Subscribers Only

Taiwan – huge CA to rise yet further

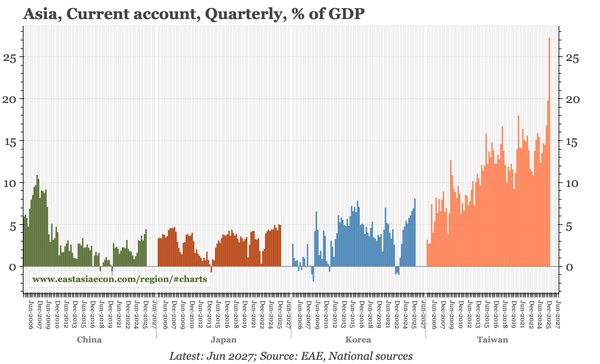

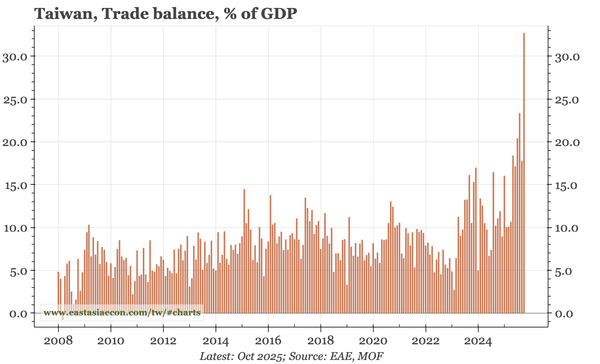

The surge in the current account surplus of January-September continued into the end of 2025. In Q4, the surplus reached almost 30% of GDP. The government's GDP forecast implies that will be roughly the size of the full-year surplus in 2026. Taiwan needs huge capital outflows to keep the TWD stable.

Subscribers Only

Taiwan – into unchartered waters

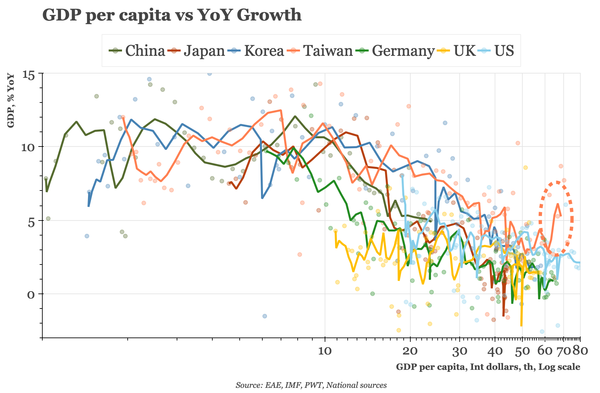

Taiwan's macro story is fascinating. Rarely has growth in such a rich economy accelerated so much, with reindustrialisation and huge external surpluses, at the same time as rates and the currency barely move. I'd think that something has to give. Will 2026 finally be the year that it does?

Subscribers Only

Taiwan – trade surplus back to 1980s levels

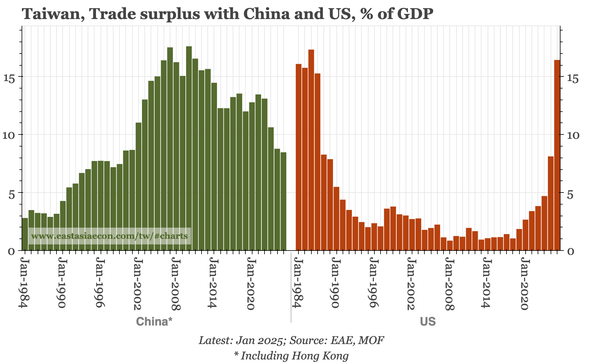

Even with data today showing a dip in exports in December, Taiwan's trade surplus last year reached the sort of sky-high levels last seen before the big TWD appreciation of the 1980s. Barring a real dislocation in AI hardware demand, underlying pressure for renewed appreciation will grow in 2026.

