The East Asia Economist

Since the pandemic began, productivity has probably increased more quickly in Taiwan than any other major economy. As a result, Taiwan isn't facing the higher inflation and rates being experienced elsewhere. Taiwan's competitiveness instead reinforces structural trends for a stronger TWD.

Taiwan – the world's best productivity story?

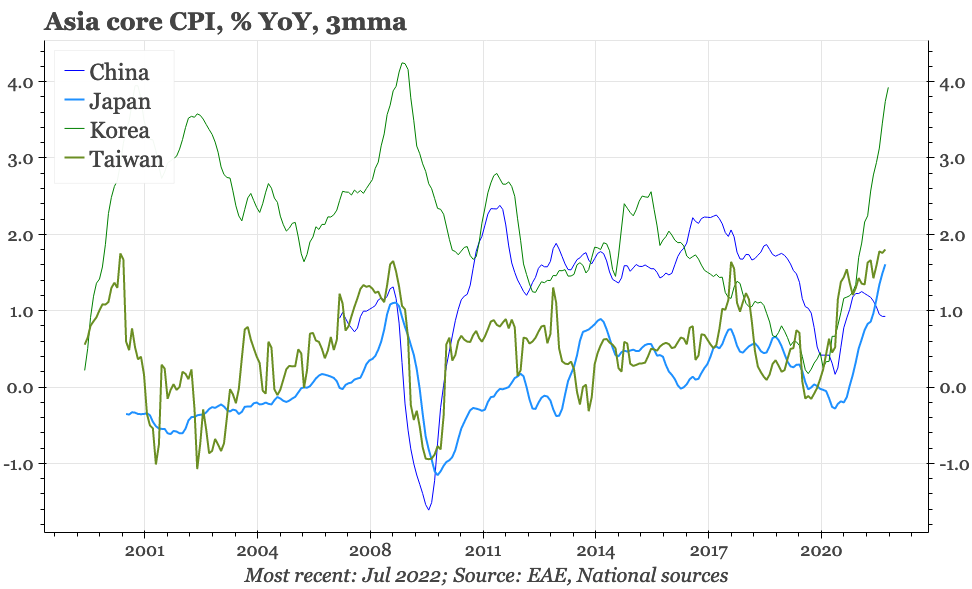

With the notable exception of Korea, East Asia hasn't yet been experiencing the surge in inflation that is being seen in much of the rest of the world. Some of this differentiation is cyclical, with China's growth for example being just too weak to generate much price pressure. But across the region, this undershooting of inflation also has structural roots. Japan's long struggles with deflation have been well-documented, but in terms of inflation Taiwan has been a global laggard too, with core CPI rising by an average of just 0.5% a year since 1998.

There are some reasons to think that these low inflation regimes are about to break. In Japan, the most obvious cause would be the rapid depreciation of the JPY in the context of the BOJ's reluctance to raise interest rates. In Taiwan, it is the surge in economic growth that has occurred since the pandemic. A simple analysis would suggest that the economy is operating above capacity – and that even before Covid-19 restrictions are fully liberalised.

