Region – foreign trade

Foreign trade data releases from Japan, Taiwan, and Korea today aren't entirely consistent, but it does look like exports are no longer growing, with signs of a slowdown in demand from the US beginning to appear.

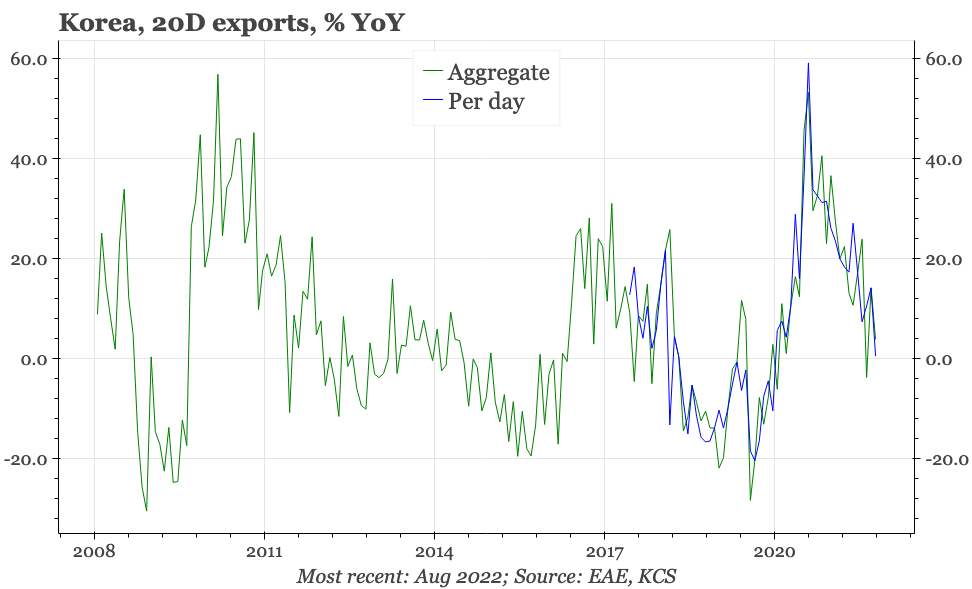

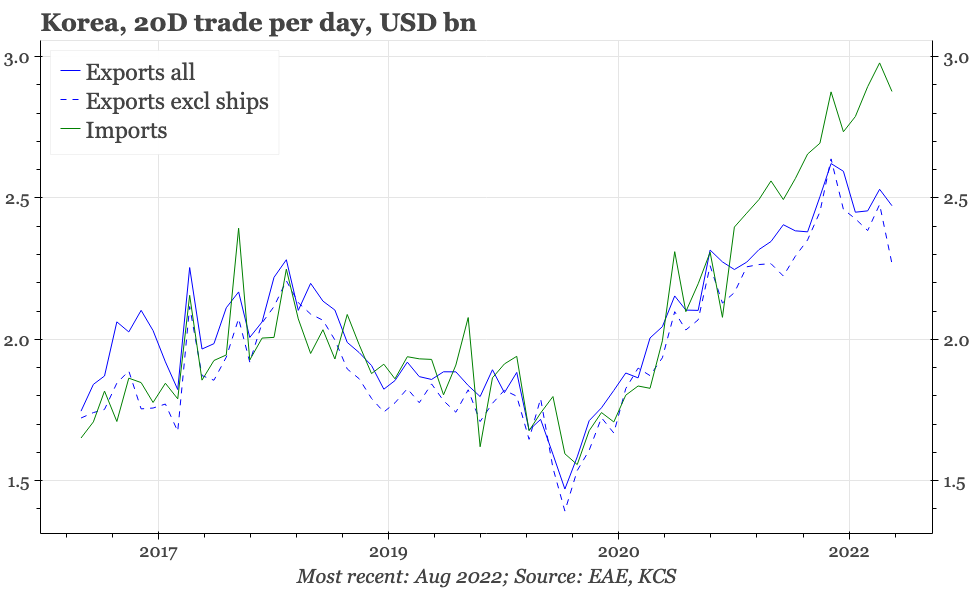

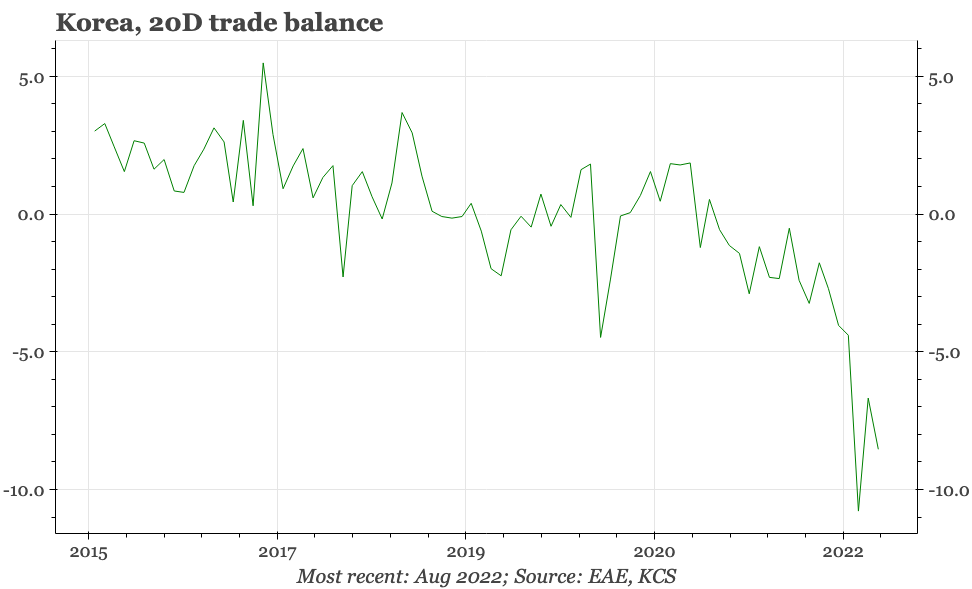

Korea: August 20D exports

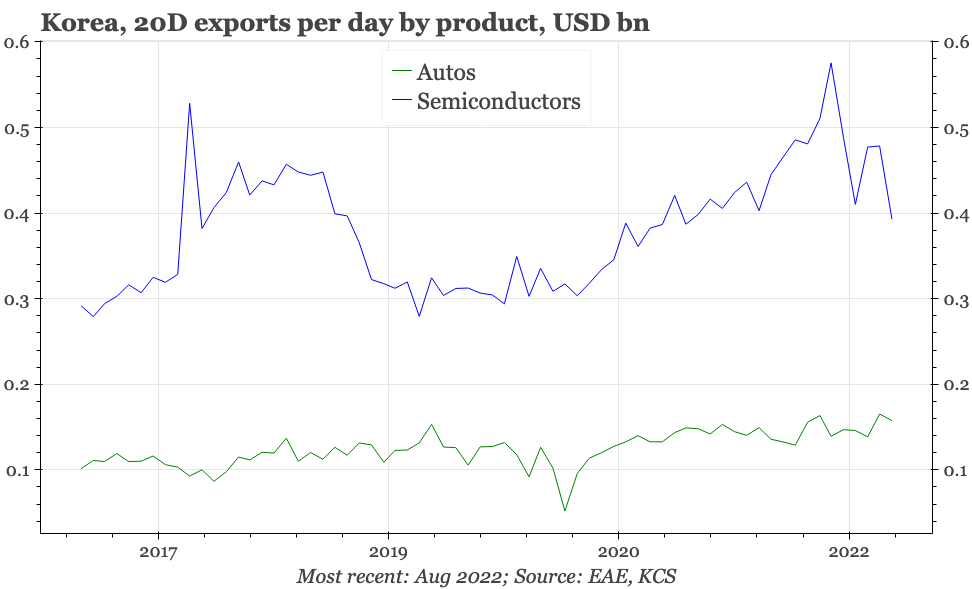

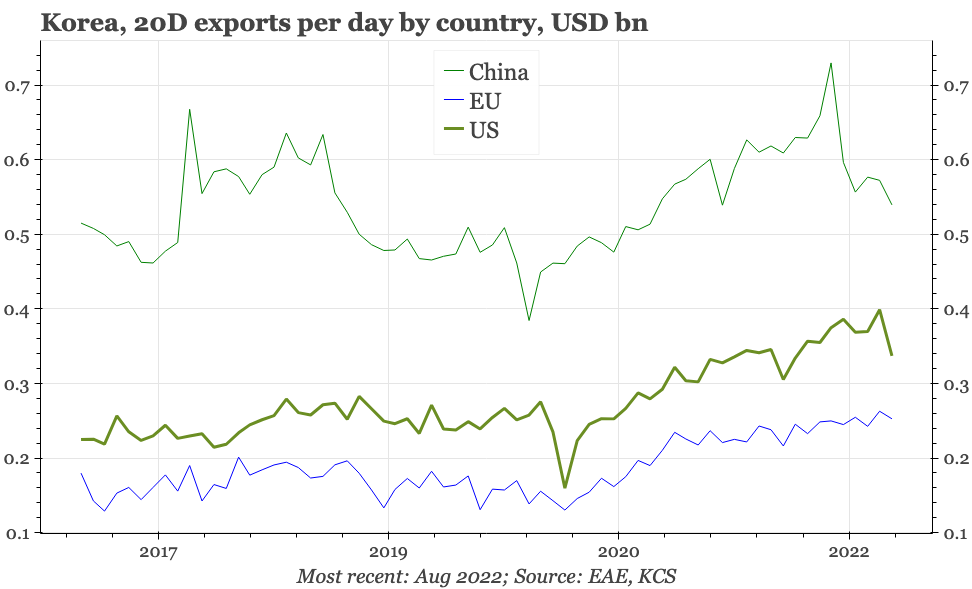

Korean export growth in the first 20 days of August continued to slow. The headline YoY rate of change