Subscribers Only

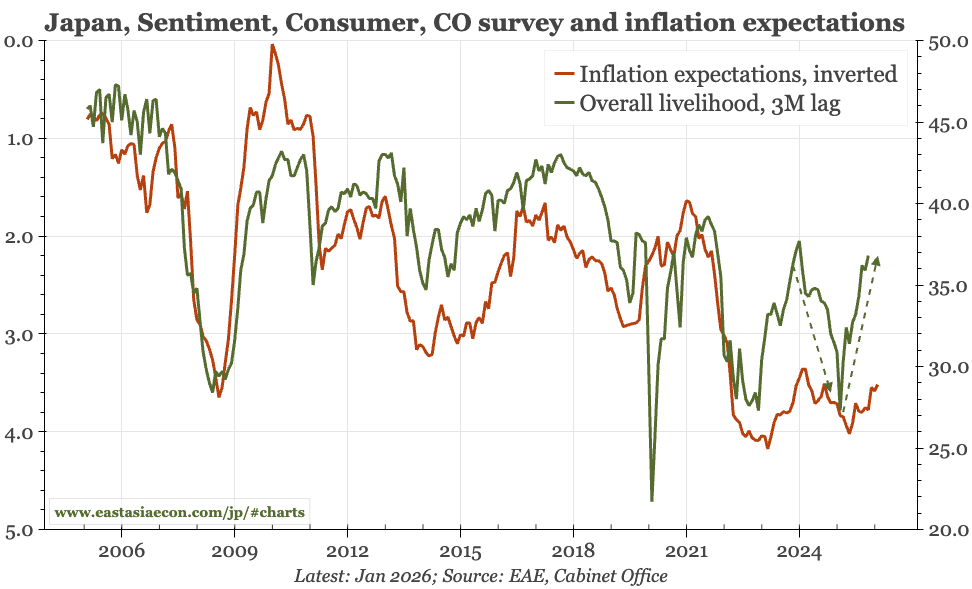

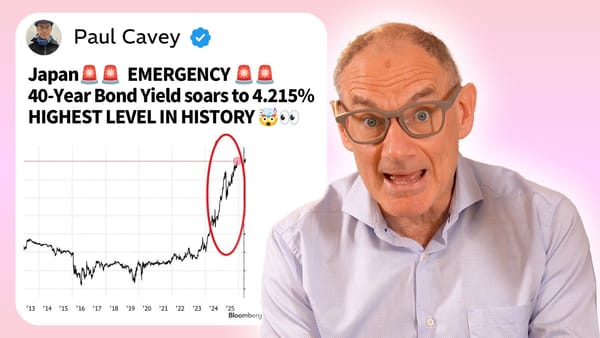

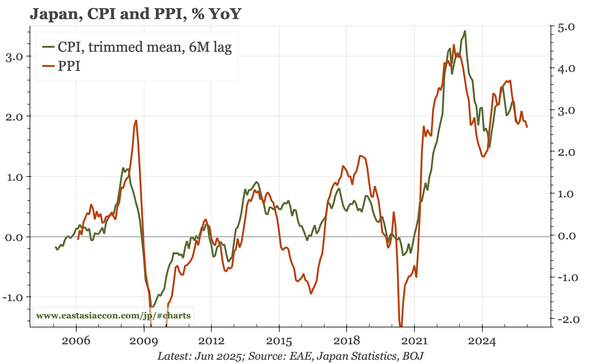

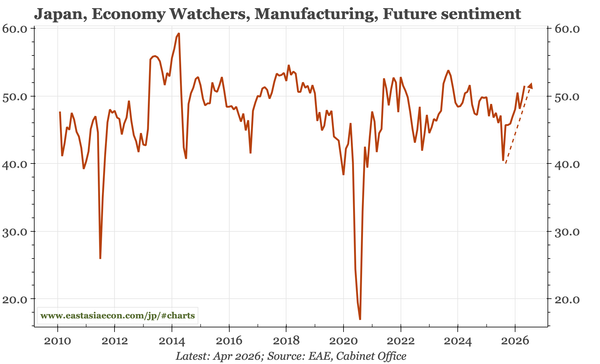

Japan – cycle still strengthening

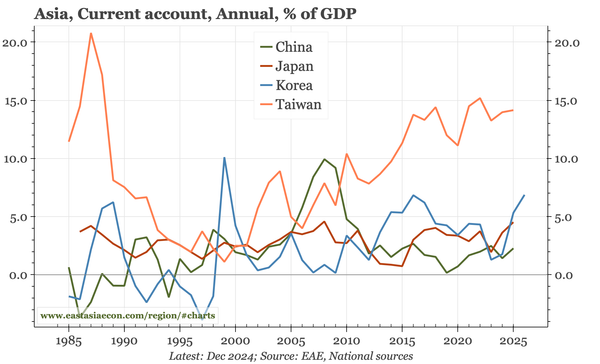

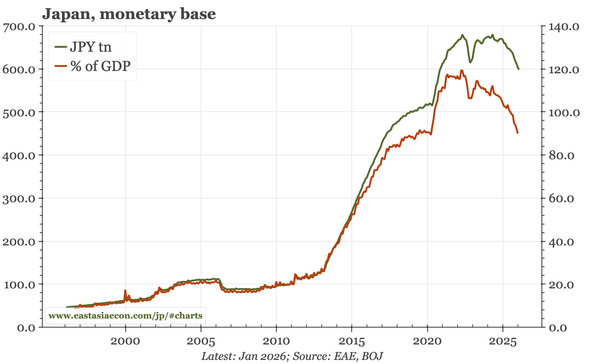

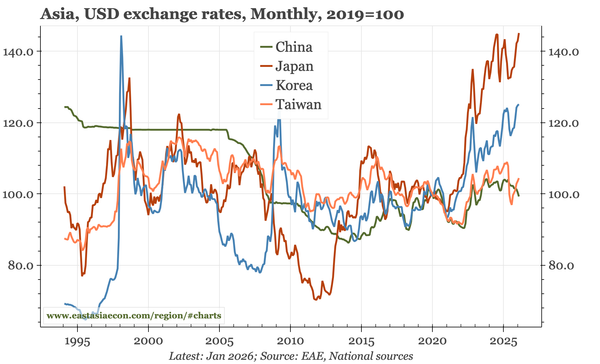

Takaichi's huge win comes when the cycle is looking stronger, with real wages close to rising, manufacturing sentiment improving and bank lending strong. This should give the BOJ confidence, and, with the current account surplus in 2025 reaching the highest level in forty years, also help the JPY.