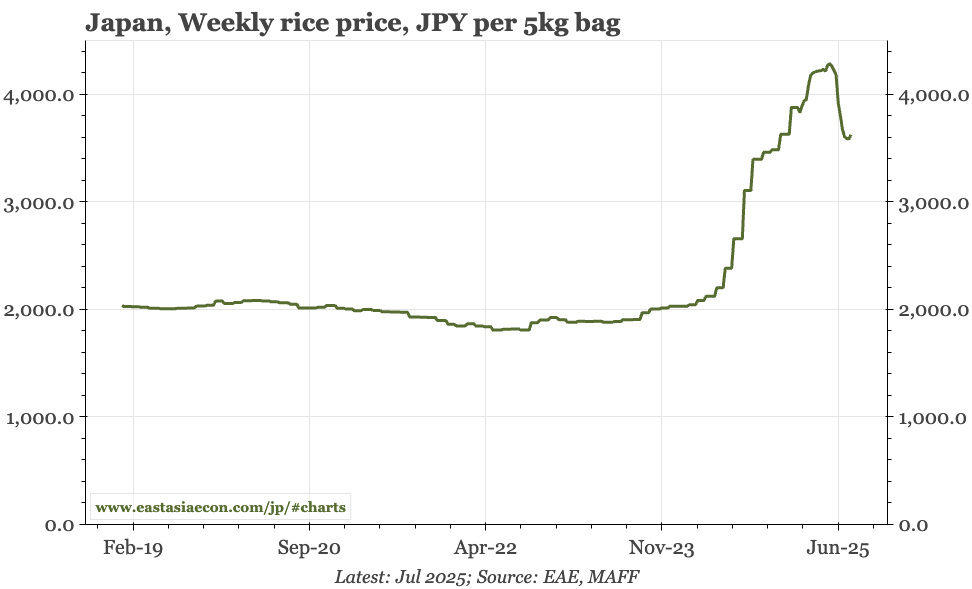

Cycle update – the end of core deflation....or is it? Today's official data show core CPI has rebounded to almost +1%. That would be an important change, but at best it looks narrow, with almost all the rise coming from "miscellaneous goods and services". The leads from PPI and the PMI remain soft. Separately, yesterday's CA data for Q2 were stable.

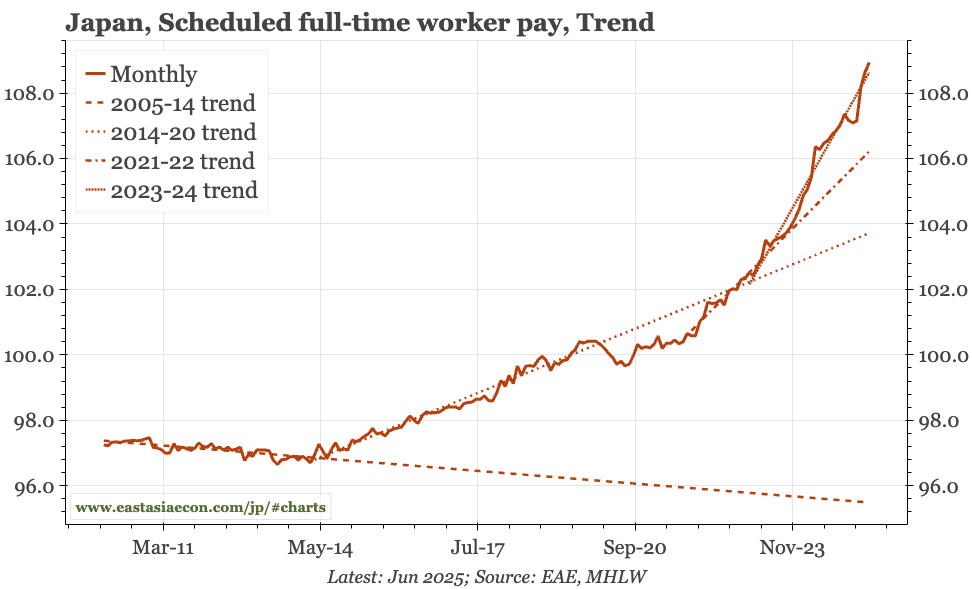

Cycle update – solid wage data. The shunto has boosted full-time regular wages, which increased more quickly in May and June than last year. Part-time hourly wage growth has also picked up again, and will get a further boost from the recently announced hike in the minimum wage. But for now, real overall wages are still falling.

Cycle update – consumption growing at pre-covid trend. The BOJ's consumption proxy ticked up MoM in June. That followed a dip in May, so in Q2 as a whole consumption is only just higher than Q1. Based on the BOJ's data, in level terms, aggregate consumption is still 7% smaller than at the end of Q319. But the growth run-rate is now similar to pre-covid.