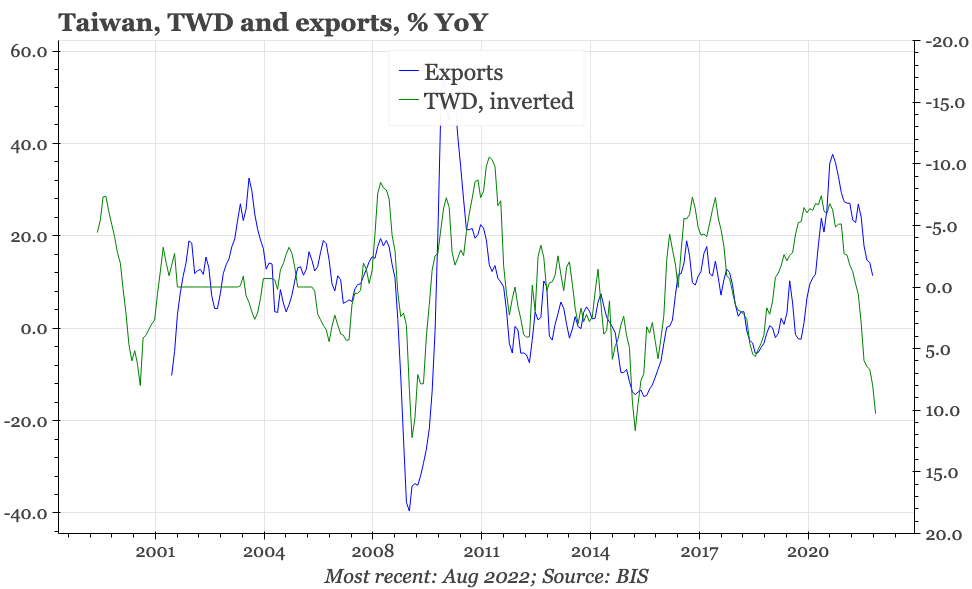

However, in Taiwan the acceleration in GDP growth, while impressive, hasn't been as big as the rise in labour productivity. That's because the expansion of the economy has been accompanied by a fall in employment. Rather than the beginnings of an inflation story and higher interest rates, the market implication of developments in Taiwan's economy since 2019 is a structurally stronger TWD.

Taiwan's pandemic boom

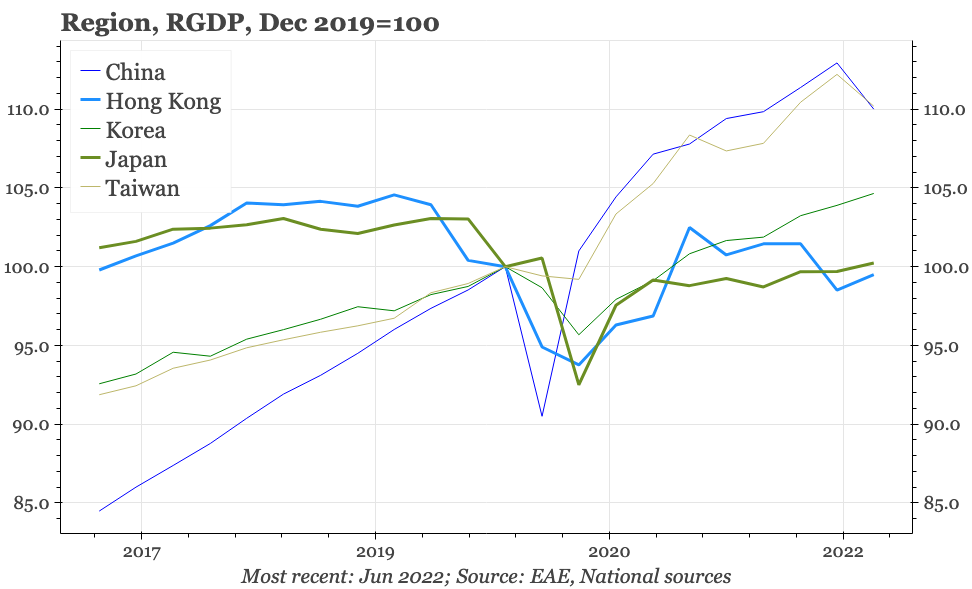

From the start of the pandemic until now, Taiwan's GDP growth rate has taken a clear step up. Previously, the economy was growing on a par with Korea's. Since 2020, Taiwan has leapt ahead, gaining a growth profile since then that is much more similar to that of China.

Taiwan's economy has been helped by the island's differentiated covid experience. Taiwan managed to suppress the death rate from Covid-19, but without having to resort to the formal lockdowns that caused the deep recessions (and surges in public sector borrowing) seen elsewhere. Taiwan did experience a technical recession in early 2020, but barely; even during the world's early struggles with Covid-19, Taiwan's economy continued to grow on an annual basis.

