The East Asia Economist

The 1997 double play isn't yet at work, and the HKD doesn't look as over-valued as then. But Hong Kong does now face a double whammy of Fed tightening and zero covid. With maintenance of the peg ultimately being a political decision, the question is how much economic pain the authorities can take.

Not a Double Play, but certainly a Double Whammy

The HKD peg – Zero Covid and Fed tightening

Just after Hong Kong became a Special Administrative Region (SAR) of China in 1997, the Asian financial crisis hit. For Hong Kong, that involved intense pressure on the HKD Linked Exchange Rate mechanism, which the authorities complained came in the form of a “double-play”. “Speculators” would short the equity market, and then sell Hong Kong dollars, which would push up interest rates and so achieve the desired fall in stocks. Such coordinated selling hasn't been so obvious so far this time, but if Hong Kong isn't facing the double play, it is clearly facing a double whammy, and one that could prove just as troublesome: Fed tightening, and zero covid.

Because the Linked Exchange Rate ties the HKD in a tight $7.75-7.85 band against the USD, its monetary policy is run by the Fed, which is tightening for a US economy that has been running hot. But Hong Kong's economy is cold, dampened in general by its close links with mainland China's slowing economy, and specifically by Beijing's zero covid policies.

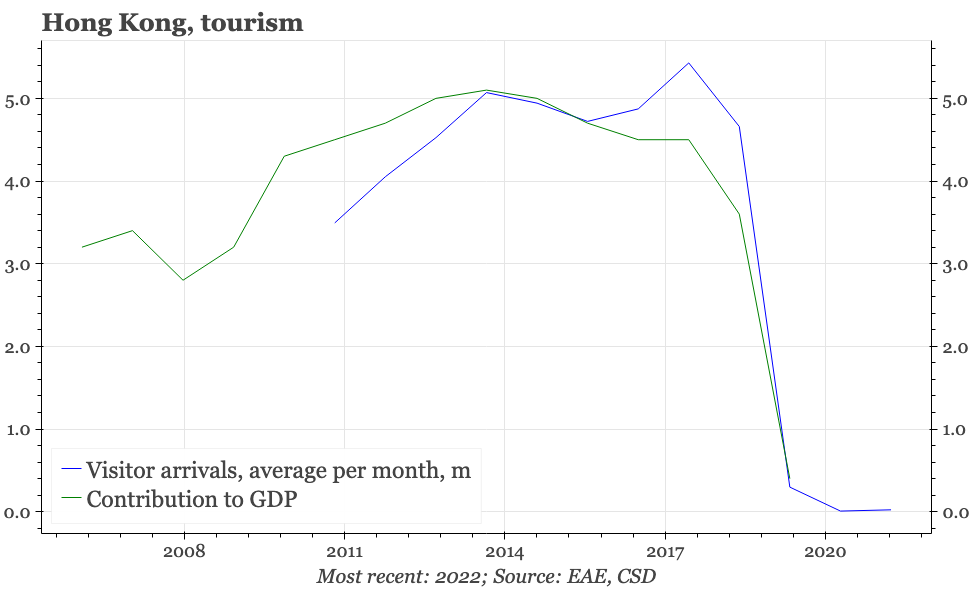

The impact of zero covid on Hong Kong has been enormous. The city welcomed just 1,800 visitor arrivals in April 2022, down from a peak of almost 7m people per month in January 2019. Those levels of three years ago weren't far short of Hong Kong's whole population – and 80% of them came from mainland China. Zero covid has thus triggered a sharp fall in Hong Kong's service exports, and called into question the city's ability to continue as a global financial centre.

