Region - exports to contract

Regional exports remain on track to fall by about 10% YoY by the end of 2022. That deterioration will continue to put downwards pressure on currencies, particularly the TWD and KRW, but the pace of depreciation should begin to lessen.

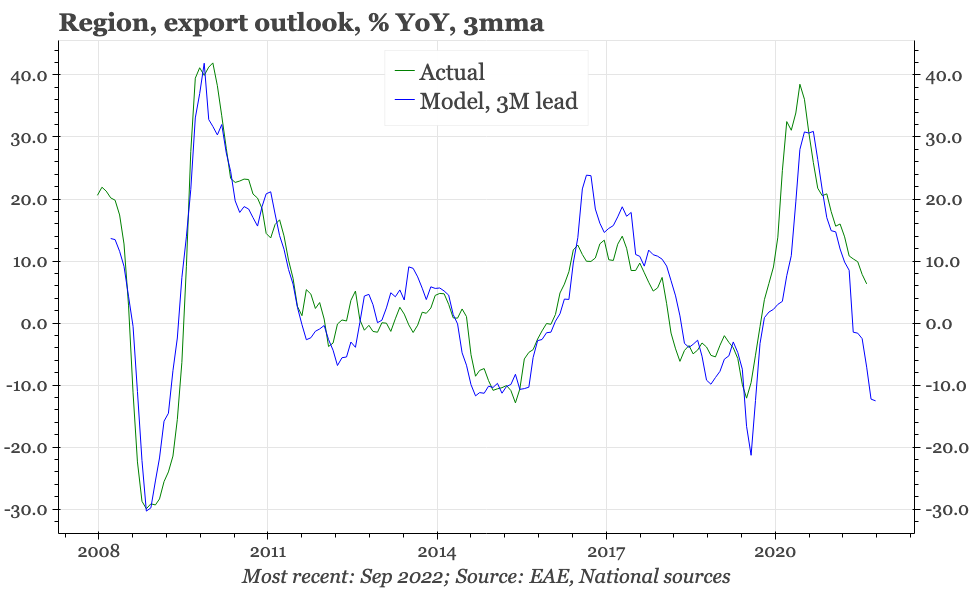

Updating the export leading indicator

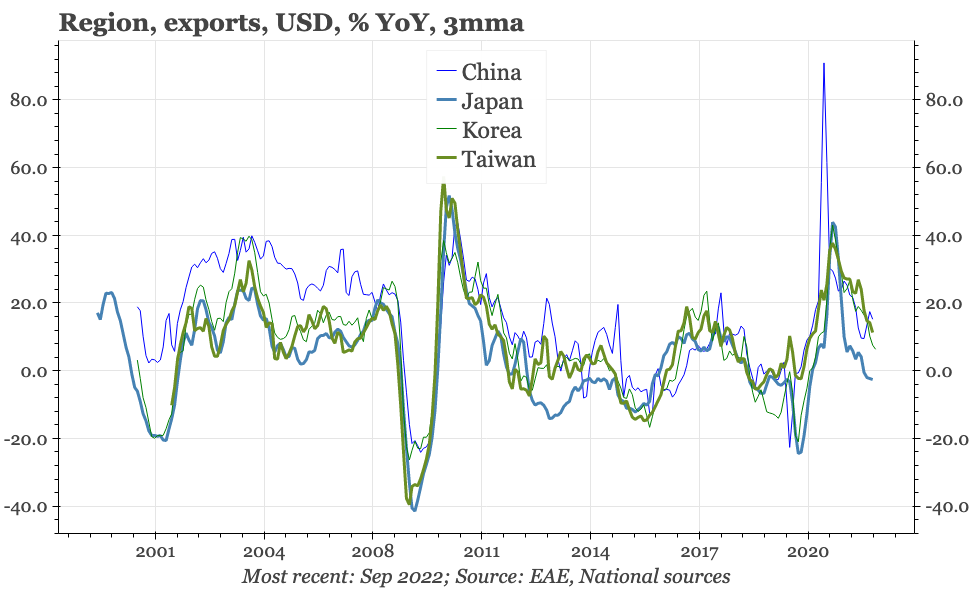

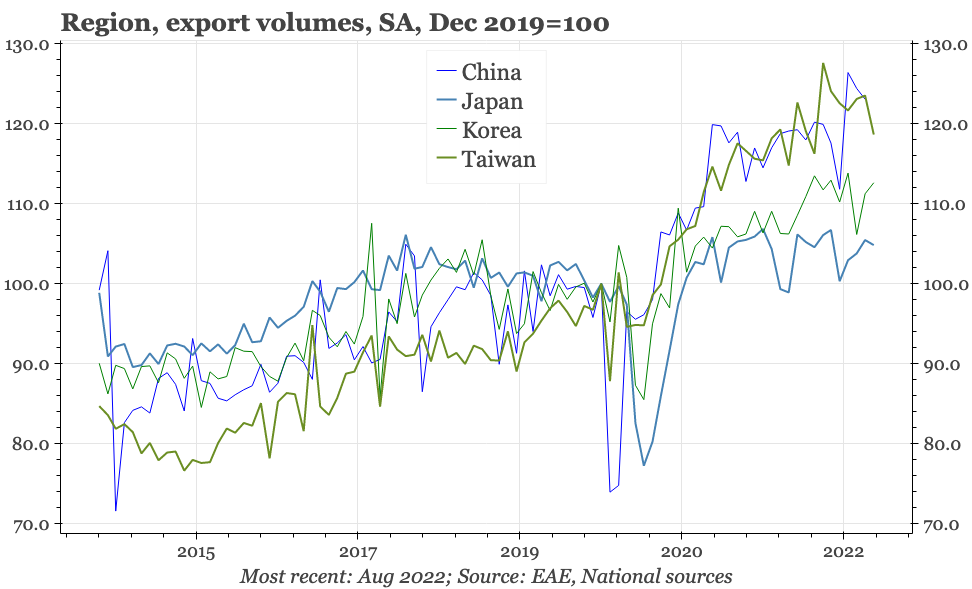

Exports across the region in the USD terms grew around 10% YoY in August. The exception was Japan, where exports on this basis contracted - although they surged in JPY terms. Sequentially, exports in most economies fell quite sharply in August.

