Subscribers Only

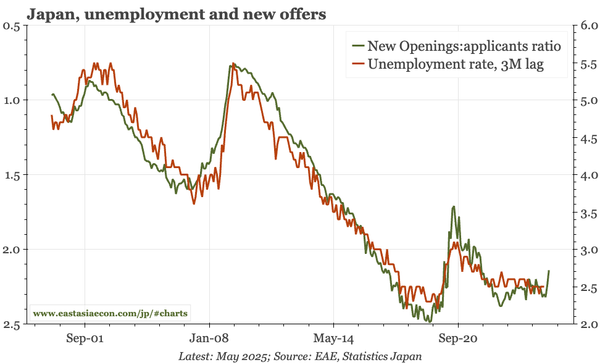

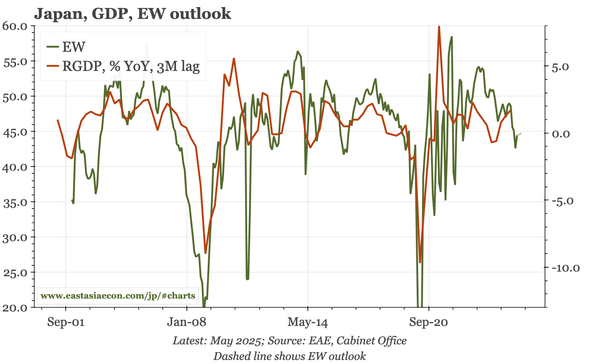

Japan – helpful rebound in consumer confidence

In recent months, Japan has encountered two headwinds: higher tariffs which threaten exports, and rebounding inflation which reduces consumer purchasing power. Inflation expectations eased in June, allowing consumer confidence to rebound. That is helpful in offsetting the pain coming from tariffs.