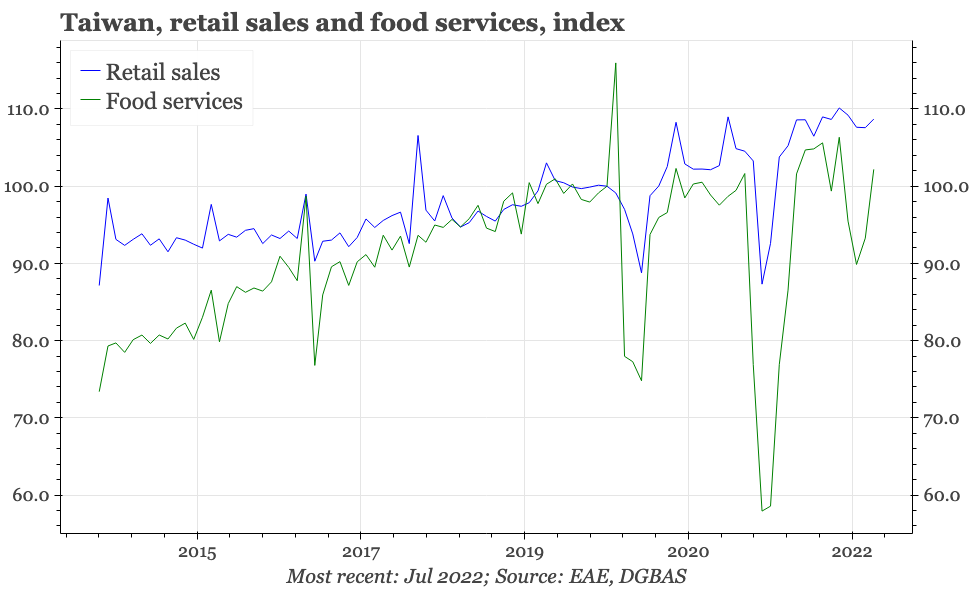

However, a key element of the government's ability to suppress Covid-19 domestically was the effective closure of the border, a measure which decimated tourism. And while Taiwan did avoid any real domestic outbreak of the pandemic in 2020, it did experience two waves of Covid-19 in 2021 and 2022, outbreaks that caused domestic retail activity to slump. Retail sales are now comfortably above pre-pandemic levels, but activity in food services has hardly grown in the last couple of years, and even now, visitor arrivals are running at just 5% of pre-pandemic levels.

A one sector economy

So, while Taiwan's success in avoiding a lot of the covid chaos seen elsewhere has been admirable, and has put a floor under the economy, it can't explain the acceleration in Taiwan's growth. Rather, the driver has been the global boom in tech during the pandemic, particularly the surge in demand for semiconductors. That was driven by the work-from-home trend, and the replacement of services spending with purchases of consumer durables. That has triggered both a surge in Taiwan's exports, and an accompanying big rise in private sector capex spending.

