Subscribers Only

East Asia Today

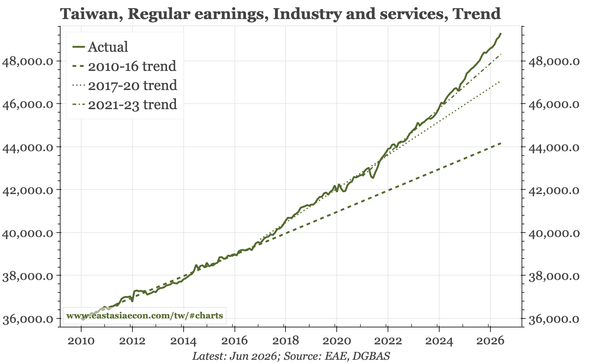

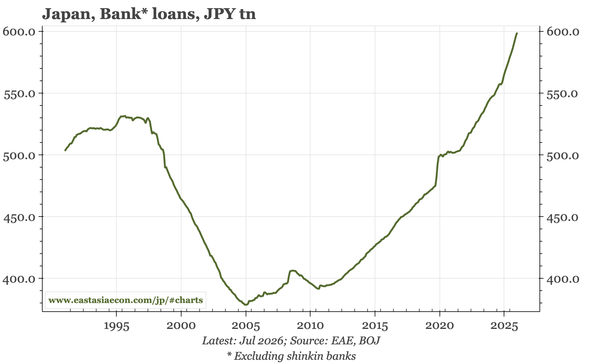

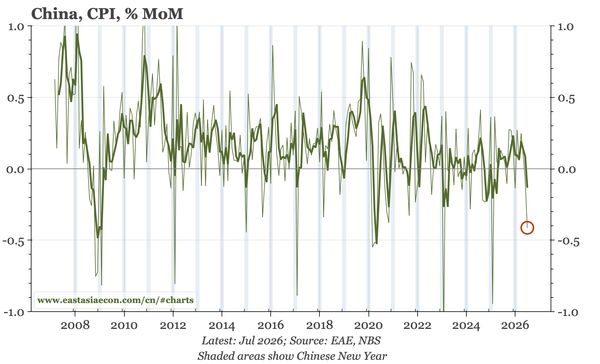

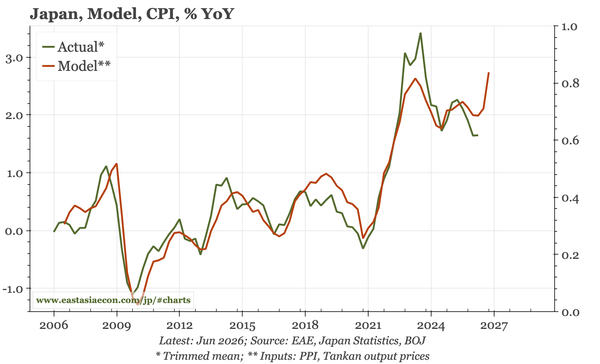

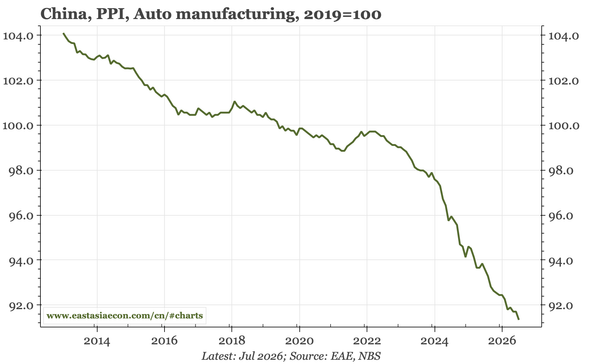

Summaries of three notes, covering: 1) yesterday's weak July inflation print in China; 2) today's summary of opinions of the July BOJ meeting and a few data releases in Japan; and 3) Taiwan's June wage data showing the slow but steady acceleration in wage growth is continuing.