Subscribers Only

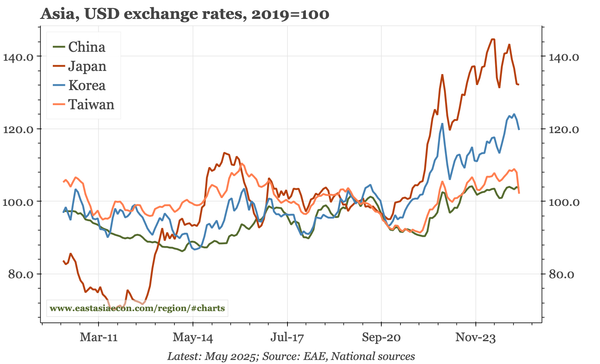

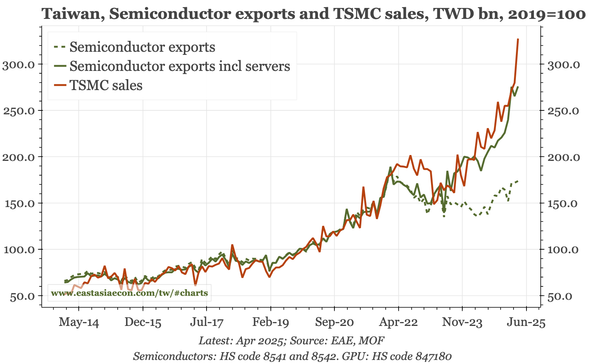

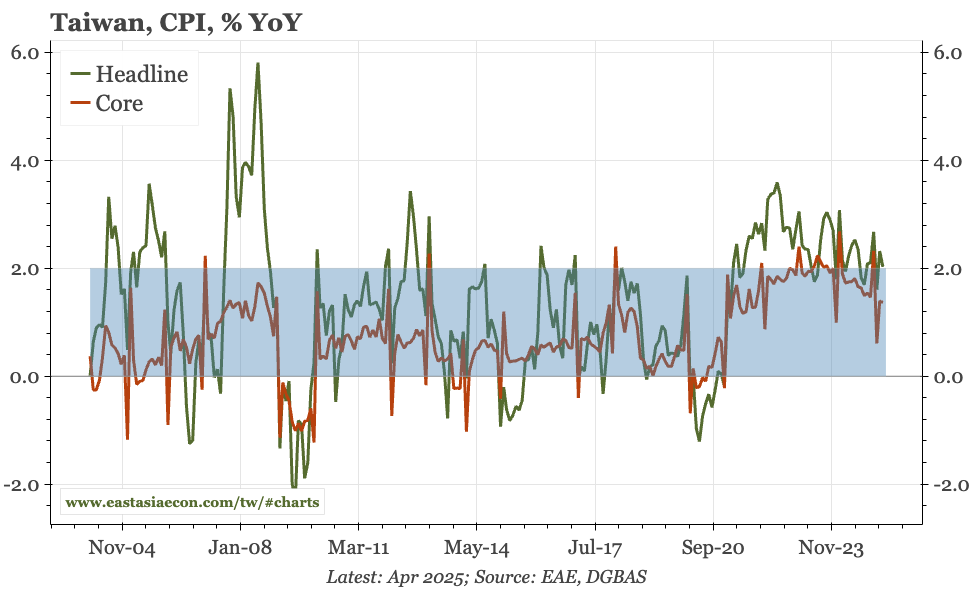

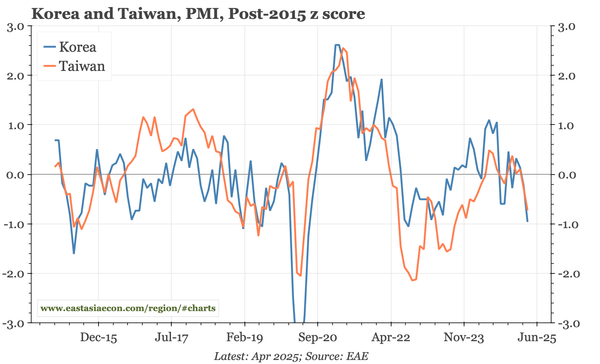

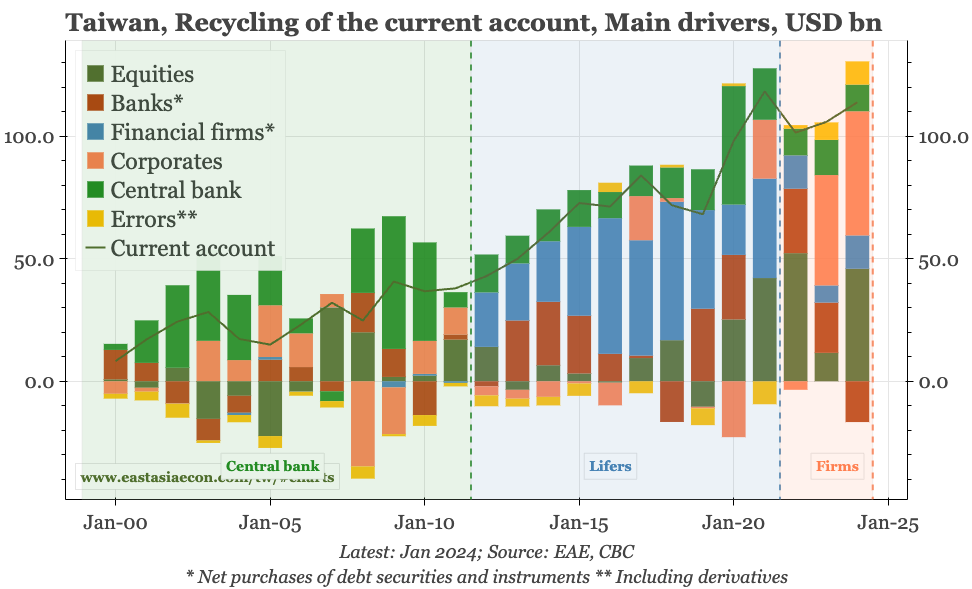

Taiwan – structure, cycle and the TWD

The market sees TWD moves as a function of US pressure and lifers. The CBC says it is all about exporters. I see a step-change in exports from 2020 that has ended deflation and exacerbated the CA surplus. The TWD consequences of that shift are stronger if US tariffs don't trigger a global recession.