Subscribers Only

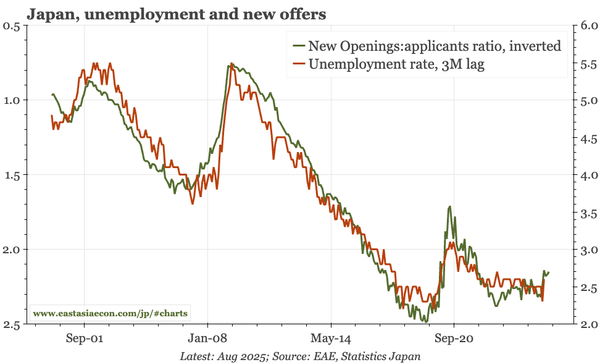

Korea – employment perks up

Employment bounced in September, providing more evidence of cycle bottoming. That shouldn't matter much for BOK thinking: in July it raised employment forecasts, and has expected recovery into 2026. I am sceptical that recovery runs far, but there are upside risks if business sentiment improves.