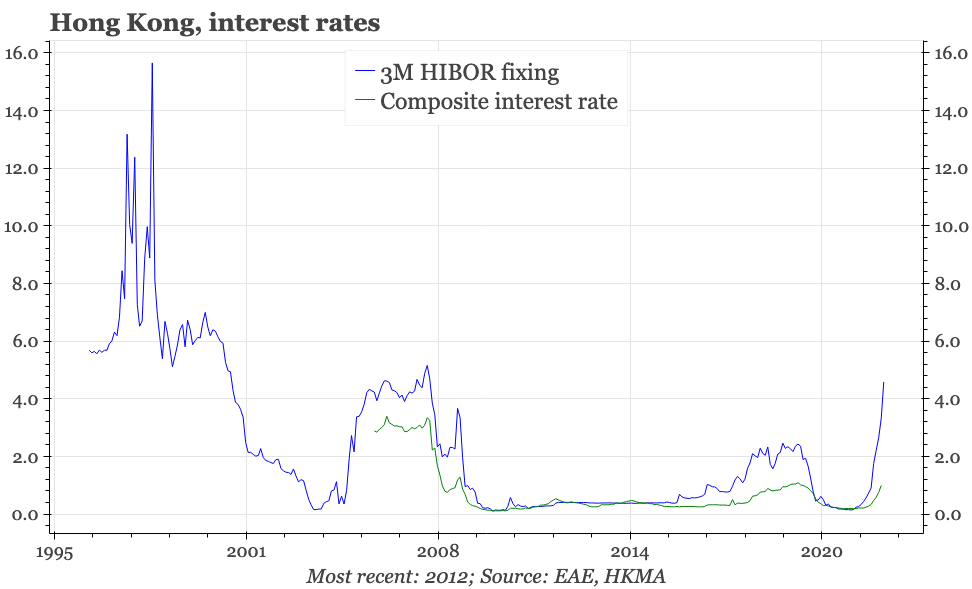

There's been plenty of market speculation this week that China is, finally, moving to change its covid regime. Whether that is true has yet to be seen. By contrast, in the unlikely event that there was any doubt, the Fed again made it crystal clear on Wednesday that it is far from being done with hiking. That is relevant for Hong Kong when even the impact of the tightening done so far hasn't been fully felt. The first of the Fed's cumulative 375bp of hikes this year only happened in March; by September, the average funding costs of Hong Kong's banks had only increased by 80bp; the ratio of Hong Kong's monetary base to GDP is still 45ppts larger than it was in 2009; and the city's hugely inflated property prices – after they almost tripled between 2009 and 2019 – have so far only fallen by 10%.

In essence, the pegged exchange rate means that Hong Kong is due for a lot of economic pain in the coming months, and possibly years. Unfortunately for the HKMA, these circumstances do create the likelihood of some sort of “speculative” attack on the HKD.

From the narrow perspective of the exchange rate, the HKD doesn't look as vulnerable as it did in 1997. But maintenance of the exchange rate is ultimately a political decision, so the bigger issue for the peg is how much domestic economic damage the authorities are willing to tolerate. We don't know where their threshold is, but the level of economic pain Hong Kong is suffering will certainly be higher if it continues to be hit by the double whammy of not just Fed tightening, but mainland zero covid too.

Hong Kong's headwinds

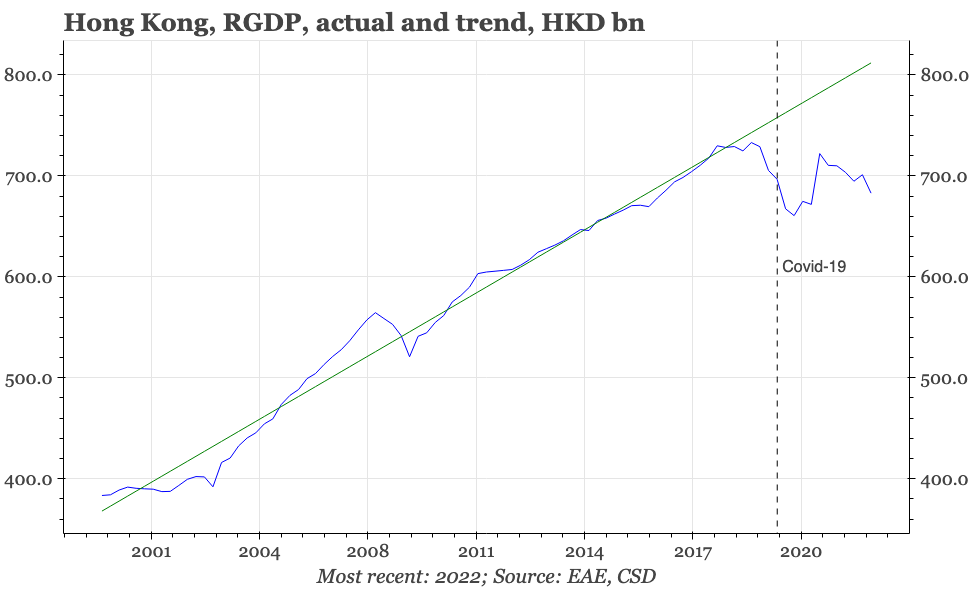

The economy is clearly in a bad way. At under HKD600bn, RGDP is still 7% below the all-time peak of HKD733bn reached in Q119; if growth had continued to grow at the same average rate achieved in the twenty years before then, RGDP would now be over HKD800bn. As it did to many other economies, covid dealt a big blow to Hong Kong. But Hong Kong's difficulties had begun before the pandemic, with the protests of 2019 causing significant economic disruption and the first falls in tourist arrivals.

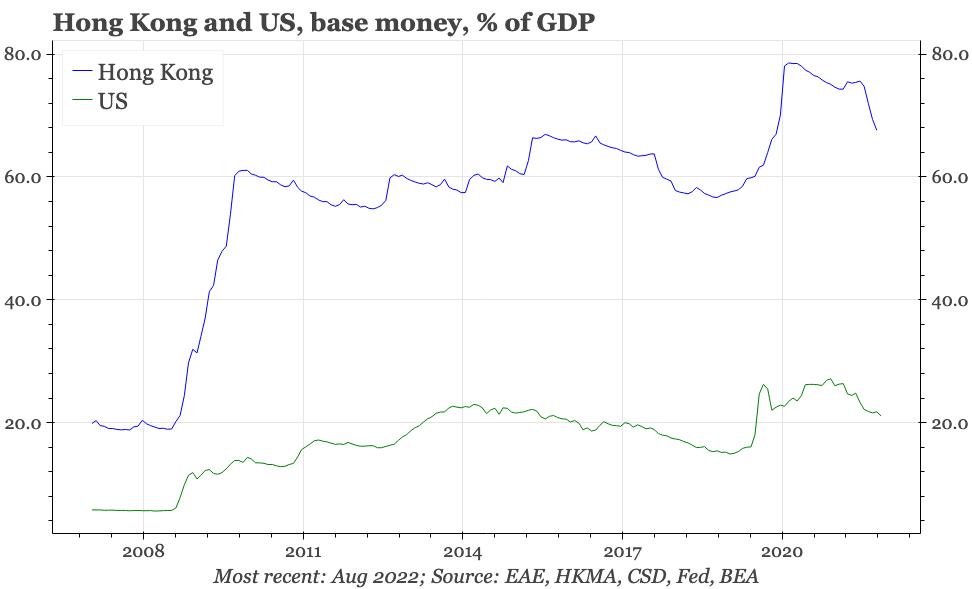

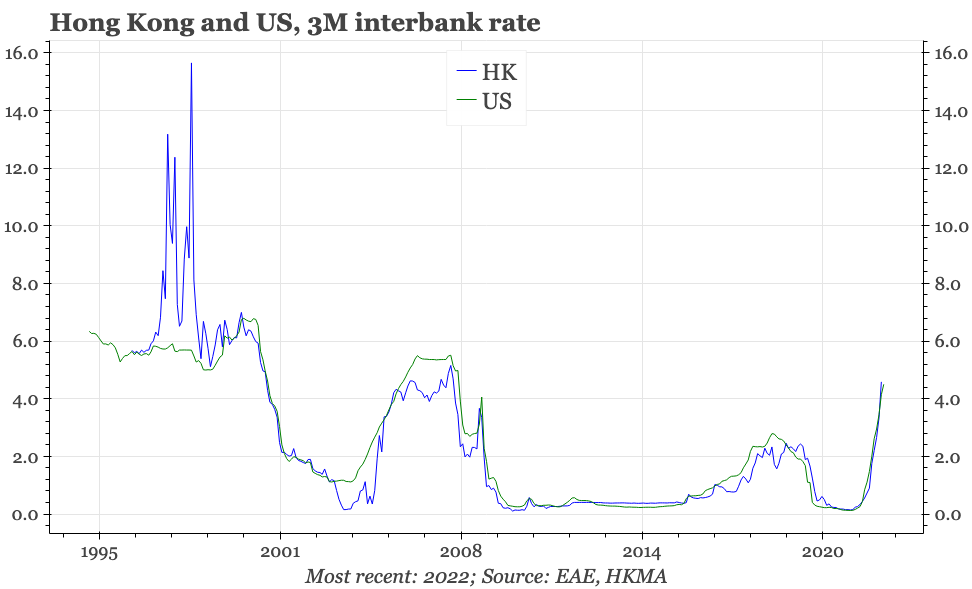

And now, there is Fed tightening. That matters everywhere, but because of the Linked Exchange Rate System, the impact is purest in Hong Kong. In essence, Hong Kong has to accept US interest rates, with the forcing mechanism being cross-border capital flows. So, since March, a period in which the Fed has hiked rates by 375bp, the HKMA has raised the Base Rate in Hong Kong by the same margin, HIBOR has increased by more than 400bp, and the city's monetary base has contracted by 10%. Both changes will matter, but the reduction in money supply is particularly worth noting, being akin to an involuntary quantitative tightening.

