Last week, next week

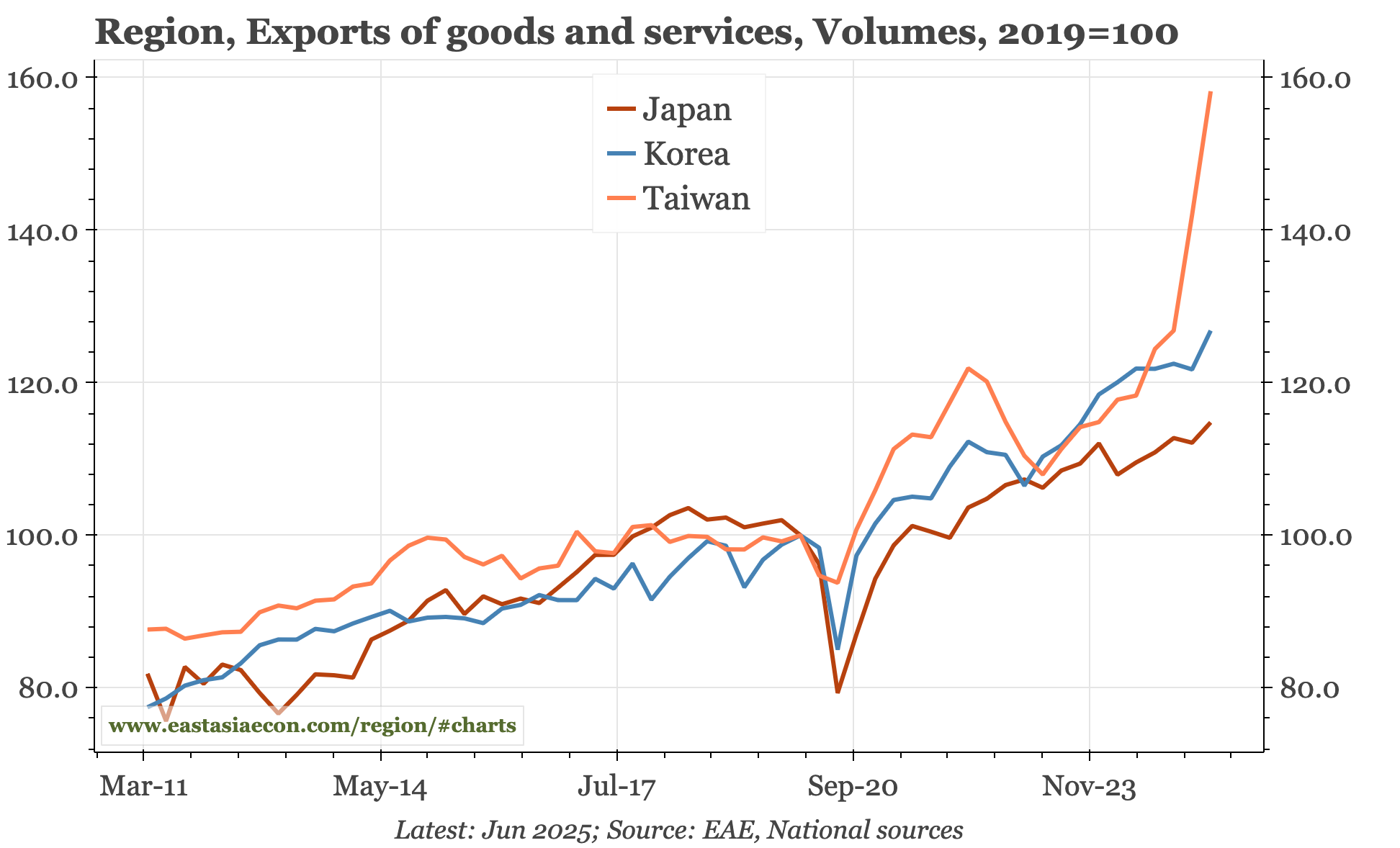

While fundamentals remain weak, onshore China's markets have a tailwind from the H-A premium. In Japan, growth is ok and inflation firm, but the JPY needs more direction from the BOJ. In Taiwan, the export cycle is holding up, which should set the stage for more TWD strength.

- Still no upside in China fundamentals. The cycle, particularly in nominal terms, remains weak. The one bright spot is M1:M2, though that is still in the process of bottoming rather than rebounding. However, China markets are benefiting from the weakness of the USD, showing up in part in the widening of the H-A premium, and I think will gain further confidence from this weekend's Russia-Trump meeting – with that as an example, Beijing will fancy its chances when the US president visits China later this year. The disconnect with fundamentals is something to be aware of, but the market rally can probably run further. It will be important this week if CSI300 finally breaks through the highs of September 2024.

