Last week, next week

A summary of what happened on East Asia Econ last week, and what to look for in the next seven days.

This is what happened on East Asia Econ this week.

Thematic

Japan: not tight enough. Our concern that the labour market wasn't tight enough to get the BOJ to change YCC proved wrong. But this line of thinking might still be useful. The BOJ on Friday changed its assessment around inflation to say risks are to the upside. Given that, if the labour market does now re-tighten, it will likely be the trigger to get the BOJ to raise its inflation forecast, which would in turn put pressure on it to allow yields to rise further.

Cycle

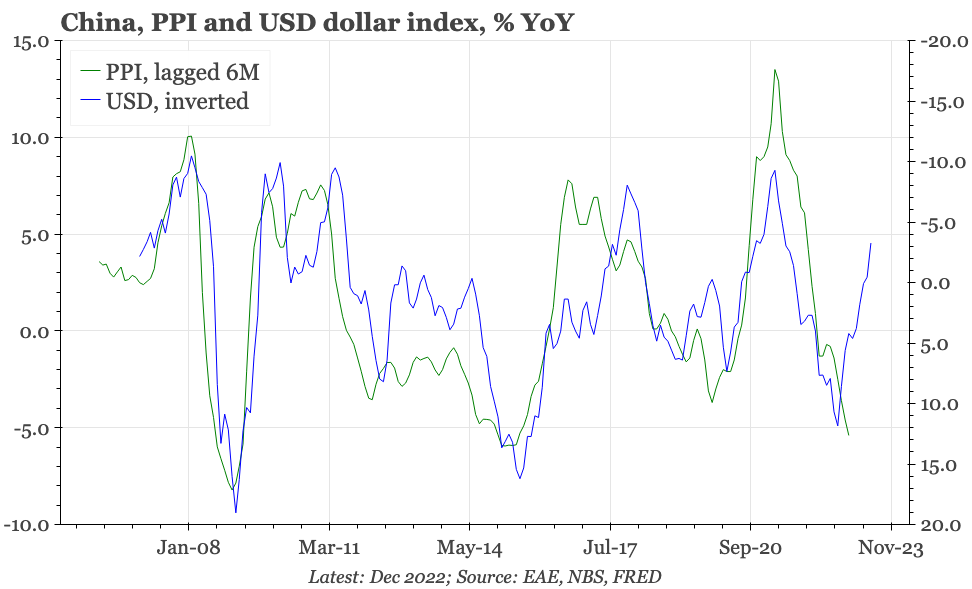

Cycle update – USD lifting prices? Industrial prices have ticked up in July. That isn't especially surprising, given the free-fall since April. More interesting is whether this reversal shows domestic prices are beginning to feel the effect of the weaker USD.

Taking stock – the Politburo meeting. The Politburo meeting excluded the phrase "housing is for living, not speculation", which seems one step towards our idea of last week, that officials say "property is for speculation". The markets liked the change, but we'd still want more help for households to get excited about a cyclical upturn.

Cycle update – Goods prices down, services up. Upstream inflation continues to ease. That is feeding into headline CPI, and given lags, that process is far from over. However, there are some signs that the fall in commodity prices has now reached a floor, and core CPI is starting to look sticky.

Taking stock – CPI risks "skewed to the upside". In raising rates on Friday, the BOJ said that it wasn't tightening because inflation was still below its 2% target. But while it didn't raise its inflation forecasts, it did alter its assessment of risks. In that context, the labour market tightening we expect becomes even more important.