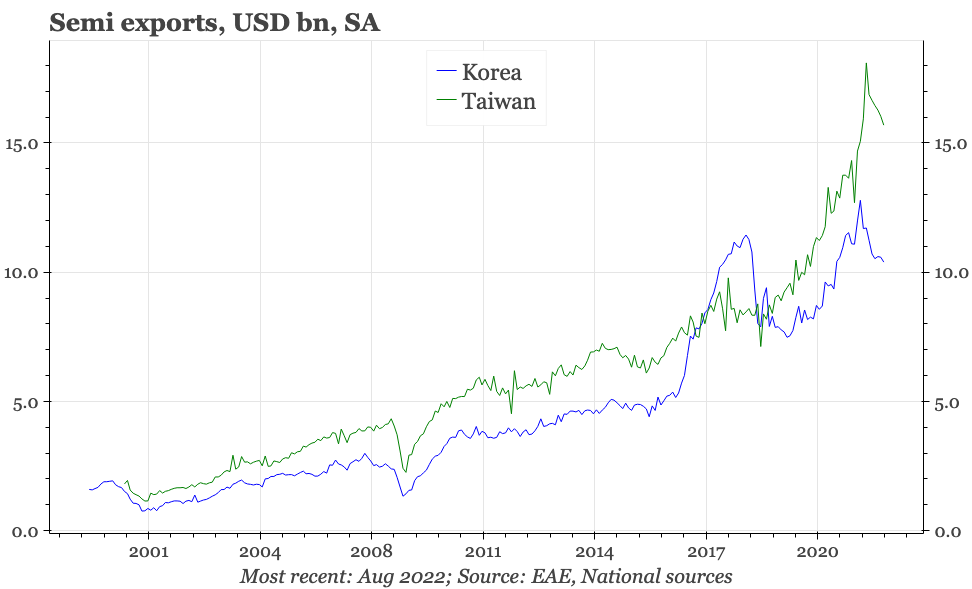

Korea was a beneficiary of these global trends too, but the impact was magnified in Taiwan. That's because tech is more important to Taiwan's economy – even before Covid-19, semiconductors accounted for around one-third of Taiwan's exports, compared with around 20% in Korea. The particular nature of the semiconductor cycle of the last two years, which has been led by foundry demand, has also played to Taiwan's strengths. Taiwan's TSMC is the clear global leader in foundry, while the Korean firms Samsung and SK Hynix are stronger in memory.

As a result of this backdrop, Taiwan's manufacturing output is now 20% bigger than it was before 2020, compared with the 10% rise recorded in Korea. From the end of 2019 to the apparent peak in June this year, the USD value of Taiwan's exports grew 50%, a more pronounced rise than at any other time at least since the 1990s.

