Taiwan – August PMI

The PMI suggests there's a big industrial cycle slowdown in the works. That is important for Taiwan and the TWD. Because it suggests more downside risk for the regional export cycle, the weaker PMI also has implications for Korea and China.

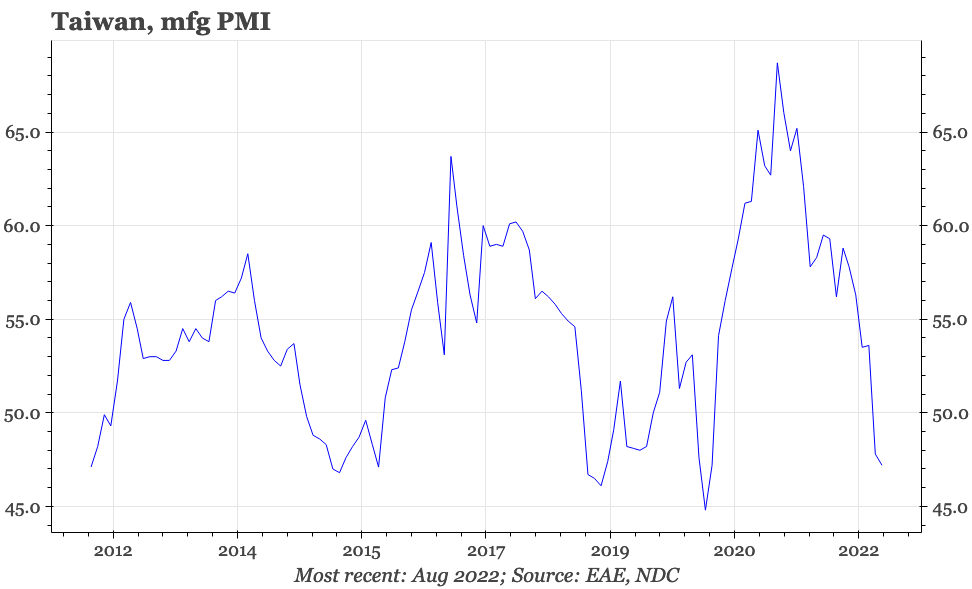

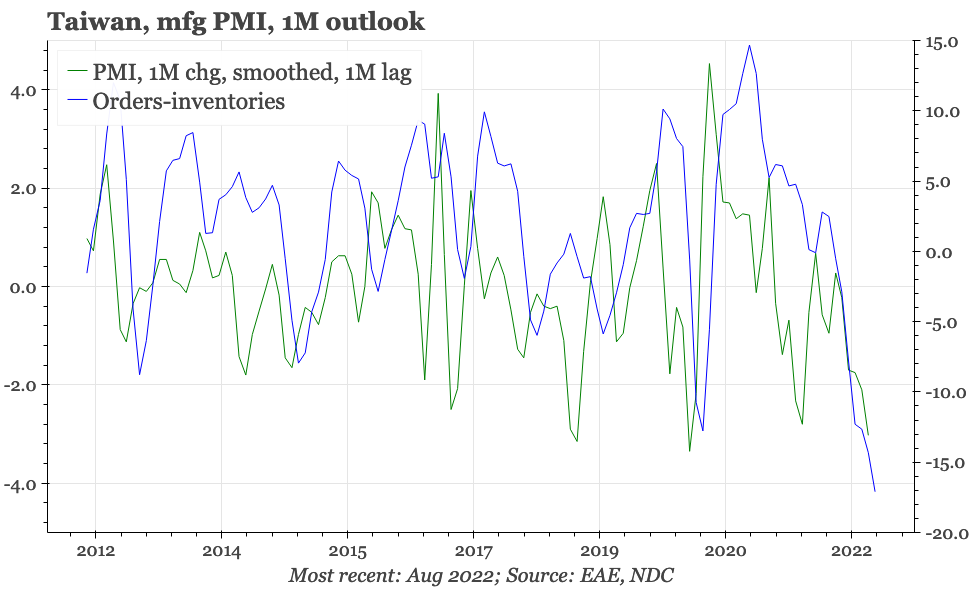

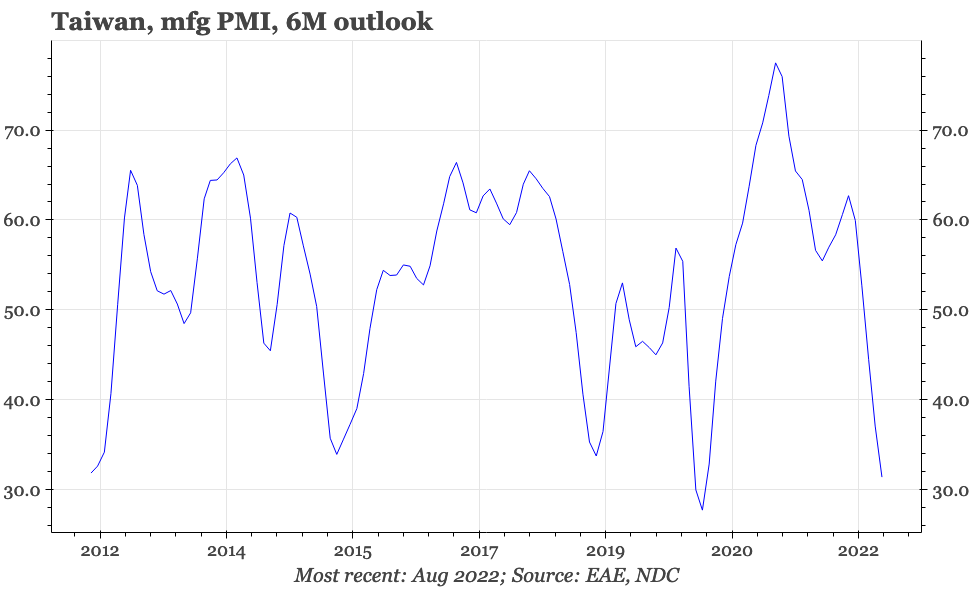

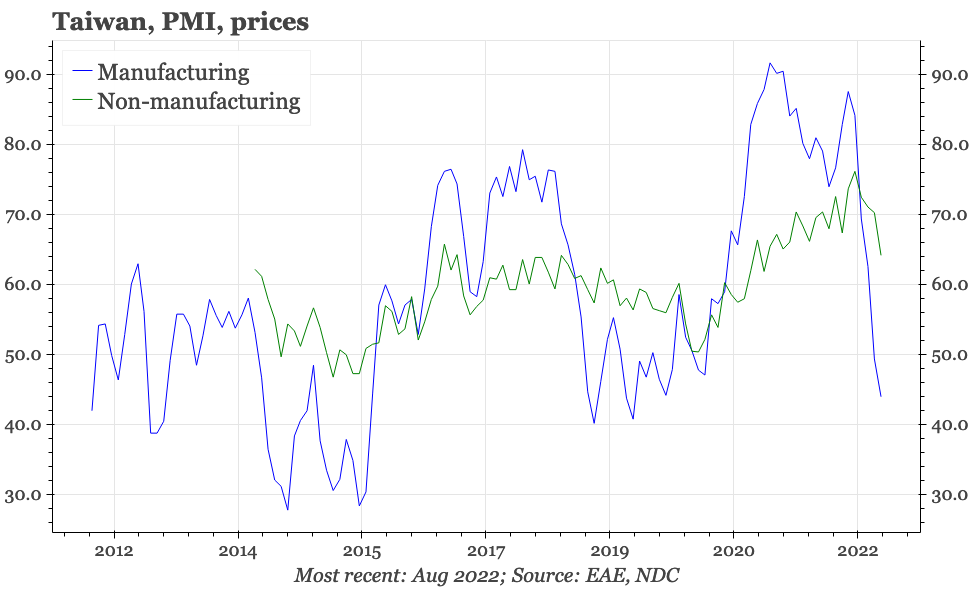

Taiwan's official manufacturing PMI fell again in August to 47.2. That's a modest fall from July's 47.8, but the details suggest the underlying picture is weaker. The 6M outlook fell to 28.3, which except for the collapse during global outbreak of 1H20 is the weakest since the series began to be collected in 2012. New orders ticked up, but new export orders fell, suggesting more downside to actual exports. The average orders:inventories ratio over the three months to August