softened to 3.9%. However, there were more working days this year, so underlying growth was even slower, at just 0.5% YoY. Moreover, after adjusting for ship exports – which tend to be volatile from month-to-month – the level of exports was almost 10% lower in the first 20 days of August compared with the same period last year, and are now around 15% below the peak of March.

Weakness this month is apparent in exports to China. That though isn't a new trend, being evident in Korea's data since April. But this month there's also been a fall in shipments to the US for the first time. A deterioration in DM demand is to expected as the surge in post-pandemic durables consumption normalises, and it would be significant for the path of exports in the next 6M if this deterioration is what is now starting.

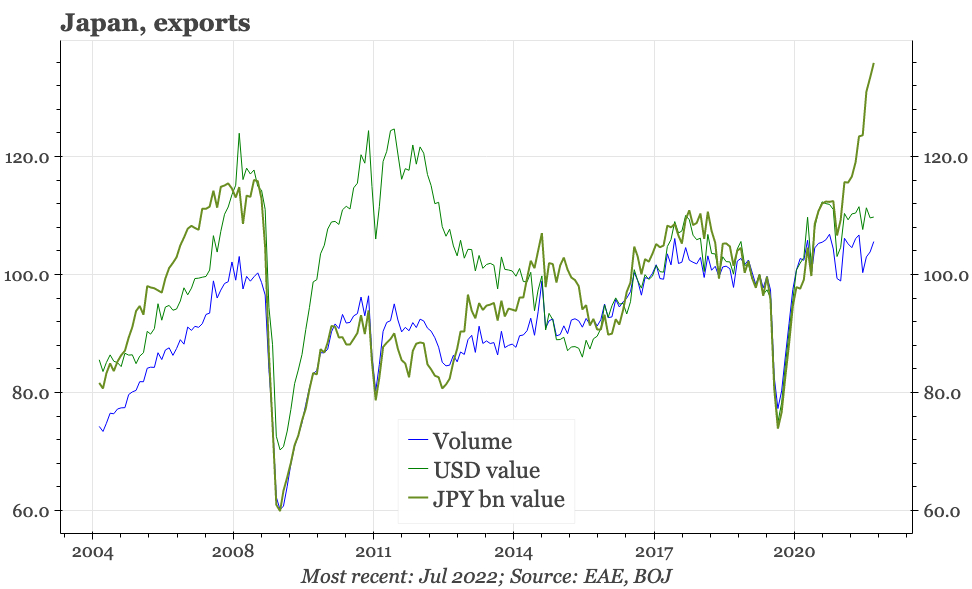

Japan: July export volume details

We already know from headline data released by the BOJ last week that overall export volumes rose MoM in July for the third consecutive month. For an economy that has been struggling, that is helpful, though in level terms export volumes are still below where they were in March.

