Public Post

Region – the upside risks to inflation

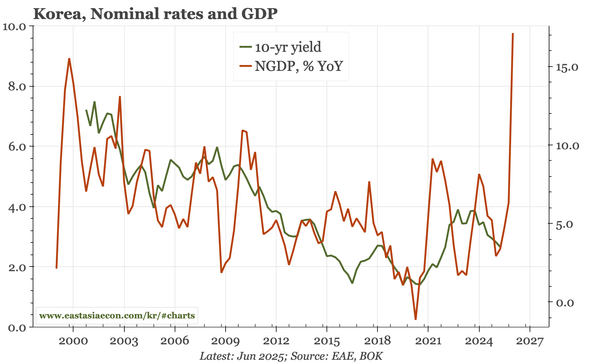

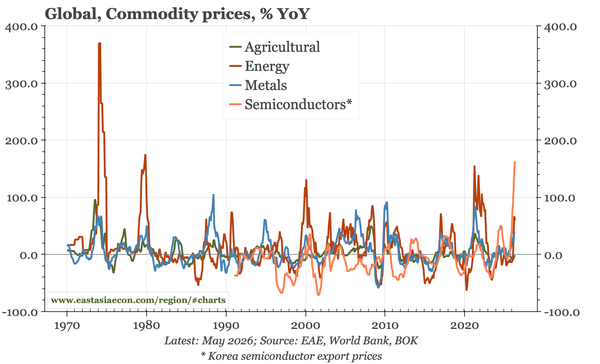

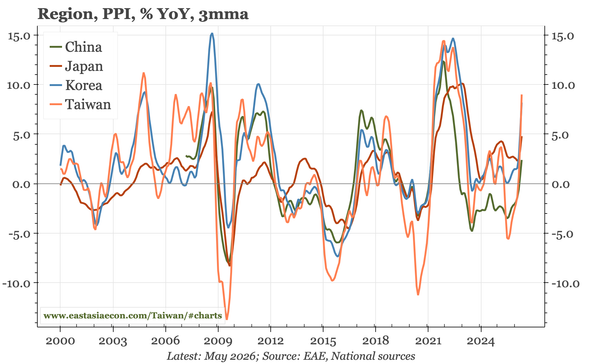

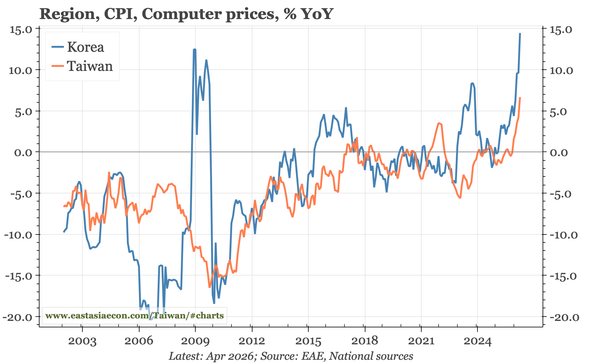

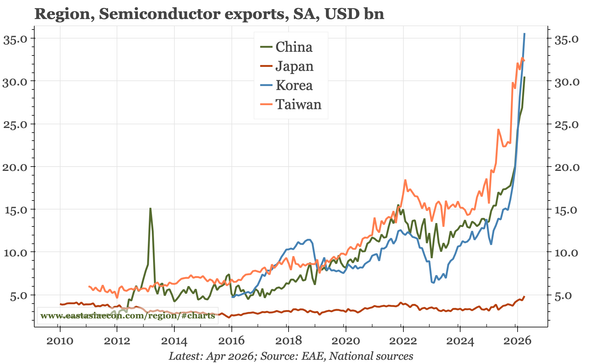

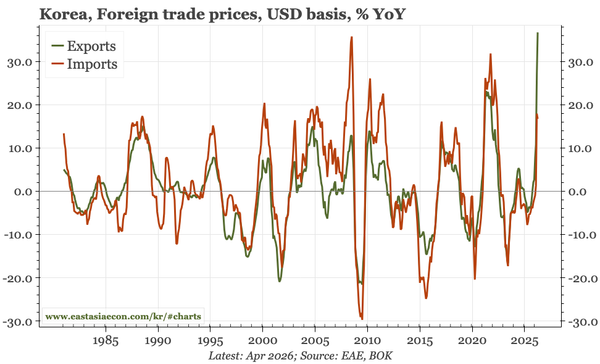

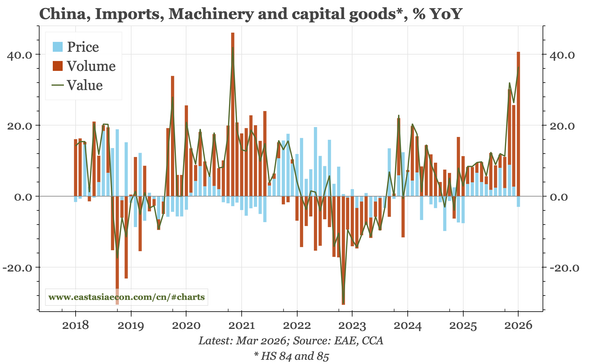

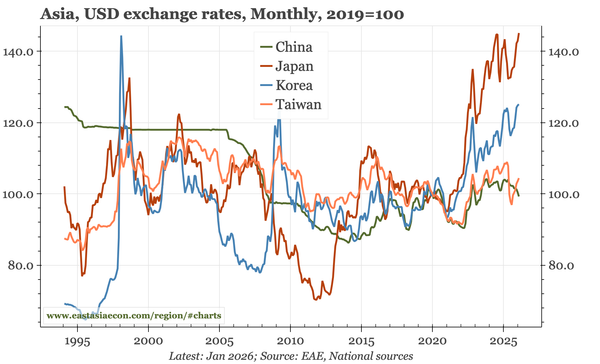

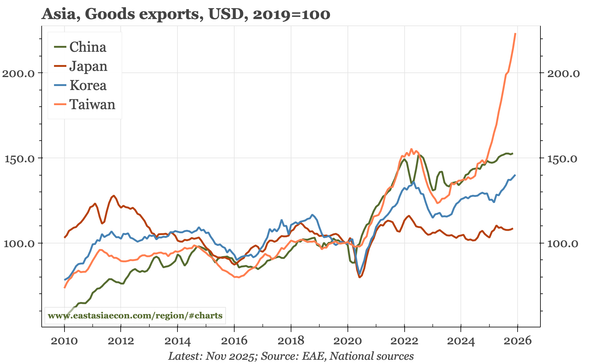

My latest video, discussing why inflation risks won't end even if the Iran War eventually does. The reasons: both cost-push and demand-pull from the semiconductor boom, dynamics that are being reinforced by the cheapness of currencies.