The China Diviner

Beijing is relying on infrastructure for growth. But with property in recession, exports slowing, and consumption dampened by Covid, the growth hole that needs to be filled feels too large. Without policies that support these other sectors, the current cyclical recovery seems unlikely to persist.

Short cycle

Needless to say, there's not much economic activity when a city is locked down. Equally obviously, there's a natural bounce back in activity when lockdowns end. That can be seen in the economic recovery in China over the last few weeks. The PMIs were up in June, consumer confidence has improved, and passenger numbers on subway systems have risen.

Clearly, the authorities want this recovery to continue. Xi Jinping has talked about the need for “more forceful measures” to bolster growth; Li Keqiang and the State Council have launched a package of 33 stimulus measures; the Ministry of Finance has pressured local governments to use fulfil their full-year special bond quotas by the end of June; and there's been a flurry of measures aimed at boosting end-user demand in the property market.

These policies are having some impact. Credit growth was strong in June, with the extra local government bond issuance playing a big role. The PBC this week said actual interest rates for corporates in Q2 fell further to 4.2%. Property transactions have been picking up in recent weeks, and property price momentum has turned up. At the PBC's quarterly press conference this week, officials from the central bank said that the turn in the economy since May had “exceeded expectations”.

However, having some impact is not the same as gaining traction. Lockdown easing and bond issuance aside, it doesn't feel like the underlying cycle is getting ready to accelerate. Since September last year, the government have been saying that Evergrande is a particular case, and that an "excessive" rise in risk aversion towards real estate in financial markets would prove temporary. And yet in the financial markets there's no sign of home builders finding a floor, with debt and equities for the sector falling last week to yet new lows. Moreover, within the sector there's continuing signs of contagion. The authorities perhaps never liked Evergrande, but now there's a risk that the likes of Vanke, which in many ways had been a model developer in official eyes, will be dragged into the void.

The government's strategy for recovery seems to assume that a combination of a corporate sector boosted by cuts in red tape and taxes, coupled with a vigorous programme of infrastructure development, can offset all the problems in real estate. But this feels optimistic. Last week's monetary data showed that companies weren't shifting money out of demand deposits, suggesting that they aren't yet optimistic about the outlook. More broadly, in the last twenty years the cycle has been determined by real estate and exports; the role of infrastructure hasn't been decisive.

Given all this, it feels that the current cyclical recovery needs at least two new initiatives to be sustained. First, something that finally puts a floor under the developer sector. Second, more direct policy support for the household sector that boosts consumption, and thus provides a new source of demand for the corporate sector. Without such shifts, there is a growing risk that China's recovery out of the lockdowns won't be sustained, and that later in Q3 growth momentum will be slowing once again.