also fell to a record low, pointing to further downside risk for the headline PMI. Delivery times and order backlogs are falling fast. Customer inventories ticked down in August, but remain at a high level.

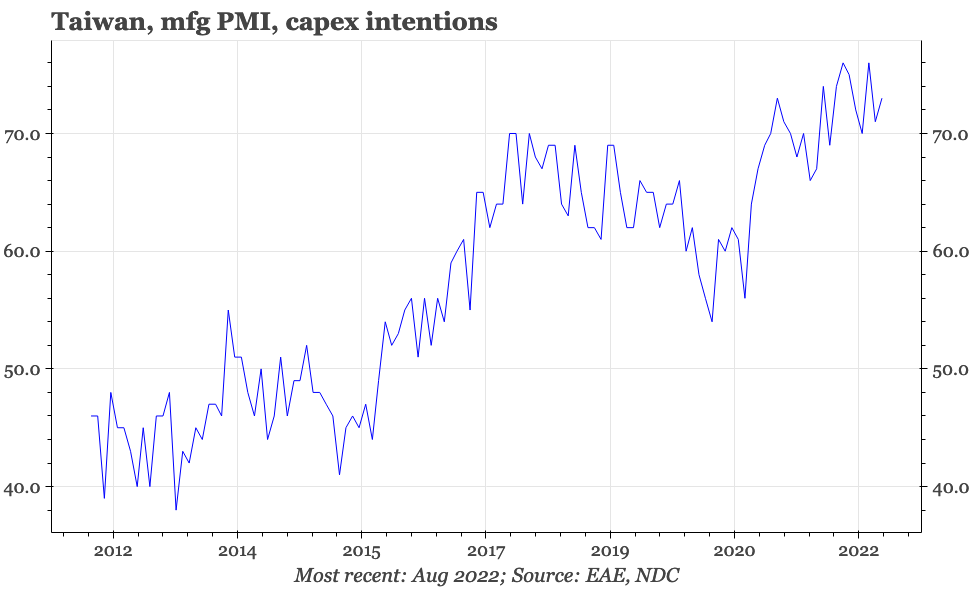

There are a couple of data points in the PMI that continue to look more positive. First, capex intentions remain elevated, though it would be surprising if that strength is maintained for much longer. Second, inflation pressure would seem to be receding fast, with prices in both the manufacturing and non-manufacturing PMIs falling again in August.

The cyclical slowdown and price trends put less pressure on the CBC to raise rates. However, without a closing of the nominal interest rate gap between Taiwan and the US, there is a risk of an intensification of the downwards pressure on the TWD that is already likely because of the slowdown in the export cycle.