Public Post

East Asia Today

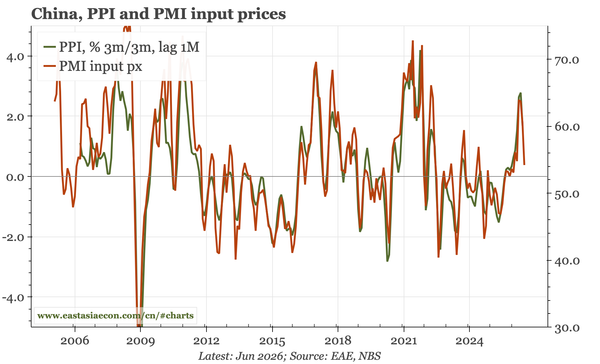

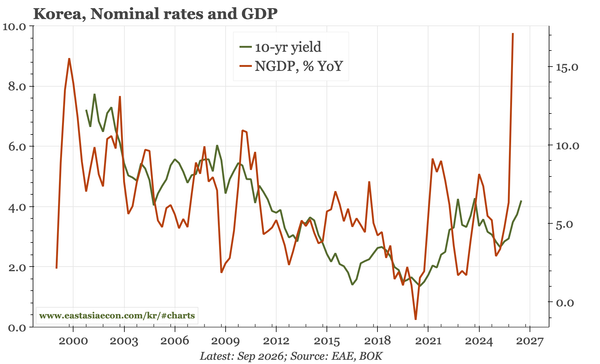

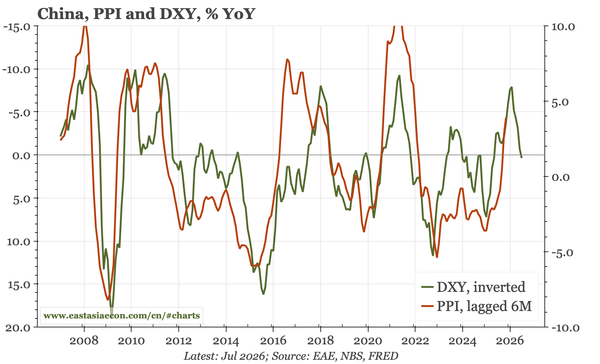

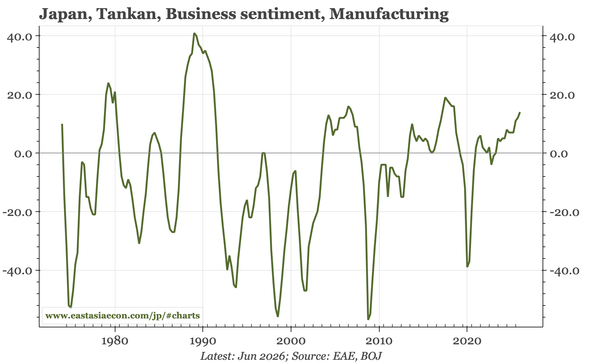

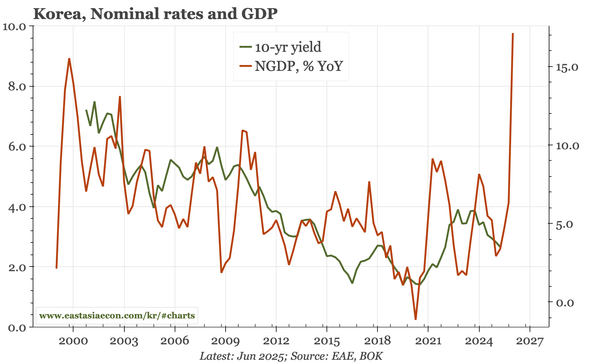

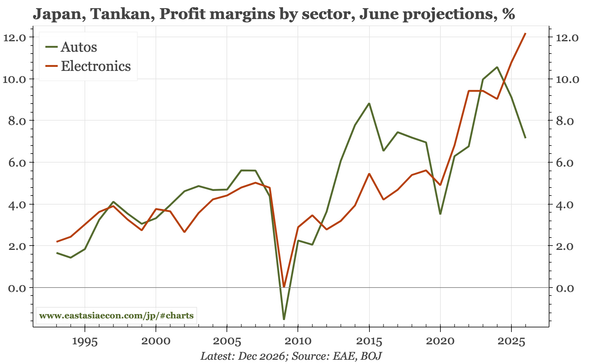

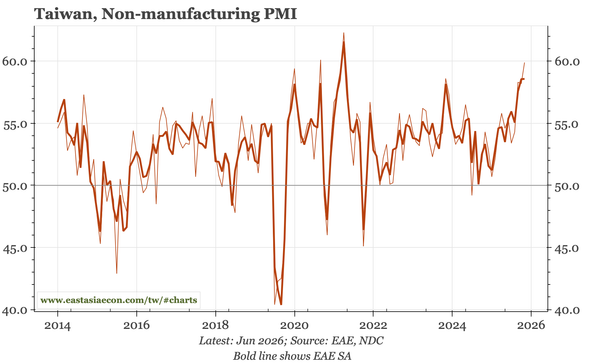

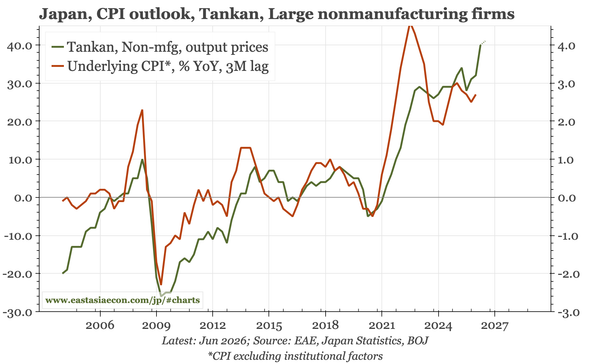

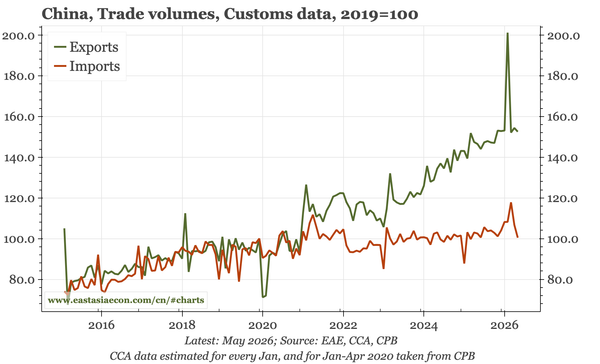

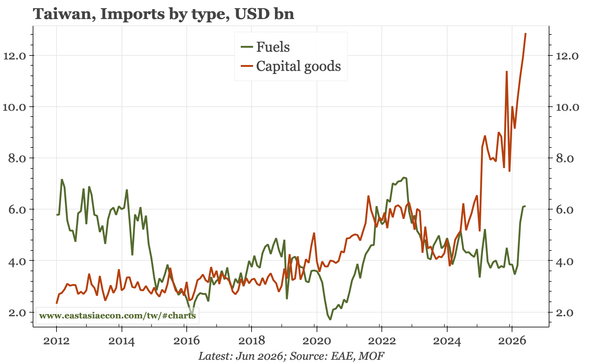

Lots today: no-change inflation data in China, a strong sakura regional report from the BOJ, Taiwan's foreign trade showing peaky exports but strong capital goods imports, and evidence that the strong rise in nominal GDP growth is boosting tax revenues in Korea.