Markets and money

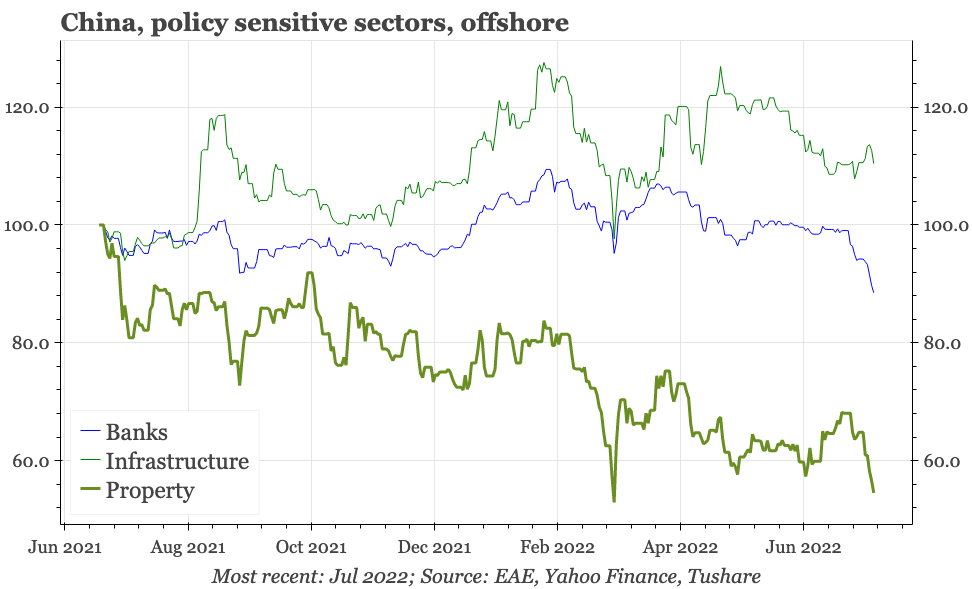

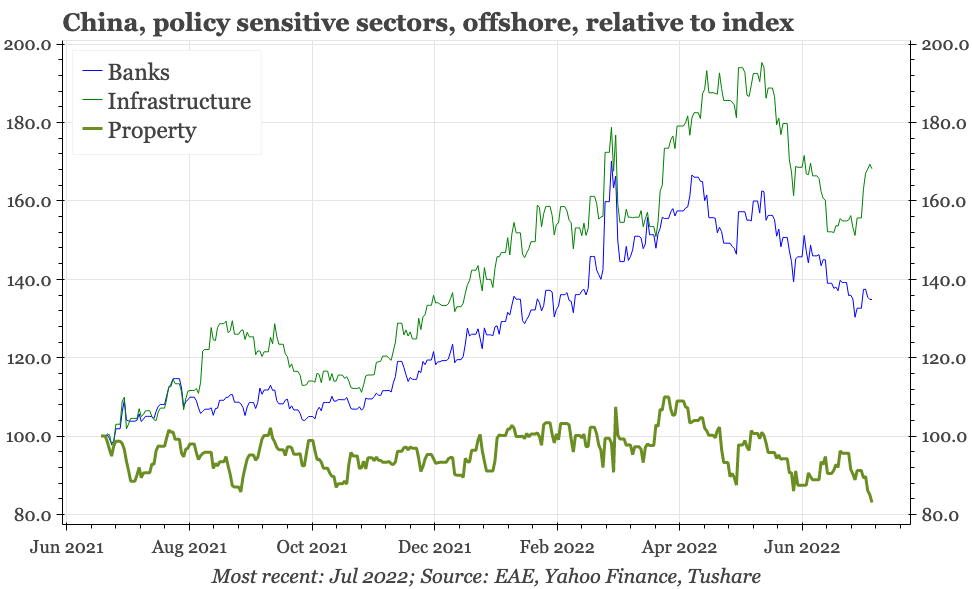

Historically, the three biggest sectors that officials use to influence growth are banks, property, and infrastructure. The reasons are obvious. The banks play a critical role in pushing money into the economy, often in China acting in a countercyclical way that isn't usual in banking systems globally. This money ends up financing real estate and infrastructure projects, favoured by officials because these sectors dominate fixed investment in the country.

The equity market doesn't suggest much life in any of these three sectors. For property, that isn't new – the sector had already fallen by more than 30% in 2021. But it is important that there is still no stabilisation. Indeed, equity and debt markets are indicating that the pain in the sector is getting ever more intense, with both falling to yet new lows last week; MSCI China real estate is now down a further 25% this year. That is quite striking given officials have been publicly calling for stability in real estate for more than nine months.

Bank equities have also been soft. There was a sell-off last week, on the flurry of news reports of buyers of properties where construction has stalled refusing to pay back mortgages. But bank equities have been weak since the beginning of July, which is a warning sign for the cycle. Moreover, within the banking sector small banks have been underperforming, which at times in the past has indicated a turn down in the credit multiplier.