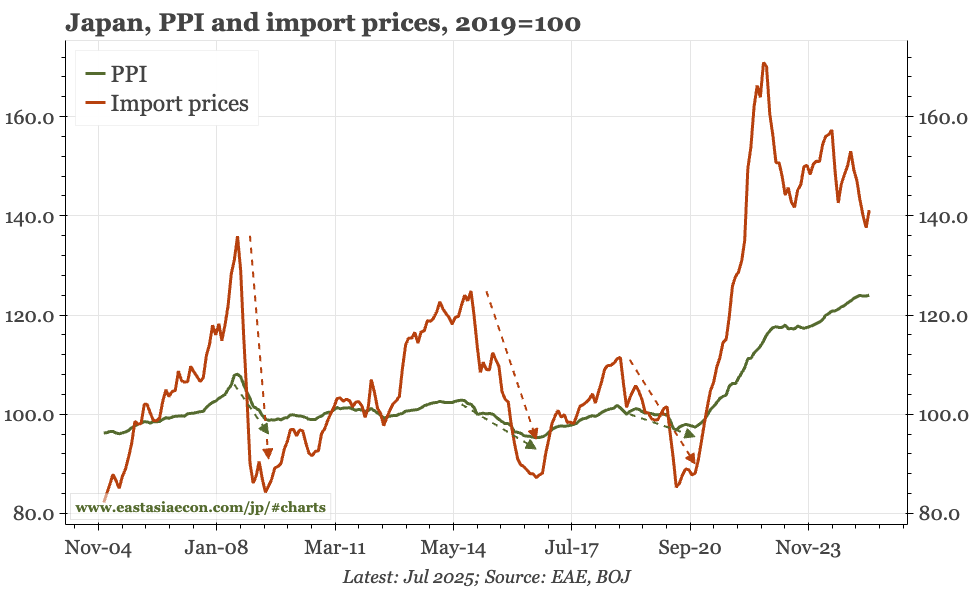

- Japan growth is ok, inflation is firm. The reacceleration in inflation of 1H25 has likely peaked, but that leaves inflation still high, and there isn't either 1) the decline in import prices or JPY strength or 2) the weakening of the labour market that would lead to a real decline in inflation. With policymakers becoming more nervous about the stubbornness of inflation, market confidence should grow that the BOJ will hike further. But for that to impact the JPY, the central bank needs to start expressing a clearer post-tariff view. In the short-term, there aren't opportunities for that to happen.

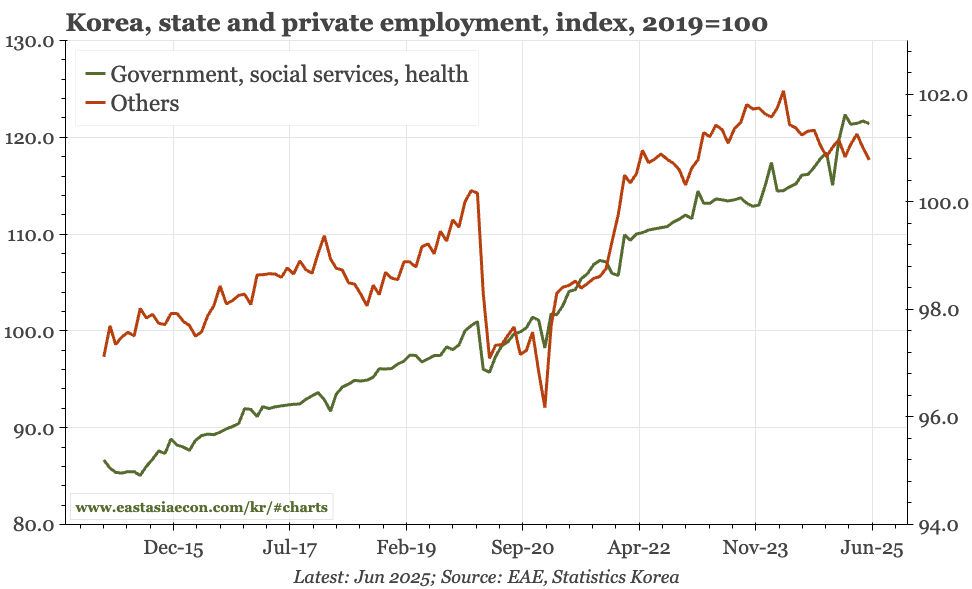

- Korea cycle less worse, but still soft. Lat week's data releases didn't shed more light on Korea's economy. Exports have risen a bit in the last couple of months, but not dramatically, the labour market remains soft, as do import prices. With consumer confidence rebounding, the BOK can feel that the worst is over. But I'd still expect rates to fall further.

