Region – the cheapness of currencies

My latest video, discussing the cheapness of currencies across the region, why that didn't change in 2025, and why it might in 2026.

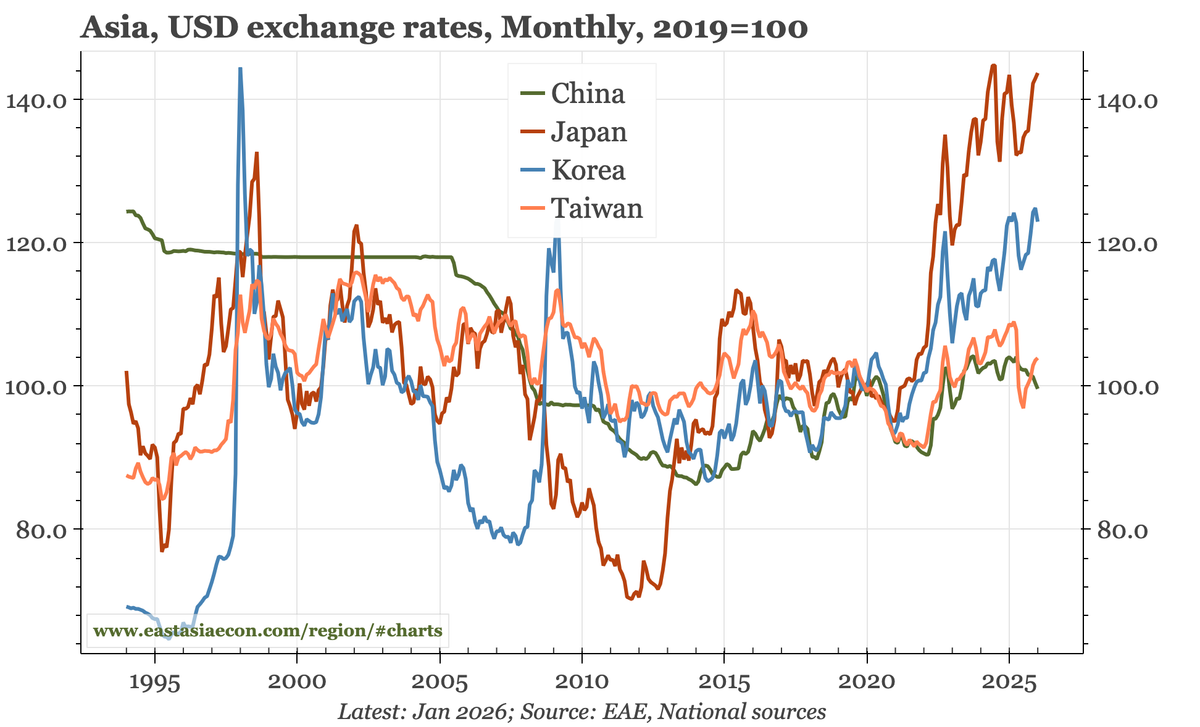

Whether judged against the USD, in real effective terms, or against the size of the external surpluses, the currencies of all four economies I look at are cheap.

That was also true 12M ago. That it didn't change in 2025 was because of tariffs worrying the BOJ and BOK, the CBC's persistent desire for stability, and continued deflation and monetary loosening in China.

Entering 2026, and things look different. Tariffs have been absorbed, and the manufacturing cycle is improving. Crazily strong growth in 2025 furthered the case that Taiwan's economy has entered a new era. China doesn't have inflation, but deflation has lessened and the pace of easing has slowed.

There are still factors specific to each economy to consider. For the JPY, it isn't helpful that any rate hike by the BOJ is accompanied by the assurance that "rates remain very negative in real terms". Korea's rising current account surplus has been offset by equity outflows that have risen even more quickly. In Taiwan, the possibility of a big change in the currency still has to be discounted by the fact that the exchange rate has now been rangebound for 30 years. And for China, a big move in the CNY is unlikely when the economy is still in deflation.

Even so, I think the likelihood of a region-wide trend of appreciation is growing.

Subscribers can read more here:

And the video is here: