The China Diviner

Chinese exports have boomed since 2019. That boom isn't (yet) turning to bust, but it is likely ending. That's a big issue when the rest of the economy is so weak. Even without a new covid outbreak, there's a rising risk of a real growth accident in 2H22.

The end of the export boom

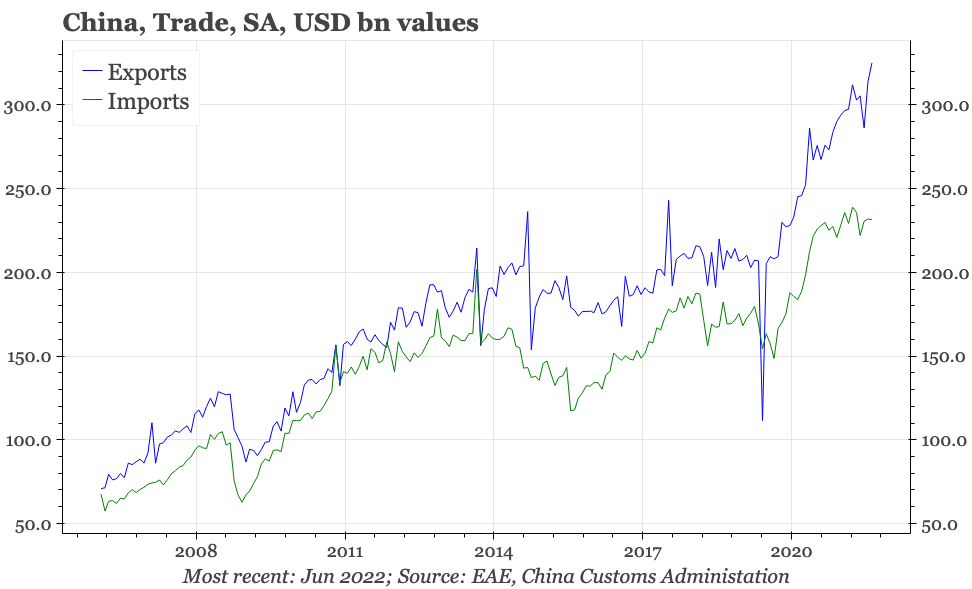

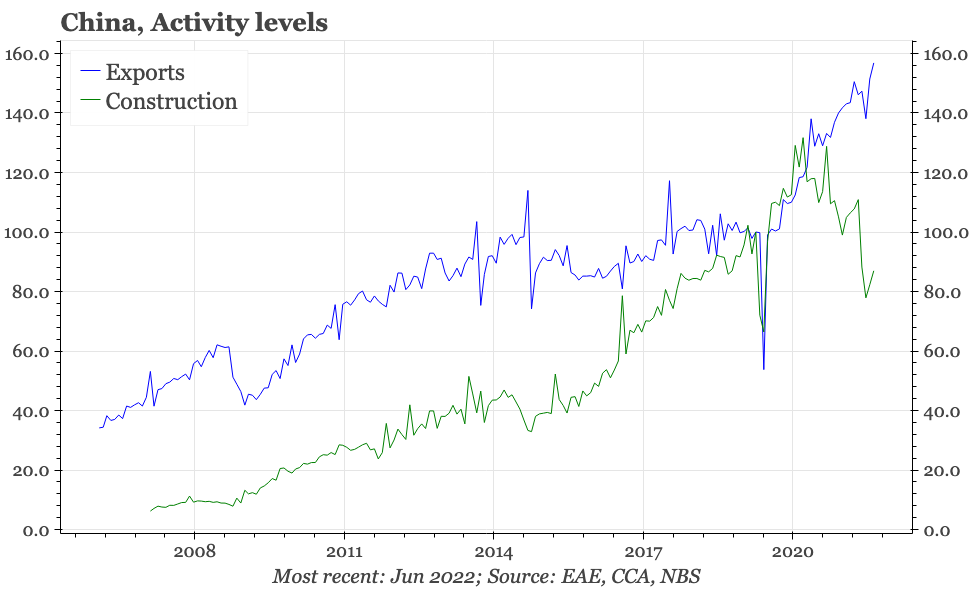

Even by China's standards, the 60% surge in exports since December 2019 is remarkable. It is the fastest rate of increase in any other 30-month period since 2014. The average MoM growth in exports since the pandemic started has been quicker than at any time in recent history, including the post-WTO entry globalisation boom, and the recovery in trade that followed the collapse of Lehman. This rapid rise has helped boost the trade surplus to an all-time high, in turn supporting the current account.