Subscribers Only

Taiwan – the export surge continues

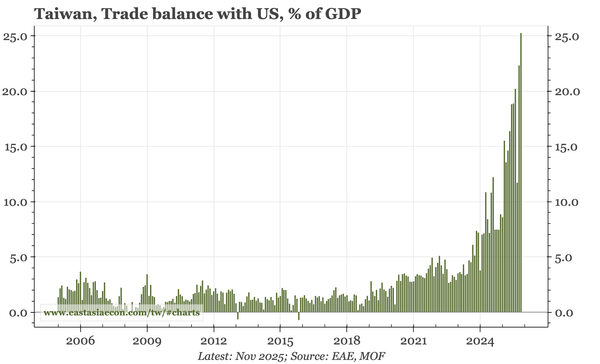

There is little growth in exports outside of tech in general, and semiconductors specifically. But the surge in chip exports is big enough to offset all the weakness in other products. The overall trade surplus eased back in November, but the bilateral surplus with the US reached 25% of Taiwan GDP.

Subscribers Only

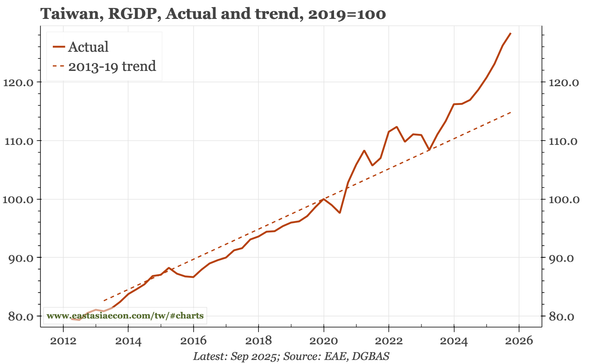

Taiwan – everything revised up, except inflation

In today's GDP release, the government raised estimated growth for Q1, Q2, and Q3. The FY forecast was raised by almost 3ppts to 7.4%. But because of AI, officials remain bullish about the outlook, and so raised the forecast for 2026 as well, And yet, none of this is expected to impact inflation.

Subscribers Only

Taiwan – trade surplus reaches 30% of GDP

I am running out of superlatives to describe Taiwan's export story in 2025. So I'll let the numbers speak for themselves: today's October data show semi exports have grown 70% this year, pushing the overall trade surplus last month to 30% of GDP, and the bilateral surplus with the US to 20% of GDP

Subscribers Only

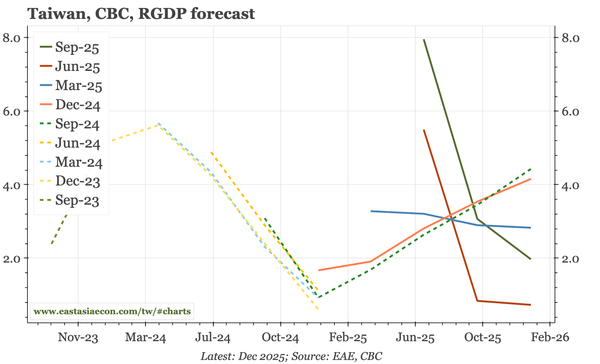

Taiwan – calmer macro, CBC on hold

Macro volatility – in inflation, growth, property prices and the TWD – eased in Q3, and it was no surprise that the CBC was on hold today. That won't change if AI demand growth slows. But the AI cycle has proven tough to forecast, and I'd expect the CBC will also be faced with more TWD strength.

Subscribers Only

Taiwan – import prices up, core CPI up more

August data today show the impact of the weaker TWD since July: fx reserves fell, import prices ticked up MoM, and CPI inflation rose. The lesson is that without currency strength, the step-change in economic growth since 2020 is more likely to show up in domestic prices.

Subscribers Only

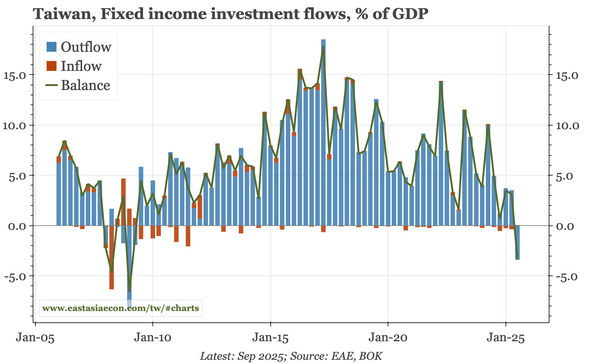

Taiwan – export orders peaking, Q2 capital flows

July export orders data show a continued reshoring, but overall export orders have clearly peaked. Today's Q2 BOP data show the rise in exports has further boosted the current account surplus. With the surplus so large, the TWD is vulnerable to the sort of shifts in capital flows seen in Q2.