Output up, employment down

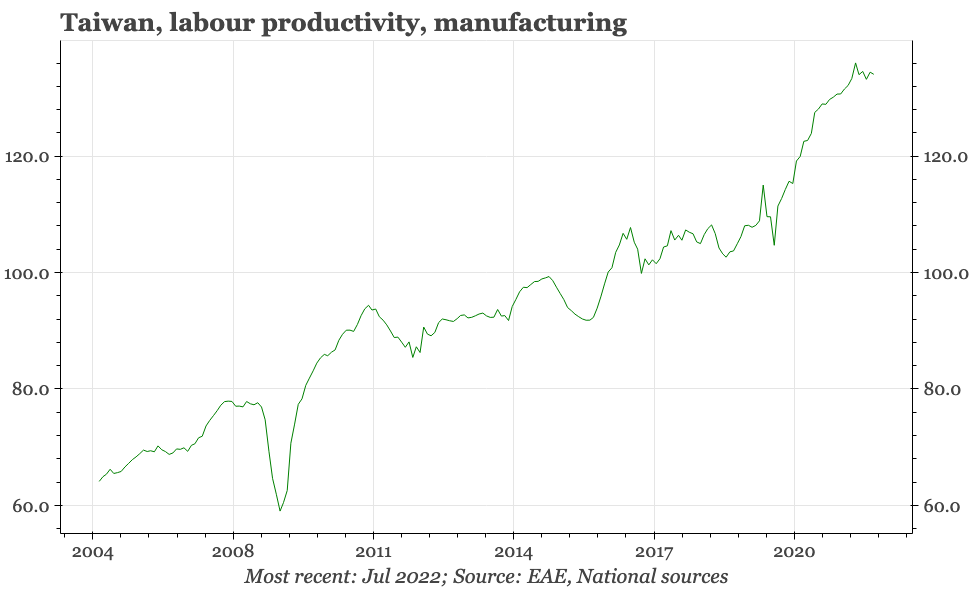

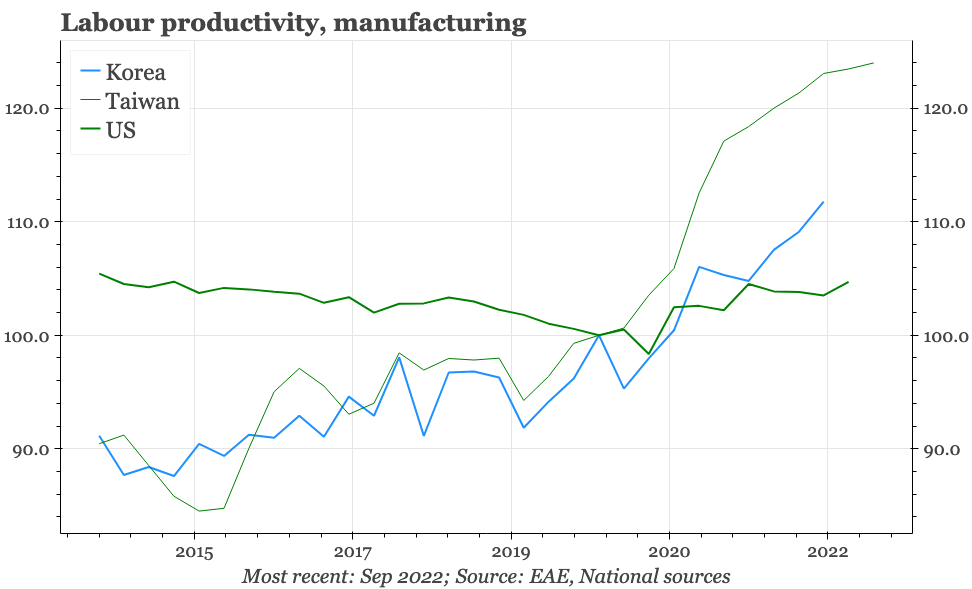

This is impressive, but not without parallel: in fact, export growth has been even stronger in China. Where Taiwan stands out more is the surge in labour productivity that has accompanied this rise in output. While manufacturing production has boomed in the last couple of years, the manufacturing workforce has shrunk. There has been a rise in average working hours per worker, but even so, the total labour input in manufacturing has at best been going sideways. With manufacturing output rising so much, the result has been a real leap in labour productivity.

Official data for productivity in Taiwan are only available for manufacturing, and it is highly unlikely that there has been such a rise in efficiency in non-manufacturing. The domestic economy is less exposed to competition from the rest of the world, and even without the Covid-19 disruption, would have lacked the massive demand-stimulus from the global tech cycle that has critical in manufacturing.

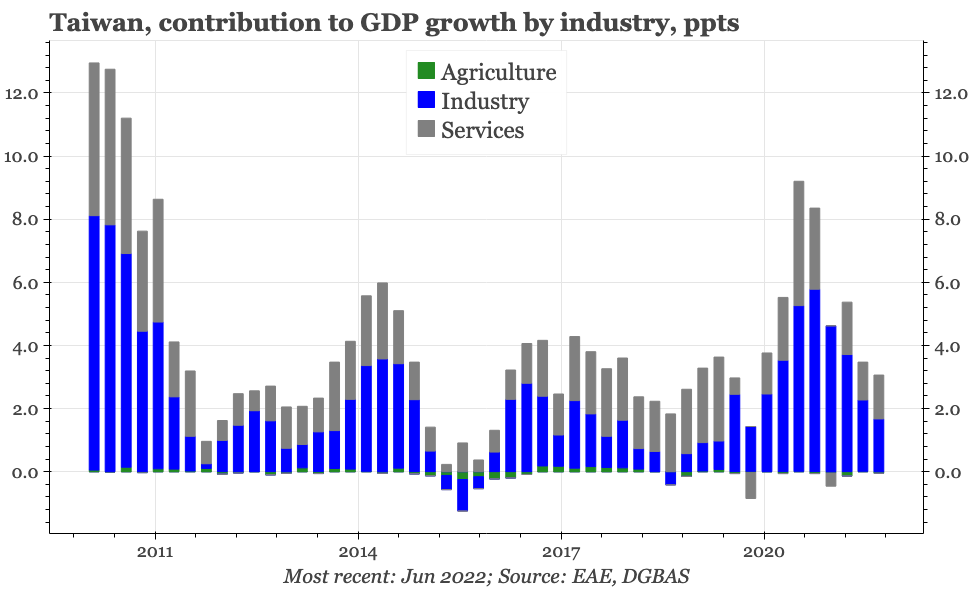

Still, the rise in manufacturing productivity is big enough to be noteworthy on its own. It is also of sufficient size to impact the overall economy. Manufacturing isn't dominant in the economy, but its share of GDP, at more than 30%, is big compared with other developed economies. Moreover, with industrial output rising so strongly, that weight of manufacturing has been growing in the last couple of years.