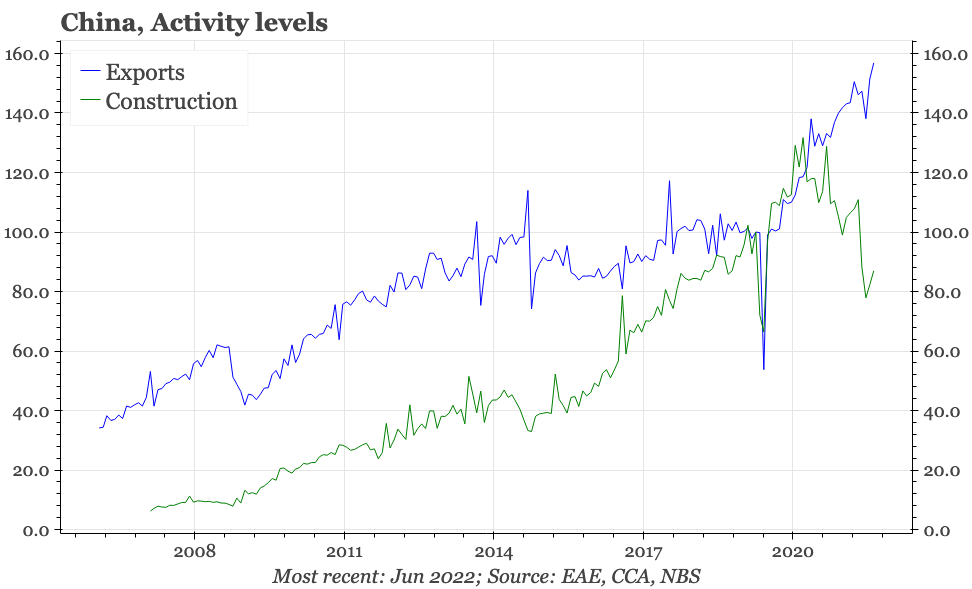

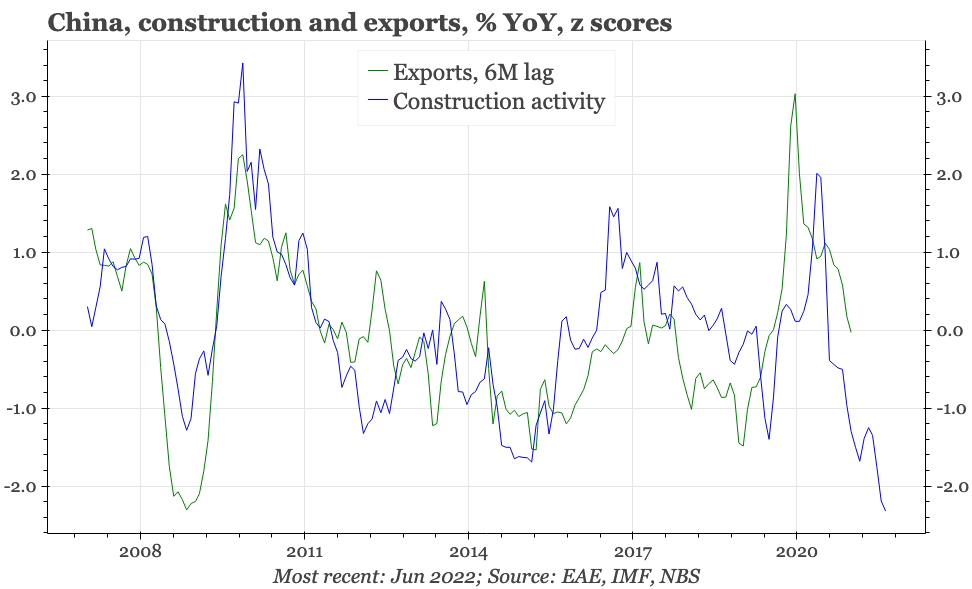

The boom in exports can't carry on forever, and there are, in fact, strong signs it is now ending. Boom doesn't (yet) look to be turning to bust, but it doesn't need to; a slowdown in export growth will be enough to affect the overall cyclical picture. That's because the surge in exports that started in 2020 has helped offset the impact on overall growth of the policy-induced collapse of domestic construction activity. With the contribution from exports now looking likely to turn down, the economy won't be growing at all if property continues to contract.

There was a further incremental softening of language towards property at this week's Politburo meeting. However, this latest shift remained gradual, and the cautious changes made so far haven't been enough to put a floor under real estate. Perhaps the government has a new policy response that it is just about to reveal. But until and unless something does change, the softening of exports will make China's already weak cycle even worse. In fact, it feels like there is a rising risk of a real growth accident in the next few months.

This cyclical picture suggests lower interest rates and, with rates in the US still high, a weaker CNY. That said, over the medium term for the currency the pressure isn't all down: given the rise in China's global market share in the last few years, it is difficult to argue that China has a competitiveness problem that needs a weaker CNY. The cyclical picture is bad news for equities in general, but the competitive strengths that been on show in the export sector should make some individual companies attractive.

