China – where we're at

China remains on course for modest recovery. Covid-19 remains a downside risk, while the upside is muted without clearer policy support.

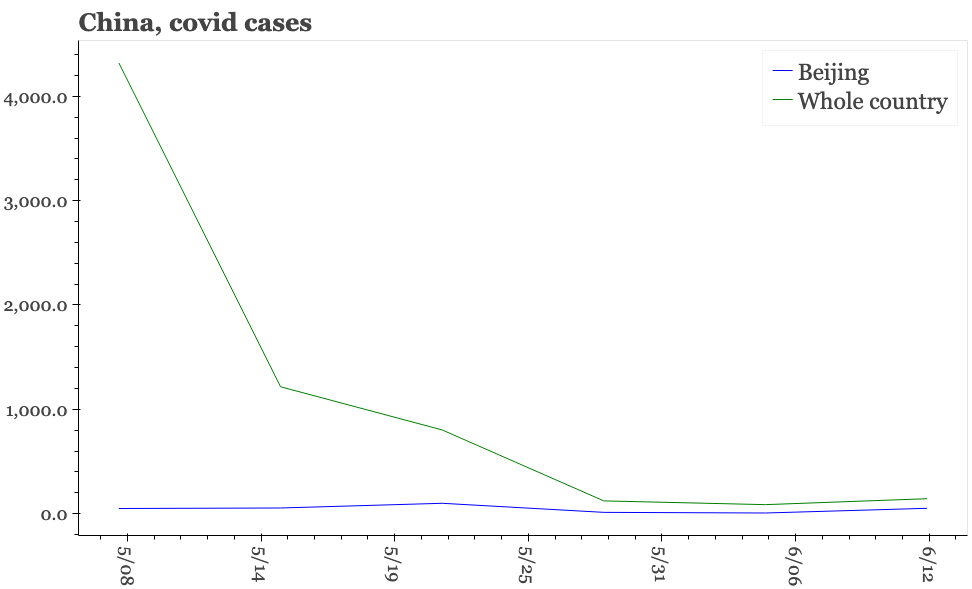

China's situation has improved from the full lockdown in Shanghai in April and May, but the country is still struggling to escape fully from the shadow of Covid-19. After showing clear improvement, case numbers in Beijing and Shanghai have both ticked up again, to a little over 50 on Sunday in the capital. In reaction, the two cities have once again started to tighten restrictions, with for example a new ban on all in-house dining in many parts of Shanghai.

Needless to say, this won't be good news for activity – or perhaps it is better to say, good news for self-sustaining activity. There's been a lot of talk in the last few days that all the spending on Covid-19 testing will provide some offset to the decline in the rest of the economy in Q2. That could well be true, but an economy just built on covid testing will obviously find it difficult to grow when the testing stops.

At times, especially after the Politburo Standing Committee's zero tolerance statement on covid a few weeks ago, it has felt like the government is running with some sort of scorched earth strategy, that nothing else matters apart from controlling the virus. It now increasingly seems that the PSC's statement was a particular call to get everyone on-board with zero covid, while the government's underlying policy continues to be one of focusing on both controlling the virus and promoting economic development. Speaking on a recent inspection trip in Sichuan, Xi Jinping himself was quoted as:

stressing the need to maintain the stable development of the economy, requesting pandemic control and economic development, and maintaining the stability of overall society

