Subscribers Only

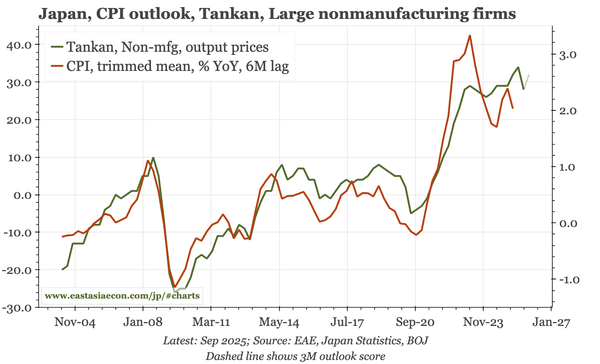

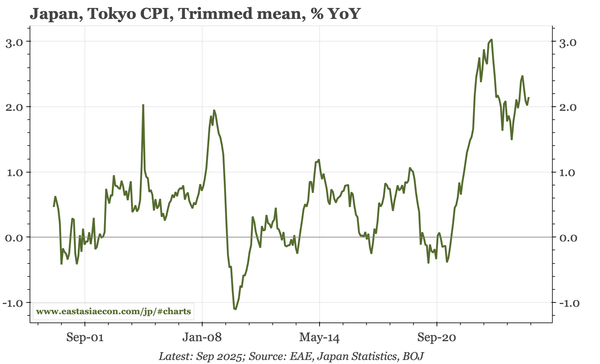

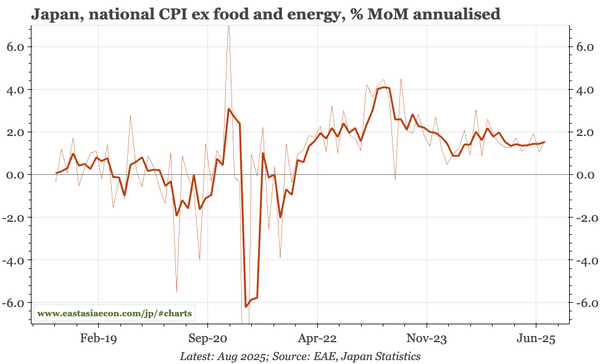

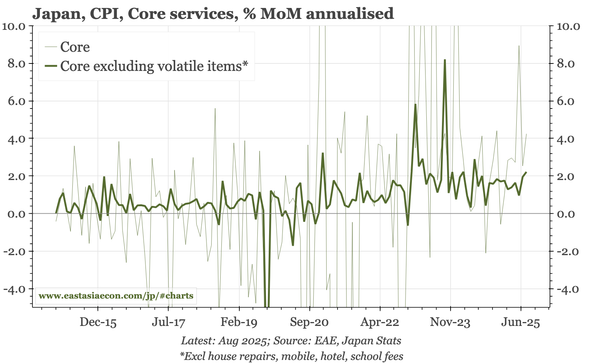

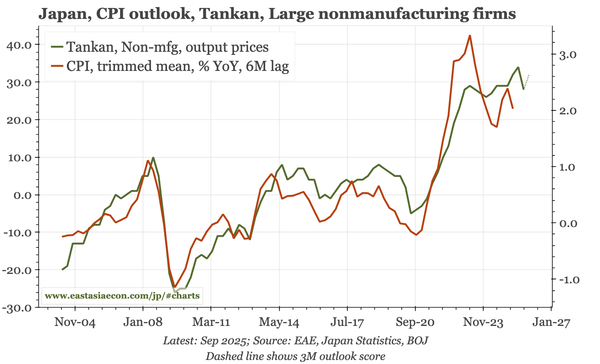

Japan – "underlying" inflation still tacking at 2%+

Inflation indicators in yesterday's summary release of the Tankan were already firm. Today's comprehensive release paints a picture that is stronger still. The implication is that one of the BOJ's older measures of underlying inflation, the trimmed mean, is likely to remain above 2% for the next 6M.