Manufacturing outweighs services

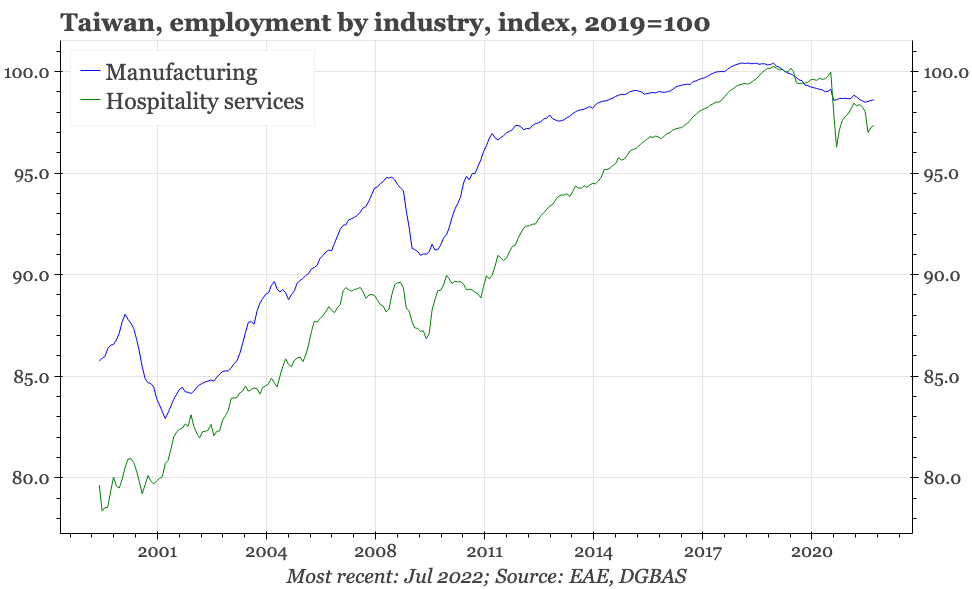

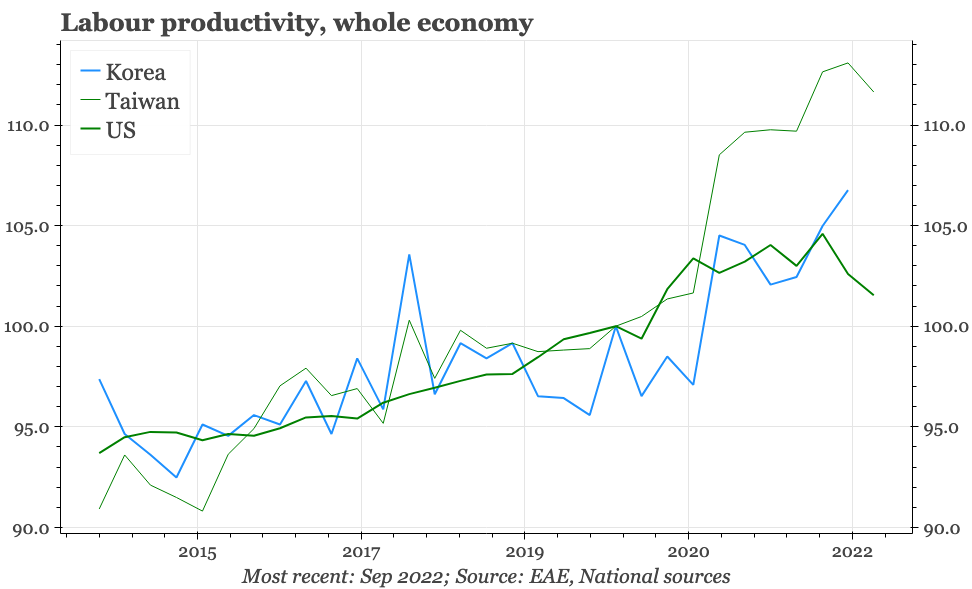

All told, and manufacturing has generated two-thirds of the growth in Taiwan's total economy recorded since the pandemic began. At the same time, while manufacturing employment has fallen, the decline in the number of jobs in the services sector has been even bigger.

This loss of services jobs is related to the depression of domestic activity caused by Covid-19. That is certainly an unfortunate development for the individuals involved, and is a phenomenon that deserves a policy response. But again, from the simple perspective of GDP, the loss has been more than compensated by the faster growth of manufacturing, with the result that it isn't just manufacturing labour productivity that has risen rapidly in the last couple of years; overall labour productivity looks to have surged too.