Export boom

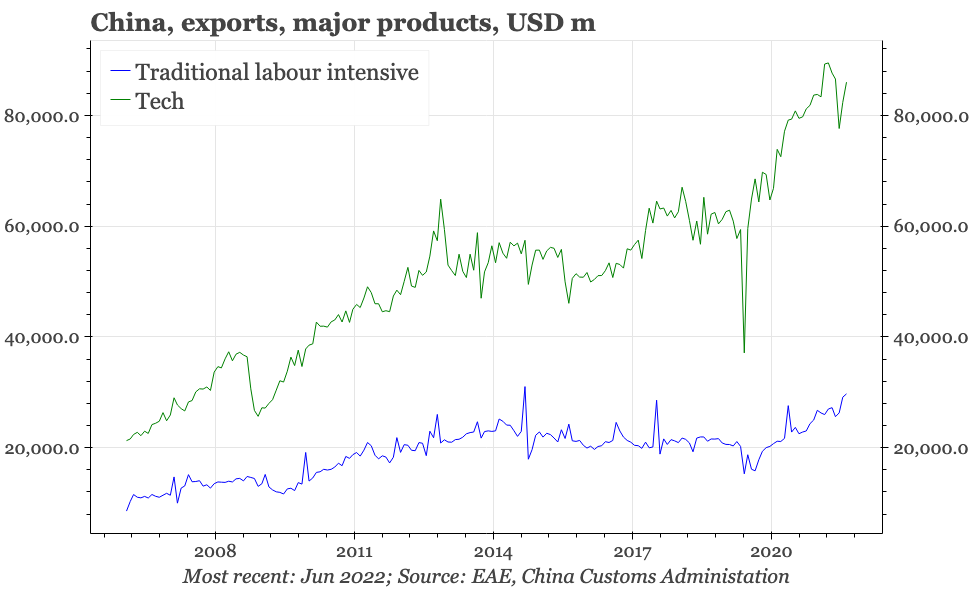

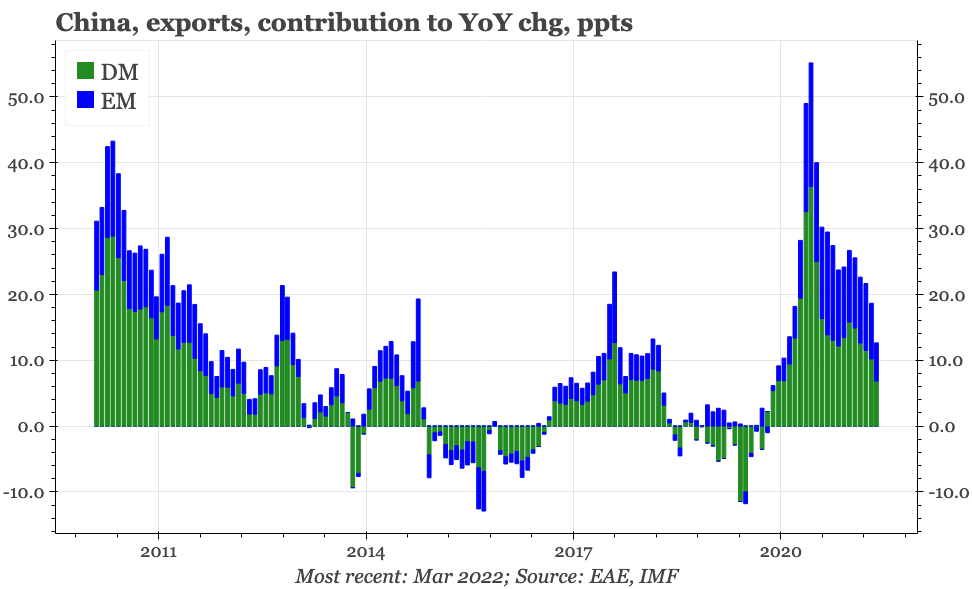

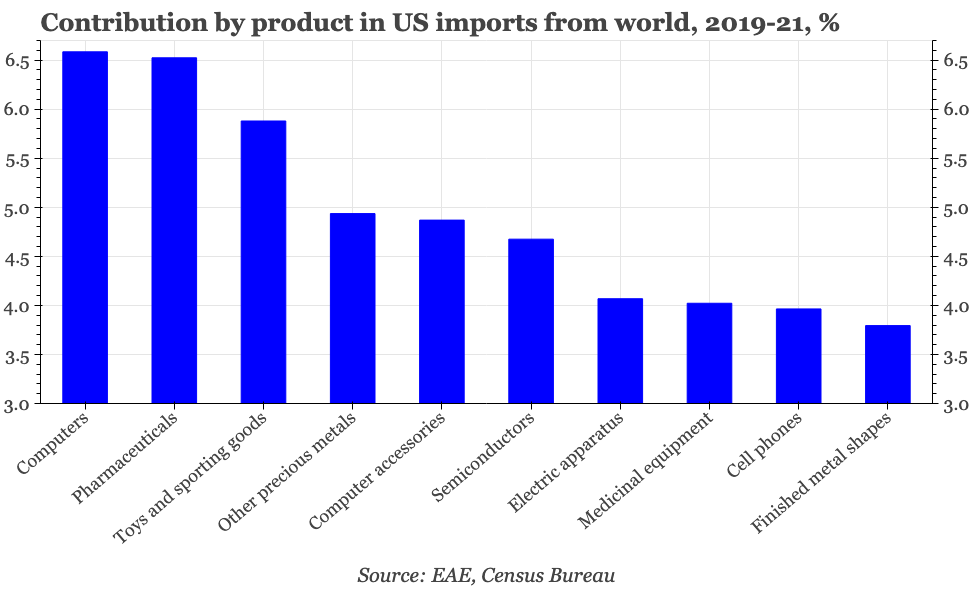

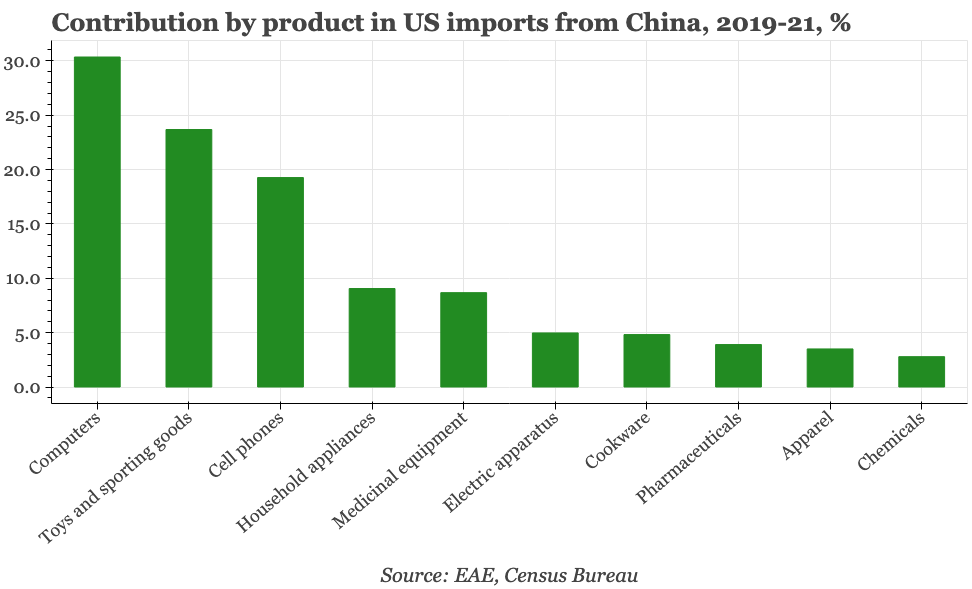

The rise in China's exports hasn't just been strong at a headline level; it has also been broad-based, in terms of both goods and markets. One of the first drivers was exports of medical equipment, though these only account for a small proportion of China's total exports. It is shipments of technology products that have been the biggest driver of the overall rise in exports since 2019. Sales of computers have risen by 70% since the end of 2019, and official data show “hi-tech” products have accounted for almost 25% of the total growth in exports of the last 30 months.

Sales of traditional labour-intensive products like furniture and shoes have also jumped by 40% since the pandemic started, the fastest rate of growth since 2014. China's exports of cars have surged 130%. That was from a very low base, and in terms of overall exports, autos are currently no more important than shipments of medical equipment. But with China's globally leading position in electric vehicles, this recent rise is likely the beginning of a multi-year trend.

The rise in exports has been led by sales to richer country economies. IMF data show that Chinese exports to advanced economies (through March 2022) have increased by almost 50% since just before the pandemic started. Sales to emerging markets though are also up strongly, and in recent months have been just as important to Chinese export growth as shipments to the likes of the US. Moreover, in both DM and EM, Chinese export growth has been the result of both increases in end-user demand, but also market share gains.

Supply side reforms

This isn't what was supposed to happen. Before the pandemic began, it was easy to think that the best days for Chinese exports were long gone: labour costs were rising, the CNY wasn't so cheap any more, there was pressure for supply chain readjustment, and, last but not least, the US had imposed broad-based tariffs on Chinese shipments.