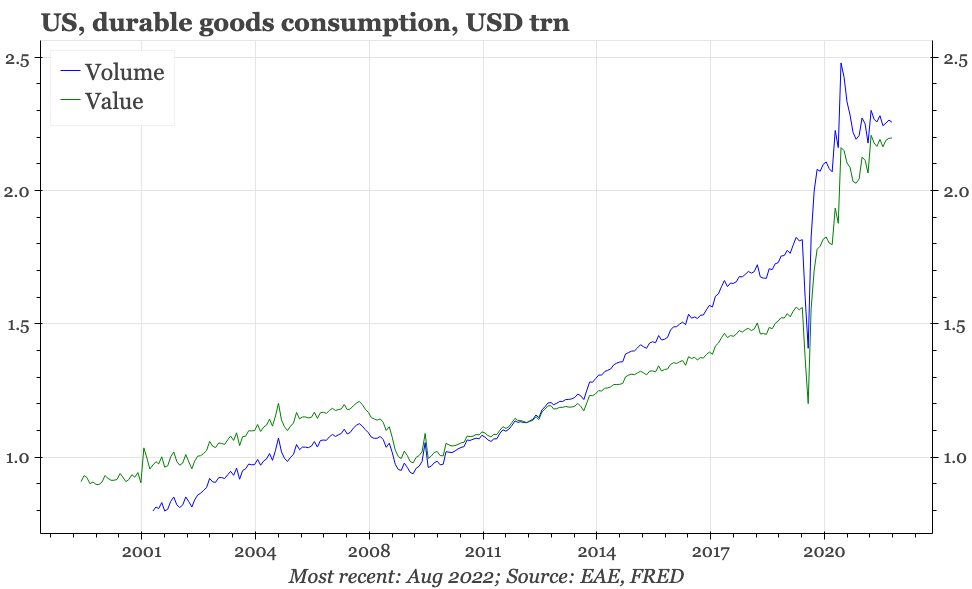

Our leading indicator continues to point to further downside ahead, with exports likely to be contracting by 10% YoY by the end of 2022. The drivers of this so far seem to be the property and covid crises in China, and the monetary tightening and energy price shocks in the rest of the world. The reversal of the pandemic shift in DM away from services consumption towards goods has started to occur, but doesn't seem particularly powerful yet. Data released yesterday show consumer durables demand in the US flat-lining, but not yet falling.

