Public Post

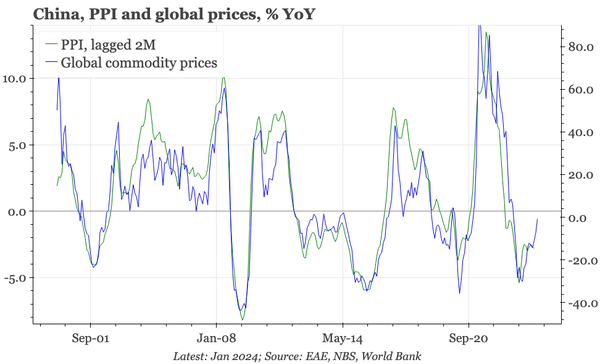

China – no inflection yet in PPI

China should be close to an inflection in PPI, but the turn didn't happen in March. PPI fell 2.8% YoY, a rate of deflation that hasn't changed much since August 2023.