Cycle update – inflation concerns grow. Today's EW survey suggests stabilisation of sentiment following the sharp deterioration through Q1. As that happens and high-frequency price measures stop falling, officials, both on the BOJ MPC and in the wider government, are expressing more concern about the continued strength of inflation.

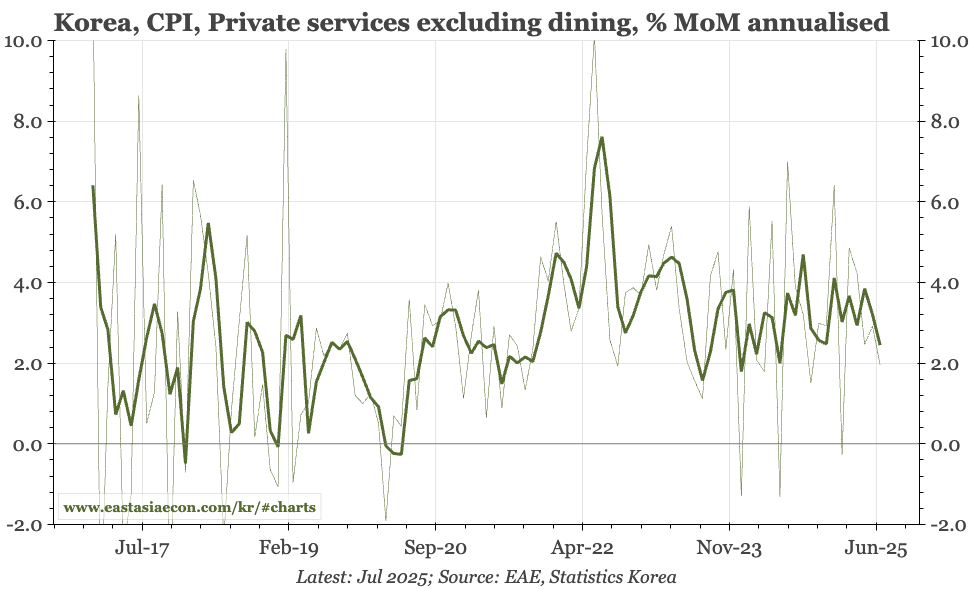

Cycle update – inflation still stable. The BOK hasn't sounded concerned about inflation for a while, and the July CPI data is unlikely to change that, with headline and core remaining close to 2%. Food prices will rise in August following the recent bad weather, but energy prices should fall. Core is also now starting to look softer.

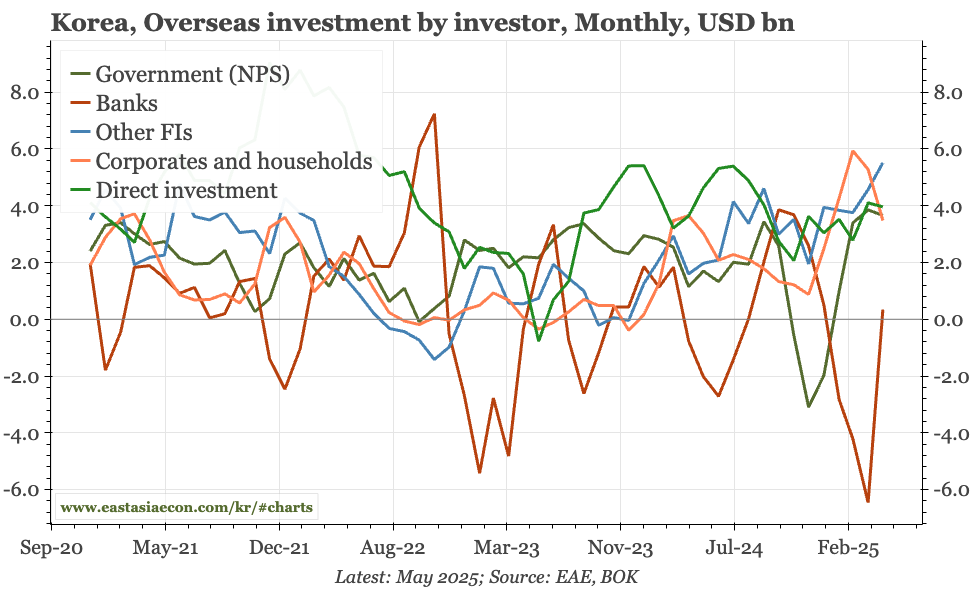

Cycle update – still the NPS outflow, but also foreigner outflows. The main flow dynamics didn't shift in June. The CA surplus remained large, while NPS and FDI outflows were solid. But the revival of domestic equities has caused some changes, with less household overseas buying, and more foreigner domestic buying.

