Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

This is what happened on East Asia Econ this week.

Regional themes

Across the region, there is evidence of industrial/export weakness, combined with services/domestic strength. But this overall theme isn't playing out the same way in all economies.

It is in Taiwan and Korea that the overall trend is most significant, in the sense that there is a real decoupling – so far– between the severe weakness of exports, and the strength of labour markets. As long as this persists, it should support core inflation, and so has implications for central banks.

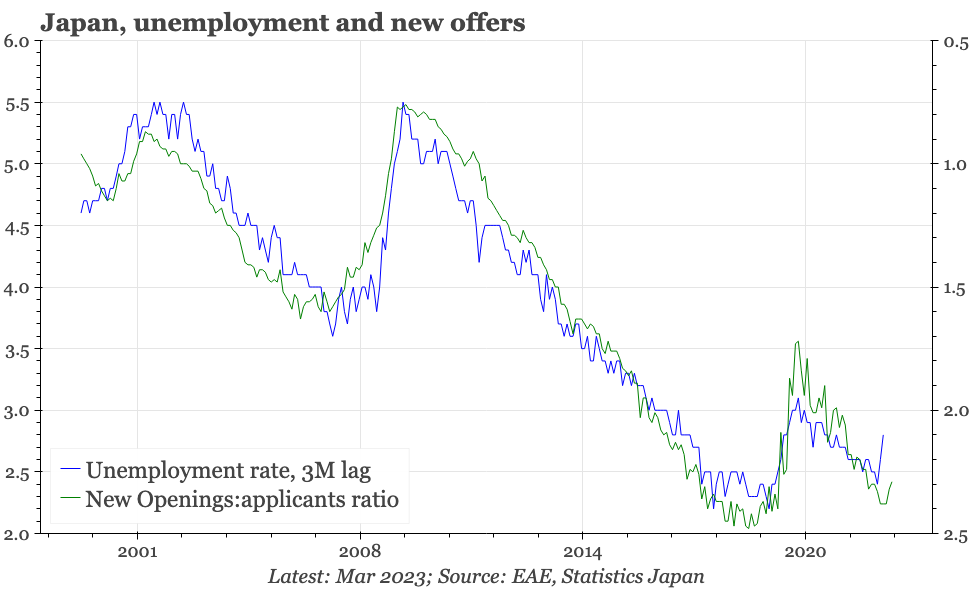

It is a real theme in Japan too, with sentiment weak in manufacturing, but strengthening in non-manufacturing, and leading indicators for the overall economy also improving. This matters when inflation is already high. But the trend is patchy, with labour market data in the last couple of months being soft. This in turn forms some of the context for Governor Ueda's comments this week on the need for patience.

The gap between services and manufacturing is perhaps most pronounced in China. But the market significance seems less, given the labour market doesn't seem especially tight, and inflation still running at a very low rate.

Thematic

The East Asia Economist: How brave is the BOJ?

Decisions about changing the policy framework are interwoven with deciding that there really is a generational shift in inflation occurring. Given the BOJ's history of premature tightening, that requires almost Jedi-like levels of bravery, and we doubt the bank is ready to reach that conclusion yet.

Cycle

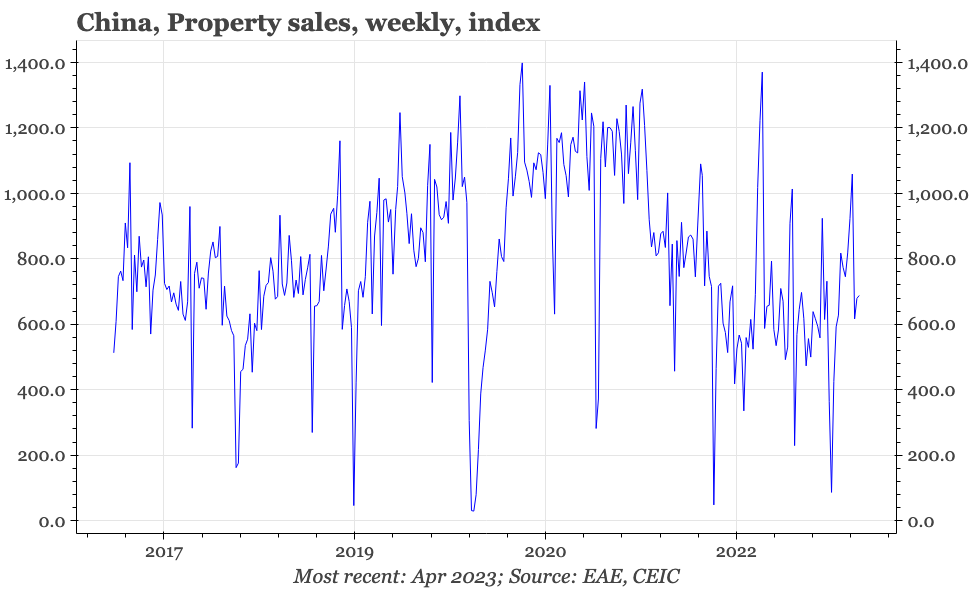

Cycle update – industrial cycle. We had started to become hopeful that the property market was picking up, but transactions have fallen back down again in April. Other indicators for the industrial cycle also look bearish, with output prices weak, and profits still falling.