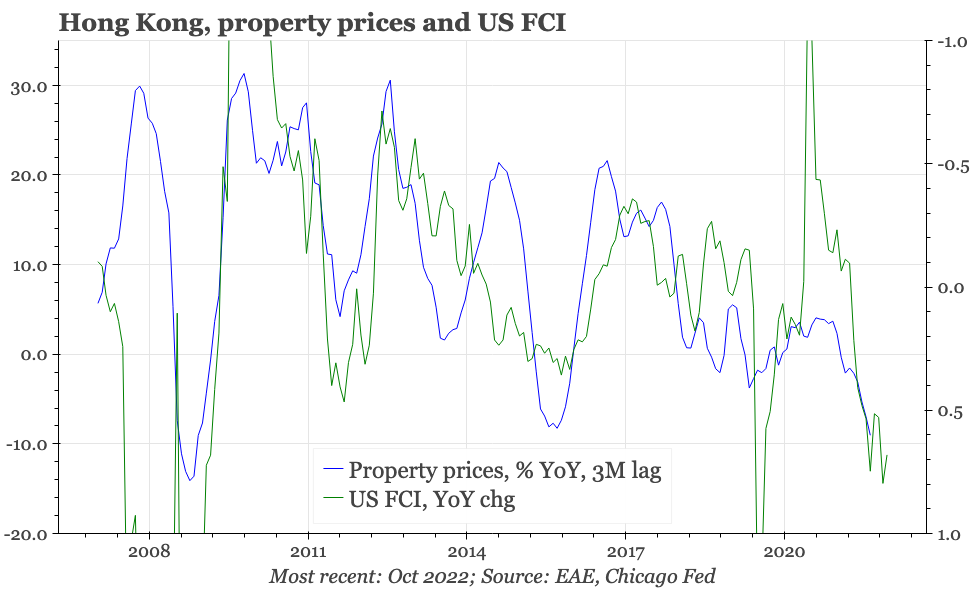

These are big, important changes, but for the domestic economy, the shock from this monetary tightening has yet to be felt. That can be seen most clearly in the property market, where prices have so far only fallen 10%. That's notable, given they should, obviously, be affected by monetary conditions. Indeed, historically, changes in financial conditions in the US have been quite an accurate leading indicator for housing prices in the SAR. It is hard to think that the further falls in property prices in the city that are suggested by the Fed's Financial Conditions Index aren't justified when the declines to date still leave average real estate prices multiples higher than they were in 2009.

Loose policy when conditions warranted tightness

Just as property prices now are starting to be pulled lower by US monetary policy, so the very high level they reached before this tightening was the result of the Fed's decision after 2009 to keep rates low and engage in multiple rounds of quantitative easing. Because of the HKD peg, these policy decisions loosened monetary policy in Hong Kong, but by a multiple of what was happening in the US: while the ratio of the monetary base to GDP in the US rose by around 20ppts between 2009 and 2021, in Hong Kong it increased by three times as much, peaking at almost 80%.