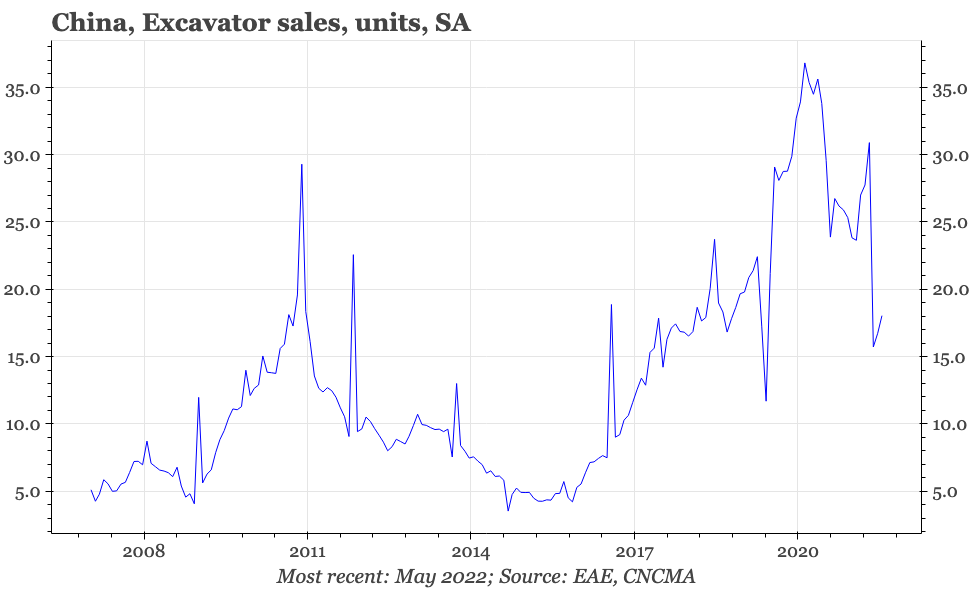

Neither just saying all that, nor all the covid tests in the world, are likely to help national construction and retail sales data for May, which will be released tomorrow. Excavator sales provide an early indication of what these official statistics will look like – in May excavator sales picked up, but were still running at only around 70% of where they were in Q421.

These May data are now backward-looking, though the property sales data that will be released as part of tomorrow's release will give some indication on the outlook. Data available so far through June do point to modest recovery. At least before the latest setback in Shanghai and Beijing, activity in both cities had started to pick up, with metro passenger numbers reaching about a third or higher of peak levels last week. Of course, that's not high, but is still a notable improvement on traffic levels seen in earlier in Q2. Our Financial Conditions Index remains loose, suggesting further upside for the economy from here.

The kind of lift that the FCI is pointing to does, however, continue to feel (very) best case. For the cycle it is good news that the government is showing rhetorically that it cares, but in substantive terms policy stimulus remains under-whelming. Policymakers continue to signal this is deliberate, that they don't want to flood the economy with liquidity – which of course is implicit criticism of the western counties that did.

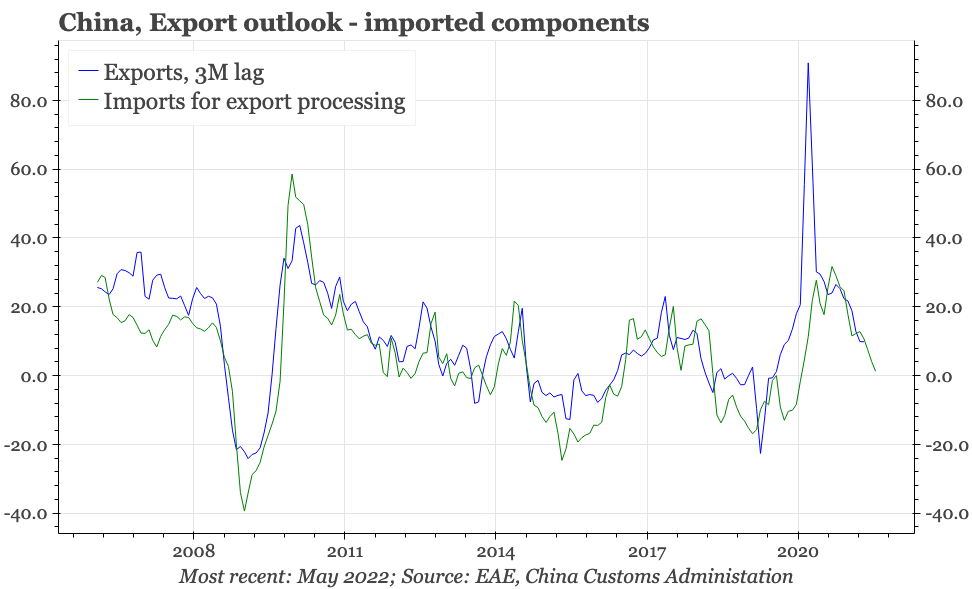

It is true that Beijing has been somewhat careful with monetary policy, which is one of the reasons inflation indicators in China remain soft compared with many other economies. Unfortunately for Li Keqiang and the other policymakers, that in itself may not mean that China escapes another boom-bust cycle. So far, foreign trade data from both China and the rest of the region continue to look surprisingly resilient. But if the US and other countries go into recession, China's export sector will certainly feel a lot of pain.

