Subscribers Only

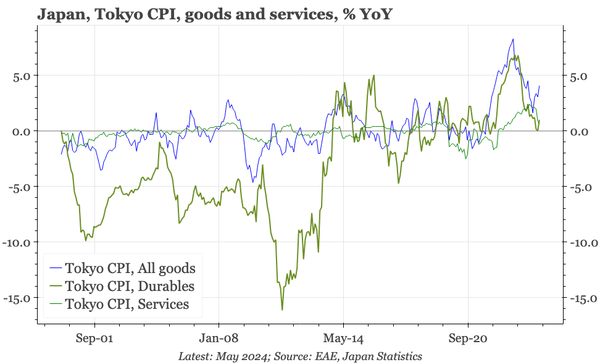

Japan – not data dependent

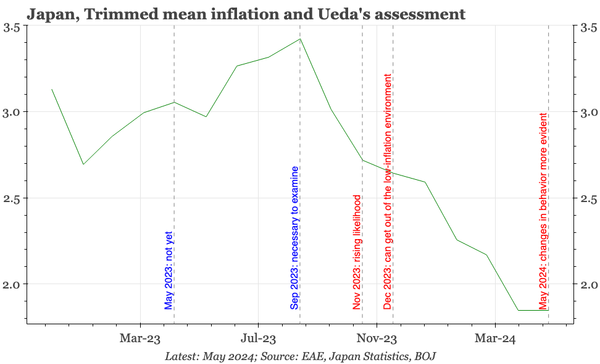

Of course, headline data matter. But not as much in Japan as elsewhere. Official data don't suggest a tightening economy, but in the last 6M, the BOJ has nonetheless become more confident that Japan is heading to sustainable inflation. We'd expect more rate hikes soon.