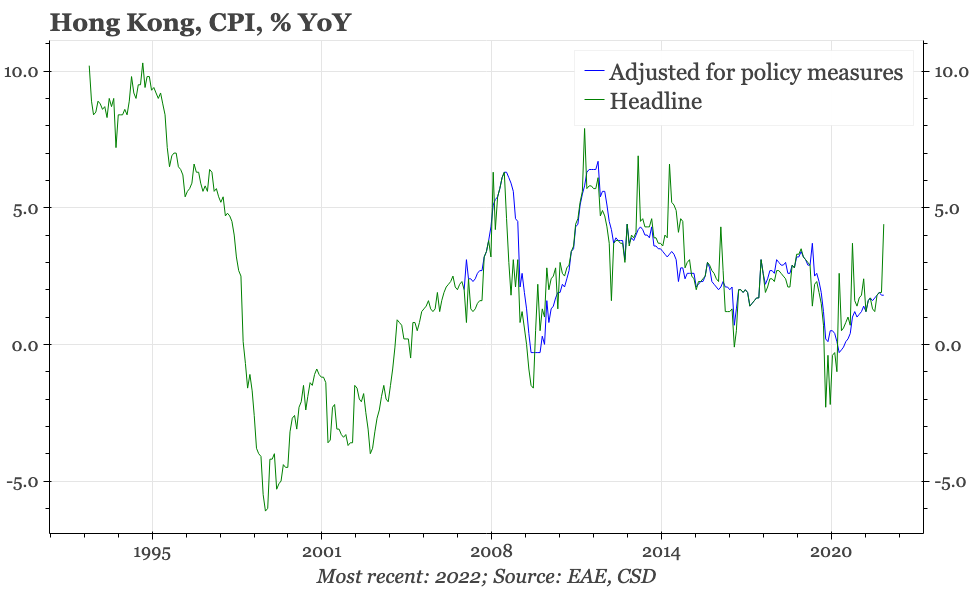

There were a couple of reasons why US monetary loosening became so much more magnified in Hong Kong. Obviously, when compared with the world's largest economy, Hong Kong's GDP is tiny. In addition, the SAR didn't suffer from the same lack of inflation experienced in the US and elsewhere following the global financial crisis. That was because mainland China – Hong Kong's biggest trading partner – boomed after 2008. As an illustration, while in the five years to 2008 CPI inflation in Hong Kong averaged less than 2% YoY, in the following half decade it rose to 3.3%. Based on Hong Kong's own economic conditions, monetary policy should have been tighter, whereas the HKD peg and Fed policy meant it was actually much, much looser.

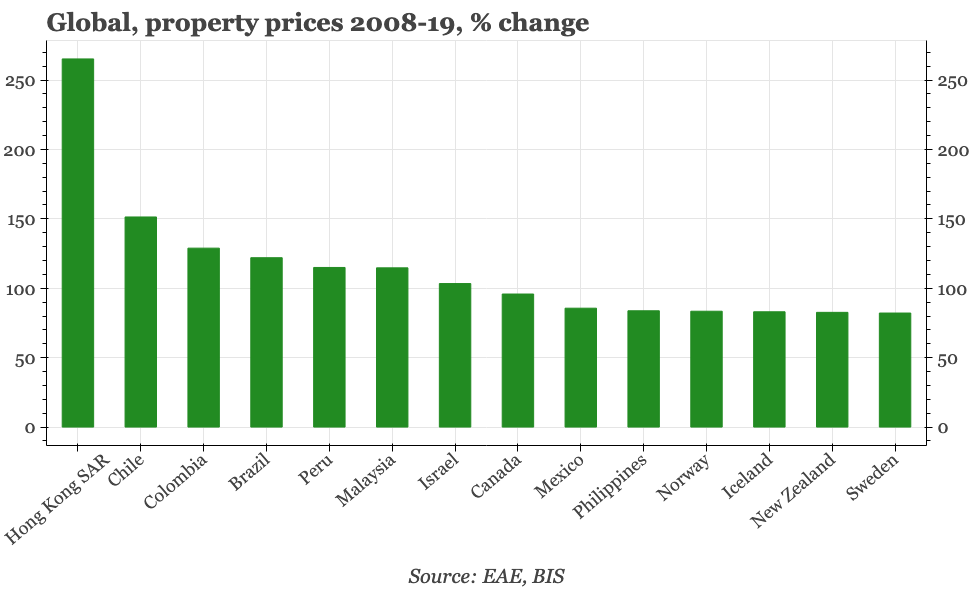

The effect of this counter-cyclical looseness in monetary policy was a surge in asset prices. To be clear, this is precisely how the HKD peg is supposed to work. If the nominal exchange rate can't rise to correct imbalances, then the work instead has to be done by prices in the domestic economy, which are supposed to drive an equilibrating shift in the price of the currency in real terms. But as much as the rise in property prices was understandable, it was still eye-watering. Average prices almost tripled between 2009 and 2019, a much bigger increase than experienced by any other economy tracked by the Bank for International Settlements. Had it not been for a range of macro-prudential measures introduced by the authorities, the rise would have been greater still.

Unsurprisingly, rises in incomes didn't keep pace with this surge. According to an annual Demographia survey, the price:income ratio for Hong Kong housing reached 23.2 in 2021. That was much higher than the next most expensive city, Sydney, where the ratio in 2021 stood at 15.3. It also represented a big rise over Hong Kong's own ratio of 11.4 in 2010. Needless to say, that means Hong Kong property is expensive – indeed, according to Demographia's own definitions, any price:income ratio over 5.1 signifies a property market that is “severely unaffordable”.

Tight policies when Hong Kong needs loosening

Obviously, US policy has now completely switched from the settings that led to this surge in prices. Moreover, the Fed doesn't look like it is yet done with tightening. If policy rates are going to end up around 5% in the US, then interest rates in Hong Kong still have around another 100bp to rise. That would be bad news for economic activity at any time, but is particularly so when economic trends in Hong Kong in themselves don't warrant such a tightening. Indeed, just as US policy remained loose after the financial crisis when Hong Kong was booming and really needed tightening, now US policy is tightening when Hong Kong's economy is stalling.