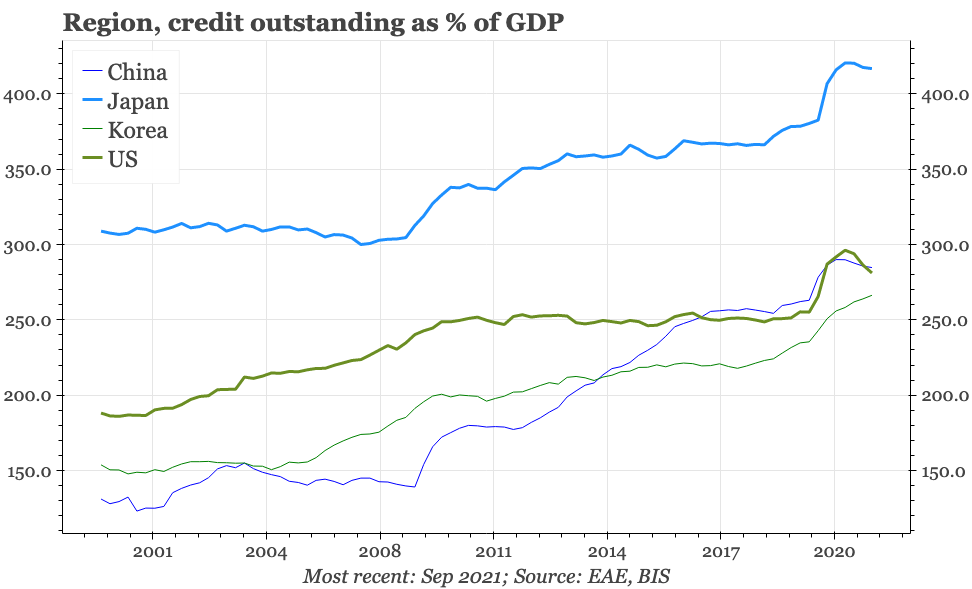

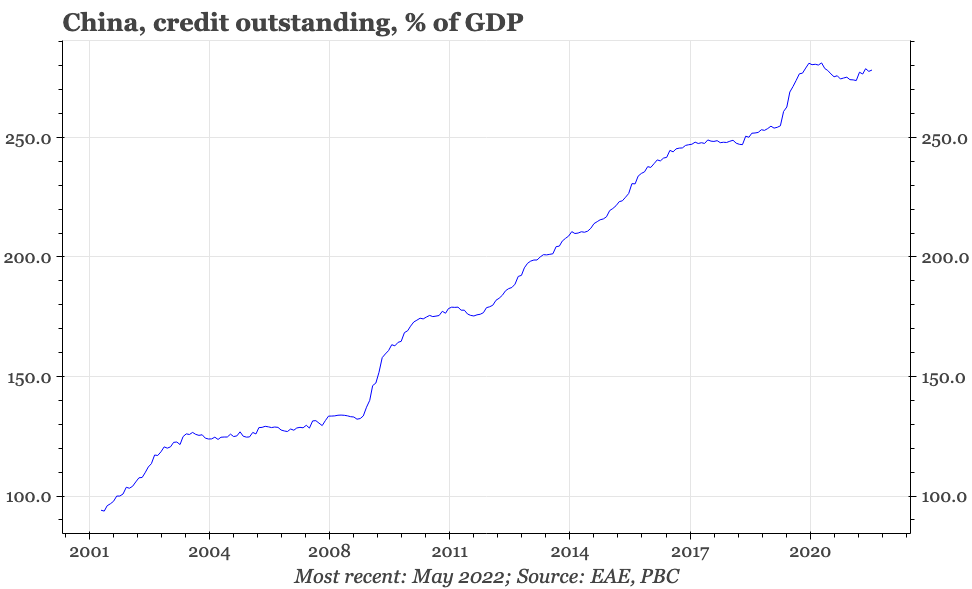

In any case, while Beijing's policymakers were more cautious than counterparts elsewhere, it is notable that the rise in the debt:GDP ratio in China in 2020-21, the first two years of covid, doesn't look so different from that of the US. And in 2022, China's debt level could well end up worsening more, as NGDP growth slows on the back of the covid lockdowns in Shanghai and elsewhere. In this respect, it isn't clear that China's policy has been so conservative after all.