Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

This is what happened on East Asia Econ this week.

Highlights

This chart pack summarises our views for the region.

Thematic

The East Asia Economist: Services and sticky inflation

Manufacturing is in recession, but employment is rising and core inflation not falling. With services normalising after covid, this unusual set-up can persist. That's particularly true in Japan, but in Korea and Taiwan too, it looks like a DM recession will be needed to bring down core inflation.

A public video summary is here.

Cycle

Cycle update – really, in deflation. That China is in deflation – both PPI and CPI fell MoM in April – while the rest of the world struggles with inflation really is a remarkable outcome. Underlying inflation isn't quite that weak: core CPI inflation remains around 0.7% YoY. But still, there really isn't upwards pressure on prices either.

Cycle update – not crazy, but still, strong. China's exports weakened a bit in April from the heady level of March, but remained strong relative to usual indicators of export demand. Imports remain weak, a reminder of the softness of the domestic industrial cycle. The trade surplus continues to widen.

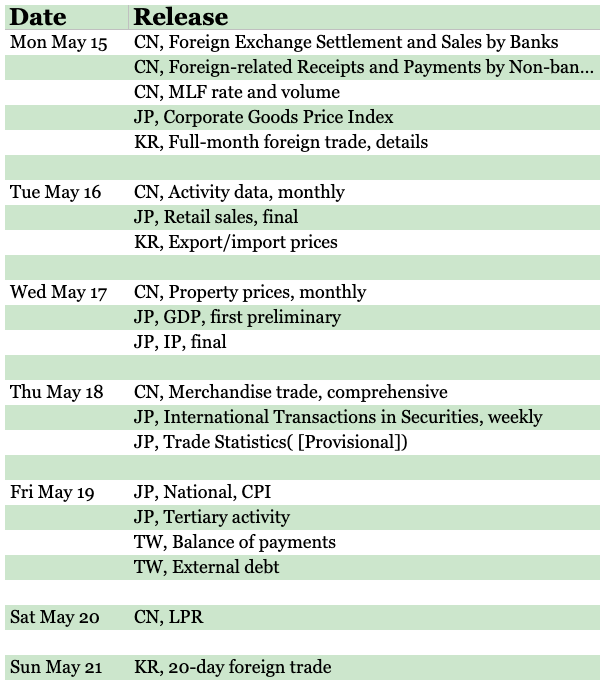

Cycle update – 2020 redux. After a strong start to the year, April credit growth was weak. The apparently short-lived credit cycle is reminiscent of 2020, but three years ago and the economy was boosted by exports and property. Real estate is much weaker this time, with mortgage lending collapsing again in April.

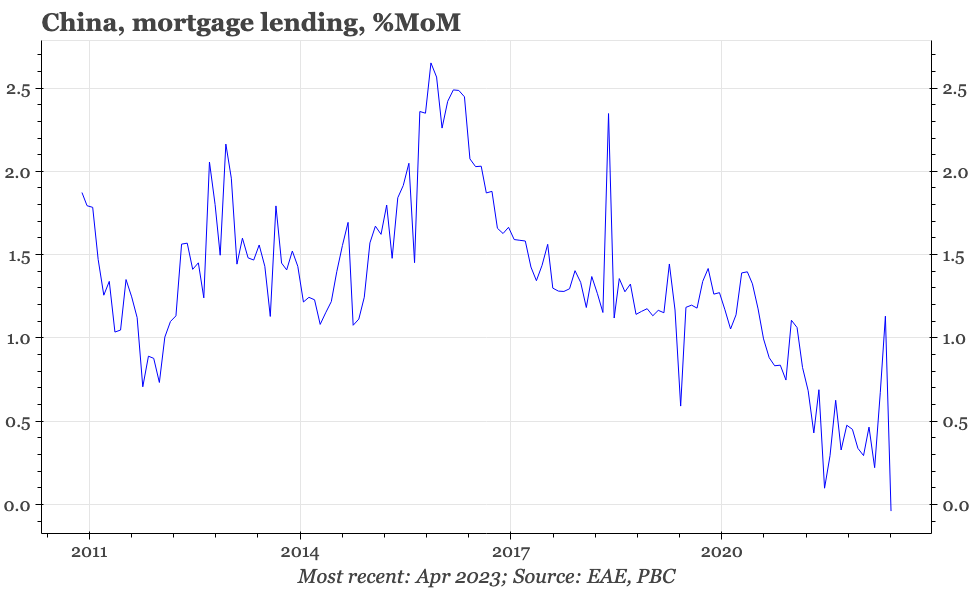

Cycle update – strengthening. Japan's cycle is gaining momentum, led by a recovery in services. In this context, the recent softness of the labour market data looks even odder. The BOJ's outlook report wasn't concerned, highlighting this year's strong shunto round. This will keep upwards pressure on core CPI.

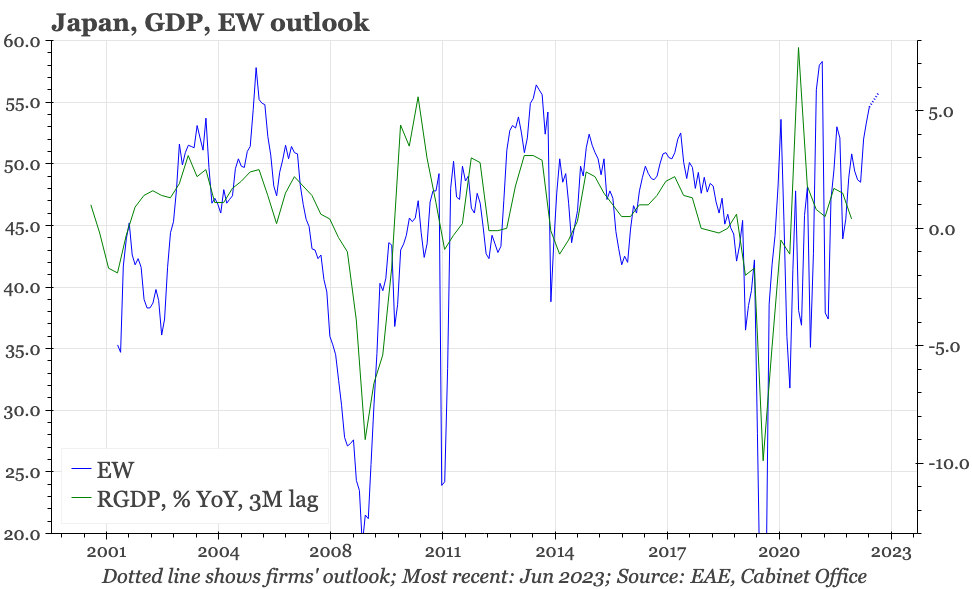

Cycle update – labour market stable. The labour market went sideways in April, keeping the unemployment rate at 2.6%, the lowest since the 1990s. Non-manufacturing business sentiment suggests employment will remain around current levels for the next 6M. That doesn't seem likely, on its own, to bring down core inflation.

Cycle update – no change. Taiwan's data continue to show that the manufacturing sector remains in recession, but that hasn't yet defused the deflationary pressure of the last few months. Indeed, wage growth in manufacturing continues to run at 3-4% annualised, which by Taiwan's standards is quite high.

Next week's highlights will be China's release on Tuesday of April activity data, and whether the likely weak data are pre-empted by a policy reaction, with tomorrow's MLF decision. We still expect rate and/or RRR cuts. In Japan, there's Q1 GDP data, but more important will be inflation indicators: April PPI will be released Monday, and national CPI on Friday. At the very end of the week, we'll get the first reading on how the regional export cycle is faring in May, with the Korean 20-day data.