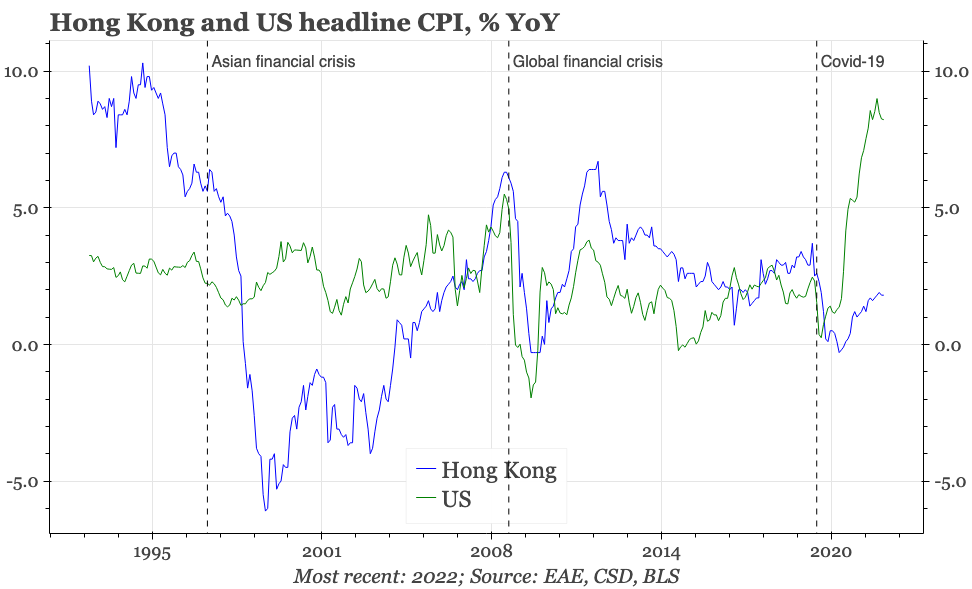

Of course, particularly in Europe, many central banks are tightening into weak growth, with their bigger concern being inflation. But this doesn't look like an obvious problem in Hong Kong. While consumer prices are rising in many countries more quickly than any time since the 1970s, in Hong Kong inflation is under 2%. Such a low rate of inflation isn't uncommon in the region – the same phenomenon is being experienced in both mainland China and Taiwan. But Hong Kong is the only one of these economies that directly adopts US monetary policy, so local inflation being so low means Fed nominal hikes will be producing big increases in real rates in the SAR.

In this environment, then, it is likely property prices in Hong Kong still have a lot of room to fall. And, it is easy to imagine such a development producing a downwards spiral, reducing domestic economic activity and inflation, and so producing a further rise in real interest rates that weighs further on real estate. To short-circuit this process, Hong Kong either needs an almighty reopening trade, or lower US rates. In other words, Hong Kong can't do much itself, being instead dependent on decisions on zero covid made in Beijing, and on decisions on interest rates made in the US.

Cushioning the fall

Without those choices going Hong Kong's way, the best that can be hoped is that the downwards spiral proceeds somewhat slowly. It is at least true that housing prices in Hong Kong didn't spike up further during the Fed's aggressive loosening of 2020-21, so perhaps prices aren't quite so vulnerable in the very short term. However, to be frank, that doesn't seem like something that can stave off a big correction in property, given real estate prices were so bubbly before covid. The authorities will likely think a bigger source of support will come from rolling back the macro-prudential measures introduced when the property market was booming, a process that has already begun. Again though, that is unlikely to be a silver bullet: as mainland China is currently finding out, the impact of such loosening when market sentiment has already turned can be disappointing.

In terms of conditions in the short-term, it is probably more meaningful that the funding cost for banks, as captured by the HKMA's Composite Interest Rate measure, hasn't increased nearly as quickly as either the Base Rate or interbank rates. The Composite Interest Rate has been rising, but as of September, it had only increased by 80bp from the lows in late 2021, and then only to 0.99%. For the moment, banks are benefiting from a plentiful supply of cheap domestic savings, with the average deposit rate in September standing at just 0.96%. As long as funding remains cheap, banks have less pressure to raise lending rates.

That is helpful for interest rate sensitive sectors like real estate. It is unlikely, however, that overall funding costs will remain this depressed. Some banks will be relying more heavily on the interbank market for money, and so the further rise in HIBOR since September would have raised the Composite Interest Rate since then. Besides, funding from depositors is unlikely to remain as cheap and plentiful as it has been: eventually ordinary depositors will start to seek higher deposit rates, for example by shifting funds out of HKD into USD savings accounts.