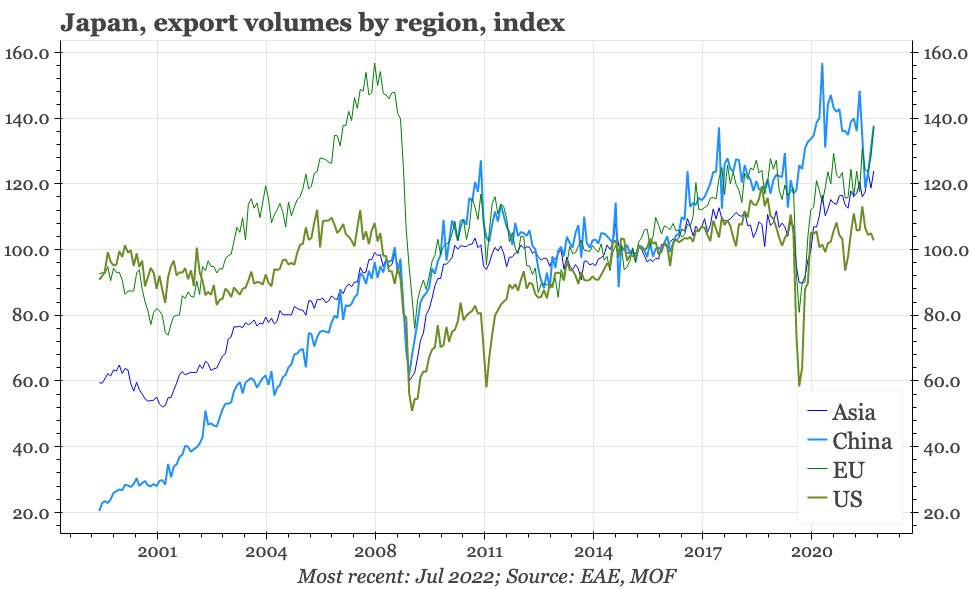

As with Korea, one reason for the fall-off since March is weakness in shipments to China. However, the detailed volume data released today by the BOJ show that, as with the overall total, exports to China rose in July for the third consecutive month. Exports to the EU and other parts of Asia were also strong, but shipments to the US weakened.

At the product level, the rise in exports in July was driven by a sharp increase in sales of capital goods. That looks like an anomaly, but we won't know for sure until next month. Shipments of autos also rose in July, though they remain well below the pre-pandemic highs.

