Last week, next week

What happened on East Asia Econ last week.

I am travelling in Japan, so this update is a bit later than usual.

This is what happened on East Asia Econ this week.

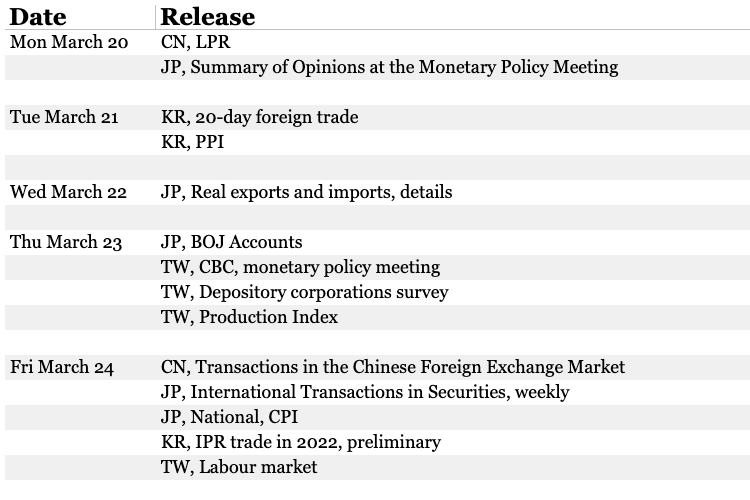

With China lacking a Monetary Policy Committee that has regular meetings at which decisions are taken about policy, we never know exactly when policy changes will be announced. But only in that sense is the cut in the Required Reserve Ratio (RRR) on Friday a surprise. Given China's macro conditions, it isn't unexpected. Our model of China's monetary policy reaction function, which uses M1 (for money supply), equity prices (for price inflation) and excavator sales (for economic activity) has been continuing to warn of further loosening, which in China can happen in the form of cuts in either the RRR or interest rates. Until the pace of China's recovery out of covid accelerates, the PBC is likely to remain in loosening territory.

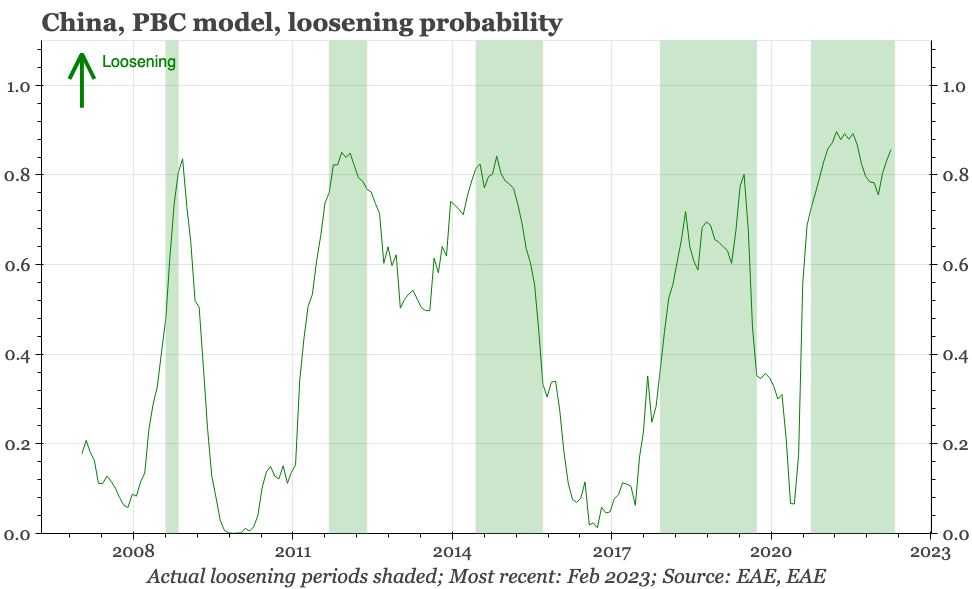

Cycle update – soft growth. Official activity data for January-February were soft, with retail sales growing by just 3.7% annualised. Through January at least, China had yet to escape fully from the shadow of zero covid, so there should be more recovery ahead. But given the low base because of the recession last year, the pace of recovery seems soft.

Cycle update – home price inflation returns. Property prices rose in February for the first time in 17 months, consistent with other data suggesting the market has reached a floor. Interest rates indicate upside, but buyer sentiment has been weak. We are waiting for the PBC's Q1 depositor survey to get a sense of change in that cautiousness.