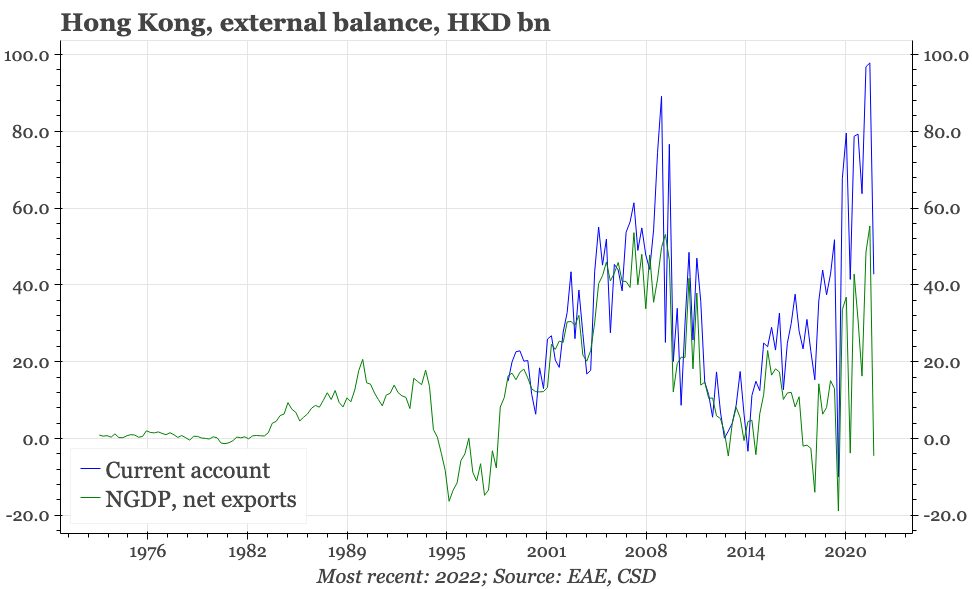

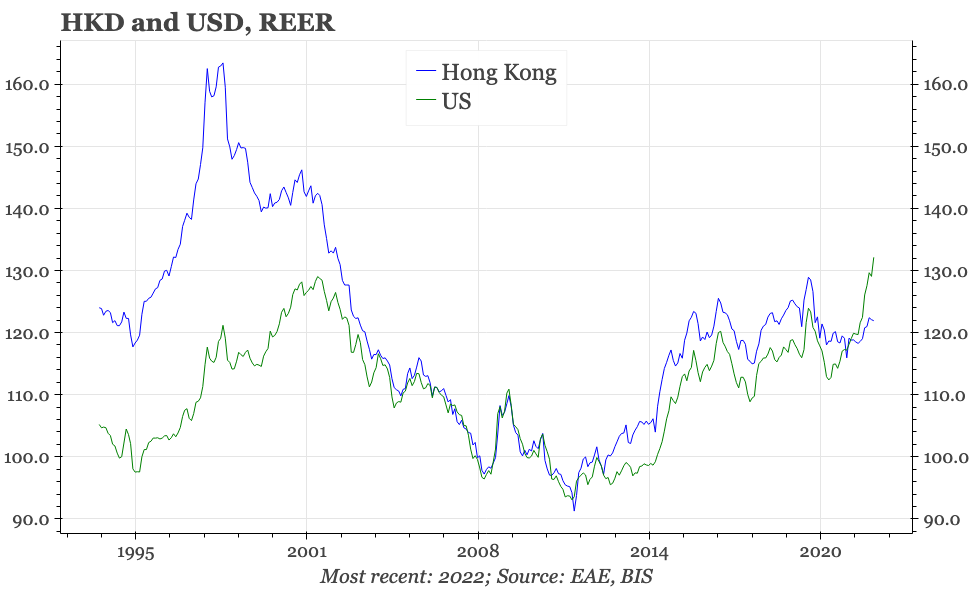

A final factor providing some offset to all the pain that should result from Fed tightening is Hong Kong's external balance. The HKD's problems in 1997 in part reflected a classic economic overheating. In the years running up to the Asian financial crisis the current account balance had fallen into deficit, leaving the economy dependent on capital inflows. An important driver of this deterioration in the external position was Hong Kong's high rate of inflation, which in turn drove the real effective exchange rate to very high levels. By 1997, the HKD was looking over-valued.

This time, the current account remains in substantial surplus. The sudden stop in tourist inflows has produced a collapse in Hong Kong's service exports. But imports have also fallen sharply, with the closed border also stopping almost anyone from leaving.