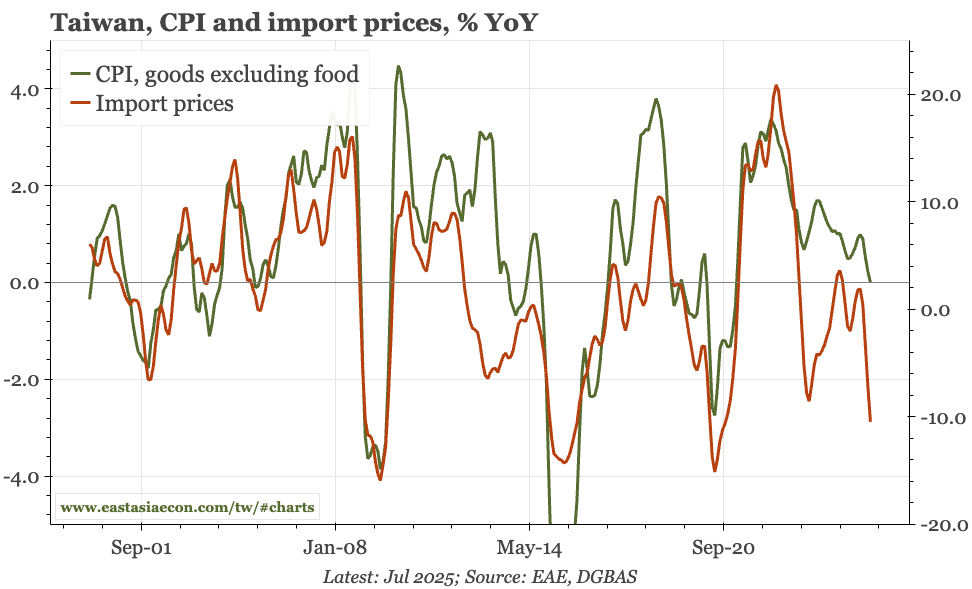

Cycle update – TWD appreciation pushing prices down. The biggest takeaway from today's July price data is the big fall in TWD import prices – and thus PPI and goods in CPI – on the back of currency appreciation. Core actually ticked up in July, and probably isn't going back to the sub-1% rate of pre-covid. But I doubt it gets back above 2% either.

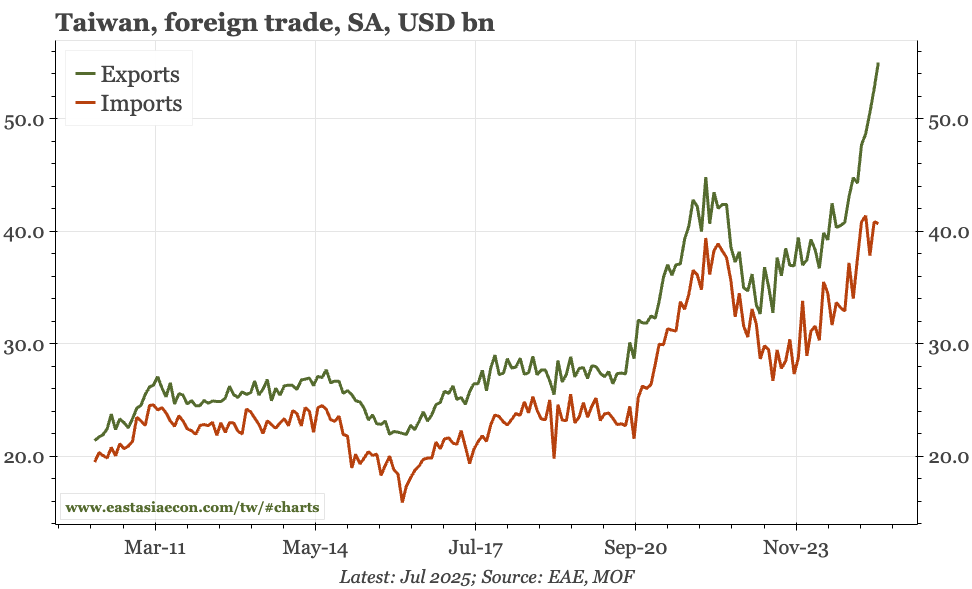

Cycle update – export surge continues. The surge in exports continued in July. Exports have now grown 30% just this year, and the trade surplus has risen to 20% of GDP. But the underlying dynamics shifted last month. Rather than semi exports to the US, the big driver was other exports to ASEAN. That looks more like tariff front-loading.