Last week, next week

This is what happened on East Asia Econ this week.

Thematic

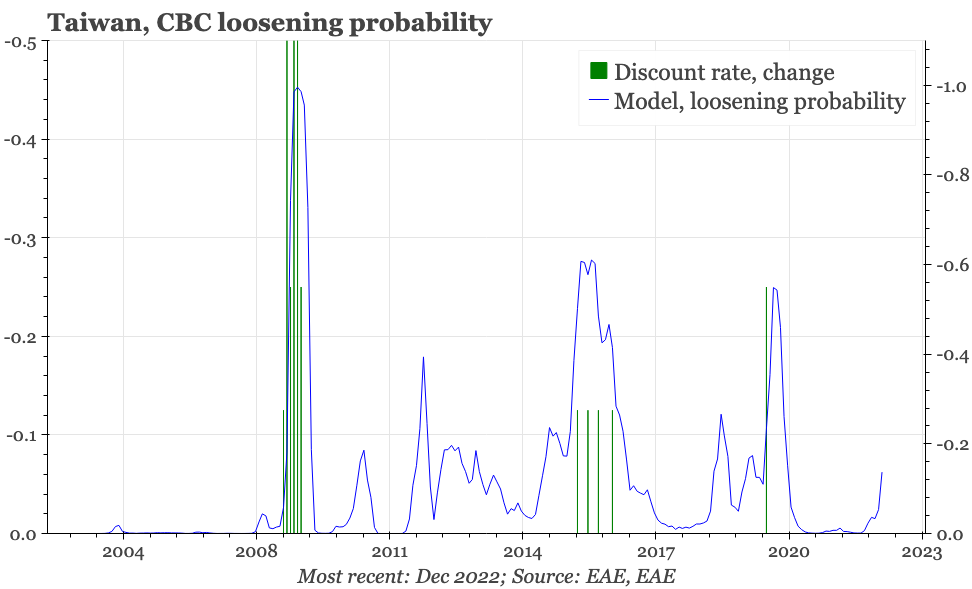

The East Asia Economist: modelling the reaction function of Taiwan's CBC

A couple of weeks ago, we outlined a policy reaction function for the BOK. Today we do the same for Taiwan's central bank, the CBC. Perhaps because Taiwan has never really experienced any inflation, we couldn't find a way in which CBC policy changes were triggered by shifts in the CPI. All the inputs are instead measures of activity, or financial market indicators. The model strongly suggests that the tightening cycle is over, but isn't yet indicating that loosening is about to begin.

Cycle

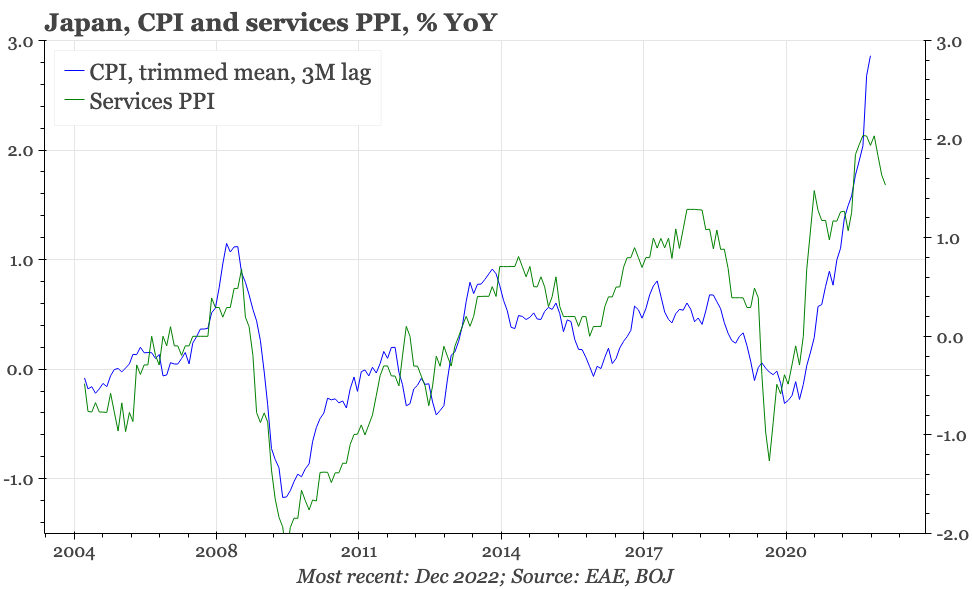

Tokyo CPI rose again in January, and on a headline basis is now above 4% YoY. MoM inflation was also strong, though leading indicators continue to suggest the peak should be close. Consistent with that, other data this week showed services PPI inflation in December falling.