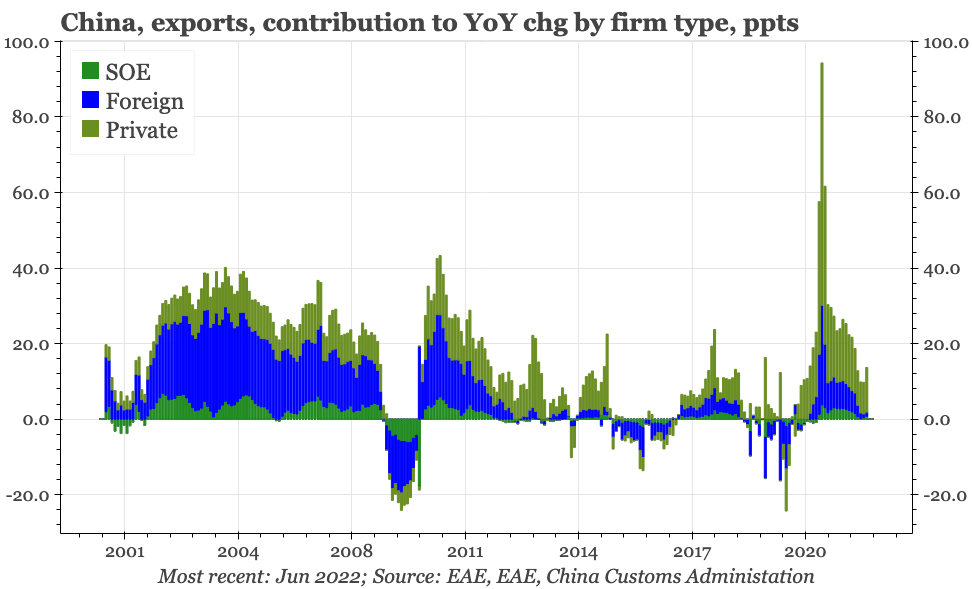

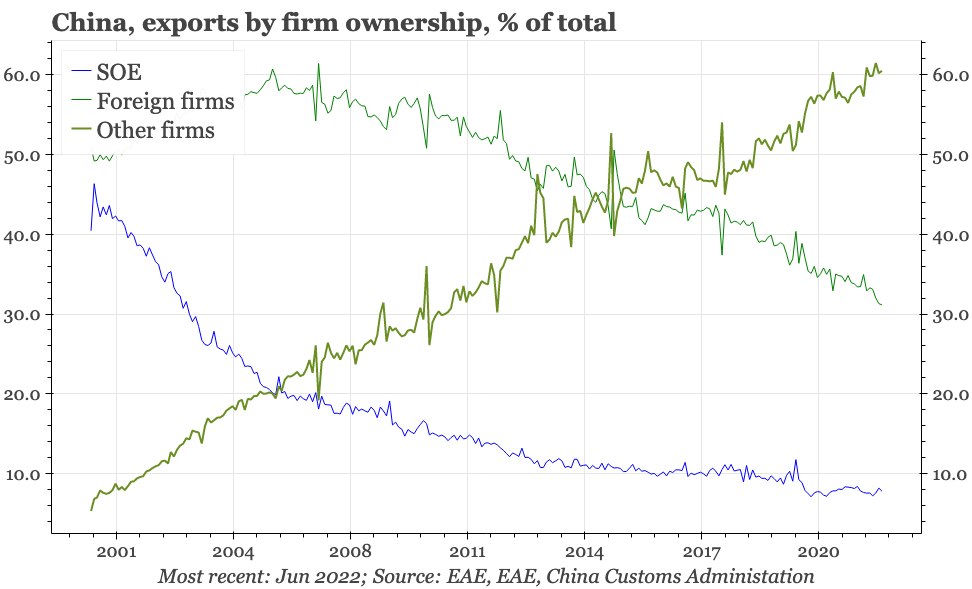

Detailed data do show there has been some supply chain adjustment. Whereas foreign-owned factories in China drove the rise in exports in the years after WTO entry, that has not been the case in the pandemic boom. However, the decline in the importance of foreign exporters predates the supply chain concerns of recent years: the foreign firm share of Chinese exports peaked back in 2006. Domestic state-owned firms stopped playing a significant role in Chinese exports in the early 2000s. So, the driver of exports in recent years has been Chinese private firms. They now account for almost 60% of exports from China, and have generated 80% of the total rise in overseas shipments in the last 30 months.

That's a big gain. It doesn't negate the narrative of “the state enters, the private sector recedes” that has been a popular way of thinking about China's economy for the last few years: it is quite likely that private firms are exporting in part because competing in the domestic economy is so difficult. But still, the export story also shows that the private sector is far from dead. It also is one indicator that the supply side changes of recent years, whether that be the big build-out of infrastructure or Li Keqiang's push to improve the business environment for smaller firms, are bearing some fruit.

Demand side growth

Supply side developments can't fully explain the surge in China's exports since 2019. After all, while it is only in more recent years that Li Keqiang's efforts to improve the business environment have become more meaningful, the build-out of China's infrastructure began long before that.

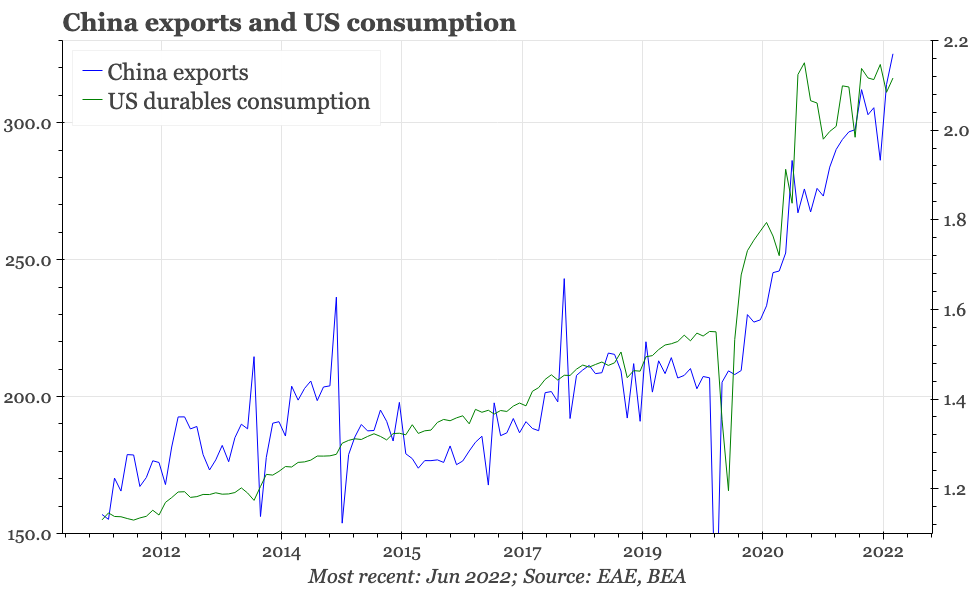

In any case, whatever has happened with supply, it is also clear that global demand for imports has risen strongly since 2019, and in a way that plays to China's particular manufacturing strengths. To be specific: there was generous income support for households in developed economies during the lockdowns; with consumers unable to go out, this money couldn't be spent on services, so consumption of goods was instead a disproportionate beneficiary; and within that, spending on tech boomed, in part because of the need for better devices to be able to work from home.