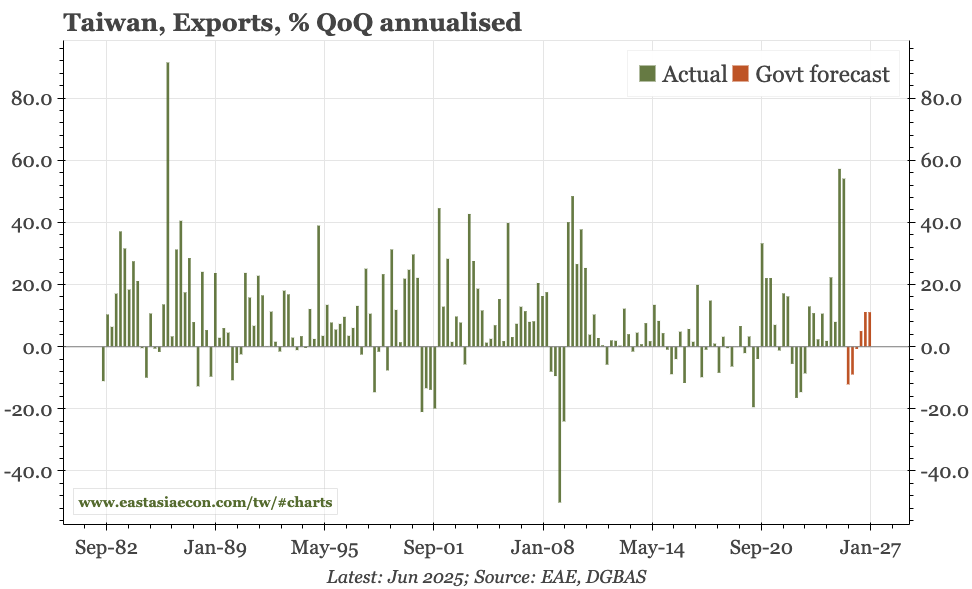

- Taiwan export strength persisting. With the July export data and then last week's official forecasts for 2H25, it is becoming clearer that the remarkably strong export growth of 1H was more AI-demand than front-loading. If the USD weakens again, that should set the stage for more TWD strength. At the same time, with the rise in the currency and the cooling of the housing market dampening inflation, there will be room for the CBC to become more dovish.

This week is quieter for data. The highlight is Japan CPI at the end of the week. In Japan, there's also July trade data, and the August flash PMI. Tomorrow's household credit data for Korea will be noteworthy, though next week's BOK meeting will depend more on higher-frequency indicators of household debt like weekly property prices. China this week releases detailed trade data for July, useful for volumes and unit prices. The main releases for Taiwan are Q2 BOP data and labour market indicators.

Cycle

Cycle update – credit data soft, but M1:M2 ratio stable. The rise in the credit impulse stalled in July, dampened by slower government, non-state and mortgage borrowing. However, the monetary data remain a bit more constructive: while the recovery in M1 growth slowed, the bottoming relative to M2 remains intact.

