Public Post

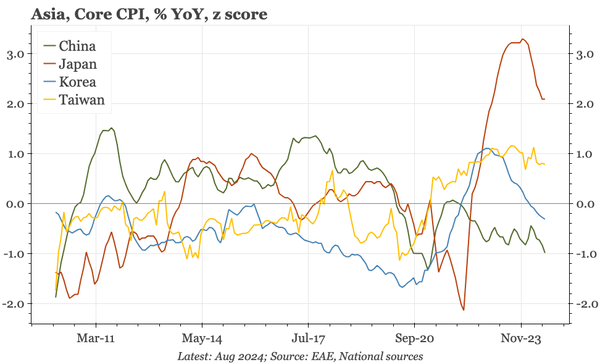

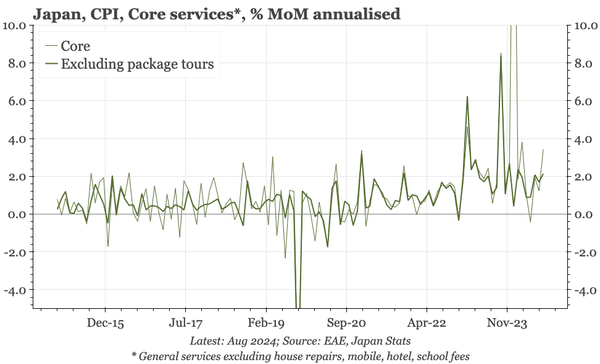

Japan – Tokyo underlying CPI stable

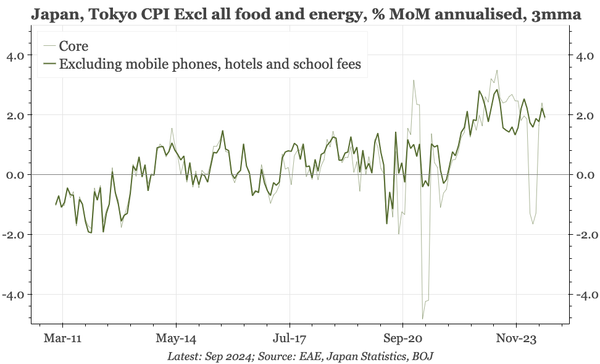

Underlying core inflation in Tokyo in September continued to run at around a 2% annualised rate. The trimmed mean has stabilised at a bit below that, and the proportion of rising items has ticked up. Inflation isn't accelerating, but there's no sign of a slowdown either.