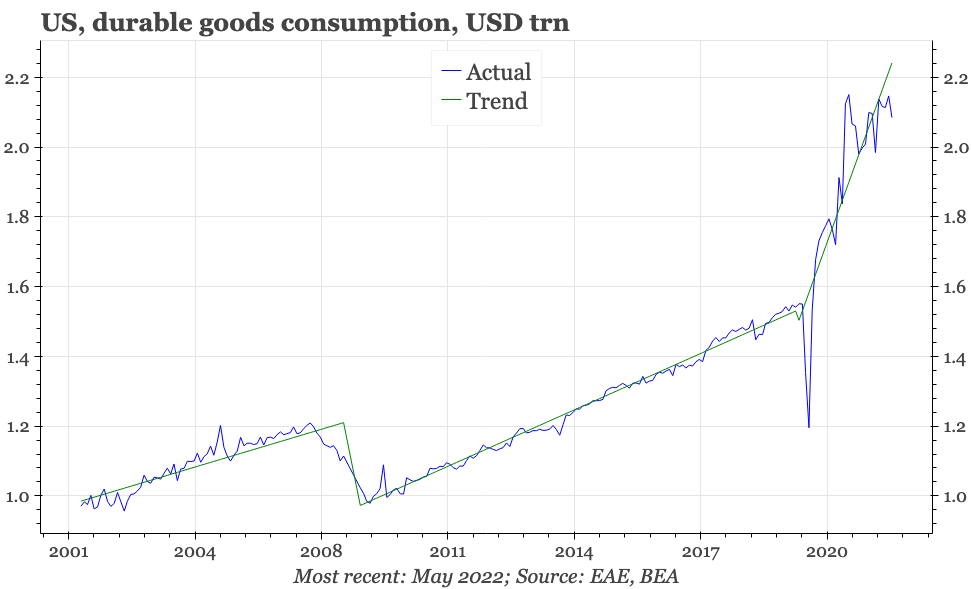

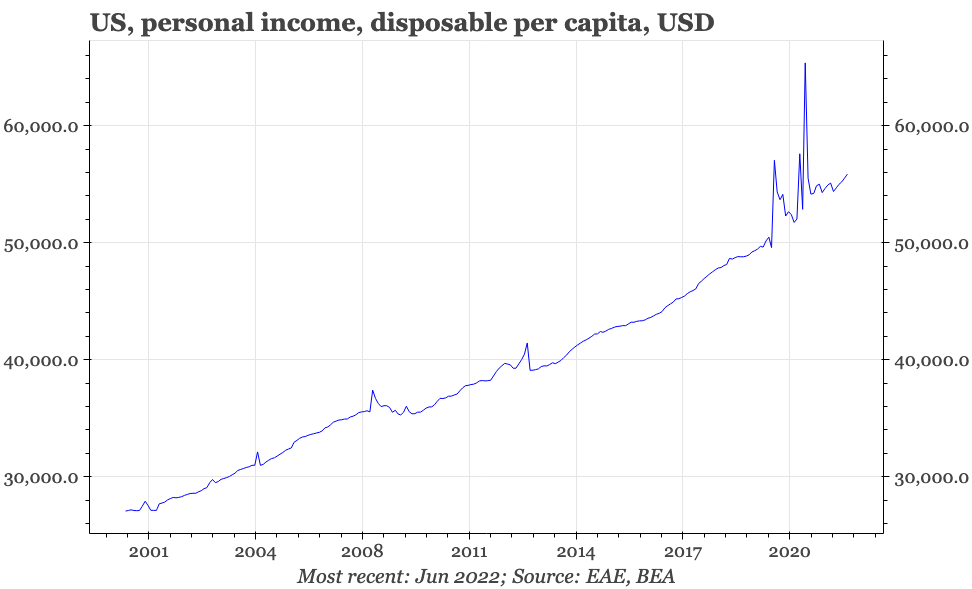

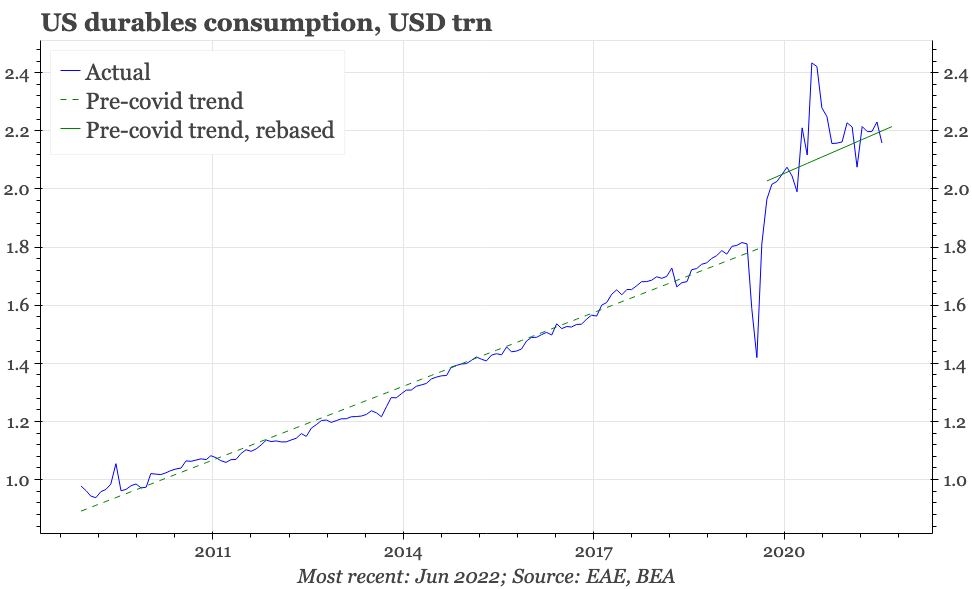

The US led these shifts. Monthly per capita personal disposable income in the US reached well over USD60,000 in March 2021, up from USD50,000 at the end of 2019. In that same period, spending on goods rose from 36% of total consumption to over 42%. Since just before the pandemic began, US imports have risen by 38%, imports of consumer goods by 43%, and imports of computers by 30%. As both the biggest goods exporter in the world, and home to most of the world's computer production, it would have been difficult to find global circumstances that were better suited to China.