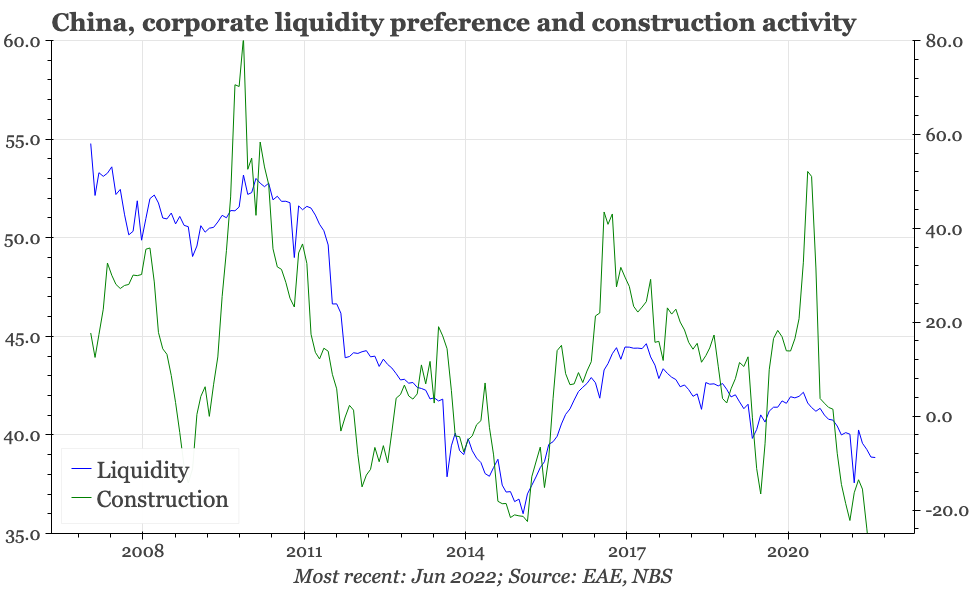

Deposit data in this week's June monetary release weren't encouraging for the cycle either, showing no reversal of the recent fall in the proportion of corporate savings held on demand. With the implication being that companies are instead continuing to lock up money in time deposits, it doesn't seem they feel the need to be holding cash on hand. That in turn suggests they aren't thinking of making new investments or increasing staff numbers.

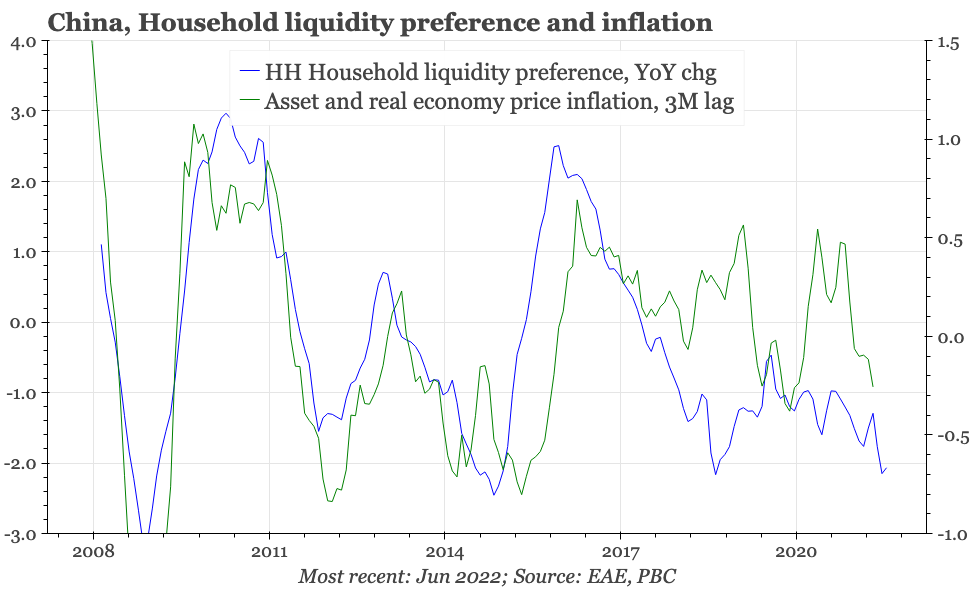

That might be reading too much into one indicator, particularly when the quality of the underlying data isn't particularly strong. Still, it is true that previous upcycles in the Chinese economy have been accompanied by a rise in this measure of liquidity preference.

We'll find out a bit more in a few days time when the PBC releases the more detailed monetary data for June, which will include demand deposits of households. That will be an important datapoint in itself, with liquidity preference of households in recent months if anything looking even more bearish than for corporates. In the past, this measure of the savings behaviour of households has been a useful indicator for assessing the likely path for inflation, and for some months now has been flashing warning signs that China is headed for deflation. Such a development wouldn't be supportive for activity.

Real economy sectors

It is perhaps conceivable that none of this matters, and that a vigorous attempt to lift infrastructure will be sufficient to lift the overall economy. We know from official rhetoric that the government continues to think highly of infrastructure development as a driver of economic growth, and Li Keqiang's 33-part package includes new rail and road projects. At their press conference this week, PBC officials again stressed that infrastructure spending was an important way to stabilise growth.

It has always been difficult to find data that reliably show just how much infrastructure development is happening at any one time. Official Fixed Asset Investment data show transport infrastructure investment grew by less than 10% YoY in the first six months of the year. That should change, with the State Council announcing additional credit facilities for infrastructure development of around CNY1trn in the last few weeks.

Equity prices of old-economy infrastructure companies still aren't yet pricing in any dramatic upturn. But the government's definition of infrastructure these days is wider than just roads and bridges, incorporating lots of new economy gizmos, so looking at the likes of China Railway Construction to gauge the strength of the official push may no longer sufficient.

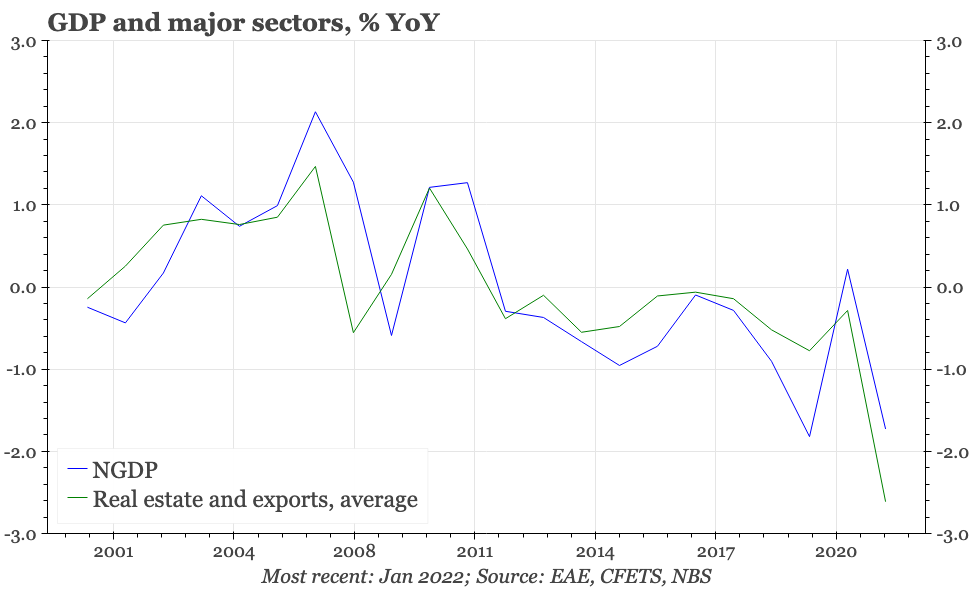

However, when looking at previous cycles, it is clear that the infrastructure push is going to have to be very big indeed to single-handedly boost the economy. That's because property and exports face significant headwinds, and in the last twenty years, regardless of what is happening with infrastructure, all upturns in China's economy have been accompanied by stronger growth in at least one of these two other sectors.

