Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

This is what happened on East Asia Econ this week.

Equities are stronger in Taiwan and Korea, but sentiment surveys overall still look bearish. In Japan, there was a meaningful rise in wage growth in May, but other labour market indicators remain soft and there's now also hints that the recent upturn in growth momentum is starting to moderate. The one economy where the picture is clearer is China, with inflation continuing to look very weak.

In this short video we try to make sense of all this.

Cycle update – no change. The BOJ Tankan suggests continued modest growth and easing inflation. There are reasons to think the risks around this outlook are to the upside. But until those risks become reality, and in particular that the labour market tightens, the BOJ likely won't be in a rush to move policy.

Cycle update – wage growth accelerates. Regular full-time worker wages lifted in May, just the sort of step-change that the shunto seemed to make likely. That is an important development. But part-time wage growth is more modest, and there was no big lift in the consumption activity index from the BOJ that was also released last week.

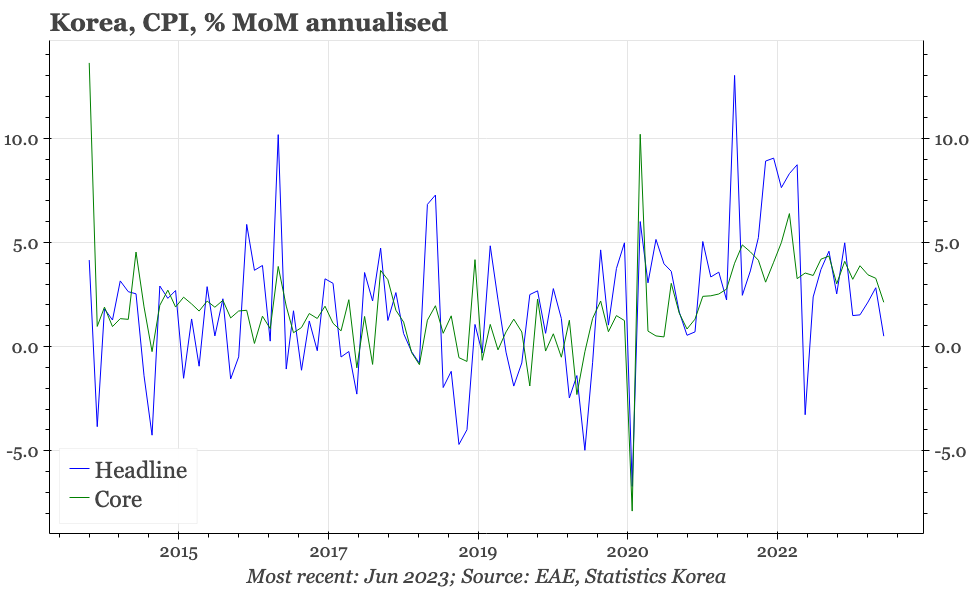

Cycle update – finally, core inflation drops. Headline inflation dropped in June, but there was also a first significant easing in core. That justifies the BOK being on hold, with the direction from here being dependent on external demand: does that now rebound on the back of AI demand for tech, or is DM about to take a dive into recession?

Cycle update – much stronger PMI. The surge in the official PMI in June is at odds with other manufacturing indicators. But it is in line with the message being sent by the equity market, and recovery is worth keeping on the table as a scenario when unemployment is low and non-manufacturing sentiment continues to rise.

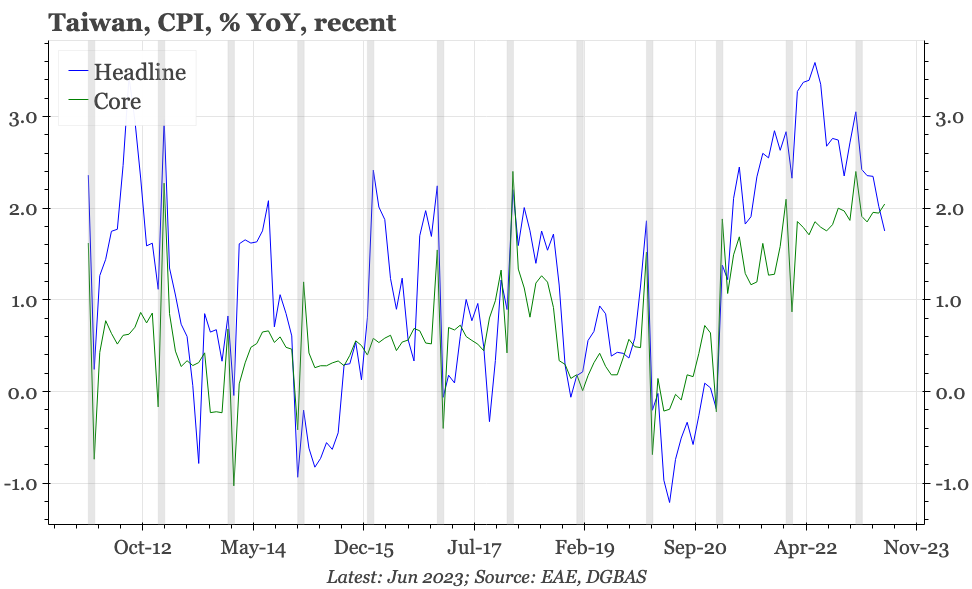

Cycle update – core inflation holds up. Headline inflation is receding fast, but core inflation in Taiwan remains elevated, consistent with the low rate of unemployment. That will become important for the CBC if there is now any upturn in export growth.

In terms of policy, next week's highlight is the BOK meeting on Thursday. The inflation data should allow the bank to be a little more doveish, but the outlook for rates will depend on how optimistic the bank is about the signs of a recovery in activity. For data, after a quiet week, the focus will be back on China, with inflation, credit and foreign trade. Inflation will likely remain very weak, which for us is the key issue for macro in China tight now. The Economy Watchers survey in Japan will give an update on the extent of any moderation of the recent upturn in cyclical momentum. Taiwan will release wage data. That has been picking up, which is consistent with the fall in the unemployment rate, and a development that in turn supports core inflation.