Exports up, construction down

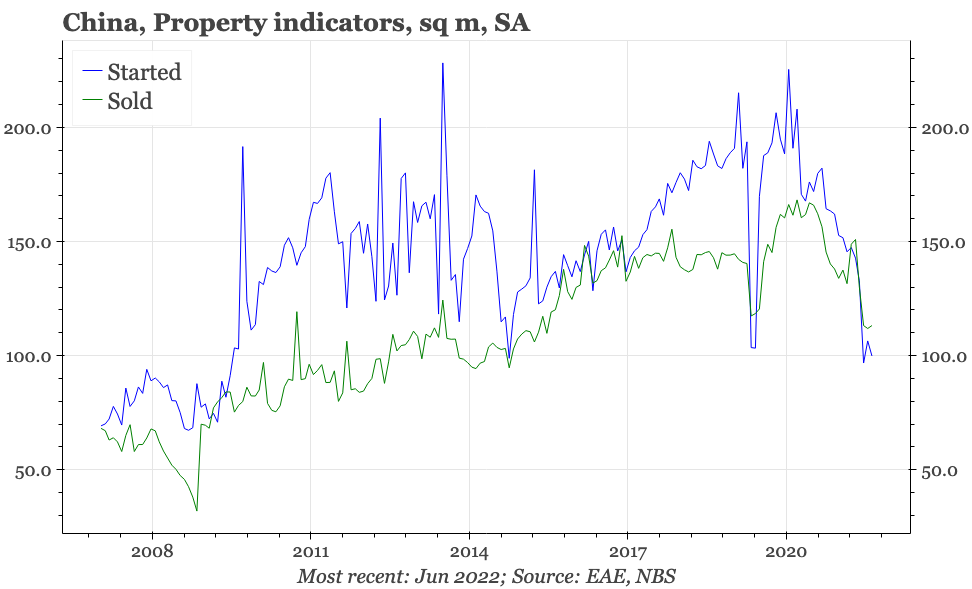

As it turns out, China needed these circumstances, because for all that exports have boomed, domestic construction has collapsed. This wasn't entirely coincidental. The statement from the Central Economic Work Conference at the end of 2020 announced that there was a “window of opportunity” for reforms in 2021. The authorities didn't specify exactly what that meant, but the window seemed to be related to the low base effect created by the collapse in economic activity in Q120 that greatly lowered the bar for the achievement of any annual growth target in 2021. As for reforms, the government seemed to want to achieve something it had never been able to do before: crack the property sector.

It did this by introducing the so-called three red lines on debt for property developers, a rule that greatly inhibited the ability of the sector (particularly private sector homebuilders) to raise funds. Given the difficulty in reining in the sector previously, the government must have been prepared for this initiative to cause some economic damage. But it does seem that the fall-out has ultimately been greater than anticipated. Officials have been calling for stability in real estate since September 2021, and yet property sales, construction and the performance of listed real estate developers have since then only fleeting signs since of reaching a bottom.

At the same time, the window of opportunity has probably opened for longer than was originally been hoped. That's partly because global developments helped hold up commodity prices in a way that hasn't been apparent in previous property slowdowns in China, and thereby postponed a synchronised downturn in both property and heavy industrial profits. But the prolonged rise in exports has been important too. Chinese export momentum has slowed since the 17% surge of 2H20, but in 1H22, Chinese exports still grew almost 10%, and that was actually a bit faster than in the previous six months.

Exports down, construction down?

The export boom then has been a very significant part of the macro picture in China over the last couple of years. So, it is equally important that the boom in exports – and for that matter, commodity prices – now finally looks to be ending.