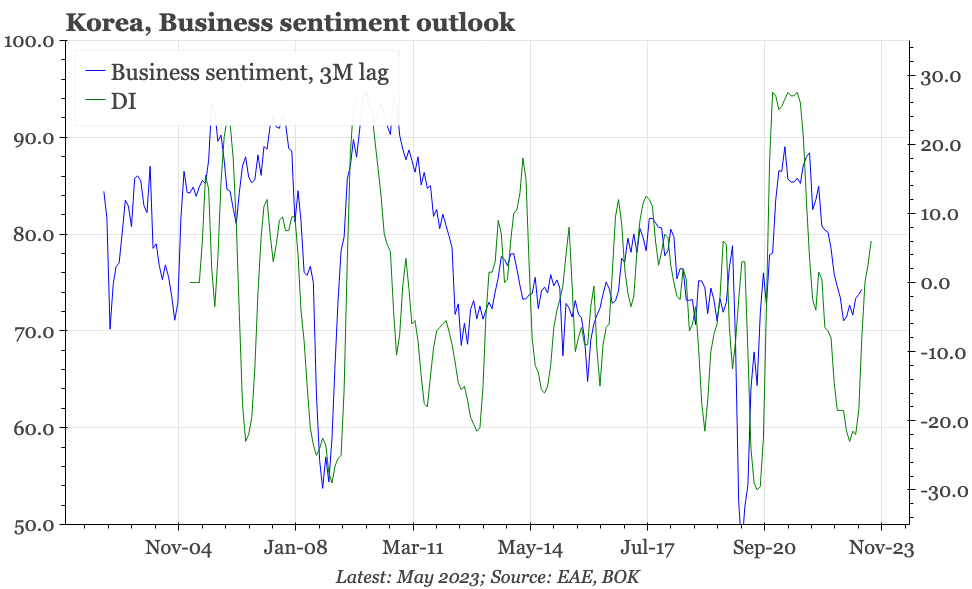

Taking stock – Going sideways. Consumer and business sentiment are helpful indicators for mapping out the direction of Korea's cycle. The July versions this week show inflation peaking, but the domestic cycle bottoming. Business sentiment is still soft, but there's a hint of bigger improvement in Q4.

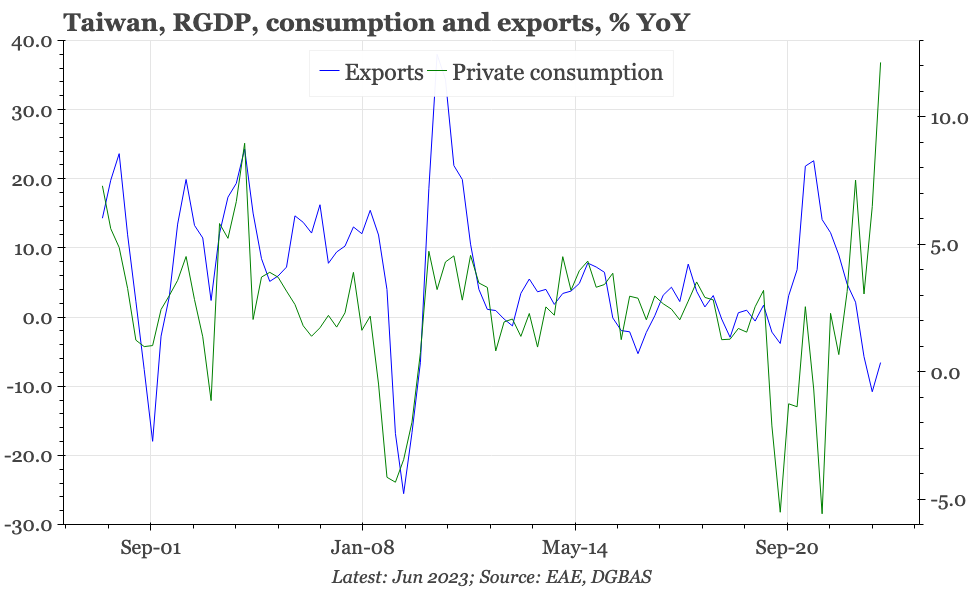

Taking stock – Still desynchronised. The defining characteristic of Taiwan's current cycle remains the desynchronisation of activity between weak exports and strong consumption. That can probably persist through Q3 but not much longer, with the next step for the central bank thus being dependent on whether exports recover from Q4.

Last week was big for policy, in both China and Japan. The next seven days it is back to the cycle, with the PMIs, Korean July exports, and Japan consumer confidence. There's also June labour market for Japan, which we continue to think is a very important indicator to be following. Korea will release CPI statistics for July.