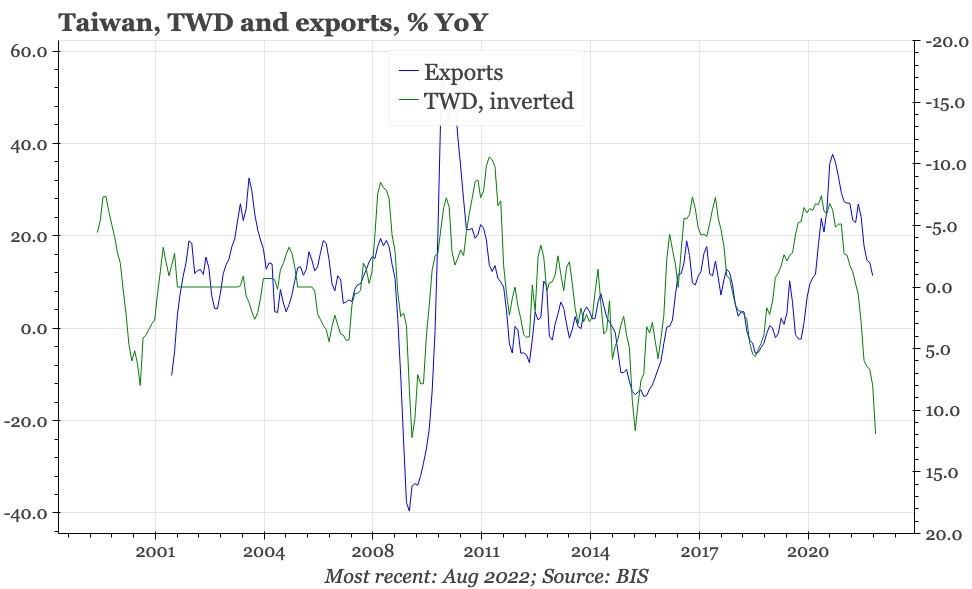

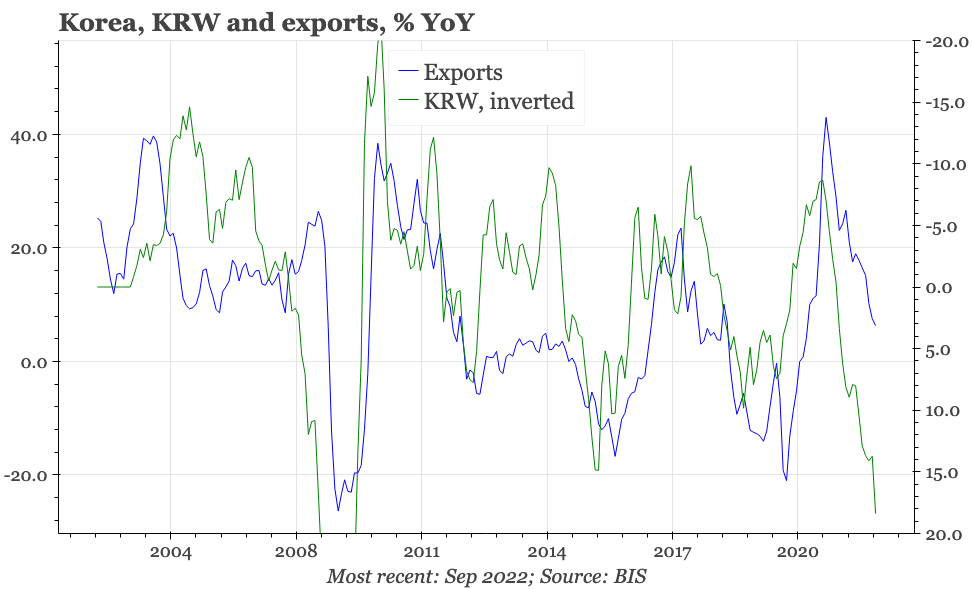

Historically, it is the KRW and TWD that have been most sensitive to the export cycle. Relative to the change in exports, both currencies have moved quite a long way already, dragged down by moves in the USD, and for Korea more than Taiwan, the rise in the import bill that has pushed the trade account into deficit. Both currencies could yet experience a perfect storm if the shift away from goods consumption in DM accelerates while US interest rates remain high. Even without that, the continuing softening in the export cycle should continue to put downwards pressure on the currencies, but the pace of the depreciation should begin to lessen.