Cycle update – manufacturing contracting again. We've been more cautious on the outlook than the consensus, and remain so after the official April PMIs. The one indicator that gives us pause for thought is the strength of the construction PMI, but that would be more convincing if there were broader signs of the property cycle really lifting.

Cycle update – BOJ and cycle continuity. As widely expected, the BOJ meeting today didn't announce changes in policy. Data releases also showed consistency, with Tokyo inflation in April still accelerating but the labour market in March going sideways.

Cycle update – no technical recession. Driven by private consumption, Korea avoided technical recession through March. The strength of consumer spending was a surprise, so we'd assume that downside risks remain. But even if that proves to be true, it won't necessarily affect the BOK's view of 2H recovery, which is based on the idea of stronger exports.

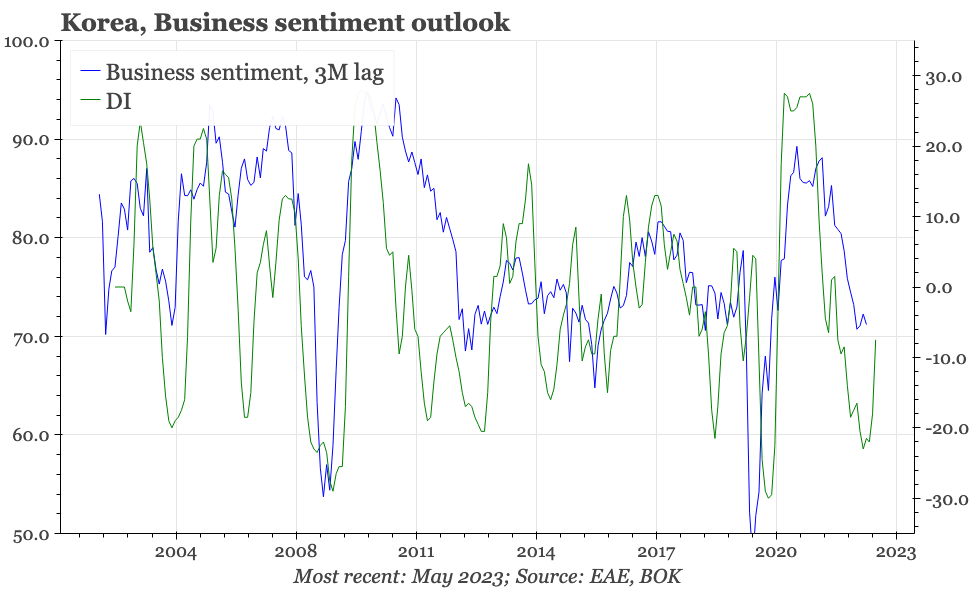

Cycle update – inflation falling, cycle rising? Business sentiment remains weak enough to suggest BOK cuts, and the fall in consumer inflation expectations indicates some easing of headline inflation pressure. But there's also signs in both surveys of an upturn in the cycle, creating a risk that core inflation won't fall so far.

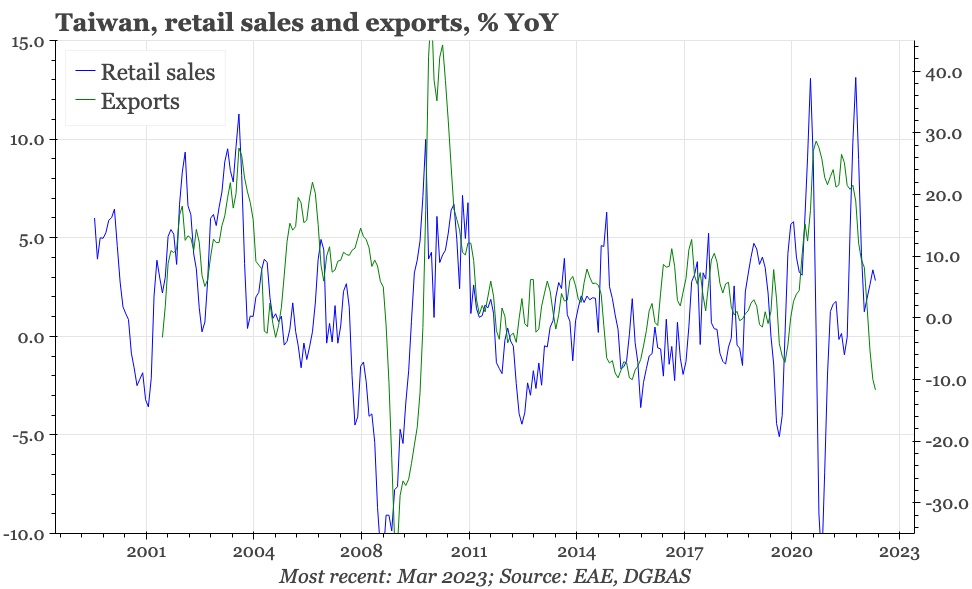

Taking stock – unusual domestic strength. Taiwan's domestic economy and inflation are proving more resilient than the weakness of the export cycle would suggest. This desynchronisation is partly due to covid, and as long as it persists, means the usual ways of looking at CBC behaviour could well prove misleading.

With the early May holidays – lengthy affairs in China and Japan – the next week is relatively quiet for both policy and data. For the region generally, the highlights will be the PMIs. In Japan specially, tomorrow's consumer confidence report is important, both for inflation expectations, and to see whether last month's lift in overall sentiment continues. For Korea, there's full-month April CPI and trade data. Taiwan will also release inflation data.