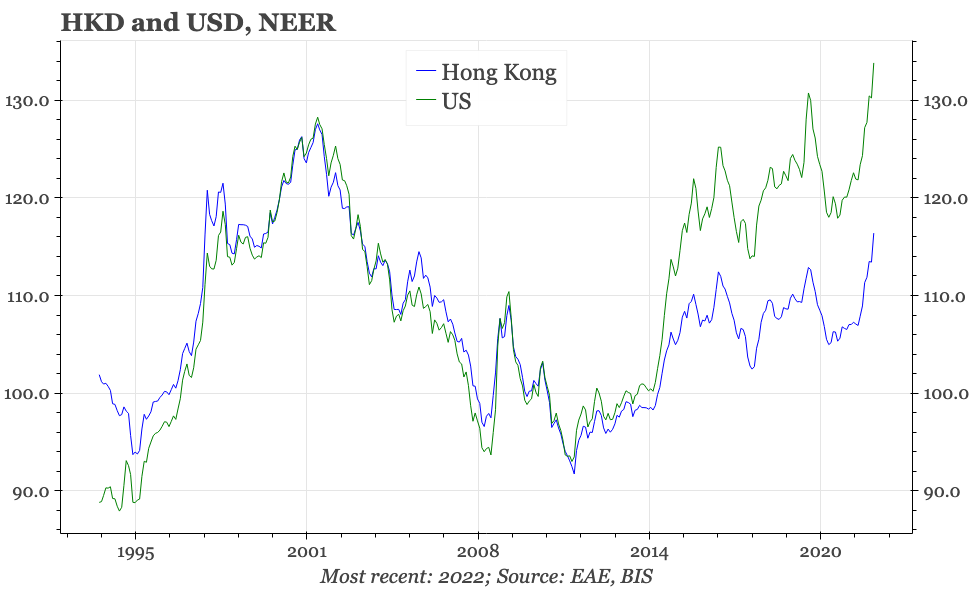

In the last few weeks, Hong Kong has liberalised its own border restrictions, and that seems to be causing the external balance to deteriorate a bit. That's because the loosening, so far, has led more people to leave Hong Kong than to arrive. But that probably doesn't change the big picture, with other forces helping anchor Hong Kong's overall external position. In the past twenty years, Hong Kong firms have greatly boosted overseas investments, with earnings from those now as big as the services surplus. With domestic inflation trending down, and with the CNY not depreciating as much as other major currencies, Hong Kong's real exchange rate isn't nearly as over-valued as it was in 1997.

The politics of the exchange rate

The external surplus is particularly important for the Linked Exchange Rate. Usually, currency pegs break in economies that are running big current account deficits, leaving exchange rates vulnerable to sudden changes in external financing conditions. Clearly, Hong Kong isn't in that position.

That said, Hong Kong's linked exchange rate mechanism does mean that Hong Kong has to accept one of the consequences of any currency peg, which is interest rates that aren't necessarily appropriate for the domestic economy. As has been argued, Hong Kong went through one such period after the global financial crisis, when domestic rates were too low. Now it is likely to have the opposite experience, having to adopt interest rates that are too high. That will likely mean big falls in property prices.

This deflation won't in itself end the peg; indeed, it is precisely the development that, from an economic perspective, is needed to keep the peg in place. In the years after 1997, falling interest rates and rising prices were the mechanism to raise the real exchange rate when capital inflows couldn't increase the nominal exchange rate. Now, falling prices will be needed to depress Hong Kong's real exchange rate and so maintain the SAR's competitiveness when every currency except the HKD is depreciating against the USD.

This, though, is just the economic aspect of the exchange rate mechanism. It is politicians, not economic bureaucrats, who ultimately decide whether this automatic adjustment process will be allowed to play out. For them, there's probably two pain points. One is the popular dissatisfaction that is likely to result from ongoing domestic deflation. Just where this particular pain threshold lies is difficult to say. However, given housing prices are so far only down 10%, it is most likely still quite some way away yet. To put this point more directly, Hong Kong is only at the very beginning of the adjustment.

The second political consideration, in this age of ever spiralling US-China tensions, is how willing leaders in Beijing are for the HKD to remain pegged to the USD. This also isn't a simple assessment to make. On the one hand, even before the further weaponisation of the USD that was part of the West's response to the Ukraine war, it is likely that national security officials in the central government would have been worrying about Hong Kong's high degree of dependence on the US currency. Those concerns would only have intensified with Russia's invasion earlier this year. On the other, there would be plenty of experts in Beijing warning that reforming the peg would be a highly complex and risky undertaking.

While on this front we don't know much, it does seem reasonable to think that officials won't want to be rushed into making any change. If the Fed isn't going to help them out by cutting rates, then the best that can be hoped for is an end to zero covid in China, and the commencement of a full-on reopening trade that in Hong Kong. That at least can buy the SAR's economy some time.