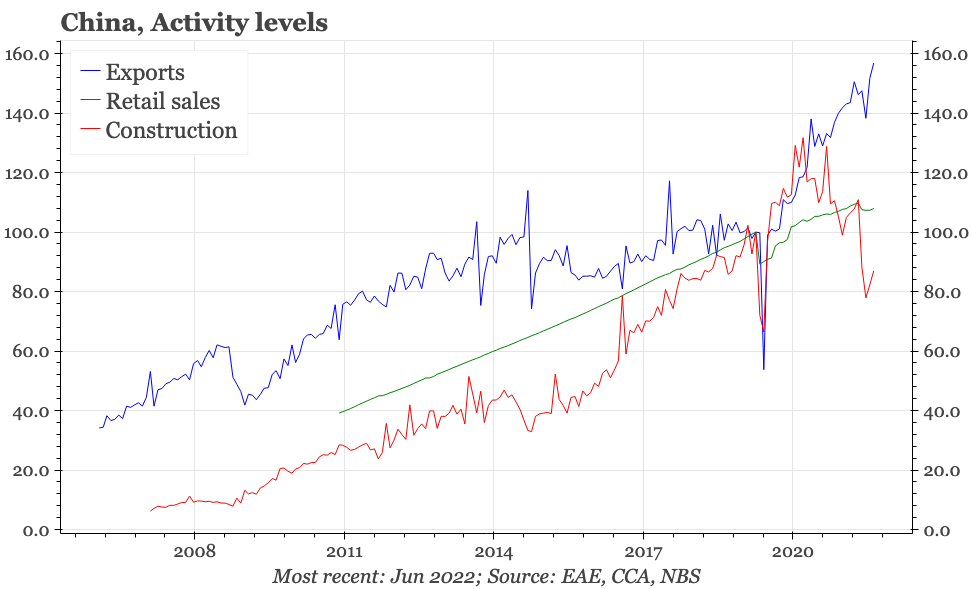

The challenges in property are most acute, with real estate construction in June contracting 40% YoY. End-user demand has shown some signs of recovery: property sales fell a bit less quickly in June, and official data show property prices stabilising. But the continued financial crisis enveloping the developer sector doesn't suggest that property construction is going to respond even if the recovery on the demand side continues. After their near-death experience of the last few months, if companies do start seeing higher revenues, they are more likely to use the money to fortify their balance sheets. It is highly probable that the construction contracts in 2022 as a whole.

Real estate has been in recession for some time now, with the impact on the overall economy offset by remarkable strength in exports. While property construction is down 30% from the peak, nominal exports are now 60% higher than they were pre-covid. China's global market share has surged 2ppts since the pandemic started.