Cyclical slowdown

This backdrop of rising efficiency gives manufacturers room to increase wages. And that does seem to be happening: regular wage growth over the last three years in manufacturing has been the fastest since the early 2000s. That rise looks to be part of a secular trend: after slowing quite sharply from double-digit rates in the 1990s to below 2% YoY for much of the 2000s, the rate of increase in manufacturing wages has been incrementally accelerating since.

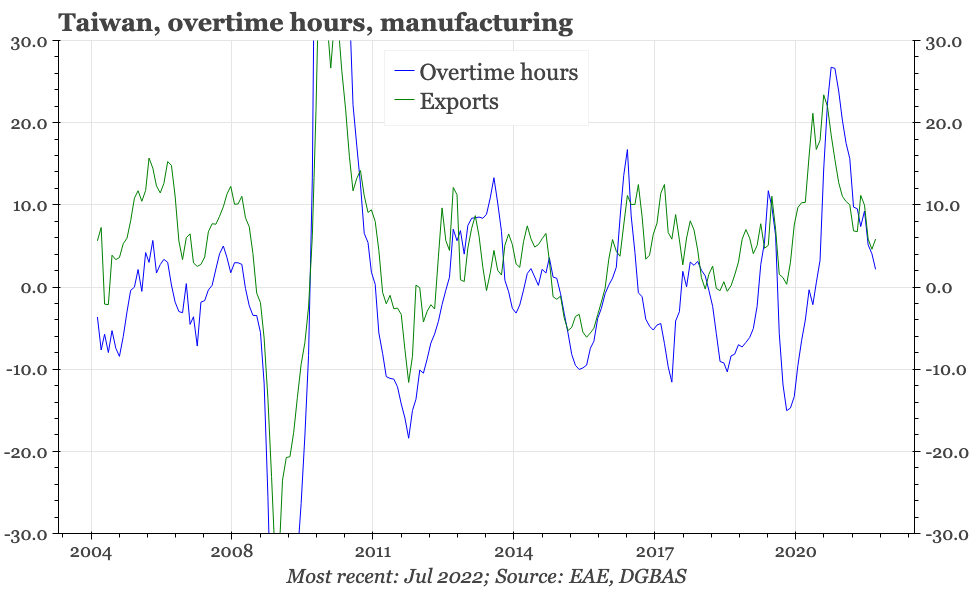

However, wage growth still isn't rapid. Even after the manufacturing boom of the last couple of years, wages are still only rising by 3.5% YoY – though, in contrast to many other economies, that is quicker than Taiwan's rate of CPI inflation. Moreover, even if the structural direction is higher, there is still a cycle around that. And right now, the PMI and other indicators are pointing to a sharp slowdown in global tech demand, which suggests manufacturing wage growth will be slowing. In an early sign of a turn in the labour market, overtime hours in manufacturing have already stopped growing.

The peaking of overtime suggests the labour market at the margin is starting to loosen up, which is important when the economic boom of the last couple of years never made it very tight. The unemployment rate now stands at 3.7%, quite similar to where it has been since 2015, and lower than it was for much of the 15 years before that. But that is still far from the sub-3% rate that was usual before 2000.

Currency, not rates

There is a risk that any loosening of labour market conditions in manufacturing employment from here is offset by a tightening on the services side as the economy normalises after covid. Broadly speaking, Taiwan's Covid-19 strategy has been to keep the virus out of the country until a critical mass of the population is vaccinated – a process that took until early 2022 – and then open up – which is what is happening now. Quarantine requirements have been cut from 14 days to three, and are likely to be liberalised further, and border restrictions are being wound back.

However, to impact inflation, the rise in services employment would need to be big enough to offset any slackening of the labour market stemming from the slowdown in manufacturing, as well as the rise in overall labour productivity in the economy. Such a surge in services employment seems unlikely.

So, it doesn't feel like Taiwan is facing higher inflation and sharp rises in interest rates. Instead, productivity developments in Taiwan's economy since the pandemic have reinforced Taiwan's underlying competitiveness, giving support for the external surplus. That isn't enough to prevent the TWD slipping against the USD as the Fed hikes and the manufacturing cycle slows. But it does suggest that the TWD shouldn't fall as much as other currencies, and when the cycle turns again, that the TWD will continue to face structural appreciation pressure.