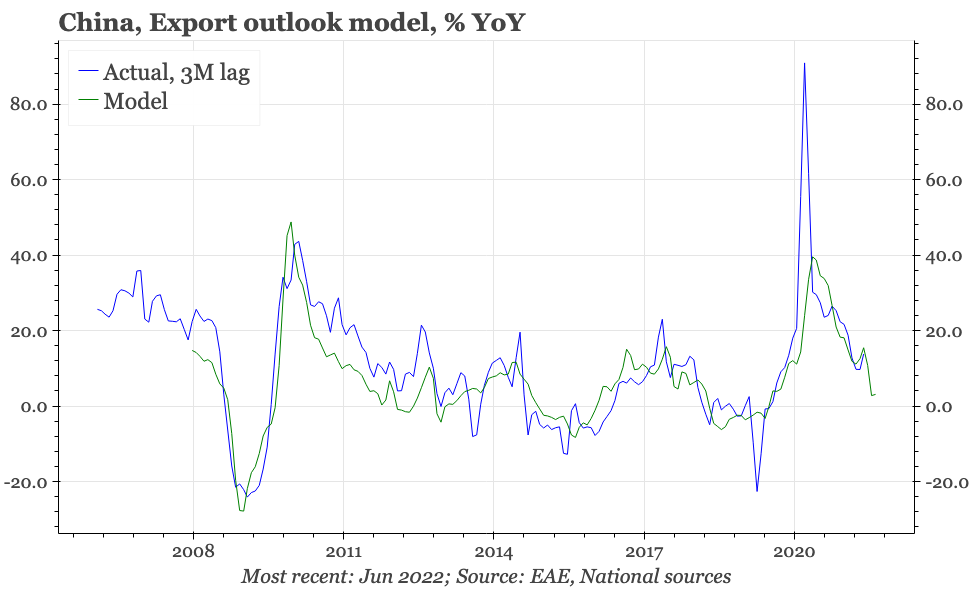

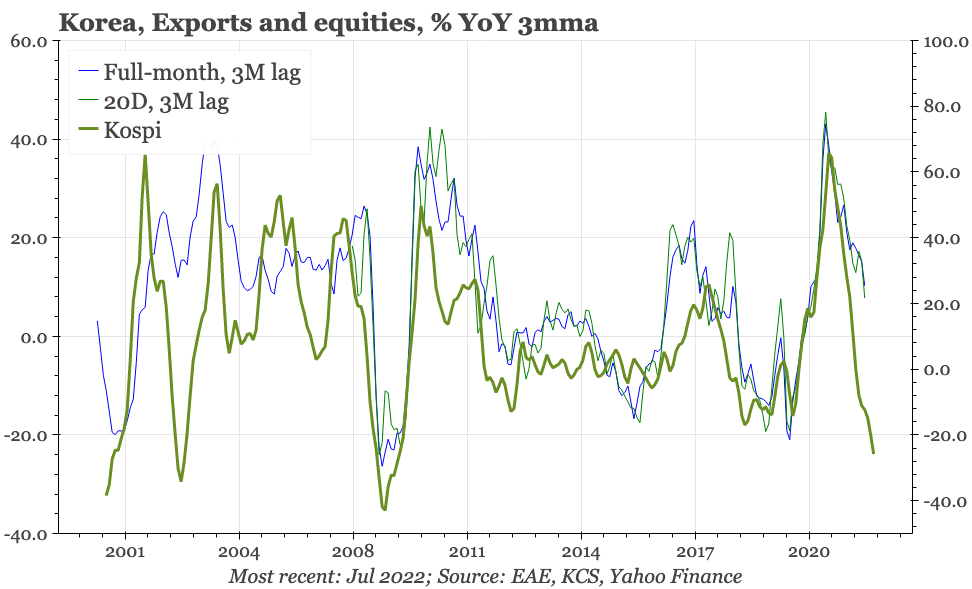

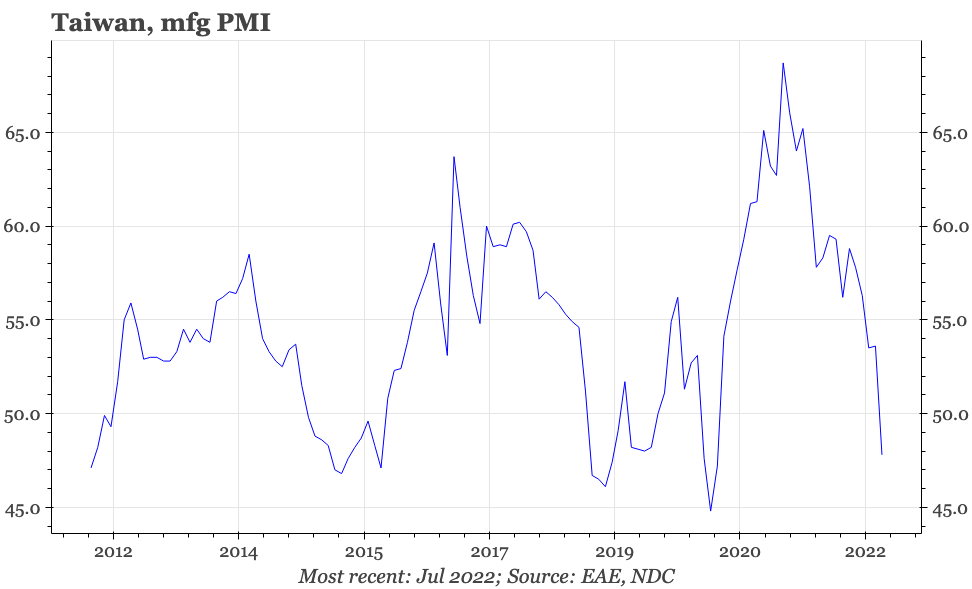

Onshore steel prices have fallen 20% since April, and input prices in Sunday's PMI suggest that the sharp fall in YoY PPI inflation of recent months continued in July. As for exports, leading indicators for the region cycle are pointing to contraction in the next 3-6M. That's the message from equity markets in Taiwan and Korea, the two most export-led economies in the region. It is also suggested by a composite leading indicator for the region's exports based on a range of macro measures from the US and EU, as well as Asia.

This probably isn't very surprising. In the US, personal incomes have normalised after the government giveaways during covid, and in real terms are almost back to the level of end-2019. The trend in growth in imports of durable goods has already returned to the pre-pandemic pace – and presumably there's downside risk around that, given the Fed's tightening. The surge in energy prices is a big negative shock for the EU economy, and is now showing up in a fall in business sentiment. The moderation in global commodity prices and the weakness in Chinese construction are all also pointing to a weakening of the global cycle.

In terms of actual data, indicators for the next 3M are that export growth slows towards zero. But given the global backdrop, it feels like the risks are to the downside, and some warning signs are beginning to appear. Equity markets in the region are pointing to a 20% decline in exports. Taiwan's July PMI also suggests the pandemic export cycle is ending with a bump.

Implications

For China, the turn in the export cycle is a big deal, given the ongoing contraction in property construction. China's economy won't be growing if both property and exports are falling. It is for this reason that historically, when the export cycle has been slowing as the leading indicator suggests is now likely, policymakers in Beijing have been engineering an acceleration in domestic construction.

That would seem to be the plan this time around too. This week's Politburo statement on the economy put “stabilising property” before the usual (for the last few years, at least) reference to “property being for living, not speculation”. But that is still just an incremental shift, a continuation of the gradual softening in official language towards real estate of the last nine months. This cautious easing hasn't yet ended the downturn in the physical market.

The cautiousness of property easing might indicate that officials have got something up their sleeves, and that somehow – seemingly most likely via more infrastructure spending – the growth picture will hold together in the upcoming months. Perhaps. But a slowdown in export growth would remove the big growth motor of the last few months, and with the continued extreme weakness of property construction, that prospect points to the growing risk of a real growth accident in China. Among other outcomes, that would bring deflation, worsening debt dynamics, and lower interest rates.

s