The summary of opinions from the BOJ meeting of 17-18th January indicated that some members of the Monetary Policy Board think inflation might be starting to gain some momentum. But that view remains somewhat tentative, and seemingly held only by a minority. The summary (unsurprisingly) gave no indication from the MPB discussion that the December change in the YCC was designed as a tightening, though one member did say the continuation of easing would need to be "examined" at some "point in [sic] future". The board did mention hope that the enhancement of the bank's Funds-Supplying Operations against Pooled Collateral operations would help improve the functioning of the bond market. Rates did fall in the first half of last week, but rebounded by Friday.

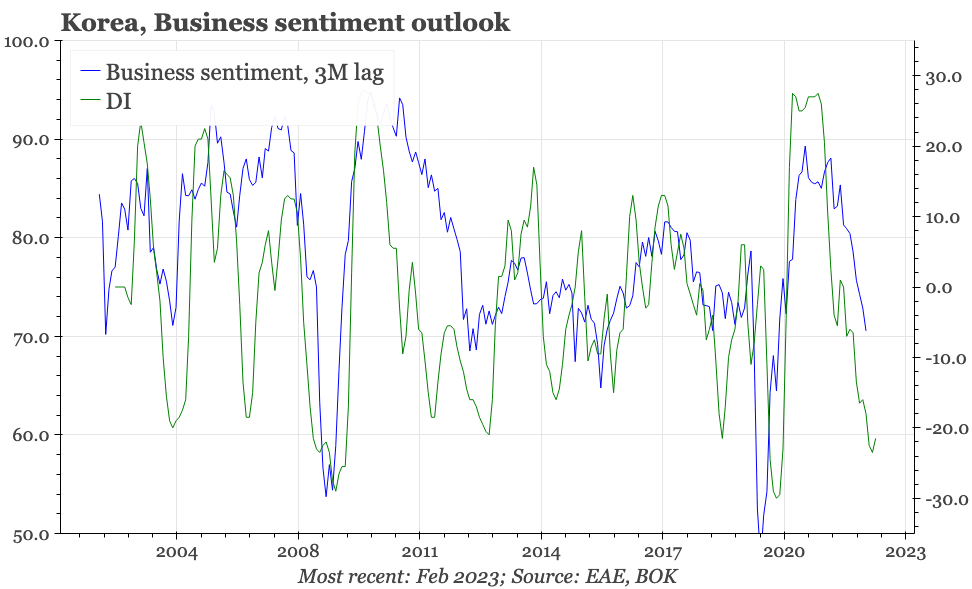

The consumer confidence survey showed a rise in inflation expectations in January. That probably reflects a stabilisation of headline CPI on the back of higher utility prices. It would be more significant for inflation if improving market sentiment towards the global cycle starts to show up in a real strengthening of Korean industrial data. On a headline basis, that didn't happen in the latest business survey, which showed sentiment continuing to fall fast, to a level at which the BOK has historically cut rates. The details, though, gave just a hint of improvement, with exporter sentiment and the diffusion ticking up.

With the Lunar New Year holiday putting all news on hold in recent days, attention in the coming week will be firmly back on China as the country gets back to work. There are data releases, with the January PMIs. However, the focus will be on high-frequency data – daily housing sales, metro passenger numbers, the return of migrant workers to cities – that will indicate how far and fast activity is recovering, not just out of the holiday, but from the covid disruption of the last few months. Elsewhere, CPI data and exports will be important for the BOK. In Japan, there's consumer confidence and December labour market data. And for Taiwan, the PMI, as well as export orders and IP.