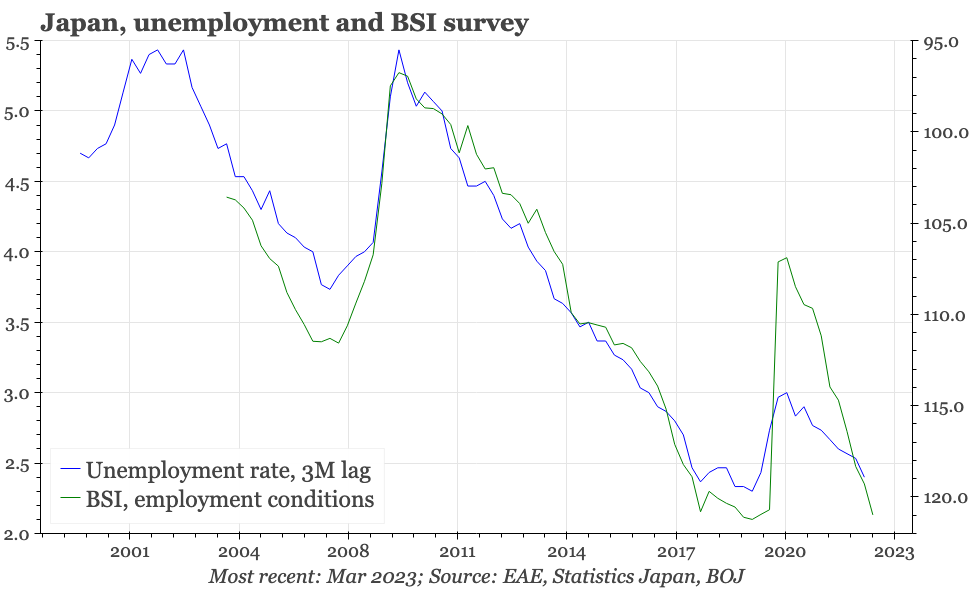

Cycle update – BSI solid. The quarterly Business Sentiment Index survey reinforces recent themes: that growth should be a bit stronger in the next few months, and that the labour market should finally get back to pre-covid levels of tightness.

Cycle update – exports sideways. Imports have fallen, allowing the trade deficit to narrow. Exports are going sideways. Our regional export leading indicator has started to lift, which should benefit Japan. But for export performance to improve materially, Japan's auto sector needs to perform more strongly.

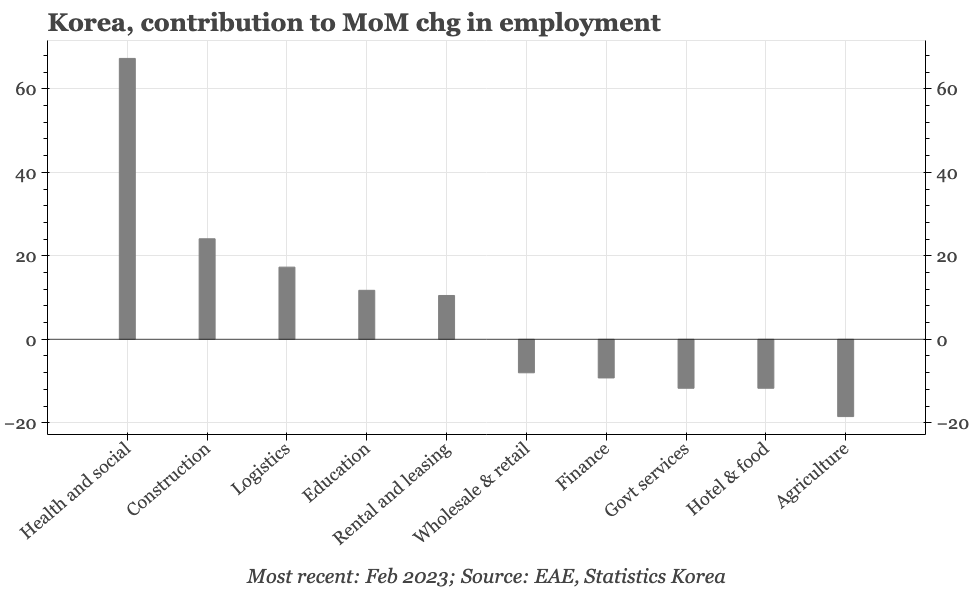

Cycle update – strong employment. Import price inflation continues to slow, as does consumer lending, but there was a sharp bounce in employment in February. That doesn't look cyclically driven, with employment in health and social services growing the most. But still, it means the BOK will likely remain hawkish for the moment.

Taiwan – resilient wage growth. Wage growth is quite strong in Taiwan, particularly relative to the weakness of the manufacturing cycle. So far, the strength is more apparent in manufacturing. It will become more important for inflation if it starts to show up in services, where productivity growth is slower.

The policy highlight this week will be the quarterly monetary policy meeting of Taiwan's central bank, the CBC. Our model isn't suggesting further tightening. This week, Taiwan also releases labour market for February. Other than that, it is a quiet week, with the data highlights being Japan CPI for February (likely lower, on the back of government subsidies), and Korean 20-day exports for March.