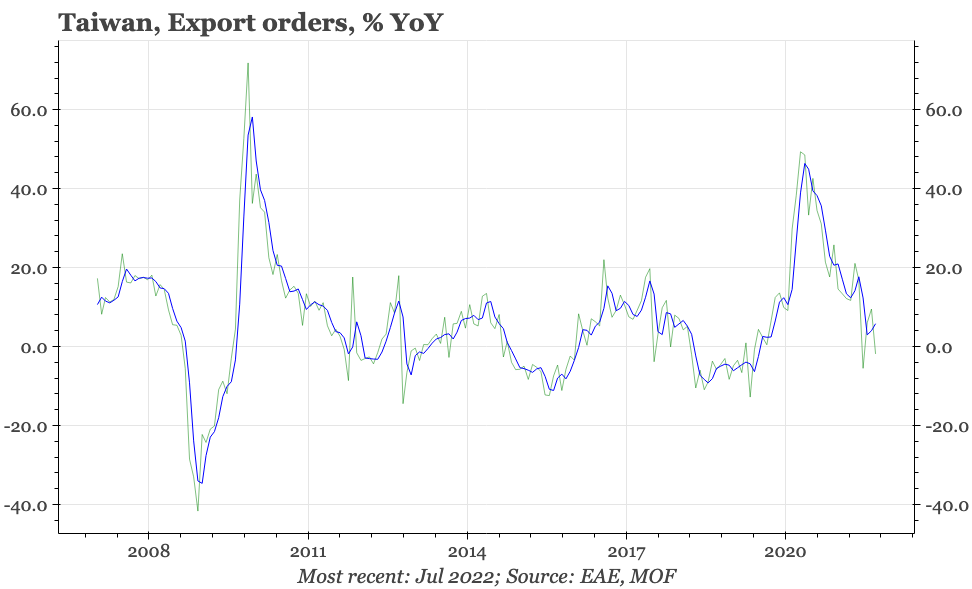

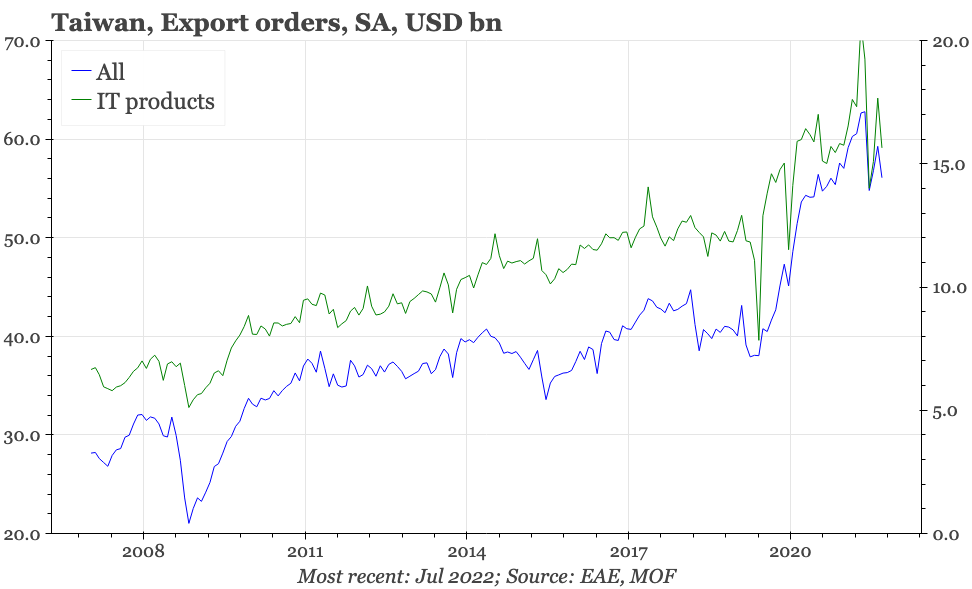

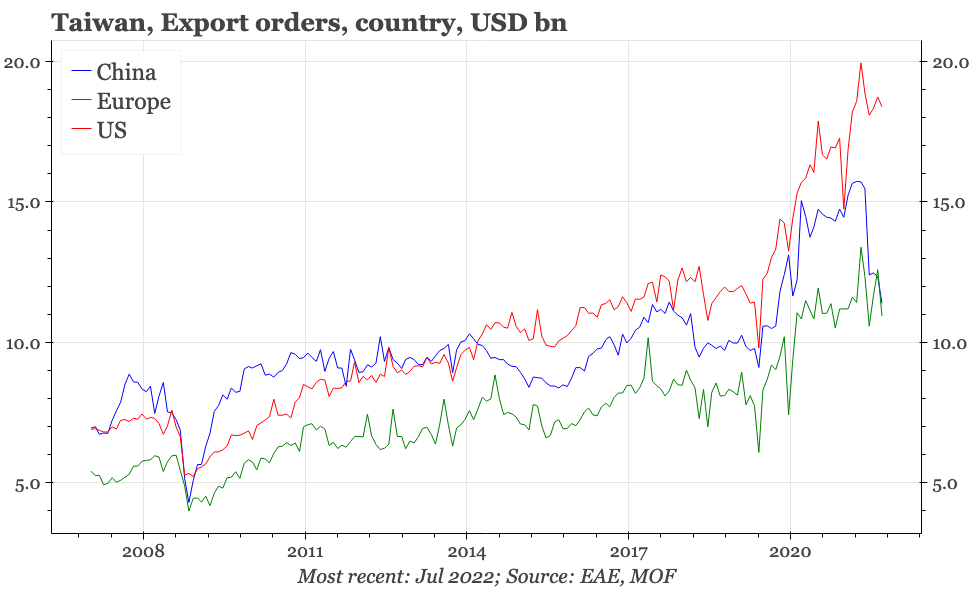

Taiwan: July export orders

At a headline level, export orders looked a bit better in August, with the smoothed average YoY growth improving to almost 6% YoY. The details though were softer. The level of orders dropped back almost to the lows of April, when the data were depressed by the lockdown in Shanghai.

Orders from China fell in July to the lowest since mid-2020. Given these are global orders received by Taiwan factories, the fall-off in demand from China likely reflects conditions in third markets as well as China itself. But specific orders from both the US and EU also fell in July. For both regions, the level of orders is still elevated, and there hasn't yet been much of a slowdown. However, the peak in orders does now seem to have passed.