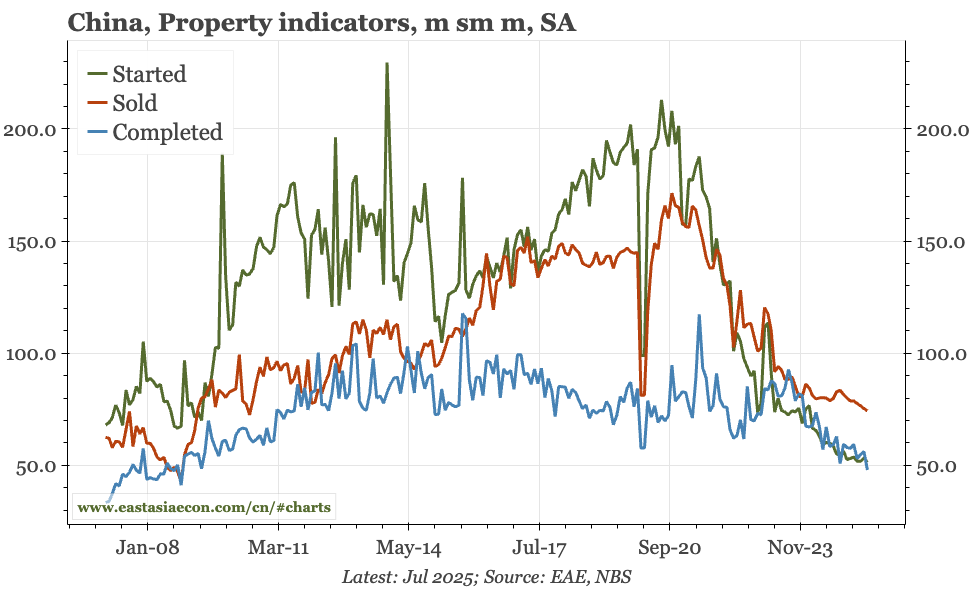

Cycle update – softer again. Property prices and sales, investment and retail sales all deteriorated in July. It is at least possible to argue that the worst of the drop in property activity is now completed. That creates room for second-derivative improvement, but even that could be offset by slowing manufacturing capex.

Cycle update – limited PPI downside without lower import prices. Headline PPI inflation is softening, but a real correction is unlikely without a bigger fall in import prices. In July, import prices ticked up, as did auto export prices, but only slightly. In other data, non-manufacturing sentiment in the August Reuters Tankan remained firm.