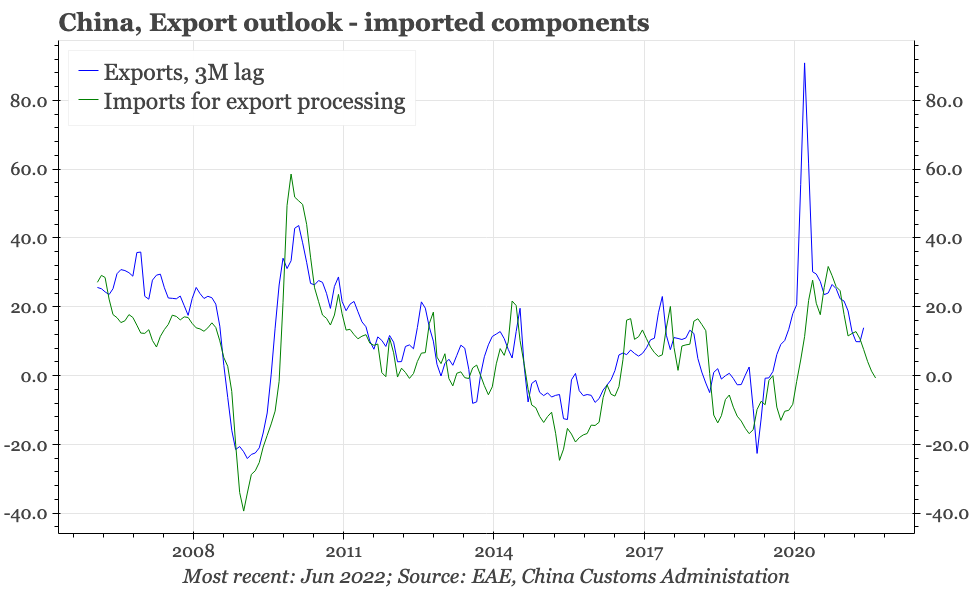

However, growth in exports has been slowing in recent months, and leading indicators suggest shipments will be flat-lining by Q4. Indicators for the broader regional export cycle are suggesting the landing could be harder, and a fall in Chinese exports would feel consistent with the normalisation of the pandemic-driven swing in DM consumer demand away from services to goods. In any case, even if exports prove resilient, it is highly unlikely that there will be a repeat of the sort of surge seen in 2020-21, a surge which for the macroeconomy was important in offsetting the contraction in construction.

Outlook

One of the difficulties in forecasting China's economy is that leading indicators that were useful in previous cycles don't necessarily prove accurate in future ones. That is a particular risk with the financial side of the economy, where regulation has cut off some of the transmission channels that were alive during and immediately after the big downturn of 2008.

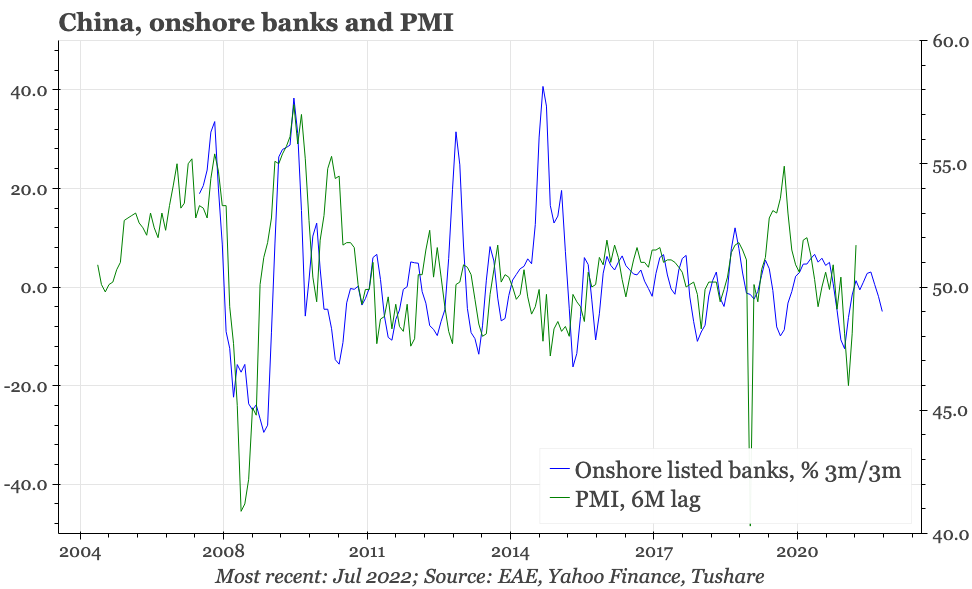

With these regulations, the government has sought to turn the financial free-for-all at the local level into something much more closely managed by the central authorities, and in so doing, draw a cleaner delineation between the fiscal and monetary spheres. If these changes work, the banking sector will be playing less of a role in directing liquidity. Along with investor wariness of rising non-performing loans, this is a reason that listed bank share prices might be losing usefulness as an indicator for the cycle.

So, despite the analysis here, is it perhaps conceivable that an enormous government-financed infrastructure push will propel a cyclical recovery that persists into 2023. It does though feel that this is unlikely. The property sector is in a deep recession, export growth is slowing, consumption continues to be dampened by Covid-19 policies, and there are some signs of deflation risks growing. That all leaves a very big hole for infrastructure to fill. As a result, without policies that offer some support to these other sectors, it feels unlikely that the current cyclical recovery can persist.