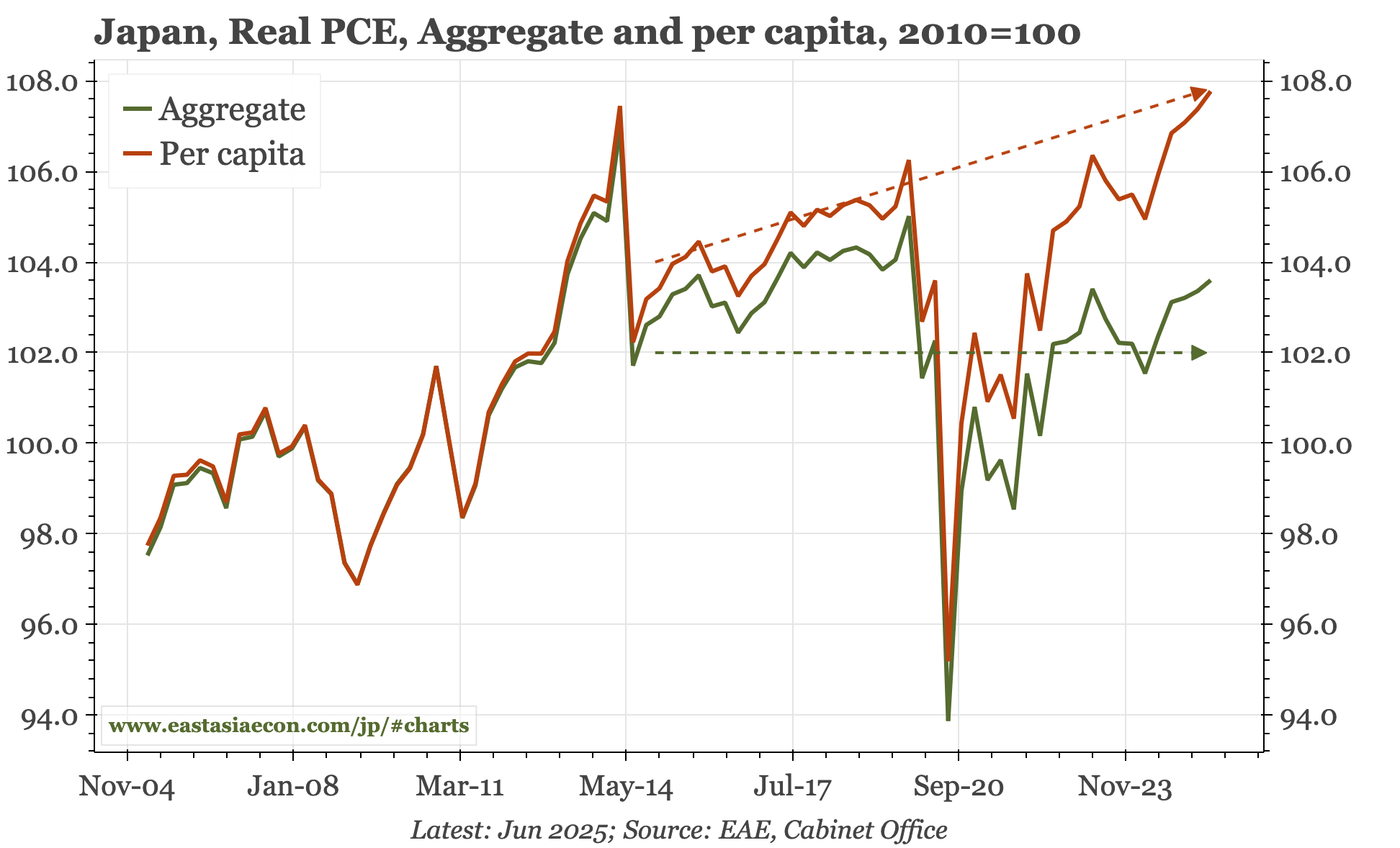

Cycle update – solid GDP. Q2 GDP wasn't particularly impressive at headline level, but the details were firmer, with both consumption and investment rising. The recovery in aggregate consumption does remain sluggish, but that is partly because of population loss. I estimate per capita consumption in Q2 reached a record high.

Cycle update – exports stable in August. After adjusting for workdays, export growth remained solid at around 9% YoY in the first 10 days of August. The growth is all because of semi and ships – exports of other products fell. That perhaps shows an end to front-loading, though exports to the US directly haven't been particularly volatile.

Cycle update – labour market still soft. The rise in optimism that followed the election in early June of a new government isn't yet feeding into a meaningful improvement in labour market data. One of the missing ingredients is that the rise in confidence seen among consumers hasn't yet spread to the corporate sector.

Cycle update – import prices fall, auto export prices fall more. Preliminary data show the recent fall in import prices lost momentum in July, but still point to more downside for CPI goods prices in the next 3M. Overall export prices were flat, but for autos show the same sharp decline seen in Japan. Asian auto firms – so farm – are absorbing much of the tariffs.

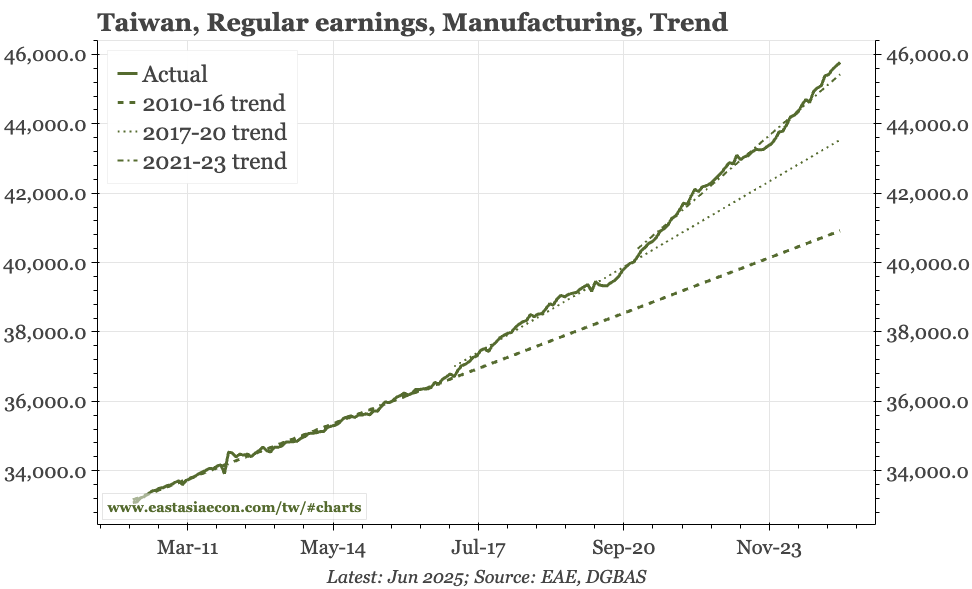

Cycle update – tight labour market, at least in manufacturing. The export surge is boosting demand for labour, with data today showing manufacturing overtime hours in June near the highest in 15 years, and wage growth of close to 4% YoY. Overall wage growth has also trended up, but less quickly, because the demand:supply balance in services isn't as tight.

Cycle update – less worried on exports. The government today confirmed the export surge of 1H – and released much less pessimistic forecasts for 2H. The underlying story is simple: AI-related demand offsetting the impact of TWD appreciation and tariffs. Exports are now expected to grow almost 25% this year, and GDP by 4.5%.